Kindstar Globalgene Files for Hong Kong IPO as Pioneering Independent Clinical Specialty Testing Provider

According to the HKEXnews website, on February 23, Kindstar Global, an independent provider of specialized clinical testing services, formally submitted its prospectus to the Hong Kong Stock Exchange for a proposed listing on the Main Board. Goldman Sachs, CICC, and Credit Suisse served as joint sponsors.

After numerous twists and turns, this long-established institution, once regarded as one of the top ten independent clinical laboratories in China, has finally taken a critical step toward entering the public capital markets. Founded in 2003, KingMed Diagnostics is now positioned as China’s first independent provider of specialized clinical testing services. Based on 2019 revenue, KingMed Diagnostics held a 42% share of China’s independent in-depth hematology testing market, ranking first, and is also among the companies worldwide offering the most comprehensive portfolio of hematology tests.

However, Kingstar Global is more widely recognized by the public as a frontline stronghold in the early fight against the COVID-19 pandemic.

In February 2020, KingMed Diagnostics rapidly developed COVID-19 nucleic acid testing capabilities through its headquarters, Wuhan Kingstar Medical Inspection Co., Ltd., located in Wuhan, Hubei Province, providing COVID-19-related testing services to hospitals within the city. During the most severe phase of the epidemic in China, KingMed Diagnostics also provided testing services for Huoshenshan Hospital and Leishenshan Hospital, two major emergency specialty field hospitals. As of the submission of its prospectus, KingMed Diagnostics had successively provided nearly 2 million person-tests of nucleic acid testing to regions including Hubei, Xinjiang, and Beijing. This new business, which generated nearly RMB 100 million in revenue, became the fastest-growing segment of KingMed Diagnostics in 2020.

Huang Shiang, the founder of KingMed Diagnostics, was formerly a clinician and is now 62 years old. During the first three decades of his life, Huang completed his professional transition from medical student to attending physician at Tongji Medical College of Huazhong University of Science and Technology. He subsequently pursued further studies and worked in the United States. In 2003, at the age of 44, Huang established KingMed Diagnostics.

In the transition from research scholar to entrepreneur, Huang Shi’ang has made many attempts.

Huang Shiang made numerous missteps. In 2011, he strategically introduced Mayo Clinic’s world-class diagnostic resources, yet incurred significant costs due to inadequate product adaptation for the Chinese market. In 2013, he substantially restructured the company’s operations to meet the requirements for a U.S. listing, fortunately halting losses before the core business foundation was undermined.

He was also right about many things. Starting with specialized hematology testing, Kingstar Global has successively developed clinical specialty testing services, including genetic and rare disease testing, infectious disease testing, and oncology testing, becoming the independent clinical laboratory with the largest portfolio of such tests in China. Rarely seen in the industry, the company established its own standardized cold-chain logistics for pharmaceutical transport and cultivated a sample logistics team of nearly 1,000 personnel, thereby ensuring the accuracy of clinical specialty testing from the source.

Seven years later, at the age of 50, Huang Shiang led his company to list in Hong Kong, once again facing unprecedented challenges, which also marked a new challenge for KingMed Diagnostics.

During his studies in the United States, Huang Shiang noticed significant differences in disease testing models between Chinese and American hospitals. At that time, most tests in domestic hospitals were conducted in-house, whereas U.S. hospitals tended to outsource more frequently to specialized third-party institutions. As medicine continues to advance, an increasing number of diseases are being identified with increasingly detailed classifications, involving thousands of medical testing items. If all these tests were conducted within hospitals, it would undoubtedly place a burden on staffing, equipment configuration, and maintenance. On the other hand, many patients living in smaller cities had to travel to larger hospitals in major cities with stronger testing capabilities, which increased healthcare costs and contributed to hospital overcrowding. Underlying this dual pressure was a strong, phase-specific demand for outsourcing clinical sample testing.

Huang Shiang, Founder of KingMed Diagnostics

When Huang Shiang returned to China to found Kingstar Global, third-party medical testing laboratories were beginning to emerge in the country. DA An Gene, KingMed Diagnostics, and other independent medical testing labs that later became industry leaders in China were established successively, completing the initial validation of their business models by providing hospitals with scaled-out routine testing services for outsourced samples. Huang Shiang chose a different path, deciding to focus on specialized clinical testing. In China, while large hospitals offer comprehensive departments, most specialized disciplines are not particularly strong.

