Neurointerventional Sector Attracts Over 24 Companies and RMB 1.5B+ in Funding: Can It Replicate the Coronary Stent Success Story?

On March 23, Zendo MedTech submitted its listing application to the Hong Kong Stock Exchange. As a company specializing in interventional medical devices for neurovascular and peripheral vascular applications, Zendo MedTech’s core business involves the research and development, manufacturing, and sales of neurointerventional and peripheral vascular interventional products. Currently, its flagship products include the Jiaolong Intracranial Thrombectomy Stent and UltrafreeTMDrug-eluting PTA balloon dilation catheters have been launched in China.

According to the prospectus of Zhenjiang Medical, its marketed product portfolio comprises two neurointerventional products and six peripheral vascular interventional products. In 2020, the company generated total revenue of RMB 27.63 million, with the neurointerventional segment contributing RMB 19.94 million, accounting for 72.2% of the total.

The prospectus submitted by GenesisCare provides detailed disclosure on the neurointerventional and peripheral vascular intervention industries, with the neurointerventional sector currently attracting significant capital attention.As of now, according to incomplete statistics from VCBeat, at least 24 innovative companies and 25 investment institutions have bet on the neurointerventional field. From 2020 to the present, there have been more than 15 financing events in the neurointerventional field, with a total cumulative financing amount exceeding RMB 1.5 billion.

Given the significant attention and substantial growth potential in the neurointerventional field, VCBeat has conducted research and surveys among frontline distributors, clinicians, and neurointerventional companies to gain an in-depth understanding of the commercialization pathways within this sector.

In 1998, coronary stents began to be widely used in China. Over the following two decades, both the volume of percutaneous coronary intervention (PCI) procedures and the usage of coronary stents maintained ultra-high growth rates. Driven by continuous innovation from domestic manufacturers, coronary stents have become one of the few high-end medical devices in China to achieve substantial import substitution. Relevant companies have reaped substantial profits by capturing a 70% share of the domestic market. Currently, the annual number of PCI procedures exceeds one million, and the penetration rate of coronary stents has further increased alongside price reductions resulting from centralized procurement.The success of coronary stents has set a benchmark for the domestic substitution of high-end medical devices in China. Many niche sectors are following this example, aiming to replicate the coronary stent model and capture the domestic market amid the wave of import substitution.

Among these, the neurointerventional field is highly anticipated by investors and innovative companies due to its many similarities with coronary stents.

So, compared with coronary stents, what are the differences in the current policy and market environments for neurointerventional procedures? Can neurointervention replicate the successful trajectory of coronary stents? What challenges does neurointervention currently face? What are the market promotion strategies adopted by various companies?

To answer the above questions, VCBeat has conducted research and obtained the following viewpoints:

1. Reviewing the Path of Domestic Substitution for Coronary Stents: Innovative High-Quality Products and Price Reductions for Market Penetration Are Two Key Strategies.

2. Profound Changes in the Healthcare Industry: A More Favorable External Growth Environment for Neurointervention

3. Factors such as product pricing, patient awareness, early screening for cerebrovascular diseases, and the number of stroke centers have resulted in low penetration rates of neurointerventional procedures.

4. In the current environment, neurointerventional companies need to enhance their competitiveness by focusing on product quality, pricing, and brand promotion.

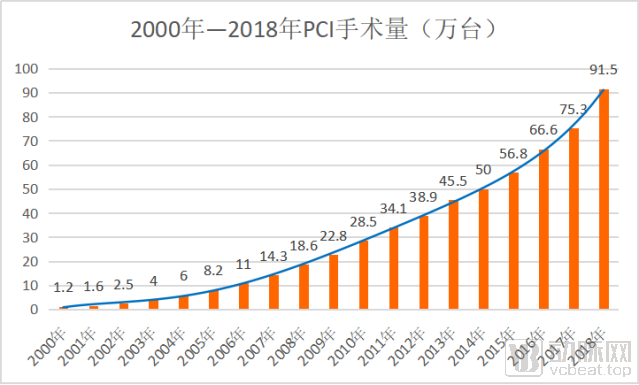

Officially released data shows that,The volume of percutaneous coronary intervention (PCI) procedures in China increased from 12,000 in 2000 to 915,000 in 2018, with a compound annual growth rate (CAGR) exceeding 40% from 2000 to 2008 and a growth rate surpassing 14% from 2009 to 2018. Meanwhile, the usage of coronary stents rose from 40,000 units in 2002 to 1.336 million units in 2018.

