Can Meituan Make Waves in the Health Industry? Five Critical Questions

Meituan

E-commerce Platform Service Provider

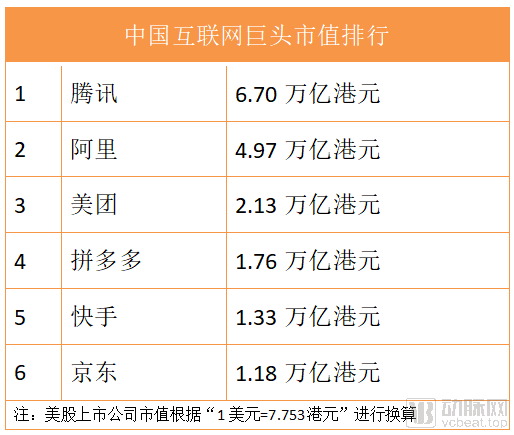

As one of China’s top three internet giants by market capitalization, Meituan faces an increasingly urgent need to identify a second growth curve, yet it has consistently lacked a compelling development strategy.

Prior to Meituan, every true tech giant possessed its own uncontested territory as the cornerstone of its business. Meituan’s shortfall in this regard has determined that it is not yet on the same level as Tencent and Alibaba.

Tencent’s social media and entertainment sectors, along with Alibaba’s e-commerce and financial services, constitute formidable moats that are difficult to challenge. In contrast, Meituan’s core food delivery business has been facing persistent counterattacks from Ele.me; its secondary pillar in hotel and travel bookings is under significant pressure from powerful rivals such as Ctrip and Qunar; while its newer ventures into mobility services and community group buying operate in highly contested markets.

In terms of core strengths, Meituan excels in labor-intensive, offline-heavy operations that are often arduous and demanding. Leveraging its robust and efficient operational capabilities, Meituan has established a solid foothold across diverse sectors, including group-buying, food delivery, movie tickets, hotel and travel services, mobility, and new retail. However, it has not been able to completely eliminate its competitors.

According to McKinsey’s Three Horizons Theory,Meituan has sufficient core frontline businesses, but it lacks second-tier businesses that are poised to generate substantial revenue in the near term, as well as third-tier, future-oriented businesses with the potential to emerge as new growth drivers.

This provides the overall background for Meituan’s expansion into the healthcare sector.

A few years ago, Meituan extended its reach into the healthcare sector. Building on its core business of local life e-commerce, it naturally expanded into two major segments: medical aesthetics (an extension of local lifestyle services) and pharmaceutical sales (an extension of its food delivery services), while also making strategic inroads into areas such as medical devices and healthcare services.

Notably, Meituan has recently launched its new healthcare brand, “Baishou Health Network.” This comprehensive medical and health platform currently offers services including pharmaceutical investment promotion, agency representation, product showcases, exhibitions, and store establishment. This move signifies that Meituan is building and refining a closed-loop healthcare service ecosystem, marking a clearer strategic vision for its foray into the medical and health sector.

This has prompted people to wonder whether Meituan, known for its “aggressive tactics,” can sustain its strong operational capabilities and take root, flourish, and bear fruit in the healthcare sector.

In the healthcare sector, Meituan has been making strategic moves for several years, yet public awareness of its presence in the broader health and wellness industry remains limited.

Currently,Meituan’s relatively mature health businesses primarily consist of two segments: pharmaceutical sales and medical aesthetics.

In terms of pharmaceutical sales, Meituan partnered with the online pharmacy of Laobaixing Pharmacy in 2015 and launched a medicine delivery module on the Meituan app in June of that year, subsequently expanding its offerings to include various services such as online medication purchasing and home delivery.

From a business model perspective, Meituan serves as an intermediary, platform provider, and delivery service for its pharmaceutical sales. Users can more easily search for nearby pharmacies and place orders through the Meituan app, while Meituan’s delivery team ensures that medications are delivered to customers promptly.

This business leverages Meituan’s vast delivery capabilities, but it clearly falls short in terms of service scarcity.

This is not reflected in the business logic. Meituan, by addressing the information asymmetry between supply and demand sides, targets two pain points faced by C-end users and traditional pharmacies, matching users’ need for immediate medication access with traditional pharmacies’ need for digital transformation. This approach is sound from a commercial logic perspective.

