BlueRun Ventures: New Entrepreneurial Opportunities in Healthcare Services Amid Industry Transformation

BlueRun Ventures China

Venture Capital Institution

From its investment cases, BlueRun Ventures China is not a trend follower but rather more akin to a trendsetter.

In 2012, before the surge in internet healthcare, BlueRun Ventures China invested in Chunyu Doctors; in 2017, it backed Shuidi Inc., strategically positioning itself early in innovative medical payment solutions; and in 2020, Baike Mingyi, an early portfolio company of BlueRun Ventures China, was acquired by ByteDance for hundreds of millions of yuan, yielding substantial returns. It is evident that BlueRun Ventures China consistently anticipates emerging trends, identifies non-consensus opportunities within industries ahead of others, and achieves significant profits through its discerning investment strategy.

Currently, BlueRun Ventures China manages multiple dual-currency funds in U.S. dollars and Renminbi, with assets under management exceeding RMB 10 billion and realized exits totaling over RMB 6 billion.

In the past two years, a flurry of national policies targeting the healthcare sector have been introduced, while innovative models and technologies in the medical field have emerged in rapid succession, attracting continued capital inflows. Driven by these multifaceted factors, China’s healthcare industry has undergone profound transformations.

Amidst the Dramatic Transformation of China’s Healthcare Industry, What New Trends Has BlueRun Ventures China, the “Trend Spotter,” Identified? Which Niche Sectors Does It Favor? What Qualities Does It Seek in Founding Teams? In This Exclusive Interview, Zhu Tianyu, Managing Partner at BlueRun Ventures China, Reveals All.

Health economics is a specialized discipline within economics. While microeconomics emphasizes supply and demand, models in health economics incorporate supply, demand, and payers. This underscores the critical role of payers in the healthcare sector.

Unlike the consumer retail industry, which typically involves only suppliers and consumers, the healthcare sector features a more diverse array of stakeholders, including suppliers (R&D and manufacturing enterprises), service providers (physicians and hospitals), payers, and beneficiaries (patients). Among these, payers include basic medical insurance, commercial health insurance, out-of-pocket payments, and, in specific contexts, pharmaceutical and medical device companies.

Zhu Tianyu stated, “A key distinctive feature of the healthcare industry is the presence of multiple payers, each with its own unique needs. Approaching issues from the perspective of these payers is what BlueRun Ventures China defines as the ‘payer perspective.’”

Since investing in Chunyu Yisheng (Spring Rain Doctor) in 2012, BlueRun Ventures China has engaged with the digital healthcare sector, successively investing in internet healthcare companies such as Xingshulin and chronic disease management firm Shuomao Technology. Through collaborative exploration and a deepening understanding of the Chinese healthcare market alongside these startups, BlueRun Ventures China has observed that in the healthcare services market, companies with significant value or stronger growth potential must prioritize the payer’s perspective; without focusing on the payer’s viewpoint, entrepreneurs will struggle to truly unlock market opportunities.

Specifically, when constructing business models, designing product forms, and exploring service models, entrepreneurs need to consider the needs of various payers and address some of these needs when delivering services or products. In addition to payers, entrepreneurs must also take into account other stakeholders, including upstream supply chains, service providers, and end-users.

Furthermore, the payer perspective holds equal significance for investment firms. Leveraging this viewpoint, investors can assess, screen, and invest in enterprises with greater value and growth potential. Accordingly, BlueRun Ventures China has adopted this perspective to examine the healthcare industry, gaining insights into its transformations, opportunities, and development trends.

As the largest payer in China’s healthcare industry, medical insurance is a core driver of transformation within the sector.

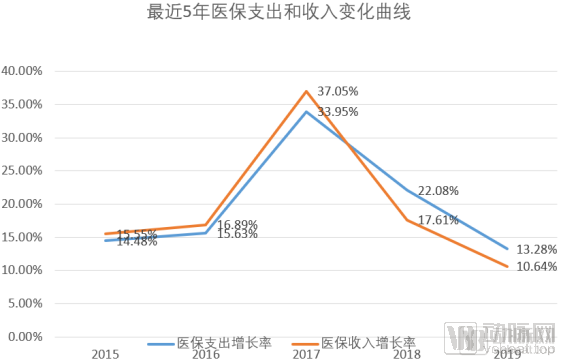

In 2018, the growth rate of medical insurance expenditures was 22.08%, while the growth rate of medical insurance revenues was 17.61%. For the first time, the growth rate of expenditures surpassed that of revenues. Without corrective measures, medical insurance expenditures were projected to exceed revenues by 2023, leading to a deficit in the operation of medical insurance funds.

Against this backdrop, the National Healthcare Security Administration (NHSA) was officially established in May 2018. Previously, healthcare insurance funds were overseen by four separate regulatory bodies; following the NHSA’s establishment, these funds were consolidated under unified management, enabling refined administration and strategic regulation. Furthermore, the NHSA has leveraged its role as a super-payer to drive transformative changes across the healthcare industry.

