SciClone Pharmaceuticals Debuts on HKEX, Powered by 'Wonder Drug' Zadaxin and Backed by Chinese Consortium Buyout

On the morning of March 3, Siniopharm (06600.HK) recorded its first trade on its debut day at the Hong Kong Stock Exchange, with a transaction price of HK$18.5, slightly lower by HK$0.3 than the previously determined IPO price of HK$18.8. On its first day of listing, Siniopharm closed at HK$18.72, down 0.96% from the opening price, with a market capitalization equivalent to RMB 10.58 billion.

Scienjoy Biopharma’s Intraday Stock Performance on First Day of HKEX Listing (Data Source: Xueqiu))

In fact, SciClone Pharmaceuticals demonstrated strong performance during its IPO period, securing subscription oversubscriptions of 10 times from institutional investors and 1,068.05 times from retail investors, with the final offer price set at the top end of the indicative range. However, the momentum shifted in the pre-market grey market trading prior to the official listing day. According to Futu’s grey market data, SciClone Pharmaceuticals’ shares rose by nearly 7% at their peak but closed with a modest gain of only 2.02%.

In May 1990, SciClone US, the predecessor of SciClone Pharmaceuticals, was founded in California, USA, by two founders, Thomas E. Moore and Nelson M. Schneider, and listed on the NASDAQ market two years later. At its inception, SciClone US operated primarily as a Contract Sales Organization (CSO).

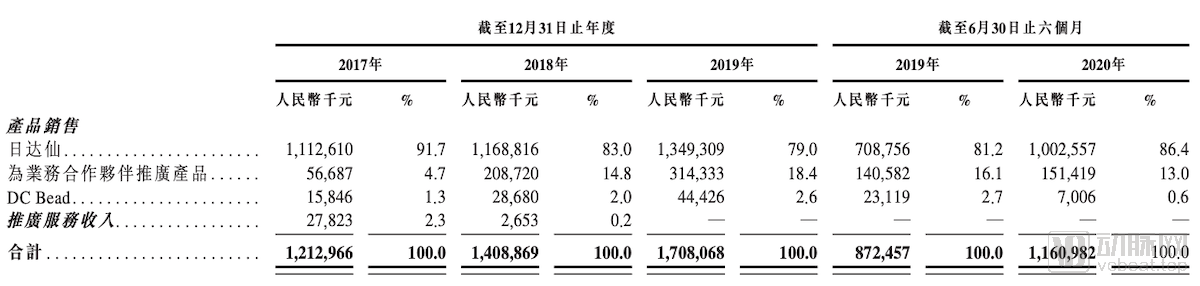

Since 2002, SciClone US’s flagship product, Zadaxin, has been approved for marketing in more than 30 countries, including Italy and China. According to the prospectus, Zadaxin accounted for 91.7%, 83%, and 79% of Sino Biopharmaceutical’s operating revenue from 2017 to 2019, respectively.

Zadaxin is an immunomodulator containing thymosin alpha-1, indicated as an immune enhancer for patients with chronic hepatitis B and those with compromised immune function. In certain clinical guidelines, Zadaxin is also listed as a therapeutic agent for sepsis, pancreatic cancer, liver cancer, and COVID-19. In China, Zadaxin played a role in the treatment of SARS in 2003 and COVID-19 in 2020; it was included by the National Health Commission and the National Administration of Traditional Chinese Medicine in the treatment protocols for severe and critical cases of COVID-19. In terms of revenue, Zadaxin accounted for 44.1% and 57.5% of the domestic market share of thymosin alpha-1 in 2015 and 2019, respectively.

In addition, SciClone Pharmaceuticals’ revenue streams include sales of licensed-in products and third-party pharmaceutical promotion services. Among the licensed-in products are Zometa, a treatment for bone metastases in solid tumors licensed from Novartis, and Angiox, a PCI anticoagulant licensed from The Medicines Company. Its pharmaceutical promotion service clients are primarily Pfizer and Baxter.

It is understood that the largest portion of the funds raised will be invested in potential drug assets in China or other global markets. SciClone Pharmaceuticals will continue to screen for investment opportunities in candidate drugs for oncology and severe infections, creating synergies with its existing pipeline and commercialization capabilities. Another portion of the funds will be used for the development and commercial operations of clinical-stage candidate products.