(Graphic by VCBeat)

Prior to 2004, the domestic coronary stent market was predominantly dominated by foreign companies. However, by 2006, domestically produced coronary stents achieved a remarkable turnaround, capturing 59% of the domestic market share. According to statistics from the Surgical Implants Professional Committee of the China Medical Devices Industry Association, the market share of domestically produced coronary stents reached 65% and 70% in 2007 and 2008, respectively, thereby fully realizing the comprehensive substitution of imported coronary stents with domestically manufactured ones.

A review of the domestic substitution process for coronary stents reveals that their rapid growth has been driven by multiple factors, including policy, market, technology, and capital.

First, China has a large population of patients with heart disease, totaling 330 million, including approximately 11 million with coronary heart disease and 8.9 million with heart failure. Given the high mortality and disability rates associated with heart disease, there is an urgent need for effective treatment. Consequently, percutaneous coronary intervention (PCI) using coronary stents, as a minimally invasive therapy, is more readily accepted by patients due to its safety, efficacy, and minimal invasiveness.

Second, domestic coronary stent manufacturers and cardiologists such as Hu Dayi have vigorously promoted coronary stents by offering free training in interventional techniques across China, cultivating a large number of physicians capable of performing these procedures and facilitating the decentralization of cardiac interventions from top-tier tertiary hospitals to county-level hospitals. Additionally, the prospect of substantial financial returns has driven hospitals and physicians to actively learn and perform cardiac interventional procedures.

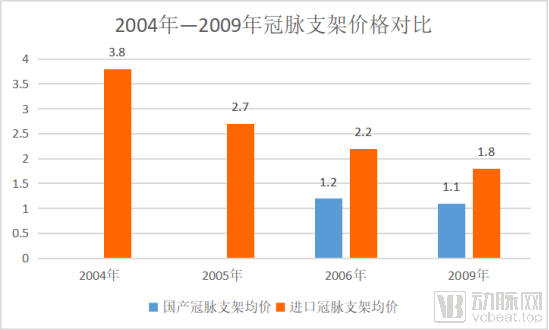

Third, multiple products from domestic coronary stent manufacturers were launched successively after 2005 and rapidly captured market share by virtue of their superior technical performance and relatively lower prices. In terms of performance, Chinese enterprises have continuously iterated their products through R&D innovation and the integration of medicine and engineering, bringing domestically produced stents to an internationally leading level. For instance, in September 2018, MicroPort published the results of a large-scale European clinical trial of its coronary stents in The Lancet, earning high recognition from medical experts worldwide. Regarding price, domestically produced coronary stents saw a significant price reduction compared to imported products. The stent cost borne by patients with coronary heart disease in China decreased from RMB 59,000 per patient in 2004 to RMB 18,000 per patient in 2009.

(Chart by VCBeat)

Fourth, national policy supports the development of domestically produced high-end medical devices, and investment firms are optimistic about the coronary stent market, having invested heavily in numerous coronary stent manufacturers. Consequently, the large number of domestic coronary stent companies has intensified competitive pressure, which in turn drives these enterprises to enhance product performance, reduce prices, and actively expand their market presence, ultimately increasing the penetration rate of coronary stents.

Fifth, domestic coronary stent manufacturers rapidly established nationwide marketing and after-sales service networks through distributors, driving rapid growth in product sales. Since distributors could reap substantial profits from promoting coronary stents, they intensified their promotional efforts. It should be noted that, under the circumstances at the time, some distributors promoted products by offering kickbacks to physicians, which, to a certain extent, accelerated the adoption of coronary stents but also gave rise to concerns about overmedicalization.

Sixth, domestic coronary stent manufacturers actively participate in academic seminars and international and domestic interventional cardiology conferences to promote the clinical application of coronary stents and enhance the brand influence of Chinese enterprises. Currently, clinicians have a high level of recognition for domestically produced coronary stents and hold Chinese brands in high regard.

Nowadays, with the intensive rollout of national policies, increased capital inflow into healthcare, and the continuous emergence of innovative models and technologies, China’s healthcare industry has undergone significant changes under the influence of multiple factors.