The issue is that Meituan is not the only platform capable of providing such services. Among them, comprehensive platforms like JD Health possess far stronger accumulations in pharmacy operations and logistics capabilities than Meituan; meanwhile, some heavily vertical-focused platforms, such as Dingdang Kuaiyao, offer user experiences that are no inferior to those of Meituan.

Meituan emphasizes that, leveraging its pharmacy network and delivery team, it can meet users’ needs for conventional medications for acute conditions such as diarrhea and stomach pain within 23 minutes. With 24/7 service, Meituan ensures timely delivery of medications at all hours, even for orders placed in the early morning.

Examining the Digital Upgrade Needs of Traditional Pharmacies: Following collaboration with Meituan Medicine, traditional pharmacies have transitioned from a purely brick-and-mortar model to a more flexible “store + warehouse” operational model, thereby enhancing operational efficiency.

However, the issue lies in the fact that while meeting users’ demand for medication delivery within 30 minutes offers considerable room for innovation, such time-sensitive needs remain non-mainstream within the overall landscape of online pharmaceutical purchases. Instead, the predominant demand continues to be for routine medications for chronic diseases, which are less time-critical.

According to the "2019 Analysis Report on the Status and Trends of Online Drug Purchases by Chinese Residents via E-commerce Platforms," user demands for online drug purchases, in descending order of priority, are: a wider selection of brands, greater safety assurances, and lower prices. Faster logistics and a more convenient purchasing process rank last. Consequently, needs requiring immediate fulfillment still represent only a small segment. The underlying reason is that the habit of purchasing urgent medications online has not yet been fully cultivated among users. The vast majority of patients opt for nearby offline medical consultations and pharmacy purchases during acute episodes. Therefore, there is still a considerable way to go in educating the market for online purchases of urgent medications.

For the B-side, in addition to empowering pharmacies, Meituan’s support is further reflected in the fact that as user frequency and stickiness increase, the accumulated user behavior data on the platform will provide a digital foundation for traditional pharmacies to optimize their pharmaceutical supply and sales operations.

It is not difficult to find that,In its pharmaceutical sales business, the services provided by Meituan are in demand in the market but are not scarce.

The value lies in addressing users’ routine needs for urgent medications and the digital transformation demands of traditional pharmacies. The core support stems from Meituan’s same-city delivery capabilities, accumulated over more than a decade, and the high-frequency application scenarios built upon its primary local community lifestyle services. However, competitors in this space and their capabilities are no weaker than Meituan’s. To secure a relatively leading position for this business, Meituan must achieve greater differentiation to meet deeper-level needs, which is no easy task.

In the medical aesthetics sector, Meituan entered the market in 2017 and, by launching its “light medical aesthetics” strategy, rapidly expanded over three years to become an industry leader. During the 2020 “618” shopping festival, the online gross merchandise volume (GMV) of Meituan’s medical aesthetics business reached RMB 2.1 billion, surpassing many specialized medical aesthetics platforms. Public information indicates that more than 11,000 medical aesthetics institutions are registered on Meituan’s platform, accounting for approximately 11.8% of all such institutions nationwide.

As a key component of local community life, leveraging Meituan’s substantial traffic advantages and its “community + reviews + e-commerce” model, medical aesthetics has rapidly become one of Meituan’s fastest-growing segments. The rapid breakthrough in the medical aesthetics sector is primarily attributed to Meituan’s focus on a “non-surgical medical aesthetics” strategy.

In the medical aesthetics industry, “light” and “heavy” are imprecise relative concepts. Procedures requiring surgical intervention, such as rhinoplasty and bone contouring, fall under the category of “heavy medical aesthetics,” while injectables and skincare treatments belong to “light medical aesthetics.” Although heavy medical aesthetics commands higher average transaction values, it suffers from low consumption frequency. In contrast, light medical aesthetics, despite its lower unit price, boasts a broader customer base and higher repurchase rates. For most consumers, light medical aesthetics is not perceived as a medical procedure since it does not involve surgery, resulting in lower decision-making costs. Consequently, Meituan’s accumulated local lifestyle user base is naturally better suited for this segment. This explains why numerous medical aesthetics providers choose to partner with Meituan Medical Aesthetics.

