Will You Miss the Boom of Digital Therapeutics? Insights from Jiang Tianjiao, 'Crystal Ball' Top Analyst

The Fourth Industrial Revolution is a transformation in social modes of production driven by technologies such as the Internet, the Internet of Things (IoT), big data, robotics, and artificial intelligence. At its core lies the deep integration of networking, informatization, and intelligentization. It represents another technological revolution, following the First Industrial Revolution characterized by steam technology, the Second Industrial Revolution represented by electrical technology, and the Third Industrial Revolution marked by computer and information technology.

History tells us that every industrial revolution has brought about profound, disruptive changes to the healthcare industry. Standing at the intersection of the Third and Fourth Industrial Revolutions, we can clearly see that the digital transformation of the healthcare sector is accelerating alongside continuous technological advancements. In 2020, the sudden outbreak of the COVID-19 pandemic further accelerated the digital revolution in China’s—and indeed the global—healthcare industry. The ongoing integration of digital technologies such as artificial intelligence (AI), big data, robotics, 3D printing, wearable devices, and virtual reality with medical technologies is driving the entire industry into a new landscape.

How Should We Understand the Future of Healthcare? What Will the Healthcare Industry Look Like in 2050? What Role Will Digitalization Play?Jiang Tianjiao, Dean of the Eggshell Research Institute, who has conducted in-depth research in the fields of digital health and healthcare services and whose team and he himself have won first-place honors and analyst awards from New Fortune and Crystal Ball, recently addressed and forecasted these issues in his public speech titled “Digital Health Revolution in Future Healthcare 2050.” VCBeat (WeChat ID: Vcbeat) has compiled his insights into this article for the reference of professionals.

Jiang Tianjiao, Dean of VCBeat.

Previously served as a Senior Analyst covering the Internet and Healthcare sectors at Founder Securities Research Institute. Was part of the first-place teams recognized by New Fortune and Crystal Ball for Best Analysts, and received individual analyst awards. Has conducted in-depth research in the fields of internet healthcare and medical services.

Formerly served as a Director in the Industrial Finance Department of Founder Securities, responsible for investment and M&A activities as well as market capitalization management in the healthcare industry;

Also serves as a Distinguished Researcher at the National Internet Research Institute, a Distinguished Researcher at the Institute of Public Policy of the Chinese Academy of Social Sciences, and a Distinguished Researcher at the School of Social Sciences of Tsinghua University;

He is the author of the books *Reconstructing Great Health*, *Internet Transformation: Decoding the Chinese Management Model*, and *Internet + Healthcare*.

The development of any industry requires behind-the-scenes driving forces such as technological innovation and the upgrading of consumer demand. For China’s healthcare industry, in addition to these factors, the ongoing transformation among payers is not only the most significant change in the industry model but will also serve as the dominant force driving future industrial development.

Over the past three decades, China has undergone a rapid transformation in its economic development model and society. Meanwhile, remarkable achievements have been made in the country’s healthcare sector. Since the launch of the new round of healthcare reform in 2009, China has basically achieved universal health insurance coverage, promoted the equalization of basic public health services, and established an essential medicine system. These measures have enhanced the accessibility and equity of healthcare services, substantially reduced child and maternal mortality rates as well as the incidence of infectious diseases, and significantly improved residents’ health status and life expectancy.

The current healthcare service system has significant limitations in its operational and incentive mechanisms. Administrative price controls have severely undervalued medical services, leading to a distorted hospital financing model known as “subsidizing healthcare with drug profits.” Consequently, medical professionals are compelled to boost hospital revenue through high-margin practices, including over-treatment, excessive prescription of medications, and overuse of medical devices.

Given that China’s healthcare system is overwhelmingly dominated by public institutions, and that health insurance reimbursement operates on a fee-for-service basis without effective cost-containment mechanisms, the medical service model has naturally evolved to be disease-treatment-centric. Under this model, any disease treatment can increase hospital revenue, whereas disease prevention has the opposite effect; consequently, prevention receives little attention.