Taking hematology as an example, a hospital may have only 50–100 beds, while patients require 300–500 different laboratory tests. Most of these tests average only 1–2 cases per day, making it nearly impossible for hospitals to offer the full range of test items. It is even more difficult to cover the high-end, precise, advanced, and novel tests required for complex and rare diseases. Therefore, Kingstar Global positioned its first product series in hematological testing, providing professional and comprehensive laboratory services to hospital hematology departments—a business model that no other company had recognized at the time.

Within three years, Kingstar Global’s hematology testing portfolio swept across China. Huang Shi’ang recalled in an interview that whenever Kingstar Global’s sales representatives entered a new city, the fourth-, fifth-, and sixth-ranked hospitals would often seize the initiative to collaborate while the top three hospitals were still hesitating about sending specimens. These mid-tier hospitals quickly surpassed their higher-ranked counterparts in both the scale and effectiveness of specialized diagnostic testing, ultimately compelling the original top-three hospitals to join the partnership.

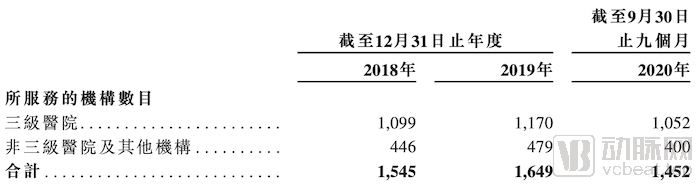

Number of Healthcare Institutions Served by KingMed Diagnostics (Source: Prospectus)

According to the prospectus, in 2019, KingMed Diagnostics (Kangsheng Global) completed a total of 1.7 million specialized clinical tests, of which 870,000 were hematology tests. This means that more than 4,600 clinical samples from over 1,600 hospitals in more than 400 cities across China are sent daily to KingMed’s independent medical laboratories located in Wuhan, Beijing, and Shanghai for testing. KingMed offers more than 2,300 clinical test items for various hematologic diseases, making it the independent medical laboratory capable of providing the most comprehensive hematology testing globally. Forty-two percent of the national annual expenditure on clinical hematology tests flows to KingMed. Huang Shiang once told employees that the volume and complexity of samples handled in one year at KingMed’s laboratories exceed what many other places would offer in ten years.

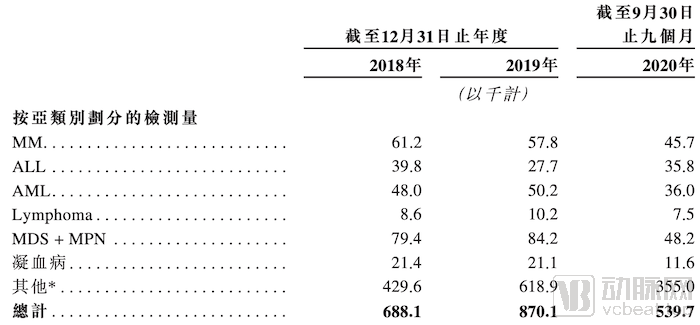

Kingstar Global Hematology Test Volume (Source: Prospectus))

Currently, Kingstar Global has accumulated over 500,000 real-world data records on hematological diseases, establishing the world’s largest database for blood disorders. This database not only helps Kingstar Global maintain its capacity for optimizing and innovating molecular diagnostic technologies but also provides numerous insights for applied research in precision medicine. Among Kingstar Global’s 3,500 specialized clinical testing items, an increasing number utilize self-developed diagnostic reagents and products, which are iterated at a rate of more than 100 items per year.

However, an analysis of operating performance indicates that Kingstar Global has reached a stage where it requires new growth drivers.

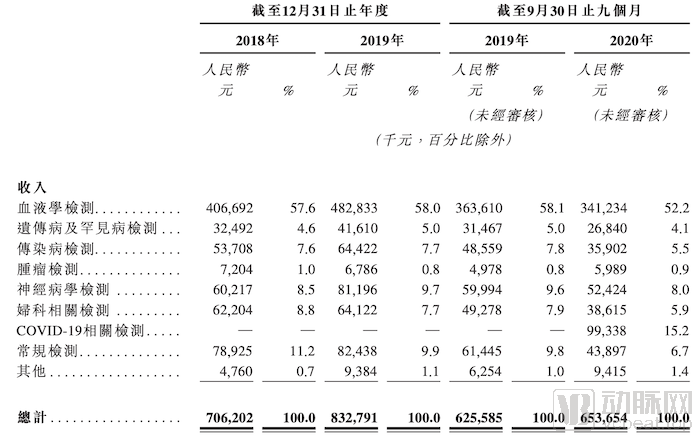

During its operations, KingMed Diagnostics operates nine business segments, which respectively handle hematology testing, genetic and rare disease testing, infectious disease testing, oncology testing, neurology testing, gynecology-related testing, COVID-19-related testing, routine testing, and services provided to contract research organizations.