However, it must be recognized that Meituan’s advantages in the medical aesthetics sector are only relative and may even be insignificant.This is because, in the medical aesthetics industry, giants like Alibaba and JD.com have also entered the market, while leading platforms such as So-Young and Gengmei have accumulated years of competitive advantages.

Meituan’s medical aesthetics business addresses the information asymmetry between consumers and medical aesthetics providers. It boosts user engagement and conducts market education through page displays and content operations. However, these offerings do not differ significantly from those of competitors and are even at a relative disadvantage. For instance, in terms of vertical expansion, although Meituan has ventured into areas such as installment payment plans for medical aesthetics services, it has yet to demonstrate substantial room for further expansion or meaningful differentiation.

As is well known, in the medical aesthetics industry, consumers place greater emphasis on service and trust. Institutions primarily focused on non-surgical medical aesthetics typically begin by serving consumers through single-item, single-session treatments, gradually evolving into single-item, multi-session regimens, and ultimately expanding to multi-item, multi-session packages. This progression is a lengthy process with an extended conversion cycle. Only after consumers have developed strong loyalty and trust in the institution will they potentially extend their engagement to the realm of surgical medical aesthetics.

“Medical-grade aesthetics” imposes even more stringent requirements on medical quality, making high-caliber physician resources a critical factor. Whether Meituan Aesthetics can secure and effectively manage a larger pool of scarce physician talent, and thereby prevail in increasingly fierce competition, remains to be seen.

In summary, Meituan has achieved commendable results in its two most critical segments within the healthcare sector—pharmaceutical e-commerce and medical aesthetics. However, it falls short in terms of service differentiation and business model scarcity. This may lead to the challenge that the market remains highly sticky yet does not allow for the rapid establishment of exclusive competitive advantages, despite requiring substantial resources and investment.In the medium term, relying solely on medicine delivery and non-invasive medical aesthetics, Meituan will still be unable to change its position in the new battlefield as a “four-way battleground” or quickly bring the competition to an end.

Who are Meituan's competitors in the healthcare sector?

If we look at Meituan’s existing individual business lines, it faces competitors such as So-Young and Gengmei in the medical aesthetics sector, and JD Health and Dingdang Kuaiyao in online pharmaceutical sales. However, this perspective is insufficient for a holistic assessment of Meituan.Judging from Meituan’s moves, the company is not merely interested in continuously piling up businesses across various niche sectors; rather, it has a stronger intention to spin off its healthcare segment and build an enterprise comparable to Ali Health and JD Health.

From a strategic perspective, this is the right direction, but the opponent remains formidable.