Jiang Tianjiao believes that while this system can satisfy the interests of multiple stakeholders—including hospitals, physicians, distribution channels, and pharmaceutical companies—it is disconnected from medical value (as evidenced by the use of adjuvant drugs, overprescription, inadequate medical services, and substandard care). Ultimately, health insurance funds and consumers bear the actual costs, and the trend continues to deteriorate.

For several consecutive years, the growth rate of expenditures from the basic medical insurance fund has exceeded that of its revenues; without intervention, this trend will lead to the depletion of the fund’s reserves. However, population aging and a sustained decline in newborn births are profoundly reshaping the demographic age structure, rendering revenue expansion efforts unsustainable. Consequently, cost containment will become the central theme in the future management of the basic medical insurance fund.

The basic medical insurance fund has repeatedly emphasized its positioning as providing “basic coverage.” Since the establishment of the National Healthcare Security Administration, its interpretation of “basic” has become increasingly clear through concrete actions: “basic” is akin to “low-rent housing,” ensuring that everyone has access to essential care, whereas “commercial housing” corresponds to “improvement-oriented needs,” which should be borne by consumers themselves (through out-of-pocket payments or commercial insurance). This trend not only ensures the stability of the “basic coverage” foundation but also encourages the “middle class” to assume responsibility for their share of healthcare expenditures—namely, those associated with “high-quality demands” that go beyond basic needs.

As cost-containment measures such as DRG and DIP are vigorously implemented, with intensifying efforts in medical insurance cost control and an expanding scope of volume-based centralized procurement, the crowding-out effect of basic medical insurance will become increasingly pronounced. The healthcare service demands that basic medical insurance fails to meet will be supplemented and absorbed by commercial health insurance, thereby creating substantial growth opportunities for the commercial insurance sector.

Jiang Tianjiao believes that the following trends will persist in the long term: First, centralized volume-based procurement (VBP) under the national medical insurance scheme and cost-containment measures will continue, steadily squeezing out inflated profits from high-volume product categories. The intensity of medical insurance cost control will further increase, exceeding expectations. Concerns that “VBP fails to incentivize industry innovation” are unfounded. Historically, the traditional pharmaceutical industry has rarely allocated its super-normal profits toward innovation, whereas capital markets and policy initiatives have already demonstrated significant momentum in driving technological advancement. Going forward, the state can more efficiently support innovative enterprises through targeted policy and financial incentives.

Secondly, the habit of supplementing high-quality, upgrade-oriented, and niche medical needs through commercial health insurance or out-of-pocket payments is gradually being established. In the early stage, commercial health insurers will compete for market share with a diverse range of product offerings, where the core competitive factors are product development and marketing sales. Finally, once the market enters a phase of entrenched competition among existing commercial health insurers, the key competitive differentiators will shift to service quality and cost control.

Cost containment is the ultimate shared objective of both public health insurance and commercial insurers, fundamentally aimed at paying for genuine medical value. Effective cost control can be achieved through measures such as centralized procurement, fraud prevention, rational drug use, clinical pathways, improved therapeutic outcomes, and reduced disease incidence—all of which require and will long remain dependent on digital technologies.

In summary, the transformation of payers will significantly reshape the supply-side pricing, product offerings, and sales systems of traditional pharmaceuticals, medical devices, and hospitals, bringing about comprehensive changes in the industry’s competitive landscape, key competitive factors, and profit models. For this reason, it will become a pillar force driving industry transformation over the next 30 years.

