Capital Winter Can't Stop the Surge in Healthcare: Top VC Insights Reveal 2021’s Hottest Medical Tracks

With the conclusion of the Spring Festival, 2020 has come to a complete end.

Everything the healthcare industry experienced in 2020 was akin to Barcelona’s magical Sagrada Família, which broke ground during a capital winter and took shape in an unpredictable manner.

In our interviews and surveys with leading healthcare venture capital firms such as Sequoia Capital, Shenzhen Capital Group (SCGC), CDH Investments, Sato Capital, and Yuansheng Venture Capital, we observed that healthcare investments in 2020 witnessed many dramatic shifts due to the high uncertainty characteristic of the VUCA era. Nevertheless, the industry continued to grow rather than stagnate. The outbreak of COVID-19 exposed the vulnerabilities of the traditional healthcare supply chain, while further underscoring the sector’s foundational role in safeguarding societal operations. Consequently, in the second half of the year, as the initial wave of the pandemic was brought under control and new growth drivers—such as “new infrastructure” initiatives—were strongly injected into the economy, the healthcare industry experienced a robust surge in investment activity.

Our research focuses on what precursors for the changes in 2021 were laid in 2020, what new variables were introduced, and how these variables might manifest.

Data shows that the overall market size of China's public healthcare sector was approximately RMB 8 trillion in 2019. Ten years later, in 2029, the industry’s scale is projected to reach RMB 16 trillion, with its asset base surpassing that of the real estate sector to become the largest industry. Undoubtedly, 2020 marked the inflection point for growth in this transition.

What Major Changes Did Frontline Healthcare Investors Perceive in 2020? How Did They Address the Challenges of 2021? In seeking answers to these questions, VCBeat interviewed institutional investors. It is worth noting that most respondents have over a decade of experience in the healthcare investment sector, boasting extensive expertise in financing and investment. Their track records include involvement with healthcare companies that have achieved market capitalizations in the hundreds of billions. Moreover, they maintain a strong curiosity about the industry and remain diligently active on the frontlines.

To showcase our insights from both macro and micro perspectives, this article presents this feast of ideas in two parts: “Part I: Macro Outlook” and “Part II: Analysis of Specific Sectors.”

001. Bracing for a Harsh Winter, Only to Encounter an Industry Boom

In 2020, the industry, poised to brace for a harsh winter, instead welcomed a booming market.

According to statistics, there were more than 260 investment and financing events in the medical field in 2020, with 66 companies going public. Among the top 10 companies by funds raised on the A-share market, six were innovative drug R&D enterprises. In this moving feast, everyone wants to get a share.

In certain hot sectors, a frenzy for projects has erupted. One investor quoted a saying: “It’s like a pack of wolves charging onto burning coals—nothing but sheer madness.”

Some investors have pointed out that in sectors such as cardiovascular intervention, neurointervention, and sports medicine, company valuations have far exceeded the projected upper limit of the total addressable market for these entire sectors. Yet even in these areas, projects still attract fierce competition among investors.

Taking neurointerventional devices, the hottest niche segment in the medical device industry in 2020, as an example, valuations of popular projects have reached levels that many top-tier venture capital firms find unacceptable and thus cannot participate in. “We recognize the value of these projects, but we cannot accept their valuations. This metric has risen repeatedly during the decision-making process, ultimately reaching a point where we are no longer able to invest.”

Soaring valuations and fierce competition for deals may be the norm in the TMT sector, but they represent a rare anomaly unseen for years in the healthcare industry, a field traditionally known for its stability. In 2020, investors who had identified promising companies found they could no longer afford to wait, as corporate valuations tripled within just two months. Even under such circumstances, they felt compelled to grit their teeth and invest.

What warrants our caution, however, is that the true driver behind this surge is not any epoch-making technological or business model innovation within the industry. Rather, the primal force fueling this frenzy stems from fluctuations in market sentiment—more precisely, from the secondary market, including the spillover of investor sentiment and changes in listing policies.

