The Next Battleground for CXO: Dozens of Chinese Companies Enter Formulation CDMO Space

This article was first published on PharmCube and is republished here with authorization from VCBeat.Author:Brother Tao in the Pharma Circle, Header image source: 123rf.

Note: This article does not constitute any investment advice or recommendations; please refer to the announcements of listed companies for accuracy. This article is intended solely for introducing medications related to healthcare and medical services, and does not recommend treatment plans (if applicable).

WuXi Biologics has recently entered into two acquisition agreements, aiming to complete the acquisition of Pfizer China’s Hangzhou biologics facility and a 90% stake in Suzhou BioBridge by the first half of 2021. These acquisitions are expected to rapidly expand the company’s drug substance and drug product manufacturing capacity, thereby meeting the surging demand for commercial production services. Large CXO companies have begun to expand their footprint in the drug product CDMO sector through mergers and acquisitions. Compared with CMOs, CDMOs offer customized R&D services, representing an upgraded version of the CMO model. The primary driver of growth in China’s CDMO industry is the substantial market opportunity created by this business upgrade. Originating in Europe and North America, the CDMO industry has gradually shifted toward the Asia-Pacific region, represented by countries such as China and India, evolving alongside the specialized division of labor in the pharmaceutical industry and economic globalization.

If 2014 is taken as the watershed, prior to this year, China’s formulation CDMO (Contract Development and Manufacturing Organization) sector performed moderately overall. This was primarily because domestic companies struggled to secure formulation CDMO orders from Europe and the United States. Additionally, Chinese pharmaceutical manufacturers typically handled formulation in-house, as outsourcing would erode profit margins. These two factors constrained the development of China’s formulation CDMO industry. After 2014, China’s innovative drug sector experienced rapid growth, driven comprehensively by policy support and capital investment. Compared with their foreign counterparts, Chinese innovative pharmaceutical companies are more inclined to outsource both active pharmaceutical ingredients (APIs) and formulations together. Meanwhile, facing China’s vast market, multinational pharmaceutical companies have initiated collaborations with local firms for regulatory submissions in China, often outsourcing formulation manufacturing to domestic CDMOs. Furthermore, the normalization and institutionalization of volume-based procurement has driven generic drug costs to an extreme low, while the implementation of the Marketing Authorization Holder (MAH) system has significantly unleashed industrial productivity. These developments have generated substantial incremental demand for CDMOs operating within the supply chain. It is foreseeable that the formulation CDMO sector will witness significant growth in the future.