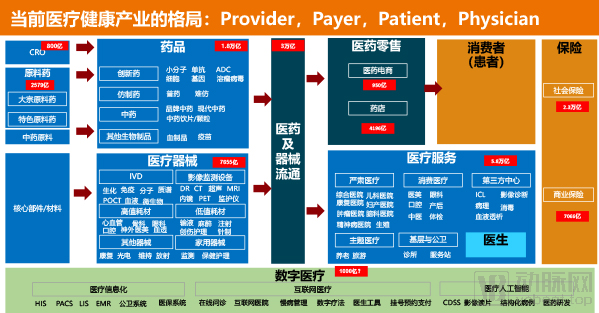

Traditionally, the various participants in the healthcare industry can be categorized into four segments: pharmaceuticals and medical devices, payers, patients, and physicians (or hospitals).

As the name suggests, the pharmaceutical and medical device sector is divided into two segments: pharmaceuticals and medical devices. In the pharmaceutical segment, the upstream of the industry chain comprises CRO services and various active pharmaceutical ingredients (APIs), followed by finished drug products, which ultimately reach patients through diverse distribution channels and are reimbursed by corresponding payers.

Based on different economic characteristics, the finished drug industry, with a market size of up to 1.8 trillion yuan, can be divided into innovative drugs, generic drugs, traditional Chinese medicines, and other biological products including blood products and vaccines.

For instance, the research and development (R&D) of innovative drugs resembles a pipeline-based betting mechanism, necessitating rational portfolio allocation. This process demands substantial time and resources in the early stages; if R&D lags behind competitors or fails to advance to the next clinical phase, the investment is entirely lost. In contrast, generic drugs depend more on product selection and inclusion in the National Reimbursement Drug List (NRDL).

The classification of medical devices is also relatively clear, ranging from upstream core components to mid- and downstream equipment, such as large-scale imaging systems or other diagnostic devices, as well as high-value consumables, low-value consumables, other medical devices, and home-use devices. These products are delivered to patients through specialized channels via physicians or healthcare institutions.

It is worth noting that, compared with the finished drug market, China’s medical device market is significantly smaller—with a market size of approximately RMB 765.5 billion, less than half that of finished drugs. By contrast, the ratio of the medical device market to the finished drug market in the United States remains roughly at 1:1.

Jiang Tianjiao believes that disparities in medical technology are one of the key factors contributing to the difference in market size between China’s and the United States’ medical device and finished drug markets: “Why is China’s medical device market so much smaller than its pharmaceutical market? The use of medical devices requires significantly more extensive physician training than prescribing medications.”

“Of course, with the advancement of medical technology in China, the improvement of doctors' skills, and the surge in demand for home medical devices among the general public, the scale of China's medical device market is expected to see significant growth in the future,” Jiang Tianjiao added.

Based on distinct economic characteristics, healthcare providers can be categorized into serious medical care, consumer-oriented medical care, specialized thematic medical care, primary public health services, and third-party centers. Within the traditional ecosystem, physicians practice within healthcare institutions. However, with societal development, independent medical practice by physicians is gradually becoming more prevalent.

The vast majority of these services are covered by basic medical insurance, with patients bearing the remaining out-of-pocket costs. Currently, only a small fraction is covered by commercial health insurance.

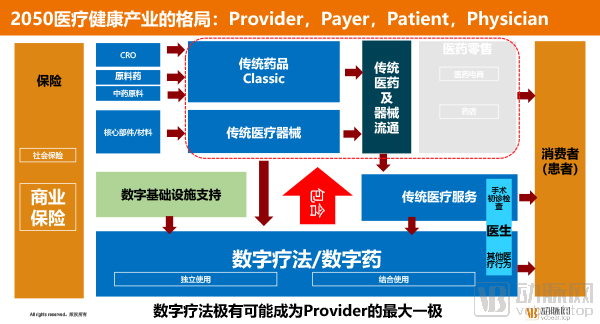

In traditional panoramic views, the positioning of digital health has been somewhat ambiguous—ubiquitous yet seemingly marginal. However, with reforms among payers, digital health is poised to emerge as a distinct pillar, assuming an increasingly important role in the future. “Digital therapeutics, digital drugs, and digital health may evolve into independent entities within this industry,” stated Jiang Tianjiao.