Since its establishment, the National Healthcare Security Administration has issued multiple landmark policies that have significantly impacted the industry, such as the “4+7” volume-based procurement pilot, the normalization of centralized drug procurement, and the centralized procurement of high-value medical consumables. These policies have been instrumental in shaping the development trajectories and strategic layouts of pharmaceutical and medical device companies.

Zhu Tianyu told VCBeat, “A key focus of this healthcare reform is to rectify the valuation of pharmaceuticals. In the past, the value of medical diagnosis and treatment was overlooked while the value of drugs was exaggerated, leading to a reliance on drug sales to subsidize medical services and distorting industry development. For instance, startups and listed companies in the healthcare sector have historically focused primarily on pharmaceuticals, medical devices, or consumables, whereas the true value of medical services has yet to be fully realized, and the potential of the medical services market remains largely untapped.”

“Now that centralized drug procurement has become routine, the value of pharmaceuticals will return to normal levels, while the true value of medical services will be fully realized. Both physicians and hospitals must consider how to improve the quality of medical services, while policymakers, the industry, and the market must recognize the true value of these services and pay accordingly. Medical services encompass not only in-hospital activities such as consultations, registration, and surgeries, but also out-of-hospital services like follow-up care and health management. ‘In other words, the medical services sector, including health management, is poised for greater and more diverse development opportunities. This is one of the key reasons why BlueRun Ventures China emphasizes the supply of high-quality, high-efficiency services from the payer’s perspective. Service is the keyword; we believe that healthcare services will constitute a larger market,’ added Zhu Tianyu.”

The realization of the value of medical services will inevitably lead to an adjustment in physicians’ compensation structures, thereby breaking the entrenched cycle of “funding healthcare through drug sales” and enabling doctors to earn reasonable income primarily through their professional medical services.

Currently, the National Healthcare Security Administration is piloting DRG (Diagnosis-Related Groups) and DIP (Big Data Diagnosis-Intervention Packet) payment models. Both DRG and DIP place greater emphasis on refined hospital management and cost control, while standardizing treatment expenses for diseases. Under these payment frameworks, healthcare institutions must manage expenditures to ensure profitability. For enterprises or institutions, cost control typically involves two approaches: reducing costs and improving efficiency. However, due to the unique nature of the healthcare industry, there is a third approach: enhancing the quality of medical services to reduce the risk of subsequent complications, thereby lowering overall expenditures. Consequently, high-efficiency, high-quality healthcare services will present significant development opportunities in the next phase.

In addition to “cutting costs” through centralized procurement, DRG-based payment, and DIP-based payment, the National Healthcare Security Administration is also alleviating pressure on the basic medical insurance fund by “broadening revenue sources,” namely by introducing new payers and encouraging the development of commercial health insurance.

Historically, in China’s healthcare expenditure structure, basic medical insurance accounted for the largest share, followed by out-of-pocket payments, with commercial health insurance representing the smallest portion. This imbalance has exposed the basic medical insurance fund to the risk of deficit and has driven many low-income households back into poverty due to illness-related expenses. In fact, while the core function of commercial health insurance is to mitigate risk volatility, its impact had been relatively limited in the past. In response, the Chinese government has promoted the development of commercial health insurance through policy, regulatory, and industrial measures, aiming to unlock its full potential.

Prior to the new healthcare reform, the medical services sector lacked a procurement party that could foster mutual benefits and win-win outcomes. With the development and widespread adoption of commercial health insurance as a new payer, it is expected to procure high-efficiency, high-quality medical services akin to foreign insurance institutions, thereby driving innovative development in pharmaceuticals and medical devices and ultimately reducing cost expenditures.Furthermore, as a purchaser, commercial health insurance will drive the development of the healthcare services industry. In turn, the healthcare services industry will indirectly reduce commercial health insurance expenditures by improving the efficiency and quality of care, thereby creating a positive, win-win cycle.

Emphasizing innovative payers and the payer perspective, BlueRun Ventures China recognized Waterdrop’s growth potential when it first engaged with the company in 2016. Consequently, in 2017, BlueRun Ventures China led Waterdrop’s Series A financing round and continued to increase its investment in subsequent rounds, becoming an investor in both Waterdrop’s Series A and Series B rounds.

“In the early stages of BlueRun Ventures’ investment, Shuidi’s business primarily consisted of ‘Shuidi Chou,’ which engaged in online fundraising, and ‘Shuidi Huzhu,’ which operated online mutual aid programs. ‘Mutual insurance, as a form of insurance, has long existed. However, in the past, challenges in building trust and a limited pool of homogeneous risks made it difficult for mutual insurance to scale. Yet, when startups began promoting the mutual aid model on the internet, new channels for information connectivity brought forth fresh possibilities,’ disclosed Zhu Tianyu. For instance, once Shuidi reaches a certain scale, it has the potential to create an innovative model that empowers existing payers, thereby potentially integrating with healthcare service providers to establish a virtuous cycle.”