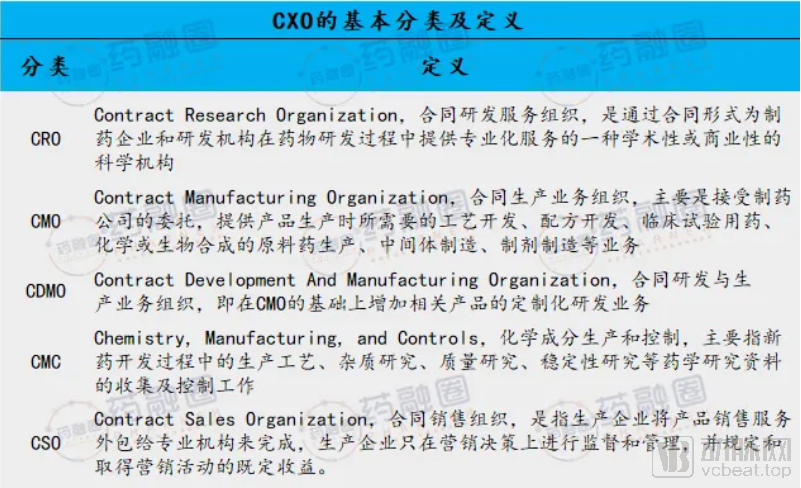

Table: Basic Classification and Concepts of CXO

Source: Public information; compiled by PharmCube

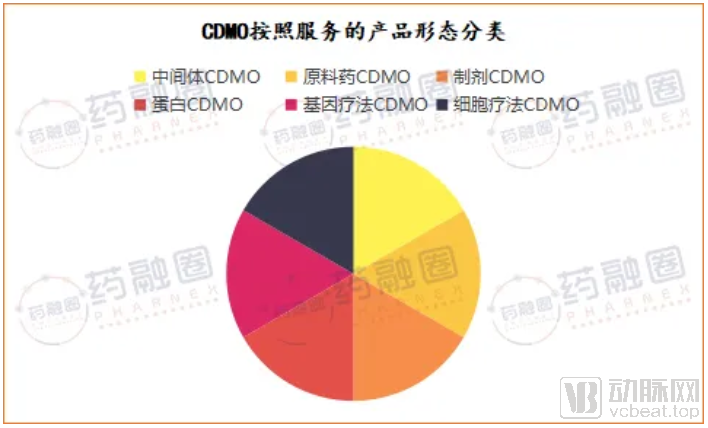

The CDMO industry is relatively fragmented and covers a broad range of service areas. According to the financial reports of Porton Pharma Solutions, it can be categorized into small-molecule drug CDMO and biologic drug CDMO based on the attributes of the drugs served; and into intermediate CDMO, active pharmaceutical ingredient (API) CDMO, finished dosage form CDMO, protein CDMO, gene therapy CDMO, and cell therapy CDMO based on the product forms served, with the latter two belonging to the frontier biologics sector.

Source: Chart by PharmCube

From the perspective of the CDMO industry chain, European and American enterprises are concentrated in the high-value-added downstream segments. They not only provide one-stop services ranging from drug discovery to commercial-scale manufacturing and supply but also possess absolute technological advantages in cutting-edge biological fields such as cell therapy and gene therapy. Most domestic CDMOs in China operate in the upstream segments of the industry chain, primarily supplying intermediates required for API production to these Western CDMOs. This results in low business value-added and limited market space for individual products. However, a significant number of Chinese CDMOs have already expanded into these high-value-added business areas.

Global leaders in the formulation CDMO sector include Lonza, Patheon, Catalent, and Siegfried. In 2020, Lonza reported sales of CHF 4.5 billion, representing a 12.0% year-over-year growth. Its core business generated an EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) of CHF 1.4 billion, with a profit margin of 31.2%. The company is currently a global leader in small-molecule CDMO, biopharmaceutical CDMO, and cell and gene therapy CDMO services.

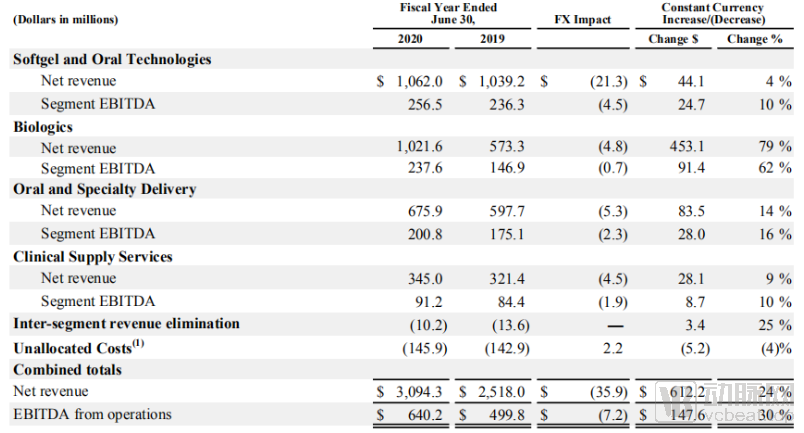

Catalent specializes in drug formulation. Its 2020 annual report disclosed total revenue of $3.1 billion, with formulation CDMO revenue amounting to approximately $2 billion. The company holds numerous patents in softgel technology, biologics, specialty drug formulations, and oral drug formulations. According to Catalent’s official website, more than 1,000 scientific professionals at Catalent contributed to the approval of 40% of new drugs globally. With over 30 facilities worldwide, the company achieves an annual production volume of 100 billion individual units. Catalent’s significant intellectual property in oral, injectable, and respiratory dosage forms, as well as advanced pharmaceutical packaging, has resulted in more than 1,200 patents and patent applications.

Source: Catalent Annual Report

According to Catalent’s 2020 annual report, the total size of the global drug formulation market exceeded $50 billion, with an projected annual growth rate of over 8% in the next five years.

