Amid Sector-Wide Sell-Off from Volume-Based Procurement, How Can Orthopedic Companies Forge a Second Growth Curve?

A student once asked the renowned anthropologist Margaret Mead a question: What exactly is the earliest sign of human civilization? Many students guessed answers such as fishhooks, stone tools, and fire. However, Mead stated that the earliest sign of human civilization is our discovery of “a femur that has been broken and then healed.”

The healing of femoral fractures signifies that humans began to understand how to assist their fellow beings in times of need. The treatment of bone injuries, a hallmark of human civilization, has evolved into a global market worth tens of billions of dollars. This high-volume, highly diversified market has become a fiercely contested arena for medical device giants, with the orthopedics sector frequently witnessing large-scale mergers and acquisitions. In 2014, Johnson & Johnson acquired Synthes for $19.7 billion; Medtronic previously acquired Kanghui Medical for $816 million; and in 2014, MicroPort Scientific Corporation acquired Wright Medical Group’s joint reconstruction business for $290 million.

However, the once-booming orthopedics market hit its darkest hour in 2020. Observing the stock price trends of domestically listed orthopedic companies,Since the second half of 2020, the orthopedics sector has experienced uninterrupted sharp declines, wiping out hundreds of billions in market capitalization.

The share price of Double Medical has halved, dropping from RMB 119.78 on June 30, 2020, to RMB 47.60 by March 10, 2021, with its market capitalization shrinking by more than half to just RMB 19.146 billion. Similarly, the share price of Kellytai fell from RMB 30.64 on July 13, 2020, to RMB 10.02 by March 10, 2021, leaving its market capitalization at only RMB 7.244 billion. Chunli Medical’s share price declined from HKD 63 on July 13, 2020, to HKD 19.280 by March 10, 2021, with its market capitalization standing at merely HKD 6.668 billion.

Alongside the continued decline in stock prices, institutional investors have been reducing their holdings. Morgan Stanley reduced its stake in Chunli Medical (01858-HK) by 54,825 shares. The number of funds holding positions in Double Medical Technology fell from 213 in the second quarter of 2020 to just 11 in the third quarter of 2020. Hillhouse Capital, which had increased its stake in AK Medical by 50 million shares for RMB 350 million in 2019, also reduced its holdings in AK Medical during the second quarter of 2020.

VCBeat, after conducting research,The primary cause behind the sharp decline is the pessimistic sentiment triggered by expectations of centralized procurement.The decline in the stock prices of leading orthopedic companies coincided with the period from the issuance to the implementation of China’s nationwide volume-based procurement (VBP) policy for high-value medical consumables. Although the first round of VBP did not include orthopedic products, leading orthopedic firms had already felt the disruptive impact of VBP during the centralized procurement of coronary stents.

We believe that the impact of volume-based procurement on the orthopedics industry will extend beyond stock prices. Volume-based procurement is not merely a phenomenon-level event; it will bring systemic opportunities to the entire industry.

Discussing the impact of volume-based procurement (VBP) on the orthopedics industry at this particular moment holds special significance. On one hand, coronary stents subject to VBP have already entered clinical use, transforming the impact of VBP from mere prediction into established fact, thereby offering valuable references for VBP in the orthopedics sector. On the other hand, the national results of VBP for orthopedic products are expected to be finalized in May and June this year. On the eve of this critical policy implementation, leading orthopedic companies such as Weigao Orthopaedics (whose IPO has passed review) and Chunli Zhengda (whose IPO application has been accepted) are reaching a crucial stage in their bids for listing on the STAR Market. Analyzing VBP, the most significant variable facing the future orthopedics landscape, will help us better understand the potential of these industry leaders.

Not long after the first round of centralized procurement was implemented, the list for the second round of medical consumables procurement was quickly leaked. Among the six major categories—artificial hip joints, artificial knee joints, defibrillators, occluders, orthopedic materials, and staplers—orthopedic products are the key focus. Currently, centralized procurement for orthopedics is imminent; industry insiders predict that the results will be implemented in May or June this year.