Dr. Liu Dan, Partner at CDH Investments’ Innovation and Growth Fund, stated: “The capital frenzy in 2020 was linked to the spillover of sentiment from the secondary market to the primary market, a highly specific factor for that year. The outbreak of the COVID-19 pandemic in early 2020 brought society to a standstill, leading to generally low expectations for economic and social development; consequently, most investors adopted a wait-and-see approach or held pessimistic views. As the pandemic came under control, the response efforts served as a window that highlighted the value of the healthcare industry. It drew greater attention to the significant progress China had made in biomedical technologies—particularly in testing and inspection, vaccine R&D, and new drug development—demonstrating the potential to compete with international peers. This led to enthusiastic investor interest. Moreover, the rising sentiment in the secondary market quickly transmitted to the primary market.”

Another major driver of the healthcare market’s surge last year was the green light given to exit channels in the secondary market,Whether on the STAR Market, the Hong Kong Stock Exchange, or the A-share market, a large number of healthcare companies have gone public, becoming the main force in initial public offerings (IPOs) and providing effective exit channels for primary market investments. As a result, a total of 71 healthcare projects were listed throughout 2020, with a combined IPO market capitalization of RMB 1.56 trillion. Among these, 42 biotechnology companies and 20 medical device companies were listed.

From a global perspective,Some investors also emphasized the impact of capital liquidity.。

Cao Yibo, Managing Director at Sequoia China, stated, “In 2020, abundant global liquidity, the strategic influx of substantial non-sector-specific capital, and smooth exit channels all encouraged funds to invest more aggressively in the healthcare industry, leading to a significant rise in both the number of deals and the total investment amount across the sector.”

Zang Jialun, Managing Partner and Head of China at Sidao Capital, pointed out: “From a funding perspective, USD-denominated funds have relatively ample capital, driven by abundant USD liquidity and the upswing in the U.S. capital market. In terms of RMB-denominated funds, liquidity has also improved to some extent. Moreover, as national and local governments place greater emphasis on the development of the healthcare and biotechnology industries, substantial capital has flowed into this sector, all of which has heightened enthusiasm for healthcare investment.”

It is evident that these factors did not undergo significant changes in 2021; therefore, the healthcare sector’s strong momentum is expected to persist.

First, the fact that the pandemic has not fully subsided will further increase the weighting of the healthcare sector in overall asset allocation. Leading healthcare-focused funds will attract more capital injections, while government-guided funds and corporate strategic investors will continue to expand their presence in the healthcare industry.

Secondly, in the secondary market, the surge in healthcare IPOs is unlikely to subside quickly. Furthermore, the robust performance of the healthcare sector in the secondary market over the past year will serve as a catalyst for further growth in the valuations of healthcare startups. The IPO boom will continue in 2021.

Once the green light for IPOs is given, the first wave of companies will be relatively larger and more mature. Subsequently, smaller yet higher-quality enterprises will also enter the capital markets.

The surge in IPOs has had a profound impact, primarily blurring the boundaries between primary and secondary market investments.

Cao Yibo of Sequoia China pointed out: “The STAR Market and the Hong Kong Stock Exchange have provided healthcare companies with a wave of securitization opportunities, leading to a large number of companies going public. However, in the new cycle, listing should be regarded merely as an honor; the core of investment lies in capitalizing on growth. As securitization expands among enterprises, significant opportunities will also emerge among already-listed companies. Therefore, whether investing in the primary or secondary market, the focus remains on the company’s long-term development.”In the U.S. market, many specialized healthcare investment firms apply nearly uniform criteria to select investment targets across both primary and secondary markets.”

Secondly, from a longer-term development perspective, the secondary market will also experience polarization.