After years of development, China’s policy environment, quality system construction, technological capabilities, and talent reserves in the pharmaceutical sector have reached a level that enables domestic CDMO companies to expand their operations into downstream high-value-added segments. With the accelerated market entry of imported drugs in China and the rise of domestically developed innovative drugs, domestic CDMOs with advanced technologies are well-positioned to undertake formulation services for some of these innovative therapies. Formulation represents the final stage of drug manufacturing, offering substantial market potential and profit margins. Dozens of companies in China have already established their presence in the formulation CDMO space. Among publicly listed companies, representative players include WuXi AppTec, Porton Pharma, Hepalink, Jianyou Pharmaceutical (a subsidiary of Genimune), Jiuzhou Pharmaceutical, and Asymchem. Among private companies, there is a group of pioneers who initially engaged in contract manufacturing of formulations (C(D)MO), such as Ruiyang Pharmaceutical in Shandong, Pude Pharmaceutical in Shanxi, Aoya Biotechnology in Hangzhou, Tongde Pharmaceutical in Chengdu, and Qikang Pharmaceutical. At that time, due to regulatory policies, production approvals for early-stage R&D enterprises were typically held by manufacturing plants. However, in recent years, the implementation of the Marketing Authorization Holder (MAH) system, which separates license holders from manufacturers, has spurred significant growth in the CDMO sector. Other notable companies include Huayi Pharmaceutical, Xinghao Pharmaceutical, Hualu Pharmaceutical, Bostech, Haina Pharmaceutical, Phrontis Pharmaceutical, Bozhi Yanxin, WisePharm, Baifan Biotherapeutics (specializing in large-molecule formulations), and Suqiao Biotherapeutics (specializing in large-molecule formulations). This article provides commentary only on selected companies with distinctive features. For information on more outstanding enterprises, please contact PharmCube. According to a research report by Zheshang Securities, Chinese CDMO companies are currently transitioning from intermediate CDMO services to API and formulation CDMO services. Significant breakthroughs in local undertaking of API and formulation projects are expected within the next 3–5 years, followed by an accelerated shift of API and formulation manufacturing to China over the subsequent 5–10 years.

WuXi AppTec:In March 2019, the new drug product manufacturing base in Waigaoqiao passed the GMP certification of the European Medicines Agency (EMA) for the first time. In 2019, the commercial drug product manufacturing base in Wuxi New District undertook the production of registration or validation batches for several projects. In January 2020, STA Pharmaceutical commenced construction of a new drug product development and manufacturing base in Wuxi, which will further enhance its capabilities and capacity for the development and production of solid dosage forms, while also adding capabilities for the development of sterile products, as well as the production of clinical trial supplies and commercial manufacturing.

Jiuzhou Pharmaceutical:In November 2020, the company announced a proposed investment of RMB 1.6 billion to establish a CDMO and drug product manufacturing base. The company decided to invest in the construction of a CDMO and drug product manufacturing base project in Medicine Port Town, Qiantang New Area, Hangzhou, Zhejiang Province. The project will involve the construction of a new CDMO (contract development and manufacturing organization) base for small-molecule and large-molecule innovative drugs, as well as a center for drug product research, development, and manufacturing.

Porton Pharma Solutions:According to the 2020 annual report, in 2019, the company officially launched the construction of two new business segments: formulation CDMO and biological CDMO. In terms of formulation CDMO business, Porton Pharma Solutions served as the implementing entity. During the reporting period, three formulation laboratories in Chongqing completed renovation and acquired the capability to undertake projects, while the Shanghai Zhangjiang R&D Center began providing formulation CDMO laboratory services in November 2020. Porton Pharma Solutions has signed three customer orders (with a total value of approximately RMB 19 million) and initiated preliminary R&D work for the first project. As of the end of the reporting period, the formulation CDMO business had nearly 60 employees. In addition, Porton also has Porton Biologics (focused on gene therapy), which is currently undergoing financing.

Hepalink:The 2020 semi-annual report disclosed that, according to a Frost & Sullivan report, the Company’s CDMO business ranked among the top three Chinese-owned biologics CDMO providers by revenue in 2018.

Asymchem:In its 2020 interim report, the Company disclosed that it had established platforms for oral enteric-coated formulations and sustained-release formulations within its formulation segment, and had successfully delivered projects. The formulation business expanded into overseas markets, completing its first U.S. formulation analytical service project and its first Korean formulation project. The injectables workshop successfully completed R&D and manufacturing tasks for new drugs across multiple therapeutic areas during both the Investigational New Drug (IND) and New Drug Application (NDA) stages.

