DRG/DIP Pilot Bidding Landscape: Market Leadership Emerges Amid Intensifying Competition

Recently, the National Healthcare Security Administration (hereinafter referred to as the NHSA) released the Statistical Bulletin of Healthcare Security Work in 2020. Regarding the highly anticipated progress of healthcare security payment reform, the Bulletin stated that all 30 pilot cities for the China Healthcare Security Diagnosis-Related Groups (CHS-DRG) had successfully passed the pre-simulation evaluation and assessment, thereby entering the simulation phase. Despite disruptions caused by the pandemic, the CHS-DRG pilot program proceeded into the simulation phase as originally scheduled.

Regarding the DIP pilot program launched in mid-last year, VCBeat also noted that 71 pilot cities are currently conducting intensive trials. According to the original plan, pilot regions with completed technical preparations and supporting policies could initiate actual payment implementation after filing, starting from March 2021. By the end of 2021 at the latest, all pilot regions were required to enter the phase of actual payment implementation.

Although the DIP pilot program was launched much later than the CHS-DRG pilot, its pace of implementation has been even faster than that of CHS-DRG at a comparable stage. Given that most DIP pilot cities do not stand out in terms of healthcare informatization, the urgency and difficulty of advancing the DIP pilot have only increased.

So, what is the current status of DRG/DIP bidding across different regions? Are there any discernible patterns? What elements does a DRG system require to meet customer needs? VCBeat (WeChat ID: Vcbeat) has also compiled an overview of the current DRG/DIP bidding results in various regions, aiming to answer these questions.