So, what exactly is digital therapeutics? Digital therapeutics (DTx) are software-based therapies that provide patients with evidence-based therapeutic interventions to prevent, manage, or treat diseases.

Digital therapeutics can be used independently or in conjunction with medications, devices, or other therapies. These products integrate the latest advancements in design, clinical validation, usability, and data security, and are subject to regulatory review and approval as required. Digital therapeutics need to provide intelligent and accessible tools for patients, healthcare providers, and payers to address a variety of clinical scenarios.

Simply put, in the traditional system, patients obtain medications from pharmacies based on prescriptions issued by physicians. Digital therapeutics, however, merely replace the medication with a specific mobile application—though it may also involve integrated hardware and software products.

By definition, digital therapeutics have two major characteristics. First, digital therapeutics can be used independently. In the improvement of many mental disorders, digital therapeutics themselves serve as an intervention method, directly providing treatment through software-based interventions.

Clinical trials conducted over the past several years have demonstrated that digital therapeutics exhibit significant efficacy in managing behavior-mediated conditions that are not adequately addressed by conventional pharmacotherapy, such as depression, post-traumatic stress disorder (PTSD), smoking cessation, type 2 diabetes, and insomnia. For these conditions, traditional medication offers limited benefit and carries a high risk of drug dependence. The opioid addiction crisis plaguing the United States is one prominent example of the drawbacks associated with pharmacological treatment.

Secondly, digital therapeutics exhibit strong inclusivity and can be used in combination with pharmaceuticals and medical devices, often yielding greater efficacy than the use of either modality alone. By embedding medical instructions and subsequent procedural steps into standardized product workflows, digital therapeutics enforce patient adherence, thereby improving compliance with medication and device usage.

This holds immense appeal for traditional pharmaceutical and medical device companies. For this reason, these companies are strategically positioning themselves in the field of digital therapeutics to facilitate a transition from traditional pharmaceuticals and medical devices to digital-enabled counterparts. Consequently, Jiang Tianjiao believes that digital therapeutics have the potential to emerge as a distinct pillar, playing a highly significant role within the pharmaceutical and medical device industry.

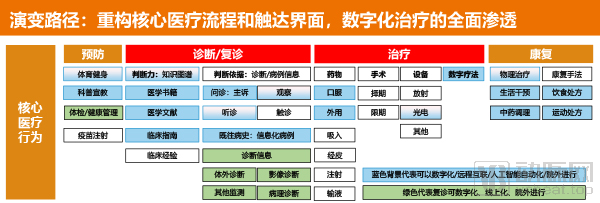

With the rise of internet-based healthcare, the role of physicians is also shifting. Apart from surgeries and diagnostic tests that must be performed in hospitals, nearly all other medical services can be conducted online.

Depending on the disease type, this transition can be categorized into three scenarios: First, if diagnosis relies primarily on medical consultation, and treatment depends mainly on oral medications, topical agents, and digital therapeutics, the entire process can be fully conducted online. Second, if diagnosis can be completed through medical consultation, review of medical records, and data from home-use devices, and treatment relies on oral medications, topical agents, and digital therapeutics, full online delivery is ultimately achievable. Third, if surgical intervention is required, the treatment phase is difficult to conduct online, while other phases can be gradually migrated to online platforms.

Therefore, in the future, more physicians may not practice exclusively within traditional healthcare institutions but will instead become key providers of digital therapeutics and digital pharmaceuticals. This will represent a significant transformation.

As payer reforms deepen, digital therapeutics (DTx) and digital drugs will see further development. Compared with traditional pharmaceuticals and medical devices, DTx offers the advantage of lower costs and superior efficacy. Meanwhile, driven by cost-containment pressures and the demand for higher quality of care, digital technologies such as artificial intelligence will be increasingly implemented in clinical practice.