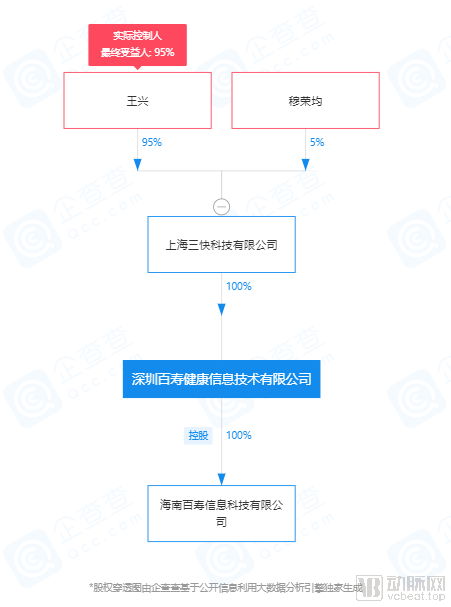

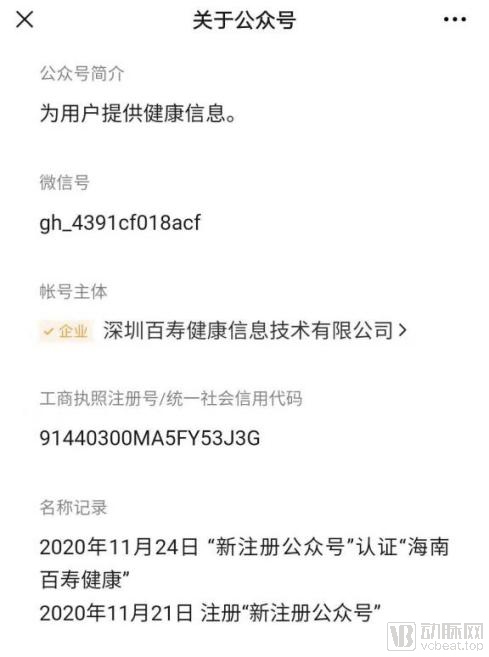

As Meituan’s new healthcare brand, the recently launched “Baishou Health Network” is exploring this approach. The entity behind “Baishou Health Network” is Shenzhen Baishou Health Information Technology Co., Ltd., which was established in November 2019. Zeng Wei serves as its legal representative and executive director, Li Jinfei as general manager, and Xu Rongcong as supervisor. Equity penetration analysis reveals that the company is affiliated with Shanghai Sankuai Technology Co., Ltd., with Wang Xing (holding a 95% equity stake) as the actual controller and ultimate beneficiary.

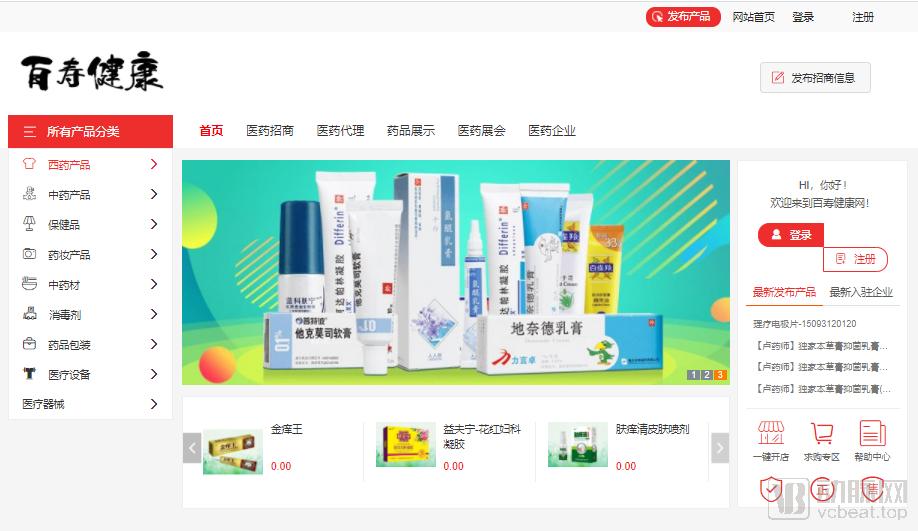

As shown on the official website of “Baishou Health Network,” the platform currently offers features such as “Pharmaceutical Supply/Demand” and “Pharmaceutical Investment Promotion/Agency,” exhibiting characteristics of a pharmaceutical e-commerce platform. Its business scope covers Western medicines, traditional Chinese medicines, health supplements, cosmeceuticals, disinfectants, and medical devices. Moreover, “Baishou Health Network,” which is still in the testing phase, provides merchants with services such as product listing and one-click store setup. In summary, “Baishou Health Network” currently resembles a comprehensive healthcare platform integrating multiple functions, including pharmaceutical e-commerce and investment promotion for store establishment.