SciClone Pharmaceuticals’ HKEX Listing Bell-Ringing Ceremony (Image source: Provided by the interviewee)

After 15 years of trading on the NASDAQ, SciClone US was delisted in October 2017. At that time, SciClone US was valued at $605 million. Based on real-time exchange rates from the Hong Kong Stock Exchange, Sinocare’s market capitalization on the Hong Kong stock market was approximately $1.6 billion equivalent. From this perspective, Sinocare has achieved growth through its exit from and re-entry into the capital markets.

On June 7, 2017, Silver Biotech, a buyer consortium initiated by Top Glory Capital and comprising BOC International Investments, CDH Investments, Shangda Capital, and Boying Investment, entered into a merger agreement with SciClone US to acquire all of its outstanding common shares at a cash consideration of $11.18 per share. This agreed price represented an 11% premium over SciClone US’s closing price on its last trading day on the NASDAQ, and a 16% premium over the weighted average of its closing prices for the preceding 10 trading days.

Following the completion of the acquisition, SciClone US was delisted and continued to exist as a subsidiary of Silver Biotech. Regarding the delisting, Jon S. Saxe, then Chairman of the Board of Directors of SciClone, merely downplayed the matter by stating that the Board’s decision to sell the company represented the most opportune moment to maximize shareholder value.

In reality, there is a simple logic behind this acquisition. Although SciClone US’s growth strategy had been performing well, Zadaxin’s primary indication—chronic hepatitis B—has a low incidence rate in the United States but a high one in China. As a result, SciClone US’s core business was heavily dependent on the Chinese market. Continuing to operate as an independent U.S.-listed company would not have been conducive to sustaining strong long-term growth for SciClone US. After weighing the challenges and benefits of continued independent operation, SciClone US’s board of directors chose to sell the company to a Chinese consortium, accepting a premium acquisition offer.

Nearly two decades after its market launch, Zadaxin’s sales are approaching their peak. However, since 2018, SciClone Pharmaceuticals has witnessed a new surge in revenue generated from Zadaxin.

Between 2017 and 2019, Zadaxin achieved sales revenues of RMB 1.126 billion, RMB 1.168 billion, and RMB 1.349 billion, respectively, with a compound annual growth rate (CAGR) of 10.1%. According to Frost & Sullivan statistics, the total sales revenue of various thymosin alpha-1 products in China amounted to approximately RMB 2.4 billion in 2019, with a CAGR of around 3.5% from 2015 to 2019. This indicates that even after being hailed as a “miracle drug” for many years, Zadaxin’s revenue-generating capability still far exceeds that of other similar products on the market.

SciClone Pharmaceuticals Financial Data (Source: Prospectus)

Further analysis reveals that, to a certain extent, the new growth driver for Zadaxin stems from the prescription outflow exploration initiated by SinoCellTech in collaboration with its distributor, Sinopharm Group.

In China, Sinopharm serves as the importer and distributor of Zadaxin. After procuring Zadaxin from SciClone Pharmaceuticals, Sinopharm is responsible for customs clearance in China and further distributes the product to hospitals and pharmacies. As of June 30, 2020, Sinopharm helped SciClone Pharmaceuticals sell Zadaxin across 31 provinces, municipalities, and autonomous regions in China. The distribution network for Zadaxin covered approximately 1,340 tertiary hospitals, 2,220 secondary hospitals, 690 pharmacies, and 4,860 other medical institutions throughout the country.

Since 2015, SciClone Pharmaceuticals has collaborated with Sinopharm Group to pilot a Go-to-Patient (GTP) platform, aiming to expand the sales distribution of Zadaxin from hospitals to pharmacies and enhance patient accessibility. The GTP platform began generating sales revenue for SciClone Pharmaceuticals in 2018. According to the prospectus, in the second quarter of 2020, sales volume through the GTP platform accounted for more than 50% of Zadaxin’s total sales volume.

Originating from the need for pharmacies to provide value-added drug delivery services to patients and gradually expanding to cover various internet-based medical services, the GTP platform has enabled SciClone Pharmaceuticals to partially bypass hospitals and reach patients through a new sales network.

GTP Model Diagram (Source: Prospectus)

Specifically, under the traditional prescription model, patients consult physicians at hospitals and purchase Zadaxin based on prescriptions. In contrast, under the GTP model, after registering on SciClone Pharmaceuticals’ online immunology portal, patients have two options. First, they can upload prescriptions obtained during physician consultations, order Zadaxin online, and have it delivered by DTP pharmacies. Second, they may also purchase Zadaxin directly from DTP pharmacies.