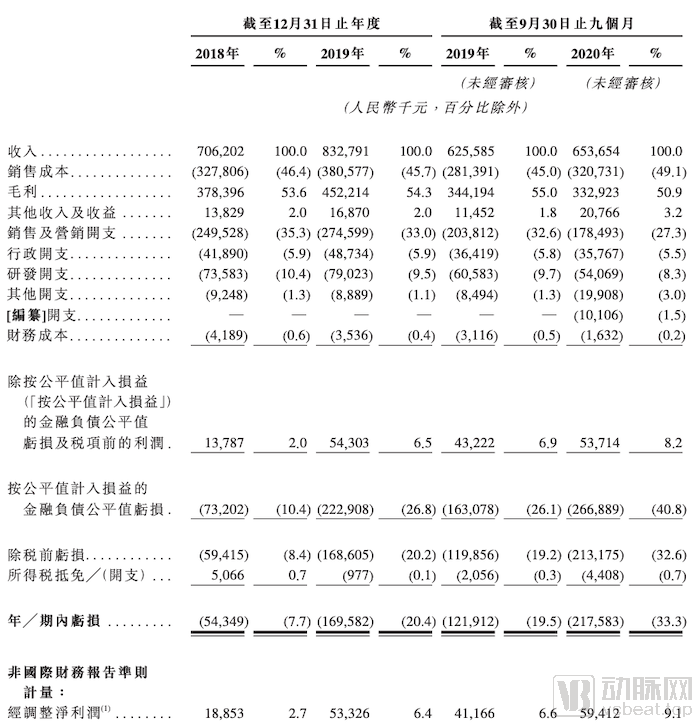

For the years ended December 31, 2018 and 2019, and for the nine months ended September 30, 2019 and 2020, KingMed Diagnostics generated operating revenues of RMB 706.2 million, RMB 832.8 million, RMB 625.6 million, and RMB 653.7 million, respectively. Among these, revenue from hematology testing accounted for over 50% each year, while the contribution of various clinical specialized tests to operating revenue remained relatively stable. The newly added COVID-19-related tests in 2020 generated nearly RMB 100 million in operating revenue, accounting for 15.2%, which helped KingMed Diagnostics barely avoid a decline in performance.

KingMed Diagnostics Revenue Structure I (Source: Prospectus)

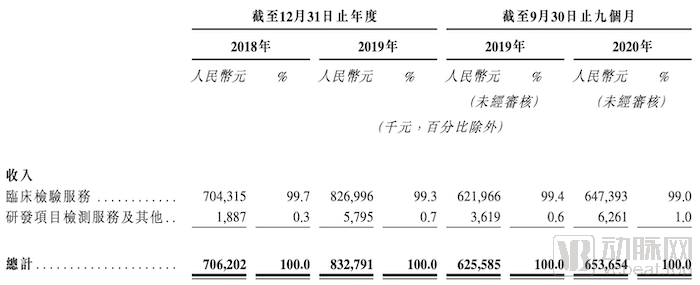

In terms of revenue structure, clinical laboratory testing services constitute Kingstar Global’s core competitive advantage, accounting for over 99% of total operating revenue. Although third-party R&D services provided to biopharmaceutical companies and CROs currently represent a small base, both their absolute amount and share of operating revenue are growing at an annual rate of nearly 100%.

KingMed Diagnostics Revenue Structure II (Source: Prospectus)

According to statistics, the market size of China’s clinical laboratory services grew from RMB 3.529 billion in 2015 to RMB 9.765 billion in 2019, representing a compound annual growth rate (CAGR) of 29%. This growth rate is projected to decline to 19.8% over the next five years. However, compared with the performance data disclosed in the prospectus, Kingstar Global’s clinical laboratory services recorded growth rates of 17% from 2018 to 2019 and 4% from 2019 to 2020, significantly below the industry average. This indicates that Kingstar Global’s traditional business is hitting a growth ceiling, which may well be the practical reason behind the rapid expansion of its R&D services business—evidence of its “second startup” initiative permeating every aspect of its operations.