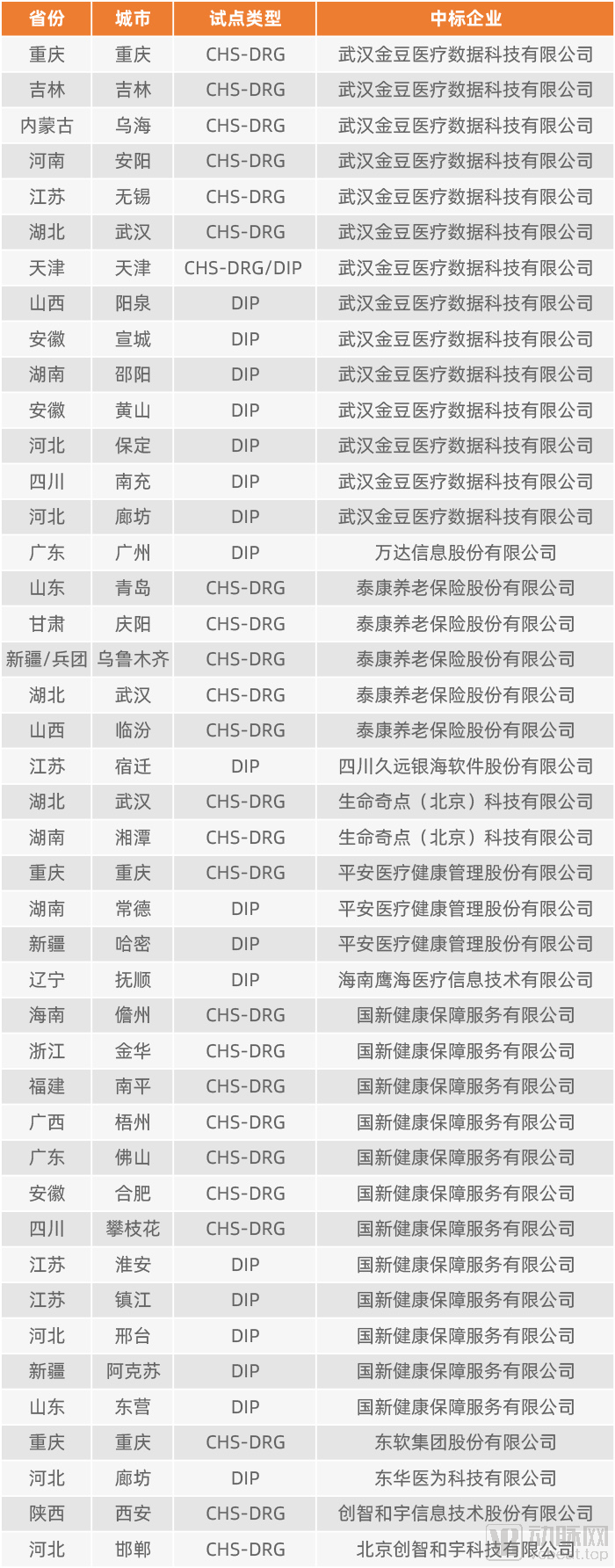

It should first be clarified that pilot DRG/DIP systems are primarily divided into two components: the Healthcare Security Administration side (the “Bureau side”) and the hospital side (the “Hospital side”). Based on practical considerations for data collection, we selected the Bureau side as the subject of our statistical analysis. We compiled publicly available bid award information for local Healthcare Security Administrations’ DRG/DIP systems up to March 2021, drawing from sources including but not limited to government procurement websites, official websites of local governments and Healthcare Security Administrations, publicly disclosed corporate financial reports, official announcements, and news reports that indirectly reflect bid award outcomes.

It should be noted that these winning bid statistics remain incomplete, as cases involving missing information, unverifiable data, or the presence of tender notices without corresponding award announcements have been excluded. This indirectly highlights that, although China has established relevant regulations on information disclosure, further improvements are still needed in their implementation.

VCBeat Graphic

Based on the publicly announced bid results from pilot cities implementing CHS-DRG/DIP, two established industry leaders in DRG—Wuhan Jindou Medical Data Technology Co., Ltd. (hereinafter referred to as “Jindou Data”) and Guoxin Health Security Service Co., Ltd. (hereinafter referred to as “Guoxin Health”)—form the first tier, significantly outpacing other competitors. Taikang Pension Insurance Co., Ltd. (hereinafter referred to as “Taikang Pension”) ranks third in the number of successful bids. Although trailing considerably behind the two leading firms, Taikang Pension maintains a clear advantage over subsequent bidders, thereby constituting a distinct second tier.

VCBeat Graphic

Although the bidding processes in national pilot cities are not yet complete, the market landscape for provider-side DRG/DIP solutions has largely taken shape. Two leading companies have collectively captured more than half of the market share, amid intense competition. Based on currently available public information, Jindou Data is temporarily leading in bid awards across national pilot cities, with Guoxin Health ranking second. Taikang Pension, which holds the third-highest number of successful bids, falls within the second tier of competitors.

Evidently, in the hospital-side DRG/DIP market, fierce competition has begun to drive orders toward leading enterprises. As this round of bidding in national pilot cities nears its conclusion, future competition will shift to non-pilot cities, and VCBeat will provide timely updates and analysis accordingly.

So, compared with other competitors, what common competitive advantages do the current leading companies possess that have won the favor of the National Healthcare Security Administration? Analysis shows that these advantages mainly include the following: First, leading enterprises typically have many years of in-depth experience in the industry and are capable of providing integrated solutions; second, they possess mature grouper capabilities; third, they often have a track record of successful project implementations.

Take Jindou Data, a standout performer in the current landscape, as an example. The founding team of Jindou Data all graduated from the Health Statistics program at Tongji Medical College, Huazhong University of Science and Technology. Since 2008, they have collaborated with national ministries and universities on research in areas such as healthcare payment method reform, AI-powered intelligent coding, and health technology assessment, making them typical practitioners of academic-to-industry translation. Leveraging over a decade of expertise in the field, Jindou Data has participated in the development of multiple national platforms and accumulated key models and algorithms for DRG grouping and pricing.