The trend toward secondary market differentiation was already emerging in the Hong Kong stock market, which introduced Chapter 18A in 2018. This policy allows pre-revenue biotechnology companies to list publicly. Since its implementation, more than 20 unprofitable biotech firms have gone public, with many innovative pharmaceutical companies at early Phase II clinical trials becoming listed entities on the secondary market. However, the harsh reality is that numerous companies have seen their share prices fall below the initial public offering (IPO) price. For example, Ascletis Pharma was valued at USD 738 million after a financing round in late 2016, yet its market capitalization stood at only around HKD 3 billion two years after its Hong Kong listing.

Zhou Yi, Partner at Shenzhen Capital Group’s Healthcare Industry Fund, stated, “The secondary market will exhibit increasing polarization in the future. Companies lacking competitive advantages and core competencies will inevitably experience post-IPO share price declines, and may even face valuation inversions. Investors must adopt a consistent investment mindset across both primary and secondary markets, gaining a profound understanding of their convergence and interlinkage.”

One direction that warrants attention is that, due to the large number of companies going public,Mergers and acquisitions among listed companies will also occur frequently in the future.. Mergers and acquisitions (M&A) are driven by two factors: first, listed companies have a need for organic growth; second, as consolidation increases within China’s pharmaceutical industry, “big fish eating small fish” M&A activities will occur more frequently.

The sudden surge in the medical investment market warrants caution. Amidst rapidly evolving technologies and ever-refreshing IPO and financing figures, it may be difficult for both investors and entrepreneurs in the industry to discern how much of this prosperity is fueled by bubbles.

002. Foam: It Is Merely an Essential Component of a Glass of Beer

We define a bubble as a sector-wide surge in collective enthusiasm that drives corporate valuations beyond their intrinsic value.

Is there a bubble in healthcare investments in 2020? Regarding this question, VCBeat received almost unanimous affirmative responses during its research.

Some investors have bluntly stated that in 2020, bubbles emerged to varying degrees in sectors such as vaccines, medical devices, innovative drugs, and diagnostics, with valuations deviating from fundamentals. The most significant bubble was in the vaccine sector, followed by medical devices, and then innovative drugs and diagnostics. The surge in interest in the vaccine sector was largely driven by the impact of the novel coronavirus, while the concentration of capital in the medical device track resulted from a limited number of comparable companies in the secondary market and a scarcity of high-quality targets in the primary market.

How Do Bubbles Form and Ferment? Cao Yibo of Sequoia China stated, “Bubbles in the healthcare sector are concentrated in multiple areas. In one scenario, leading companies hold a dominant industry position, and investors share highly consistent views and perceptions. Among these investors, institutions with lower capital costs and return expectations have driven up the valuations of these leading enterprises. In another scenario, certain hot sectors, despite significant uncertainties, have become trending topics due to successful overseas benchmarks or substantial market potential. With many institutions participating, those with higher risk appetites have stepped in, causing valuations to rise sharply.”

While acknowledging the existence of a bubble, most investors view its value to prosperity with a positive mindset. Compared to the capital winter of 2018, a bubble is preferable to industry stagnation; it is an essential ingredient in a good beer.

Zang Jialun of STOB Capital stated bluntly: High valuations of companies in the healthcare sector are a concern for the market, but to some extent, bubbles at least make the industry appear prosperous, and the traditionally conservative healthcare industry needs them to inject vitality. Moderate bubbles help startups attract talent and provide research-intensive companies, which require substantial investment, with sufficient resources to realize their strong growth momentum and development potential. From a historical perspective, the existence of bubbles has certain value.

Investors’ acceptance and tolerance of bubbles are also steadily increasing,More people believe that amid the rapid development of China’s healthcare industry, the likelihood of bubbles solidifying is greater than the probability of their bursting.

Investment institutions are able to tolerate the current bubble because they believe in the rapid development of China’s healthcare industry. They hold that the present investment bubble can be absorbed amid the sector’s high-speed growth, given the vast capacity of the Chinese healthcare market and the sufficiently inelastic future demand. From a longer-term perspective, the current bubble remains within a controllable range.