Anhui Huayi Pharmaceutical:Established in 2006, the company boasts over a decade of experience in CDMO services for solid oral dosage forms compliant with EU standards. It is the first enterprise in Anhui Province to obtain EU certification, specializing in R&D and manufacturing of tablets, capsules, and liquid oral formulations for the Chinese and European markets. Huayi has built an open CDMO service platform for oral dosage forms. With an existing production capacity of 3 billion units, expandable to 5 billion, the company offers contracted R&D (including dual filings in China and Europe), clinical batch production, and commercial manufacturing for tablets, capsules, and liquid oral formulations.

Beijing Xinghao Pharmaceutical:Founded in 2000, Star Pharma currently operates nine GMP-compliant production lines. Its wholly-owned subsidiary, Guangdong Xinghao Pharmaceutical Co., Ltd., commissioned its lyophilization and small-volume injection workshop in Phase I, which was among the first in China to receive certification under the 2010 version of Good Manufacturing Practices (GMP). This workshop employs advanced international liquid nitrogen lyophilization technology. Phase II is currently under construction to establish small-volume injection, lyophilized powder for injection, and oral solid dosage form production lines that comply with U.S. FDA and European EMA standards, covering the manufacturing of oncology drugs and modified-release formulations.

Chengdu Tongde Pharmaceutical:Founded in 1958, its predecessor was the former state-owned Chengdu Pharmaceutical Factory No. 3 (one of the three major state-designated biochemical pharmaceutical enterprises). The company was restructured into a joint-stock enterprise in 2000. It holds 81 product approval numbers, covering four dosage forms—hard capsules, tablets, granules, and lyophilized powders for injection—as well as active pharmaceutical ingredients (APIs). It is a founding member of the International CMO Development Alliance.

Shandong Ruiyang Pharmaceutical:Established in 1966, the company was restructured from the Fourth Branch Factory of Shandong Xinhua Pharmaceutical Factory. The company operates three manufacturing bases with more than 30 modern production workshops, capable of producing nine dosage forms—including active pharmaceutical ingredients (APIs), conventional powder for injection, lyophilized powder for injection, tablets, capsules, large-volume parenterals, granules, mixtures, and suppositories—comprising nearly 400 product specifications. For many years, the company’s main business revenue has ranked among the top 50 of China’s Top 100 Pharmaceutical Enterprises.

Shandong Hualu Pharmaceutical:Established in 1977, the company has the production capacity for over 170 product specifications across six major dosage forms: large-volume parenterals, water-based injections, inhalants, capsules, tablets, and active pharmaceutical ingredients (APIs). Leveraging the implementation of the Marketing Authorization Holder (MAH) system, the company focuses on Blow-Fill-Seal (BFS) plastic ampoule products. Its CMO/CDMO services cover contract manufacturing for a wide range of specifications, including PP/PE material-based products, sterile injectables, ophthalmic solutions, inhalants (including hormonal products), water-based injections, polypropylene infusion bottles, non-PVC multi-layer co-extruded infusion bags, glass bottles, and oral preparations.

Hangzhou Aoya Biotech:Established in 1993, the company is a modern pharmaceutical enterprise integrating production, education, and research, with sterile lyophilized powder injections as its core products. Currently, five sterile lyophilization workshops certified under the 2010 version of China’s Good Manufacturing Practice (GMP) are in operation. Its main dosage forms include lyophilized powder injections in vials, pre-filled syringes, cartridge pens, and small-volume vial injections. With an annual production capacity approaching 500 million units, it is one of the largest contract manufacturing organizations for lyophilized powder injections in China.

Shandong Qikang Pharmaceutical: Established in May 2003, the company is primarily dedicated to the research and development, manufacturing, and sales of pharmaceutical formulations. It currently operates two production lines for tablets and capsules, with its main products being cisapride tablets and nateglinide tablets. The annual production capacity is 200 million tablets and 300 million capsules.

Driven by supportive policies, the rapid rise of China’s innovative drug industry and the broader trend of global supply chain relocation to China are jointly propelling the swift advancement of the Chinese CDMO sector. To seize this wave of CDMO growth opportunities and remain competitive amid the intensifying rivalry in the biopharmaceutical industry, domestic companies must actively leverage their technological strengths to transition into higher-value-added formulation manufacturing, focusing on differentiated contract formulation services.