Today, Shuidi Inc. has developed into two major business segments: insurance protection and medical health. The insurance protection segment includes business lines such as Shuidi Mutual Aid, Shuidi Crowdfunding, and the Shuidi Insurance Mall; the medical health segment includes business lines such as Shuidi Health and Shuidi Haoyaofu.

Currently, all businesses launched by Shuidi Inc. in the healthcare sector are in their early stages of development. However, its various initiatives—such as Shuidi Good Medicine Pay, Shuidi Health, and the Shuidi Insurance Mall within its insurance protection ecosystem—correspond respectively to four key elements of the closed-loop health management system: innovative payment and pharmaceuticals, internet-based healthcare, and insurance. “In the future, if Shuidi integrates the interfaces across its platforms, it can build a one-stop health service management platform combining ‘insurance + medical care + pharmaceuticals + innovative payment,’ becoming China’s version of UnitedHealth,” said Zhu Tianyu.

Overall, factors such as centralized procurement, medical insurance cost containment, and innovation in commercial health insurance are driving accelerated transformation in the healthcare industry. In times of change, the market often eliminates companies that fail to keep pace with the times, while simultaneously nurturing a new generation of great and innovative enterprises.

So, in the healthcare industry undergoing transformation, which niche segments offer greater opportunities?

BlueRun Ventures China believes that niche sectors and enterprises addressing currently unmet clinical needs through innovative models or technologies will usher in development opportunities.

In addressing healthcare accessibility, significant opportunities will emerge in telemedicine, internet-based healthcare, and wearable devices. To tackle healthcare payment challenges, commercial health insurance and insurtech will experience rapid development. As payment issues gradually ease, disruptive changes will occur in sectors currently lacking clear payers, such as rehabilitation, elderly care, nursing, chronic disease management, and health management.

In addition, innovative technologies that enhance efficiency and improve the quality of medical services will be extensively adopted, such as digital technologies that streamline information communication and follow-up management, surgical robots that increase success rates and reduce risks, and exoskeleton robots that improve rehabilitation outcomes.

BlueRun Ventures China is also highly optimistic about the wearable device sector. Zhu Tianyu stated, “Wearable devices will establish a closed-loop service ecosystem leveraging recorded biometric data: by monitoring such data, they help physicians gain clearer and more accurate insights into changes in patients’ physiological conditions, thereby enabling better formulation of personalized treatment plans and enhancing the quality of medical care. Meanwhile, other stakeholders can also leverage monitoring data to deliver improved services to users.”

For example, a smart toothbrush project previously invested in by BlueRun Ventures China features devices that not only assist users with brushing but also record brushing motions, pressure, frequency, and duration, thereby assessing whether users have established proper brushing habits. These oral hygiene practices will largely determine users’ future oral health status and their anticipated costs for dental treatment. Leveraging this data, the company has engaged in discussions with insurance providers to design tailored insurance service packages.

In practical terms, how does BlueRun Ventures China identify high-quality enterprises? Which projects and teams does it favor?

Zhu Tianyu pointed out: “While BlueRun Ventures China categorizes investment sectors during project screening, our final assessment evaluates projects from three perspectives: demand, supply, and payers. The healthcare industry is dynamic, with significant changes and abundant opportunities; however, enterprises that address challenges faced by demand-side users, supply-side providers, or payers ultimately possess greater growth potential.”

From the supply side, can the founding team enhance the quality of health services through technological or business model innovation? From the demand side, can the founding team provide a better user experience for its target audience? From the payer side, is the founder aware of the potential for new payers to participate?

Taking Waterdrop Company as an example, founder Shen Peng and his team have effectively integrated these dimensions. “Shen Peng and his team gained a clear understanding of market demand and entered the health services sector by empowering payers through innovative connectivity models, thereby meeting the health service needs of a larger population.”

Therefore, BlueRun Ventures China seeks projects with the following characteristics: founders who can clearly identify core issues and provide solutions addressing the pain points of payers, suppliers, or demand-side users; founders who have a clear understanding of their development path; and solutions that are sufficiently efficient and point toward a higher growth ceiling.

“Many innovative projects follow cross-disciplinary models, making them difficult to categorize using traditional classification methods. This is precisely the type of innovation that BlueRun Ventures China favors. Cross-disciplinary teams often possess broader perspectives, and their multi-dimensional capability genes are more likely to achieve success in the healthcare services industry,” said Zhu Tianyu. “When other institutions are unwilling to invest time in understanding these projects or fail to comprehend them, we are more willing to devote time to in-depth communication. Innovation emerges at the intersection of disciplines.”

Perhaps it is this attitude of gaining in-depth understanding of innovative projects that enables BlueRun Ventures China to often identify emerging trends ahead of the curve.

BlueRun Ventures China believes that the healthcare services industry will inevitably produce at least one super-giant, and this giant must possess highly efficient organizational capabilities, as well as the ability to leverage large-scale digital tools to connect with or deliver high-quality, high-efficiency services, akin to companies such as Meituan and ByteDance.