Liu Dan of CDH Investments offered an analogy: “It’s like pouring a glass of beer; some foam on top is unavoidable. As long as what we mostly get to drink is beer, with just a bit of foam to adjust the taste, that is acceptable.”

However, bubbles have two sides: high valuations signify prosperity but also constitute the risk component of a speculative gamble. Concerns about bubbles manifest at both the industry and corporate levels. For companies, excessive bubbles and inflated valuations can severely overdraw future growth potential, thereby escalating risks.

Cao Yibo of Sequoia China stated, “Fundamentally, the valuation of healthcare companies is not based on their existing assets, but rather reflects expectations for the future development of their product pipelines. Companies vary in their ability to absorb valuations inflated by market hype; those unable to meet excessively high growth expectations face the risk of a bubble burst.”

For the healthcare industry as a whole, bubbles can also lead to a misalignment in its developmental trajectory. In an interview, Zang Jialun of F-Prime Capital highlighted the potential for “bad money to drive out good.” While high-quality companies that appear overvalued due to bubble conditions may actually be undervalued, the industry will regress if an increasing number of firms excel at fundraising but fail to create real value. Although a boom in venture capital investment can foster medical innovation, excessive prosperity may also result in homogeneous competition.

For investors in the industry, a bubble is also like a passing storm, testing whether their resolve is firm enough.

A seasoned investor remarked, “Many projects in 2020 left me deeply conflicted. The essence of investing lies in monetizing one’s insight and understanding. However, last year we encountered a widespread phenomenon: certain pre-revenue biotechnology companies needed a valuation of RMB 4 billion to meet the listing requirements of the STAR Market. Consequently, their pre-IPO valuations reached RMB 3.5 billion, enabling them to file for a STAR Market listing after raising RMB 500 million. Although these projects were not inherently worth RMB 3.5 billion, they had a high probability of successfully listing on the STAR Market, where their market capitalization could potentially soar to RMB 8–10 billion. In such scenarios, whether or not to invest poses a significant test of one’s investment values.”

Amid the risk of “bad money driving out good” in the industry, Zang Jialun from Sidao Capital stated that this situation severely tests investors’ independent judgment and sense of social responsibility. As investors, they should adopt a more prudent approach toward valuations, not only fulfilling their obligation to ensure a sufficient margin of safety for their investments but also actively shaping entrepreneurs’ valuation expectations, thereby safeguarding the healthy development of the entire industry.

What Did 2020 Change? Behind the Ever-Changing Figures, Perhaps the Greatest Change Was the Reshaping of Mindsets, and the Greatest Test Was a Test of Values.

What concerns us more is how the changes in 2020 will influence institutional investment moves in 2021. In this regard, VCBeat has compiled and organized an overview based on the major categories within the healthcare sector.

Innovative Drugs: The Era from Biotech to Big Pharma Has Arrived

Innovative drugs have been the earliest sector for domestic healthcare investment in China. Although China's biopharmaceutical industry has experienced several waves of enthusiasm, it has consistently remained in a catch-up phase.

Cao Yibo of Sequoia China stated, “The domestic pharmaceutical industry has experienced rapid development over the past two decades,”We have now entered a phase that combines imitation and innovation.The capabilities of China’s innovative pharmaceutical companies are continuously strengthening. Their “fast-follow” products have gained recognition from major overseas pharmaceutical firms, and “global-first” innovations are gradually emerging. The integration of imitation and innovation means there are still ample market opportunities. In the United States, where the biopharmaceutical market is relatively mature, it is nearly impossible for new Big Pharma companies like Pfizer to emerge, and it is difficult for biotech firms to grow into Big Pharma. However, in China, amid the major shift from generic drugs to innovative therapies, biotech companies still have the opportunity to evolve into Big Pharma if they chart the right course.

Selecting targets from the vast pool of biotech companies and accompanying them as they grow into big pharma places extremely high demands on the capabilities of investment firms. As one investor bluntly stated, “If everyone merely focuses on evaluating mature projects, that would be utterly foolish.”