Prior to its initial public offering, Kindstar Global conducted 25 clinical trials through external collaborations. Its technical capabilities include identifying new targets and mechanisms of acquired drug resistance, retrospective sample analysis for the rapid identification of biomarkers associated with drug response and resistance, prospective screening and patient referral to accelerate clinical trial enrollment, prospective clinical trial research, and companion diagnostic development to support therapeutic approval and commercialization. In fact, based on the disclosures in its prospectus, Kindstar Global has positioned such translational medicine services as its third growth pillar, beyond deepening hospital market penetration and expanding the scope of clinical testing.

Let us now examine the gross profit margin. Kindstar Global’s gross profit margin is relatively low compared to its industry peers, remaining within the range of 50.9% to 55% during the reporting period. According to Kindstar Global, factors influencing the gross profit margin include economies of scale in business operations, operational efficiency, accumulated experience, and the utilization of outsourced services. In the first nine months of 2020, the company experienced a 4.1 percentage point decline in gross profit margin, driven by an increased proportion of COVID-19 nucleic acid testing services in its operations, which are characterized by higher standardization and lower pricing flexibility.

KingMed Diagnostics Income Statement (Source: Prospectus)

As for whether the gross profit margin can truly increase in the future, the following analysis provides reference. In short, the low gross profit margin is due to low operating revenue and high cost of sales.

Increasing operating revenue essentially boils down to either boosting market penetration or raising product unit prices. Regarding market penetration, a key component of Kingstar Global’s IPO fund allocation plan is to strengthen its marketing network, which evidently requires sustained, long-term effort. As for raising product unit prices, this is likely a strategy that Kingstar Global abandoned years ago.

Previously, Kingstar Global had introduced from Mayo Clinic a cardiovascular risk factor detection product developed based on the latest international clinical guidelines. However, sales performance was less than ideal, as the product’s price of approximately RMB 2,000 was significantly higher than the few hundred yuan typically charged for specialized clinical laboratory tests in China, and its usage differed from the established practices of Chinese physicians. Since then, Huang Shiang has been committed to developing and applying new products tailored to China’s specific conditions, with cost control being a key consideration.

Next, let’s examine the cost of sales. A further breakdown of Kingstar Global’s cost of sales reveals that personnel costs account for approximately 22%, outsourcing costs for about 30%, raw materials for 30%, and other expenses for 18%.

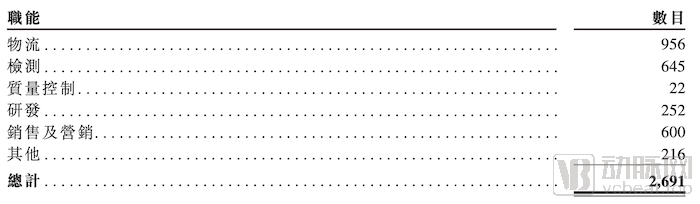

First, by cross-referencing the employee headcount across Kingstar Global’s various business lines provided in another table, we can preliminarily conclude that there is limited room to reduce personnel costs within its cost of sales. Based on the personnel costs constituting the cost of sales in 2019, the average annual salary for Kingstar Global’s testing staff was RMB 144,000. Given that specialized clinical tests are more complex and demand higher operational standards than routine tests, the testing personnel recruited by Kingstar Global typically possess strong educational backgrounds and professional experience. Furthermore, as these employees are primarily based in major cities such as Wuhan, Beijing, and Shanghai, it is unrealistic to expect further reductions in personnel costs.

Distribution of KingMed Diagnostics Personnel (Source: Prospectus)

Kingstar Global’s Personnel Costs (Data Source: Prospectus; Table by VCBeat)

As for outsourcing costs and raw materials, it is necessary to consider Kindstar Global’s pricing power within the industry chain. Clues can be found in Kindstar Global’s prospectus, which indicates that its gross profit margin is constrained by the economies of scale of its business, suggesting limited room for cost compression. Thus, it will be difficult to increase the gross profit margin in Kindstar Global’s traditional core businesses in the short term. The prospectus does not provide detailed data on whether increasing investment in the new translational medicine business will boost the gross profit margin; we speculate that it may be beneficial, after all, the translational medicine business differs significantly from clinical laboratory services in terms of human, financial, and resource inputs, as well as settlement methods and payment terms.