The GTP model establishes connections among patients, physicians, hospitals, pharmacies, and SciClone Pharmaceuticals. For patients, the GTP model offers more flexible options for purchasing Zadaxin, thereby improving its accessibility. For physicians and hospitals, the GTP model separates medical services from drug sales, enabling physicians to focus more on diagnosing and treating patients’ conditions. For pharmacies, the GTP model significantly increases revenue from drug sales. For SciClone Pharmaceuticals, the GTP model expands the sales reach of Zadaxin from hospitals to pharmacies, diversifying sales channels while maximizing patient coverage.

In its prospectus, SciClone Pharmaceuticals stated that the GTP model is gaining increasing popularity among patient populations, thereby enhancing customer loyalty. During the post-listing press Q&A session, Zhao Hong, Executive Director, President, and CEO of SciClone Pharmaceuticals, introduced that the GTP model has been integrated with internet healthcare platforms to provide online medical services to patients. Unlike mainstream platform-based internet healthcare companies, the GTP model leverages established doctor-patient relationships formed through offline consultations, resulting in more targeted online interactions. Furthermore, SciClone Pharmaceuticals has established partnerships with oncology big data companies such as Sipei and LinkDoc. Moving forward, SciClone Pharmaceuticals aims to replicate the success achieved with Zadaxin under the GTP model across its other products.

Furthermore, SciClone Pharmaceuticals is striving to expand the indications for Zadaxin. Zhao Hong stated that as the medical community’s understanding of the human immune system deepens, Zadaxin is likely to be incorporated into new treatment regimens for a broader range of conditions, including cancer and severe infections. He revealed that SciClone has been collaborating with clinical experts on research into new scenarios for Zadaxin as both monotherapy and combination therapy, such as combining it with PD-1 inhibitors for cancer treatment and augmenting the efficacy of COVID-19 vaccines. New research findings will be released in due course.

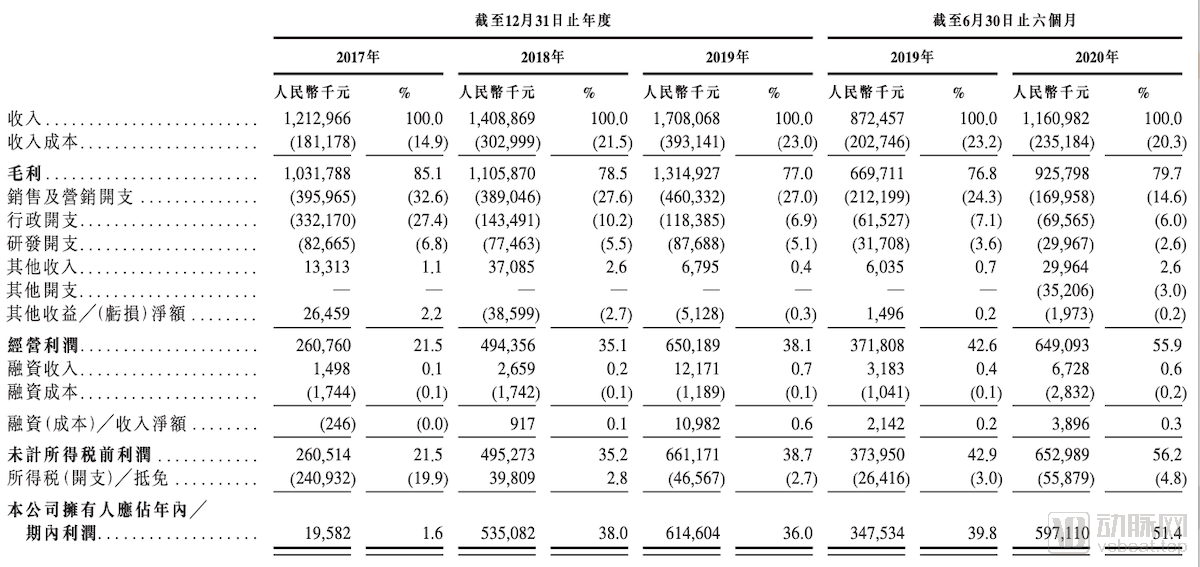

People often liken Sinocare Pharma to a second Simcere Pharmaceutical, as both exhibit the characteristic transition from traditional pharmaceutical companies to innovative drug developers. However, when evaluated by R&D investment, Sinocare Pharma’s innovation capabilities may still require improvement.