How Investors Can Hunt for Promising Biotechs in the Increasingly Competitive Innovative Drug Sector

From a technical roadmap perspective, multiple institutions shared the directions they favor.

Zhou Yi stated that Shenzhen Capital Group (SCGC) favors companies with differentiated strategies, rich product pipelines, and strong synergies in the innovative drug sector. The firm also pays close attention to emerging technology platforms and technical service providers, such as those involved in gene therapy, cell therapy, nucleic acid drugs, and viral vector CDMOs. In the field of biotechnology, SCGC is optimistic about directions including gene editing, synthetic biology, and gene therapy.

Furthermore, VCBeat’s interviews revealed that key areas such as cell therapy, gene therapy, PROTAC technology, RNA-related technologies, AI-driven drug discovery, and breakthroughs in the mechanistic design of small-molecule K-RAS inhibitors have become common focal points for multiple investors.

Historically, these technologies were predominantly applied in the oncology field, which also served as the primary focus for innovative drug investment. In recent years, however, the sector has witnessed a clustering of efforts around oncology targets, leading to significant overcrowding in the oncology pipeline.

Regarding this phenomenon, Cao Yibo of Sequoia China stated, it is indeed reasonable for innovative drugs to focus on the field of oncology, as is the case in global innovative drug development; however, China’s focus is indeed more concentrated.The disease characteristics of cancer mean that current treatment standards remain suboptimal, leaving many unmet needs. Clinical trials in oncology typically require relatively small sample sizes and have shorter observation periods, leading to a faster return on investment. Furthermore, as cancers are often life-threatening conditions with direct implications for survival, patients’ willingness to pay is strong. Consequently, oncology has become the primary R&D focus for innovative pharmaceutical companies globally. In China, other major therapeutic segments prevalent in overseas markets—such as neurological disorders and autoimmune diseases—are not immediately life-threatening; thus, they have received insufficient attention from physicians and patients, and their development remains immature. However, with future economic growth and increased awareness, the distribution of innovative drug development in China will gradually shift from being heavily concentrated in oncology toward a portfolio mix more closely aligned with that of international markets.

Beyond oncology, more institutions are beginning to seek new opportunities. Therapeutics in ophthalmology, dermatology, central nervous system (CNS) disorders, and orthopedics have emerged as new focal points. Just as the rapid growth in oncology has been driven by the major technological breakthrough of tumor immunotherapy, progress in these fields similarly hinges on identifying opportunities for technological breakthroughs or industrial upgrading.

From the perspective of commercial competition, Sequoia China stated that it is more optimistic about products with competitiveness in mature markets for innovative drugs.

Cao Yibo stated, “In the field of innovative drugs, Sequoia China’s strategy has always focused on unmet needs and global competitiveness. We have consistently prioritized ultimate commercial value, and it appears that the most effective way to realize the commercial value of innovative drugs remains by unlocking their potential in the global market.”

may not fully align with the understanding of some other investors,Cao Yibo believes that the changes in medical insurance policies in recent years have demonstrated that pharmaceutical companies must face reality and abandon illusions regarding the Chinese market for innovative drugs. As a developing country, China’s drug prices must align with its payment capacity and economic conditions. Since medical insurance funds essentially derive from ordinary people’s wages and taxes, drug prices cannot exceed the nation’s economic strength.“Therefore, the primary battlefield for innovative drugs remains in mature overseas markets, which is why I place greater emphasis on products with global competitiveness. This does not necessarily mean they must be first-in-class; rather, they need to demonstrate sufficient differentiation and clinical value. Sequoia China favors ‘in China, for global’ enterprises that can leverage China’s advantageous resources to develop products with global competitiveness.”

CXO Boom: A Showcase of Global Competitiveness

Within the innovative drug industry chain, the CXO sector (encompassing pharmaceutical R&D services and customized manufacturing), which experienced a surge in 2020, warrants particular attention as a distinct segment separate from innovative drugs themselves.