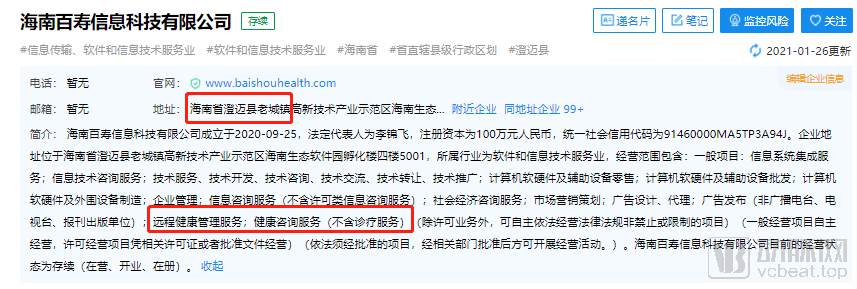

It is worth noting that Shenzhen Baishou Health Information Technology Co., Ltd., the entity behind “Baishou Health Network,” has a wholly-owned subsidiary, Hainan Baishou Information Technology Co., Ltd., located in the Old Town High-Tech Industrial Demonstration Zone of Chengmai County, Hainan Province. “Many companies are currently establishing entities in Chengmai County with the aim of securing an internet hospital license in Hainan. For example, Duoduo Health Technology (Hainan) Co., Ltd., under Pinduoduo,” said a senior industry practitioner in the internet hospital sector to VCBeat. From this strategic layout, it appears that Meituan intends to obtain an internet hospital license in the future, thereby developing services such as online remote diagnosis and treatment and medical information consultation, ultimately achieving full-chain medical service coverage.

Additionally, VCBeat discovered that the “Hainan Baishou Health” WeChat Official Account quietly launched on November 21 last year. The account is operated by Shenzhen Baishou Health Information Technology Co., Ltd., and is positioned to provide health information to users, although it has not yet published any posts. Given Li Jinfei’s previous experience at Baidu, where he achieved notable success with information-based products such as “Baidu Zhidao” (Baidu Knows) and “Baidu Wenku” (Baidu Library), it is highly likely that “Baishou Health Network” will develop similar products to “Baidu Health Medical Dictionary” and “Encyclopedia of Famous Doctors” as traffic entry points in the future.

It is not difficult to see that,Behind Meituan’s launch of the “Baishou Health Network,” clear strategic arrangements have already been made in areas such as team building, corporate affiliations, and pilot business operations, underscoring Meituan’s strong commitment to the healthcare sector.

However, judging from the development experience of internet healthcare, current players—whether listed companies like Ali Health and JD Health, or rapidly expanding entities such as Baidu Health and Xiaohe Medical (part of the ByteDance ecosystem)—have all ventured into fields including pharmaceutical e-commerce, internet hospitals, and health information consulting. This is because, unlike other startups, internet giants possess inherent advantages in traffic, capital, and distribution channels, enabling them to rapidly build one-stop services encompassing “health science popularization, online consultation, pharmaceutical sales, and health management,” thereby increasing their leverage for future commercialization.

The difference is that Baidu Health places greater emphasis on building a dual ecosystem of “content + services,” while Xiaohe Medical is still in its early stages. Meituan competes with them in a differentiated manner, andGiven the strong pharmaceutical e-commerce orientation of Alibaba Health and JD Health, Meituan is competing with them in the same sector.. Notably, Alibaba’s Ele.me overlaps with Meituan, and in recent years, Meituan has been continuously integrating financial modules into its app while Alipay has been steadily adding local lifestyle services. Given these trends, Meituan and Alibaba, whose business models are increasingly converging, will face more direct competition in the healthcare sector.

Of course, JD Health and Alibaba Health have largely entered the internet healthcare sector through their online retail pharmacy businesses, placing greater emphasis on building and leveraging e-commerce channels. In contrast, their ventures into high-gross-margin areas—such as third-party merchant commissions, platform usage fees, advertising service fees, and traffic monetization for consumer healthcare providers (including medical aesthetics, health check-ups, and dental services)—are still in their early stages. In this regard, Meituan holds a relative advantage.

It is evident that Meituan will inevitably engage in a fierce competition with Alibaba Health and JD Health within the same sector.

The question of whether Meituan will become the next Alibaba has been widely discussed in the industry. Answering this question also seems to address whether Meituan’s business in the healthcare sector will grow into the next AliHealth.

First, an empirical conclusion: it is difficult for any company to defeat a market leader by simply replicating its successful strategies.

Although Meituan has been expanding its boundaries and striving to create ecosystem effects, it has not yet built strong synergies. In contrast, Alibaba, leveraging its superior resource integration capabilities, has established relatively mature closed-loop ecosystems in payments, new retail, and B2B on the foundation of its e-commerce business. This divergence is determined by the inherent “DNA” of the two companies.

What is Meituan’s “DNA”? Compared with Alibaba, what “DNA” does it lack?