The National Healthcare Security Administration (NHSA) has conducted intensive research on the centralized procurement of orthopedic products. From February 22 to 23, Hu Jinglin, Director of the NHSA, visited Sichuan Province to conduct field investigations at West China Hospital, West China School of Stomatology Hospital, and Sichuan Provincial Orthopedic Hospital, examining the procurement, management, and utilization of medical consumables in orthopedics and dentistry. He also solicited perspectives from provinces, autonomous regions, and municipalities—including Sichuan, Jiangsu, Inner Mongolia, and Tianjin—on deepening the volume-based procurement of high-value medical consumables, as well as feedback and recommendations from healthcare institutions.

From February 25 to 26, Chen Jinfu, Deputy Director of the National Healthcare Security Administration, conducted field visits to the Tianjin Medical Device Quality Inspection Center and Zhengtian Medical Device Co., Ltd. to assess the production and distribution of orthopedic consumables and to solicit feedback and recommendations from the enterprises.

Why Has Orthopedics Become the Second Target of the National Healthcare Security Administration Following Cardiac Stents? The Reason Lies in the Many Similarities Between Orthopedic Artificial Joints and Cardiac Stents:High national consumption, high prices, and high gross margins; the sector is already characterized by robust competition, has given rise to several large domestic integrated companies, and locally manufactured products hold a certain market share.

In terms of surgical volume, the total number of joint replacement surgeries in China approached 700,000. According to data from the Chinese Medical Doctor Association, in 2018, there were 439,324 total hip arthroplasties, 249,259 total knee arthroplasties, and 11,200 unicompartmental knee arthroplasties performed in China.In China, the volume of PCI procedures also reached approximately 700,000 cases in 2017.

Meanwhile, according to data from the American Academy of Orthopaedic Surgeons (AAOS), there were 370,770 hip replacement surgeries and 680,150 knee replacement surgeries in the United States in 2014, totaling over one million procedures. The penetration rate of artificial joint surgeries in China remains relatively low. With the aging population and improvements in living standards, the volume of joint replacement surgeries is expected to continue rising.

In addition to high volume, artificial joints, like coronary stents, have significant room for price reduction.

Regarding centralized procurement in orthopedics, the primary concern remains the magnitude of price reductions. The price of coronary stents under centralized procurement dropped from over ten thousand yuan to just a few hundred yuan, with the reduction rate under national volume-based procurement significantly exceeding the lowest prices previously seen in local volume-based procurement initiatives. Will such drastic price cuts, breaking through even the “floor price,” be repeated in the orthopedic sector? We believe that, at least in terms of gross margin and cost structure, artificial joint prices have substantial room for compression, similar to cardiac stents.

First, similar to coronary stents, orthopedic artificial joints also have significant room for profit margin compression, with the gross profit margin in the orthopedic industry generally exceeding 60%.In 2019, Double Medical’s overall gross profit margin was 85.61%; Kinetic Medical’s overall gross profit margin was 65.74%; and AK Medical’s overall gross profit margin was 69.41%.

From the perspective of specific products, artificial joint products, which are subject to volume-based procurement, have a gross profit margin of 70%-80%. Data from the prospectus submitted by Weigao Orthopaedics to the STAR Market show that in 2019, the gross profit margin for its spinal products was 90.95%, for trauma products 83.83%, and for joint products 66.19%.

Data disclosed in Chunli Medical’s prospectus shows that the gross profit margin for standard hip prostheses is 73.30%; for standard knee prostheses, 81.18%; for standard shoulder prostheses, 90.94%; for customized joint prosthesis products, 90.25%; and for spinal implants, 72.26%.

Overall, products with higher gross profit margins are primarily knee and shoulder joint prostheses, which feature smaller sizes and relatively complex design and manufacturing processes, resulting in slightly higher gross margins compared to hip joint prostheses. In addition, customized products require patient-specific design and entail longer production cycles, thereby achieving even higher gross profit margins.

The gross profit margin of artificial joint products is relatively lower than that of spinal and trauma products, partly due to the large number of domestic brands in the joint sector, which has led to intense industry competition.

What Is the Price Floor for Orthopedic Artificial Joints? According to data from Chunli Medical’s prospectus, the gross profit margin for Chunli Medical’s standard hip prostheses was 70.54% in the first half of 2020, while the ex-factory unit price for standard hip prostheses during the same period was RMB 1,390.24. Based on these figures, there is room for price reduction in artificial joint prostheses.