As disclosed in the prospectus, KingMed Diagnostics has completed multiple rounds of financing, with institutional shareholders including more than ten well-known domestic and international institutions such as CPE (CITIC Private Equity Funds), KPCB, Bank of China International, Agricultural Bank of China International, Investcorp, Top Group, Morningside Venture Capital, Ruifu Healthcare Fund, and United Capital. Among them, Ruifu Healthcare Fund, Morningside Venture Capital, and CPE hold 13.83%, 13.41%, and 11.83% of KingMed Diagnostics’ shares, respectively, making them the company’s major institutional investors.

In fact, Mayo Clinic, the global leader in third-party testing, has long been on the investor list of Kindstar Global, while currently hottest investment firms such as Sequoia Capital and Hillhouse Capital missed out on investing in Kindstar Global.

In 2011, when KingMed Diagnostics completed its $11 million Series B financing round, Mayo Clinic invested $3 million in cash, establishing a strategic partnership with the latter becoming KingMed’s technical partner. This marked Mayo Clinic’s first investment outside its home country in its over 150-year history, propelling KingMed Diagnostics to rapid prominence among major investors.

Huang Shi’ang once stated to the media that as its Series B financing was nearing completion, Kingstar Global received a valuation assessment of $70 million and a Series C investment offer from Sequoia Capital. Kleiner Perkins followed with an $80 million valuation, while Hillhouse Capital offered a valuation of $90 million. Kingstar Global ultimately chose Kleiner Perkins, prompting Sequoia and Hillhouse to withdraw.

The intensive influx of capital once plunged Kingstar Global into a crisis of “forced maturation.” As investors pressured the company to list in the United States as soon as possible, the original 2013 corporate target set by Huang Shi’ang’s team—which mirrored the 2012 goal of doubling performance year-over-year to achieve 100% growth—was adjusted to an annual performance growth rate of 200%. Furthermore, since U.S. investors prioritize corporate growth potential over profitability, Kingstar Global launched sweeping reforms to accommodate the rapid expansion of its business scale.

For instance, the company enhanced compensation and benefits packages, doubled salaries, and aligned its operational practices with modern corporate governance standards. In 2013, Kingstar Global recruited nearly 400 new management and sales professionals to accelerate the improvement of operational efficiency and the development and promotion of new products.

However, hidden concerns quickly emerged. At the execution level, new regulations and management standards encountered obstacles. The integration between new hires and the local team was not as close or harmonious as anticipated. Significant differences existed between the legacy and new teams in terms of goal alignment and project implementation approaches. Coupled with continued losses and revenue growth falling short of expectations, these issues led Huang Shiang to decide on an immediate termination of the transformation initiative.

Over the past four to five years, Kingstar Global has slowed the pace of its business expansion and capitalization. Huang Shiang, who has gained a deeper understanding of operational management, also recognizes that incremental development is more suitable for Kingstar Global. He advocates aligning management approaches with different stages of growth—for instance, avoiding premature increases in compensation packages when sales performance cannot yet support them—and notes that a “loss-leading” strategy is not applicable.

In the context of precision medicine, the number of market participants in the independent clinical laboratory sector is increasing. As more medical institutions transition into research-oriented hospitals, debates over whether independent clinical laboratories constitute a sustainable long-term business have persisted, placing immense pressure on all entities operating within this space. Having weathered a trough in its business performance, Huang Shiang, founder of Kingstar Global, should have a deeper appreciation of how critical IPO decisions are to an enterprise. Although profitability and new growth drivers are still struggling to take root, perhaps the market should afford this independent clinical laboratory—once a beacon of hope in the early stages of the fight against COVID-19—a stronger starting point for its next chapter.

Writing Reference:

KingMed Diagnostics Prospectus

KingMed Diagnostics: The “Special Forces” of Medical Testing Aims to Be World No. 1

KingMed Diagnostics Lists in Hong Kong: Offers Over 3,500 Test Items, with COVID-19 Testing Revenue Reaching Approximately RMB 100 Million in the First Three Quarters of 2020

Capital Influx Sends KingMed Diagnostics on a Roller-Coaster Ride