From the perspective of their core businesses,Meituan’s “DNA” lies in its understanding and operation of local lifestyle services, as well as the robust delivery network built upon this foundation. In contrast to Alibaba, Meituan lacks the inherent capability for “physical e-commerce.”This is rooted in history. Between 2010 and 2011, the then-emerging Meituan received investment from Alibaba. To avoid competing with Alibaba’s physical e-commerce business, Meituan pivoted to the local life services market. As a result, Meituan lacked experience in physical e-commerce and the corresponding supply chain infrastructure.

From the perspective of the healthcare sector, if Meituan’s “Baishou Health Network” aims to become an e-commerce platform for physical pharmaceutical products, it still has a long road ahead. Addressing challenges such as supply chain management and merchant operations will constitute significant tests.

Looking at JD Health, the key to its diversification from online pharmaceutical sales to broader medical services lies in the advantages of its supply chain “DNA.” It is worth noting that while internet healthcare is constrained by factors such as policy ambiguity and the heavy reliance on offline consultations for diagnosis and treatment, an underdeveloped supply chain and logistics system also significantly hinders its rapid growth. For example, JD Health has established 11 specialized pharmaceutical warehouses across China, complemented by more than 230 other warehouses. This infrastructure has substantially improved fulfillment efficiency, enabling next-day delivery for 80% of medication orders and greatly enhancing user experience.

Ping An Good Doctor’s “DNA” lies in its channel and operational capabilities within the insurance business. In 2020, Ping An Good Doctor established an Insurance Business Division to advance deep online collaboration with Ping An Health Insurance. By jointly developing customized integrated products combining medical health services and insurance coverage, the company has achieved mutual empowerment between its healthcare and insurance offerings. Furthermore, leveraging the corporate client network of Ping An Group’s comprehensive financial services, Ping An Good Doctor has rapidly reached its target users. By the end of 2020, Ping An Good Doctor had expanded its corporate client base to over 1,100 companies, including numerous large state-owned enterprises, leading internet companies, and renowned financial institutions.

On the eve of Meituan’s IPO, Wang Huiwen, then co-founder and senior vice president of Meituan, stated at an event that he was not inclined to limit the company by its inherent “genes.” He believed that corporate DNA could be extended, genetically modified, or even undergo mutations. The key, he argued, was to steer such mutations in a positive direction: eliminating detrimental changes while reinforcing beneficial ones, ultimately achieving a successful process of genetic transformation.

However, once a company reaches a certain scale, past experiences and modes of thinking inevitably become organizational inertia. It is not easy for the corporate “genes” to extend or mutate; this process must be left to time.

For a considerable period, Meituan’s core competitiveness lay in its massive ground-promotion “iron army” and operational capabilities.

According to Meituan’s financial report released on November 30, 2020, in the third quarter of the previous year, the platform had 6.5 million merchants, 480 million users, and over 3 million delivery riders. Managing such a vast number of merchants and riders, along with conducting user operations, clearly demonstrates the significant efforts Meituan has invested in its operational capabilities over the years.

As Meituan continues to expand and strengthen user stickiness, it has become a massive traffic pool, similar to other internet giants. Together with its capabilities in ground promotion and operations, these factors have constructed Meituan’s moat. How will these three capabilities drive and create opportunities for Meituan’s healthcare business?

In terms of ground promotion and operations, these capabilities have grown in tandem with Meituan’s local services business. This advantage enables Meituan to rapidly scale traditional retail pharmacies, as well as future pharmaceutical-related businesses under the “Baishou Health Network,” including investment promotion, agency services, product showcases, exhibitions, and store openings. However, it is worth noting that Meituan’s historical approach has often followed a strategy of “handling locally relevant services in-house, acquiring mature market businesses first, and only developing them internally if acquisitions prove unfeasible.”

In late November last year, Meituan filed a trademark application for “Meituan Professional Pharmacy.” This move indicates Meituan’s intention to expand its offline business, such as by establishing self-operated pharmacies. Drawing from the business models of Alibaba Health and JD Health, self-operated services currently represent the core revenue source. Therefore, opting to build its own pharmacy network will significantly enhance Meituan’s commercialization capabilities in the new retail pharmaceutical sector in the future.