Digital therapeutics will revolutionize access models, with online digital platforms emerging as the “new frontier” of the healthcare industry. They will also transform engagement dynamics, shifting from one-off interactions to sustained user stickiness. Furthermore, digital therapeutics will redefine intervention strategies, moving beyond pharmaceutical prescriptions to comprehensive, multi-modal interventions across the entire disease course, thereby productizing solutions (including prescriptions, medical orders, and follow-up care). Academic influence will likewise shift, transitioning from being anchored in individual experts to being embedded in products (i.e., the productization of expert knowledge).

For pharmaceutical and medical device companies, digital therapeutics will reshape the competitive landscape. By enhancing patient stickiness, digital therapeutics make “switching medications” no longer easy—thus becoming a new dimension of competition. The accumulation of doctors, patients, historical data, and information creates significant switching costs. Digital therapeutics will serve as a core enabler. Only by accumulating data around treatment can one fully penetrate and empower all elements of the healthcare industry.

Finally, digital therapeutics will emerge as a new, yet easily overlooked, battlefield. The primary development strategies of mainstream pharmaceutical companies include pipeline portfolio construction, mergers and acquisitions of product lines and regional markets, extension of the industrial chain into active pharmaceutical ingredients (APIs), complex generics and formulation modifications, and channel collaborations driven by internet-based platforms. Currently, market-wide awareness of the significant importance of digital therapeutics has not yet been ignited.

For this reason, digital therapeutics will hold significant importance.

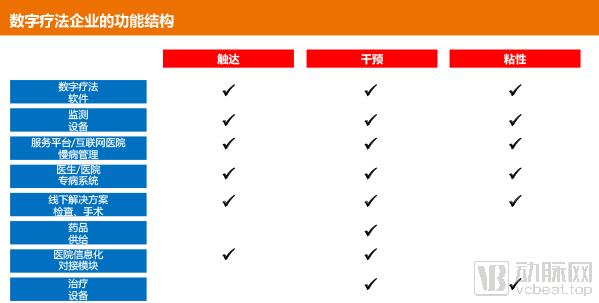

So, what functional modules should digital therapeutics companies possess? Jiang Tianjiao believes that, based on the goal of “reach-intervention-stickiness,” digital therapeutics companies should include digital therapeutics software, monitoring devices, service platforms/internet hospital chronic disease management, doctor/hospital specialized disease systems, offline solutions (examinations, surgeries), drug supply, hospital information system integration modules, and therapeutic devices.

First-mover advantage, data accumulation, product efficacy, channel marketing, patent protection, and academic influence will become the key competitive factors in the future of digital therapeutics.

Traditional pharmaceutical and medical device companies can enter the digital therapeutics market through partnerships, equity investments, mergers and acquisitions, or in-house development. Each of these approaches has its own advantages and disadvantages, making them suitable for companies at different stages of strategic deployment.

If the project is in its early stages, lacking a foundational base and facing high difficulties in talent acquisition and organizational setup, with limited visible results and ineffective incentives, it is advisable to gain extensive understanding of the project through collaboration and gradually identify key elements, while ensuring comprehensive coverage of the project pipeline.

Digital therapeutics companies ultimately require extensive healthcare networks for market promotion, creating strong demand for partnerships with traditional pharmaceutical firms. Traditional pharmaceutical and medical device companies can secure equity stakes to lock in specific pipeline products and provide empowerment. At this stage, broad screening is feasible.

Furthermore, traditional pharmaceutical companies can select targets with the highest strategic fit, strongest performance, and greatest potential for mergers and acquisitions (M&A). Meanwhile, maintaining a diverse pipeline of alternative targets can enhance their negotiating leverage in M&A transactions.

Following the acquisition of the target company, we will progressively enhance organizational structure, talent reserves, and incentive mechanisms in the digital therapeutics sector to facilitate subsequent replication and in-house development centered on our core strategic logic.