SaiSheng Pharmaceutical Financial Data (Source: Prospectus)

According to the prospectus, Siniopharm’s total R&D expenditures amounted to RMB 82.7 million, RMB 77.5 million, RMB 87.7 million, RMB 31.7 million, and RMB 30.0 million in 2017, 2018, 2019, and the first six months of 2019 and 2020, respectively, representing 6.8%, 5.5%, 5.1%, 3.6%, and 2.6% of total revenue for the corresponding periods.

Zhao Hong pointed out that SiniCare’s current low R&D investment is a choice aligned with the company’s R&D strategy. In new drug development, SiniCare currently primarily adopts the approach of in-licensing relatively mature pipelines from biotechnology companies, thereby avoiding earlier-stage R&D expenditures. Pan Rongrong, CFO of SiniCare, further explained that the R&D spending recorded in the prospectus was mainly allocated to clinical studies for in-licensed product pipelines. Looking ahead, SiniCare plans to advance 2–3 new drugs into clinical trials annually. As its pipeline under development continues to expand and its IND (Investigational New Drug) team is further strengthened, the proportion of R&D expenditure is expected to increase in the future.

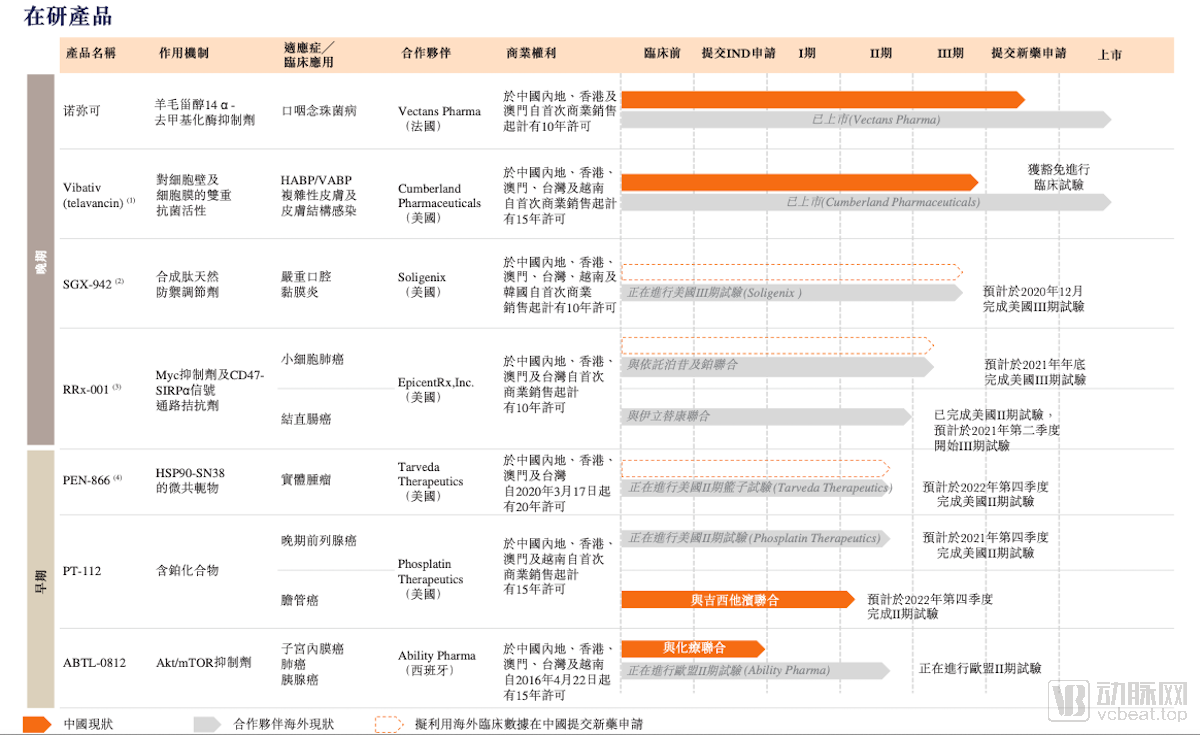

Currently, SciClone Pharmaceuticals has developed a diverse portfolio of potential drug candidates at various stages of development. As of the submission of its prospectus, SciClone’s pipeline comprised seven drug candidates, including four late-stage assets that have entered Phase III clinical trials or later stages, and three early-stage products that have entered Phase II clinical trials.