Guoxin Health, formerly known as Hailong Holdings, entered the health insurance payment sector by establishing a centralized procurement platform for pharmaceuticals and medical devices. As early as 2009, it partnered with the U.S.-based ESI Group to introduce the Pharmacy Benefit Manager (PBM) model to China, accumulating extensive experience in centralized drug procurement and related regulatory oversight. After the PBM model failed to gain traction in China, the company ventured into the Diagnosis-Related Groups (DRG) field in 2016, making new attempts at controlling health insurance costs. The most representative achievement of Guoxin Health’s DRG exploration is the “Jinhua Model,” which adopts a point-based payment system, representing a significant effort to control health insurance fund expenditures.

Moreover, Taikang Pension and Ping An Healthcare Technology entered the DRG industry in 2017 and 2019, respectively. Leveraging their substantial resource reserves, they captured a certain market share in a short period, which was no small feat.

Amid the gradual advancement of healthcare insurance payment method reforms in China, Jindou Data has been deeply involved in several key pilot initiatives. In 2017, the C-DRG “3+3” pilot program, led by the National Health Commission, adopted fully proprietary CCDT (Clinical Classification and Diagnosis Terminology) and CCHI (China Clinical Healthcare Intervention) coding systems, with Jindou Data providing comprehensive technical support throughout the process. As a result, its solutions were not only implemented across the healthcare security administrations in three regions but also firmly established within the pilot hospitals. Following the establishment of the National Healthcare Security Administration, Jindou Data secured leading positions in the national CHS-DRG and DIP pilots, becoming the construction vendor for Anyang, the first city to issue a tender for CHS-DRG, and Yangquan, the first city to issue a tender for DIP.

On the hospital side, Jindou Data has also built substantial expertise. Taking Shenzhen Third People’s Hospital as an example, this Grade 3A specialized research hospital focused on infectious diseases primarily assumes responsibility for the prevention and control of infectious diseases and major epidemics in Shenzhen and surrounding areas—including Hong Kong, Macau, Zhuhai, Dongguan, and Huizhou—as well as providing medical services to Shenzhen residents. Upon completion of Phase II of its expansion and renovation project, the hospital’s total floor area will exceed 430,000 square meters, with a total bed capacity reaching 2,300.

Jindou Data’s hospital-side systems, which it developed and implemented, primarily include the Physician Assistant and the AI Medical Record Quality Control System. The former helps physicians improve the accuracy of initial case grouping, provides timely feedback on entry errors, and offers step-by-step guidance to clinical staff on standardized documentation, thereby substantially enhancing the quality of medical record completion. The AI Medical Record Quality Control System effectively reduces the audit workload for quality control personnel and enables real-time online communication between medical record auditors and clinicians. Since its launch in December 2019, the hospital’s medical record quality compliance rate has risen to 98%.

Leveraging its integrated service capabilities, Jindou Data provides the basic hospital-side system free of charge to hospitals within the coverage area after winning bids for bureau-side systems. Currently, Jindou Data’s basic hospital-side system has been deployed in over 4,000 hospitals across China. During the implementation of DRG/DIP payment reforms, Jindou Data has identified that one of the most pressing needs for hospitals at this stage is securing reasonable and compliant reimbursement from medical insurance funds through data quality control, departmental operations, and refined management. Consequently, Jindou Data has developed a series of upgraded products based on its basic system. Since 2021, as awareness among hospitals has increased, demand for products assisting with DRG/DIP settlement has grown significantly.

The “Sanming Model” has long been a focal point in the field of healthcare reform. Since 2012, Sanming City has implemented public hospital reforms characterized by the coordinated linkage of pharmaceuticals, medical services, and health insurance (the “Three Medicals” linkage). The city has achieved remarkable results in reducing the proportion of drug costs and increasing revenue derived from medical technical services, earning widespread attention and full affirmation from top national leaders, relevant central government departments, the healthcare sector, and society at large. During Sanming’s healthcare reform process, C-DRG and the underlying Jindou Data have played an indispensable role.