CXO serves as the infrastructure of the innovative drug industry. The market is dominated by two leading players, WuXi AppTec and Tigermed. In the secondary market, the CXO sector has led the rally, with WuXi AppTec’s market capitalization exceeding RMB 400 billion. In the primary market, numerous top-tier investment firms interviewed by VCBeat have invested in multiple companies within the CXO sector. Data from VCBeat Orange Database’s “2020 Global Healthcare Industry Capital Report” shows that there were a total of 58 financing events in the research and development manufacturing outsourcing field, including 21 Series A rounds. This highlights the strong momentum in this sector.

From the perspective of external environmental changes, the surge in popularity of the CXO industry in 2020 was closely related to the pandemic. The global outbreak accelerated the shift of outsourcing services to China, thereby driving performance growth for CXO companies. From an endogenous standpoint, the ability of Chinese CXO enterprises to undertake global services essentially demonstrates their global competitiveness.

The heightened attention in the primary market stems from the role of CXO companies as “shovel sellers.” For every $100 invested in innovative drugs, approximately $50 flows into the CRO sector during early-stage R&D. Therefore, as R&D spending on innovative drugs increases and attracts more social capital, funds will theoretically shift correspondingly toward CXO enterprises.

Secondly, although there are leading players in the CXO sector, startups still have significant room for survival. In the CRO track, many niche segments offer opportunities to emerge as market leaders; WuXi AppTec, Pharmaron, and Tigermed collectively hold less than 30% of the market share, indicating substantial remaining space in the overall market.

The CRO sector offers substantial market potential, yet competition within this field is equally intense. To secure a foothold in the CRO market, companies must emerge victorious from fierce global competition.

CDH Investments has previously invested in several outstanding companies in the boutique CRO sector. Liu Dan stated that to succeed in this field, it is crucial to focus on three key aspects. First, a company must address industry pain points by helping pharmaceutical firms save time, improve success rates, or successfully validate unique models. It should not merely perform tasks for R&D enterprises or provide simple outsourcing services, but rather offer value-added services. Second, it must be capable of competing in service delivery on a global scale. Third, it must possess unique and formidable high-tech barriers. Only by leveraging distinct core technological advantages can a company remain competitive in the global landscape, deliver unique and valuable services, and secure a position in this highly competitive sector.

Medical Devices: A Year When Bubbles Begin to Accumulate

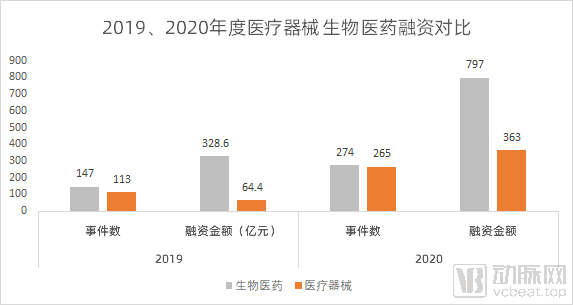

2020 can be described as the turning point year for medical device investment.

Historically, investment in medical devices has been relatively cautious due to the limited market potential of individual device products compared to pharmaceuticals. In 2020, the medical device and consumables sector attracted a total of RMB 36.3 billion across 265 financing deals. The number of financing transactions nearly matched that of the biopharmaceutical sector, while the total amount raised quadrupled.

The surge in the medical device sector is driven by a combination of factors, including the opening of exit channels. Given the relatively inelastic nature of the medical device industry, its lower risk profile, and its ongoing growth phase, it has become one of the preferred options for capital allocation. The significant rise in valuations is attributable to the scarcity of high-quality investment targets in the medical device field, the strong market consensus, and the pronounced trend of favoring industry leaders.