SciClone Pharmaceuticals’ Pipeline Under Development (Data Source: Prospectus)

The four products in Phase III clinical trials or later stages are Nuomike (introduced from Vectans Pharma), Vibativ (introduced from Cumbed and Pharmaceuticals), SGX-942 (introduced from Soligenix), and RRx-001 (introduced from EpicentRx). Sinocelltech holds 10- or 15-year marketing rights for these drugs in China, South Korea, and other regions.

Nuomike is a miconazole buccal tablet (MBT) for the treatment of oropharyngeal candidiasis (OPC), which has already been marketed in regions outside those licensed to SciClone Pharmaceuticals. Nuomike exhibits broad-spectrum antifungal activity against the most commonly observed Candida species in OPC, including Candida glabrata, Candida krusei, and Candida tropicalis. Furthermore, MBT can maintain sustained high concentrations of miconazole in saliva, thereby reinforcing its role as an alternative topical therapy for OPC. Currently, SciClone Pharmaceuticals has completed the registration trials for Nuomike, passed the data verification for sampling tests by the National Medical Products Administration (NMPA) in September 2019, and submitted the additional required data for relevant technical review in June 2020. It is expected to receive approval for market launch in mainland China soon.

Vibativ (telavancin) is a once-daily, rapidly bactericidal lipoglycopeptide antibiotic approved in the United States and Canada for the treatment of adult patients with hospital-acquired and ventilator-associated bacterial pneumonia (HABP/VABP) caused by susceptible isolates of Staphylococcus aureus. Vibativ demonstrates activity against a range of clinically relevant Gram-positive pathogens. In August 2018, Sinocelltech obtained approval from the Center for Drug Evaluation (CDE) to conduct clinical trials. Subsequently, Sinocelltech needs to first establish/define local pathogen resistance/susceptibility breakpoints, and then determine whether small-scale bridging studies are required based on the test results.

SGX-942 is an innate immune modulator for the treatment of severe oral mucositis. It inhibits the release of inflammatory cytokines by binding to the p62 protein in immune cells, without impairing the immune system’s ability to clear damaged cells or affecting the normal function of the adaptive immune system.

Currently, there are no approved drugs worldwide for the treatment of oral mucositis in patients with solid tumors, yet many patients with head and neck cancer are at risk of developing severe oral pain. In a Phase II study of SGX-942 involving 111 patients with head and neck cancer, the product demonstrated a 67% reduction in the median duration of oral mucositis among patients receiving the recommended chemoradiotherapy regimen. On June 24, 2020, SciClone Pharmaceuticals completed patient enrollment for the pivotal Phase III DOM-INNATE trial, which evaluates SGX-942 for the treatment of oral mucositis in patients with oral and oropharyngeal squamous cell carcinoma undergoing chemoradiotherapy; primary endpoint data are expected to be announced soon. Furthermore, SciClone Pharmaceuticals plans to initiate clinical trial registration in China upon completion of its overseas clinical trial registrations.

RRx-001 is a well-tolerated, next-generation small-molecule immunotherapy that targets the CD47–SIRPα axis for the treatment of various solid tumors. In June 2019, the British Journal of Cancer published data on small-cell lung cancer (SCLC) from patients in the third-line and further-treated cohorts of the Quadruple Threat phase II study. The data demonstrated that administering RRx-001 following rechallenge with platinum plus etoposide chemotherapy was feasible and yielded satisfactory outcomes. It is understood that Sinocelltech has initiated a randomized phase III trial named REPLATINUM, comparing the efficacy of platinum plus etoposide therapy administered after RRx-001 versus standard-of-care chemotherapy in patients with third-line or later SCLC.

Founded 32 years ago and delisted for four years, SciClone Pharmaceuticals has returned to the public markets, yet its financial performance remains heavily reliant on Zadaxin. As it transitions into an innovative pharmaceutical company, SciClone possesses a first-mover advantage in commercialization capabilities; however, establishing robust clinical translation capabilities may be the key to sustaining business growth.

Writing Reference:

SciClone Pharmaceuticals "Prospectus"

Drug Brief: SciClone Pharmaceuticals Acquired by Chinese Consortium—What’s Your Take?

Press Release: SciClone Pharmaceuticals Listed on the Main Board of The Stock Exchange of Hong Kong Limited