Sanming officially transitioned to the C-DRG payment system on January 1, 2018. After one year of operation, multiple indicators showed improvement. The average annual growth rate of per-admission costs decreased from 1.236% in 2017 to 0.138%, and the number of hospitals exceeding the benchmark for examination-to-cost ratio dropped significantly from 12 in 2017 to 5. One year after implementation, hospitals demonstrated heightened cost-control awareness, resulting in total medical cost savings of RMB 31.87 million throughout the year. Meanwhile, 64% of medical institutions achieved a surplus in their medical insurance funds.

Overall, there are certain differences in the functions and features of DRG systems at the hospital level and the administrative level. The administrative-level system needs to leverage price mechanisms to regulate clinical practices, calculate DRG grouping weights and DRG rates based on the medical record face sheet data and health insurance settlement data collected from hospitals, thereby determining the payment standards for each DRG group, and conducting audits and settlements with hospitals according to these payment standards. Therefore, the administrative-level system requires extensive long-term familiarity and accumulation of expertise in health insurance operations.

In addition to payment processing capabilities, hospital-side systems must also provide refined DRG management functionalities, including enhancing DRG data quality through AI-assisted intelligent coding, leveraging artificial intelligence for optimal DRG-based clinical practices, and conducting performance evaluations based on big data. Beyond functionality, user-centered design is another critical focus for hospital-side systems, ensuring they are “user-friendly and easy to use.”

Regulatory oversight is a shared requirement for both regulatory authorities and healthcare institutions. On February 19, the Regulations on the Supervision and Administration of the Use of Medical Security Funds were promulgated and will officially come into effect on May 1. The Regulations clarify the responsibilities of entities involved in fund utilization, standardize fund usage practices, improve the supervisory framework, and strengthen regulatory measures.

The DRG Supervision Platform leverages monitoring rules, metrics, and early warning systems to assist healthcare security administrations and hospitals in conducting end-to-end supervision and control of medical service behaviors and associated costs, thereby achieving precise management of medical insurance. By linking the administration and hospital sides, and focusing on “controlling unreasonable cost growth” and “building sustainable development of medical insurance,” the platform closely integrates hospitals with medical insurance through quota management, intelligent auditing, and decision analysis. This enables a truly comprehensive, closed-loop regulatory process characterized by pre-event planning, in-process control, and post-event analysis.

In this context, compared to separate bureau-side and hospital-side systems, an integrated solution maintains consistency in architecture, design, and user practices across both ends. This facilitates better integration between the bureau-side and hospital-side systems, thereby achieving greater efficiency with less effort.

Compared with CHS-DRG, DIP may differ in its grouping methodology, but its essence is similar to that of DRG. Therefore, the system requirements for DIP and DRG are essentially common. Compared with CHS-DRG, DIP is more suitable for regions with relatively lower levels of healthcare informatization. Considering that the two systems will coexist for a long period in the future, and given the fact that the level of healthcare informatization remains low in most parts of China, DIP is likely to have a broader coverage.

Furthermore, in line with the relevant initiatives of the National Healthcare Security Administration, DIP is expected to extend its coverage to outpatient services in the future. Compared to short-term hospitalizations, outpatient care presents greater complexity. Therefore, both healthcare security authorities and medical institutions should exercise greater caution when selecting DIP systems.

As an imported concept, Diagnosis-Related Groups (DRG) have matured over years of development abroad. The competitive landscape in foreign markets is characterized by high concentration. In terms of the core functions of DRG—namely, medical record quality control and intelligent coding—the two industry leaders, 3M and Optum, collectively hold more than 70% of the U.S. market share.

As the pilot programs for DRG and DIP continue to deepen, the future DRG market will gradually shift from fragmentation to consolidation among a few leading enterprises. Providing integrated services has become imperative; those who fail to keep pace with the times will inevitably be left behind. VCBeat will continue to closely monitor industry dynamics and deliver first-hand analysis to you.