Significant markups exist between the ex-factory price and the listed online procurement price. In the centralized procurement of high-value orthopedic joint medical consumables conducted by the Qinghai Provincial Public Medical Institutions Procurement Alliance, data on the current lowest national supply prices to medical institutions for selected imported and domestically produced products were published. Among the published current lowest prices for domestically produced products, the cast cobalt-chromium-molybdenum alloy femoral condyle component of the artificial knee joint from Weigao Haixing (Weigao Orthopaedics’ mid-to-high-end joint brand) was priced at RMB 26,500, and the femoral stem (biological/cemented type) in the artificial hip joint prosthesis was priced at RMB 22,900. The artificial knee joint from the imported manufacturer Stryker reached a price of RMB 46,966, while Johnson & Johnson’s unicompartmental knee system was priced at RMB 28,000.

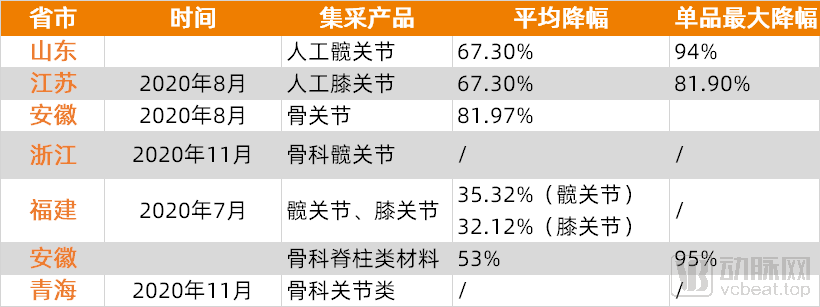

Furthermore, data from provinces such as Anhui, Zhejiang, Jiangsu, and Fujian, which have already implemented volume-based procurement (VBP) for orthopedic consumables, show that the maximum price reduction for individual products has exceeded 90%. It is foreseeable that with the further implementation of the VBP policy, the entire orthopedic industry faces a significant risk of substantial declines in terminal prices.

Regardless of how volume-based procurement drives prices to rock-bottom levels, orthopedics remains a substantial market in China, with nearly 700,000 joint replacement surgeries performed annually. The primary concern regarding volume-based procurement is not so much about how it slashes prices to their lowest possible point, but rather which manufacturers will emerge as losers from this competitive dynamic and how such procurement policies will reshape the industry’s rules.

“Volume-Based Procurement” Policy: The Core Is “Exchanging Volume for Price,” Where Manufacturers Lower Prices and Healthcare Institutions Guarantee Purchase Volumes. The Implementation of This Policy Will Have a Significant Impact on Sales Models, Product Pricing, and Market Share.

In the orthopedics sector, the most significant impact of centralized procurement has been to drive industry consolidation and increase market concentration.

Overall, China’s orthopedic medical device industry remains at a lower-middle level in terms of technological capability. Domestic enterprises still need to improve their technical proficiency in product design, raw material processing, manufacturing processes, surface treatment, and instrument fabrication. Due to a later start, there is a notable gap between the technological standards of China’s orthopedic medical device sector and those of leading international manufacturers, with imported products continuing to dominate the market.

According to relevant reports from Biaodian Information, the top five companies in China’s overall orthopedic implant medical device market in 2019 were Johnson & Johnson, Medtronic, Zimmer, Stryker, and Weigao Orthopaedics, with market shares of 17.24%, 9.70%, 5.97%, 5.19%, and 4.61%, respectively. Among these, the top five companies in China’s joint implant medical device market were Zimmer Biomet, Johnson & Johnson, AK Medical, Chunli Medical, and Link Orthopaedics.

A founder of an orthopedic company stated, “Over the past decade, domestic orthopedic companies have captured hospitals in second- and third-tier cities across China by adopting a ‘rural-encircling-urban’ strategy. However, imported products still dominate Class A tertiary hospitals in first-tier cities, where surgical volumes are highly concentrated.”

From the perspective of sub-sectors, the four major segments in orthopedics are trauma, spine, joints, and sports medicine. Among them, trauma is the largest segment, accounting for 29.80%; spine ranks second with a share of 28.23%; and joints rank third, representing 27.77%.