In the development of the digital healthcare industry, strategic adjustments must be made in a timely manner based on different value distributions. These dimensions include the value distribution across departments/disease types, the value distribution along the industry chain, the value distribution by geographic region, the value distribution by institutional hierarchy, the value distribution by service attributes, and the value distribution between Traditional Chinese Medicine (TCM) and Western medicine.

Distribution of Value Across Departments and Disease Types: Changes in the value distribution across departments and disease types may arise from factors on the demand side, such as shifts in disease spectra, and factors on the supply side, including advancements in medical devices, pharmaceutical technologies, and changes in their application methods.

Value Distribution Across the Healthcare Industry Chain: Driven by shifts in industrial policy, technological breakthroughs, and changes in demand and channel interfaces, the value distribution across the entire healthcare industry chain is continuously evolving.

Geographic Distribution of Regional Value: The distribution of regional value is continuously evolving due to factors such as medical insurance reimbursement policies, endowments of healthcare resources, disease characteristics and lifestyle habits, and changes in regional policies.

Value Distribution Across Institutional Tiers: Top-tier Grade A tertiary hospitals possess both existing and evolving value. The trend of shifting influence toward private healthcare providers may drive changes in value distribution, while policy support and business model innovations in primary care could lead to subtle shifts in the hidden value landscape at the grassroots level.

Value Distribution of Service Attributes: Serious healthcare, consumer healthcare, and health services belong to different service tracks, characterized by distinct value distribution patterns, industry growth rates, and return on investment, thereby creating potential business opportunities at any time.

Value Distribution of TCM vs. Western Medicine: As a unique healthcare offering, Traditional Chinese Medicine (TCM) possesses distinct advantages in terms of cost, patient acceptance, heritage, and exemption from clinical trials.

In terms of commercialization pathways, the landscape includes 2H (Hospital – hospital information systems, driven by political performance requirements and profit motives), 2G (Government – government-regulated tendering and procurement markets), 2B (Business – corporate health markets), 2I (Insurance – health insurance markets), 2D (Doctor – business opportunities based on physicians’ needs), 2P (Pharma & Medtech – business opportunities along the pharmaceutical and medical device value chain), and 2C (Consumer – personal consumption segments such as dentistry, ophthalmology, and medical aesthetics, as well as common diseases).

Jiang Tianjiao believes that the key to identifying a suitable commercialization path lies not in achieving breakthroughs at isolated points, but in cultivating “kill-two-birds-with-one-stone” business stickiness.

Taking Pear Therapeutics, a leading company in digital therapeutics, as an example, several of its currently commercialized products in the R&D pipeline target substance use disorders, primarily addressing opioid misuse and chronic insomnia. Its product Discovery, currently undergoing clinical validation, focuses on pain management and aims to address multiple conditions simultaneously, including irritable bowel syndrome, pain, post-traumatic stress disorder, migraine, bipolar disorder, epilepsy, gastrointestinal disorders, and oncology-related indications, which are at various stages of development.

Digital therapeutics are rapidly gaining momentum, both in China and abroad. In 2020, the U.S. FDA eased emergency authorization requirements for certain digital therapeutics, a policy change that had a positive impact on the field. Shortly after its implementation, several digital therapeutic products received emergency authorization and became available to the public. This development signifies another acceleration in the already burgeoning growth of digital therapeutics overseas.

Meanwhile, digital therapeutics in China have also achieved a breakthrough, with the National Medical Products Administration (NMPA) issuing the first registration certificate for an internet-based medical device targeting cognitive impairment. A review of the development history of digital therapeutics in the United States leads to a clear conclusion: digital therapeutics are poised for explosive growth in China.

“Digital therapeutics is by no means as simple as obtaining software certification! If you view digital therapeutics from this narrow perspective, you may fail to grasp the subsequent logical implications, thereby missing out on this wave of innovation.” Standing on the brink of transformation, are you ready?