Unlike pharmaceuticals, clinical trials for medical devices carry lower risks and have shorter durations, making the pre-market phase a critical entry point for capital. Therefore, a major investment thesis in the medical device sector is to identify leading companies by tracking their clinical trial and regulatory approval progress. Against the backdrop of increasing competition in the medical device track, more institutions have stated that it is necessary to look further upstream for investment opportunities.

This trend was also reflected in the high-profile sectors of 2020, where neurointerventional devices and surgical robots shared a common characteristic: their products had not yet entered the phase of large-scale commercial sales. This implies that these companies will need robust commercialization capabilities in the future to justify their current high valuations.

Gao Weipeng, Partner at Yuansheng Venture Capital, stated, “In the medical device sector, most investors prefer mature companies with established revenue and profits, or those with late-stage clinical progress. In contrast, we are more inclined to invest during the arduous early stages. In terms of specific focus areas, Yuansheng Venture Capital will continue to prioritize innovations in medical devices within niche segments such as cardiovascular, orthopedics, ophthalmology, and medical aesthetics. Meanwhile, we are also optimistic about key consumables for large-scale medical equipment and the localization of upstream components.”

Diagnostic Sector: Riding the Anti-Epidemic Wave to Growth, with Two Major Directions for Future Expansion

In 2020, the sector most significantly impacted by the pandemic was undoubtedly diagnostics. The influence of COVID-19 on the diagnostics sector extended beyond the surge in performance for manufacturers and third-party testing laboratories driven by nucleic acid testing; it also propelled concepts such as metagenomic next-generation sequencing (mNGS) and automated PCR into the spotlight, making them key areas of strategic investment.

It is worth noting, however, that if a sector only plays a role during sudden public health emergencies, its investment rationale is not strictly speaking robust. Gao Weipeng of Yuansheng Venture Capital stated that the diagnostics sector is somewhat unique, requiring both innovation and practical, market-ready products. We place significant emphasis on the diagnostics sector and adopt a steady and prudent investment style. The diagnostics field features numerous technological platforms, and the barrier to entry for startups is not particularly high. With multiple technological platforms and investment targets intersecting, investing in diagnostics is by no means easy. When selecting investment targets, assessing team capabilities is more important than choosing the sector itself.

Among the numerous technological platforms, VCBeat’s research has identified two primary areas of focus for institutions today. The first centers on testing needs for major diseases, with early cancer screening, respiratory testing, infectious disease testing, pet in vitro diagnostics, and coagulation testing emerging as hot application scenarios. Within these broader categories, there is still potential for niche market leaders to emerge. The second area focuses on new technological platforms, where next-generation platform technologies also hold the potential to give rise to major industry leaders.

Healthcare Services Sector: New Opportunities Are Emerging

Compared with the top three major sectors, the healthcare services sector has attracted relatively less attention. Four or five years ago, China experienced a wave of hospital mergers and acquisitions, followed by a wave of hospital divestitures after 2018. Few private hospitals have managed to list on the secondary market. Investors in private hospitals have often been asked: Can healthcare services truly be capitalized?

In 2020, the capital market finally gave an affirmative answer. The implementation of the registration-based IPO system on the ChiNext board, which allows listed companies to carry forward historical losses without prior make-up, has brought benefits to the medical services sector that requires substantial early-stage investment. As a result, multiple specialized hospitals have filed for initial public offerings (IPOs). Hygeia Oncology, a specialized oncology hospital group, was listed on the Hong Kong Stock Exchange, while Huaxia Eye Hospital Group, Purui Eye Care, and He’s Eye Hospital all filed for IPOs on the ChiNext board.

Regarding the recent wave of hospital divestitures, Zhou Yi from Shenzhen Capital Group stated: “The healthcare services sector is a promising track, but timing is critical for institutional investors. For instance, it takes approximately eight years for a tertiary hospital to progress from construction commencement to break-even—a timeframe that even exceeds the lifecycle of certain funds. Therefore, in my view, investments in private hospitals should avoid the early stages.”A wave of sell-offs emerged in 2018, which I attribute to buyers’ neglect of the fact that healthcare services require substantial long-term investment, characterized by high capital intensity, extended payback periods, and significant challenges in brand building.“Overall, in the healthcare services sector, there are still too few large-scale targets; we remain hopeful.”