In the trauma sector, the gap between domestically produced and foreign companies in terms of product variety and quality is relatively small. However, given the wide range of orthopedic trauma product categories, a comprehensive assortment of specifications is required, which places high demands on distributors’ liquidity. Foreign companies hold greater advantages over their domestic counterparts in distributor management, engagement with key academic hospitals across China, inventory optimization, and allocation of surgical instruments. In contrast, in the higher-end spinal and joint segments, which involve greater technological complexity, imported enterprises continue to dominate, particularly in the joint segment, where the level of localization remains low.

In addition to being dominated by imported products, another hallmark of this market is the prevalence of small and medium-sized enterprises (SMEs), resulting in low industry concentration. An industry insider noted that the five-firm concentration ratio (CR5) in the trauma care sector is below 40%, whereas in the United States, a single company can capture more than 40% of the market.

Volume-based procurement will undoubtedly force industry consolidation, transforming the current fragmented, disordered, small-scale, and heterogeneous landscape of the medical device sector. This shift will foster brands with international influence capable of competing globally, benefiting leading manufacturers with substantial operational scale and top industry rankings.

In addition to forcing industry consolidation, volume-based procurement (VBP) will also transform the business model of the orthopedics industry, shifting from a distributor-dominated model to one primarily based on direct sales. In the short term, adapting to this shift will subject orthopedic companies to a period of painful transition. One of the objectives of centralized medical procurement is to reduce distribution channel costs and lower marketing expenses for orthopedic firms. However, VCBeat has observed that after eliminating distributors, orthopedic companies have experienced an increase, rather than a decrease, in their sales expenses.

The reason is that, under the distribution model, distributors often provide intraoperative support services while selling products to hospitals. They undertake channel development and customer maintenance, and deliver specialized professional services for orthopedic products to end customers, including preoperative consultation, logistics assistance, intraoperative guidance, cleaning and sterilization, and postoperative follow-up, thereby maximizing the fulfillment of surgeons’ operational needs.

Under the volume-based procurement (VBP) model, selected products are expected to be sold directly to hospitals, with corresponding distributors determined as needed for logistics. Consequently, the company’s customer structure will shift from being predominantly composed of distributors to being primarily comprised of healthcare institutions such as hospitals. Under the direct sales model, the company needs to procure services—such as preoperative consultation, intraoperative technical support, cleaning and sterilization, and postoperative follow-up—directly from service providers. According to data from Weigao Orthopaedics’ prospectus, the proportion of its direct sales model has continued to rise following the implementation of the “Two-Invoice System,” leading to an increase in Weigao Orthopaedics’ sales expenses from 33.93% in 2017 to 40.25% in 2019.

Although some have questioned that centralized procurement has squeezed profit margins and will affect the subsequent R&D investment of orthopedic companies, an industry insider stated that the competitive landscape among leading domestic enterprises in the orthopedics sector remains stable. Moreover, major companies possess strong financial strength, are all publicly listed, have certain R&D reserves and diverse product portfolios, have moved beyond reliance on single-product lines, and thus demonstrate a high capacity for risk resistance.

However, deeper price cuts are not necessarily better. A secondary-market securities analyst noted that a 70% reduction would bring prices roughly in line with those for orthopedic consumables abroad. Excessively steep price reductions in China offer little benefit to patients, physicians, or industry development, and may even lead to higher healthcare insurance expenditures in the long run.

Looking back on over two decades of development in orthopedics, China’s orthopedic industry has cultivated a cohort of market leaders. The sector has moved beyond an era of disordered growth, with competition among enterprises becoming more comprehensive. The key challenge for the industry has long been how to evolve from leading players in niche segments within China to globally competitive, diversified leaders; how to transition from offering single products to providing diverse solutions; and how to establish multiple growth engines. Volume-based procurement has merely accelerated this inherent trajectory.

Through desk research and interviews, we have categorized the attempts by domestic orthopedic companies to identify new business growth drivers into three types: first, expanding product portfolios through mergers and acquisitions; second, increasing R&D investment to position themselves in higher-end orthopedic products and emerging technologies, such as orthopedic surgical robots and 3D printing.