Beyond generating revenue, another core function of Meituan’s proprietary business is to support its strategic expansion from “pharmaceuticals” to “medical services.” It is important to recognize that although the primary focus of major internet healthcare platforms currently remains on “drug sales,” providing professional medical consultation and pharmaceutical care services constitutes the foundational prerequisite for internet healthcare and serves as a key strategy for enhancing user stickiness.

It is evident that, leveraging its ground promotion and operational capabilities, Meituan’s medicine purchasing business is gradually shifting from an “asset-light” to an “asset-heavy” model, thereby advancing into the “deep waters” of the healthcare industry. In this regard, Alibaba, which aggregates resources through a platform-based model, has relatively less experience, whereas JD.com possesses strong offline operational capabilities comparable to those of Meituan.

In terms of traffic, the Meituan app has become a national-level application with tens of millions of daily active users, offering abundant traffic resources. This is a key reason why numerous merchants choose Meituan. Meituan’s next challenge lies in how to allocate this traffic more rationally, encouraging more pharmaceutical merchants to join the platform, thereby enhancing user acceptance and retention.

In summary,Meituan’s core strengths in ground promotion, operations, and traffic serve as the three major drivers for its continued expansion in the healthcare sector.

With the successive IPOs of Ali Health, Ping An Good Doctor, and JD Health, is there still a place for Meituan in internet healthcare?

Looking at the market capitalizations of the three major listed players, the latest figures show Alibaba Health at HK$392.232 billion, Ping An Good Doctor at HK$155.573 billion, and JD Health at HK$530.834 billion, bringing their combined market cap to over HK$1 trillion. According to data from iiMedia Research, the number of mobile healthcare users in China reached 635 million in 2020, and the overall size of the broader health industry is projected to reach RMB 10 trillion. From the perspective of market capacity, there remains substantial room for growth in China’s internet healthcare market.

To break it down further, currently in the field of internet-based medical and health services,The “Internet + Pharmaceuticals” model is already highly mature, while the “Internet + Healthcare” model still holds significant room for growth and innovation., especially during the pandemic, the importance of telemedicine services has begun to stand out.

Therefore, against the backdrop of slowing growth in existing internet-based market segments, expanding into the healthcare sector represents a crucial avenue for Meituan’s business growth. In the realm of physical e-commerce, Meituan faces competition from two giants, JD Health and AliHealth. By pursuing a differentiated strategy focused on community-based local life services and targeting users with urgent medication needs, Meituan will be well-positioned to solidify its “Internet + Pharmacy” business.

In the realm of “Internet + Healthcare,” both JD Health and Alibaba Health have been actively strategizing. Whether by establishing internet hospitals, collaborating with physicians from more public Grade 3A hospitals, or delving into specialized medical sectors as participants, these initiatives will present them with substantial opportunities.

Furthermore, compared with Alibaba and JD.com, Meituan has relatively weaker technological accumulation, while internet healthcare demands more robust technical capabilities.

In summary, Meituan’s strengths lie in its robust operational capabilities, while its weaknesses include a relative lack of accumulation in industrial internet technology compared to competitors. At the business model level, Meituan lacks exclusivity externally; internally, the proliferation of new businesses entering the expansion phase raises questions about whether sufficient resources and commitment can be guaranteed.

Of course, internet giants equipped with abundant resources—such as a vast pool of tech talent, ample capital, massive user traffic, and strong distribution channels—often make rapid headway when initially entering a specific niche. However, in the process of deepening their engagement with the healthcare industry, many companies have experienced setbacks and failures. For instance, Haven, a health insurance venture jointly established by three corporate behemoths—Amazon (with a trillion-dollar market capitalization), JPMorgan Chase, and Berkshire Hathaway—announced its dissolution after just two years.

In the vast field of healthcare, Meituan undoubtedly has a long way to go. Nevertheless, Meituan has already rolled out full-chain services encompassing new retail pharmaceuticals, pharmaceutical e-commerce, and internet hospitals, thereby expanding its strategic possibilities. This may well position Meituan as one of the key disruptors in the healthcare sector.