In the healthcare services sector, Aier Eye Hospital and Topchoice Medical, specializing in ophthalmology and dentistry respectively, have achieved market capitalizations exceeding RMB 100 billion, setting benchmarks for the industry. Who will be the next Aier Eye Hospital?

Cao Yibo of Sequoia China, which has invested in Jinxin Fertility, the world’s largest private assisted reproductive technology group, outlined his investment criteria from a macroeconomic perspective:In the healthcare services sector, strategic selection of investment tracks requires a balance across multiple dimensions. Ideal investment targets should possess certain competitive barriers to avoid excessive competition akin to that seen in the medical aesthetics industry, while also offering sufficient replicability. This enables expansion after a viable business model has been established, rather than being confined to operating only a single flagship facility, as is often the case with some highly specialized clinical fields.While selecting the first equilibrium point, it is also essential to consider the balance of interests between capital and physicians within the industry. In certain sectors, physicians hold disproportionate influence, limiting the value that capital can add and ultimately making profitability difficult. The ophthalmology sector satisfies both criteria. Although dentistry has achieved the first balance, it remains imperfect in terms of the second. This underlying dynamic explains why ophthalmology has become virtually the only area of private healthcare to achieve significant success.

Stone Capital has analyzed new opportunity points from a specialty care perspective. Stone Capital invested in Boner Orthopedics as early as 2014 and has long focused on opportunities in the healthcare services sector. Zang Jialun stated: “Although China’s private healthcare services have a relatively short development history, we can still observe the evolution of opportunities within specialized fields. In the initial stage of the industry’s rise, driven by consumption upgrades and guided by the liberalization of medical policies, business opportunities were concentrated in consumer-oriented specialties, such as plastic surgery, obstetrics and gynecology, and dentistry. Today, these specialty sectors have seen the emergence of leading healthcare groups, with competition becoming increasingly intense. During the early stages of industry development, certain specialties within serious medicine seized opportunities in grassroots county-level markets, such as ophthalmology, orthopedics, and radiotherapy. This trend placed higher demands on entrepreneurs’ professional expertise and business capabilities, and a number of pioneering companies successfully capitalized on this wave of ‘encircling cities from rural areas.’”

As the private healthcare services industry enters its mid-stage of development, we have observed several new potential directions: 1) Major specialties for critical and severe conditions, such as cardiovascular diseases, oncology, and neurology, which were once absolutely dominated by public hospitals, are gradually presenting opportunities for non-public medical institutions. The prerequisite is that private healthcare providers must identify precise, differentiated entry points, prioritizing medical quality and therapeutic efficacy above all else, before flexibly considering their positioning and business models. 2) As consumption upgrades become more refined, demand for niche specialties is increasingly emerging and being released. Specialties such as otolaryngology, psychosomatic medicine, rehabilitation, and pain management—traditionally under-prioritized and under-resourced in public hospitals—offer substantial commercial opportunities in these nearly untapped fields, provided that market-oriented product thinking and customer acquisition strategies are effectively employed. We remain bullish on the healthcare services industry. In particular, with the nationwide implementation of DRG/DIP payment reforms and volume-based procurement, the role of public hospitals in providing “basic care” is becoming increasingly clear, thereby creating greater room for growth for private healthcare as a complementary market force.

The tumultuous year of 2020 has swept past, and I believe every professional in the healthcare industry has had their own way of bidding it farewell. Regardless of how 2020 unfolded, let us borrow a line from *The Remains of the Day* to reflect on the present: “What is the point of worrying oneself too much about what one could or could not have done to control the course one’s life took? Surely it is enough that the likes of you and I at least tried our best to make something worthwhile out of what we were given.”