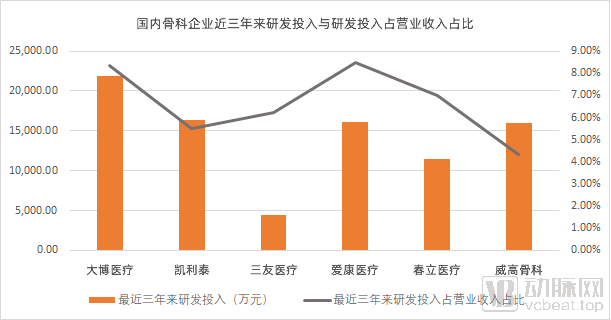

Let us first examine R&D investment, which serves to solidify the foundational capabilities of companies. Over the past three years, the R&D expenditure of major domestic orthopedic enterprises has accounted for less than 10% of their operating revenue, indicating that both capital scale and R&D investment remain relatively small. China’s orthopedic industry is still in a relatively early stage of development, and there are numerous technological gaps that domestic leading orthopedic companies must address to catch up with their foreign counterparts.

An orthopedic manufacturer stated, “The gap between domestically produced and imported orthopedic products is smallest in the trauma segment, followed by spine. Domestic manufacturers are primarily concentrated in these two major areas. Artificial joints represent a specialized orthopedic segment characterized by high technological content, high value-added, and high entry barriers. The largest gap exists in the sports medicine field. Beyond overcoming technical bottlenecks, domestic substitution must also undergo industrialization; in some areas, technical breakthroughs have been achieved, but industrialization remains inadequate.”

From a technical perspective, domestic brands still lag behind imported products in areas such as prosthetic materials, prosthetic shape design, the precision of surgical positioning instruments, joint surface smoothness, and the treatment of bone-contacting surfaces. These gaps represent the key focus areas for R&D investment by Chinese orthopedic companies.

Taking Weigao Orthopedics as an example, its key products under development include dual-coated interbody fusion cages, unicompartmental knee implants, trabecular metal interbody fusion cages, novel 3D-printed hip joint systems, and bioinductive absorbable suture anchors. Projects with budgets exceeding RMB 10 million are primarily focused on sports medicine, joint reconstruction, and technologies for treating bone-contact surfaces.

Focusing on high-end products to fill domestic gaps is a key priority for leading orthopedic companies in China. Furthermore, we observe that these industry leaders are shifting their growth strategy from relying solely on organic growth to pursuing inorganic growth through mergers and acquisitions (M&A). M&A enables companies to bypass lengthy R&D cycles, acquire internationally advanced technologies, rapidly enter underserved market segments, and accelerate product commercialization.

Looking at the development trajectories of global industry leaders, their growth has involved significant mergers and acquisitions to consolidate strengths, address weaknesses, and gradually achieve a leading position in their respective fields.

In M&A strategies, the most closely watched sector is surgical robotics.

MicroPort Scientific Corporation made a high-profile entry into the surgical robotics sector in 2020, immediately covering five “golden tracks”: laparoscopic surgery, orthopedics, vascular intervention, natural orifice surgery, and percutaneous puncture. Weigao’s laparoscopic surgical robot had already completed 168 clinical trial cases by 2020. In 2015, Weigao also established an orthopedic surgical robotics company with a registered capital of RMB 20 million, with Weigao Group holding a 95% stake.

Major players such as Johnson & Johnson, Medtronic, and Zimmer Biomet have also entered the surgical robotics market. Chinese companies have narrowed the gap with these giants through acquisitions and R&D investments. It is anticipated that future competition in orthopedics will extend beyond the four traditional sectors—trauma, spine, joints, and sports medicine—as the field of orthopedic surgical robots becomes a new arena for competition among orthopedic companies.

While the final outcome of centralized volume-based procurement (VBP) for orthopedic products remains uncertain, the challenge for companies extends beyond merely achieving sufficiently low costs or price floors. What is truly being tested is a company’s sustained innovation capability, diversified product portfolio, and commercial prowess in both domestic and international markets. Although VBP will reshape the industry landscape, it cannot alter the inevitable emergence of a great Chinese high-value medical consumables enterprise.