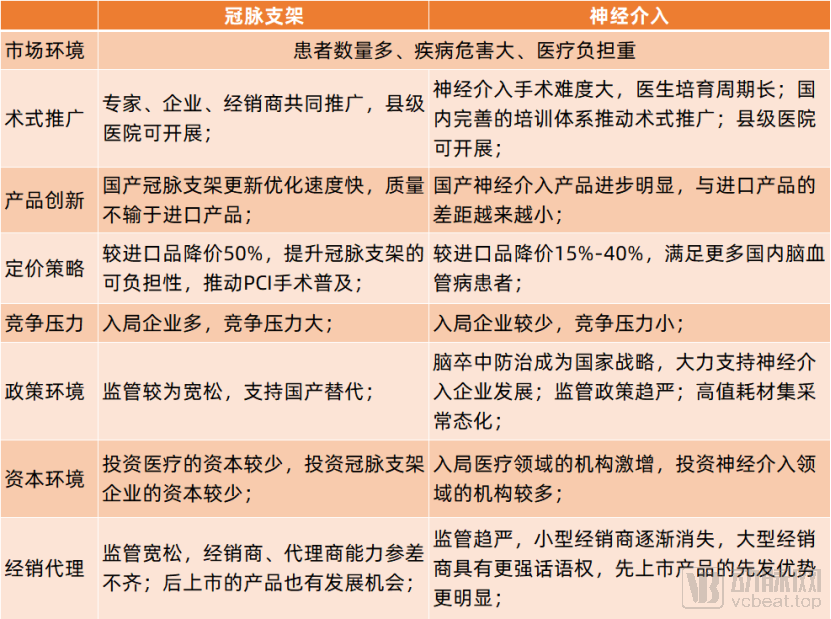

Twenty years ago, coronary stents enjoyed a rare market opportunity and favorable growth environment. Today, two decades later, the healthcare industry has undergone dramatic changes. How do the growth conditions facing neurointerventional companies compare with those once experienced by the coronary stent sector—what are the similarities and differences?

(Chart by VCBeat)

From the perspective of the market environment,Cerebrovascular diseases associated with neurointerventional procedures share certain similarities with heart diseases, such as a large patient population, significant disease burden, and heavy healthcare costs. According to the prospectus of Zetian Medical (Guichuang Tongqiao),In China, the number of stroke patients has reached 13 million, with approximately 2 million new cases annually. In 2019, cerebrovascular disease accounted for over 20% of all deaths among Chinese residents. According to the "2019 Health Statistics Yearbook," there were 5.67 million hospital discharges for cerebrovascular diseases in China in 2018, including over 720,000 cases of intracranial hemorrhage, 3.73 million cases of cerebral infarction, and 87,000 cases of cerebral artery occlusion and stenosis. Regarding costs, the average per-patient medical expense for intracerebral hemorrhage at provincial hospitals was RMB 25,480, while that for cerebral infarction was RMB 14,117.

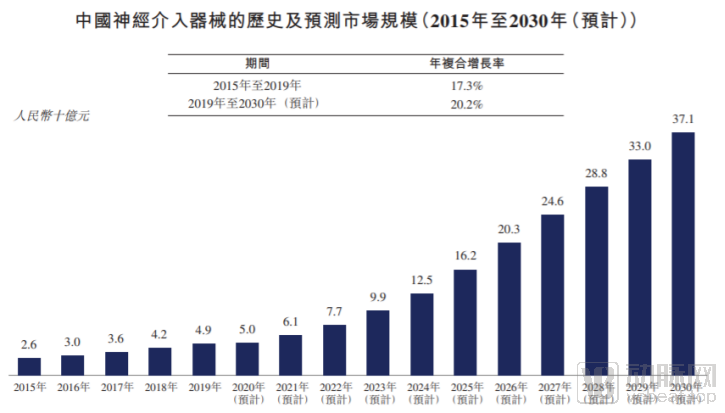

According to the prospectus of Zhiwei Medical, the market size of neurointerventional medical devices in China increased from RMB 2.6 billion in 2015 to RMB 4.9 billion in 2019, with a compound annual growth rate (CAGR) of 17.3%. It is projected to further grow to RMB 37.1 billion by 2030, representing a CAGR of 20.2% from 2019 to 2030.

(Image source: Prospectus of Genesis MedTech)

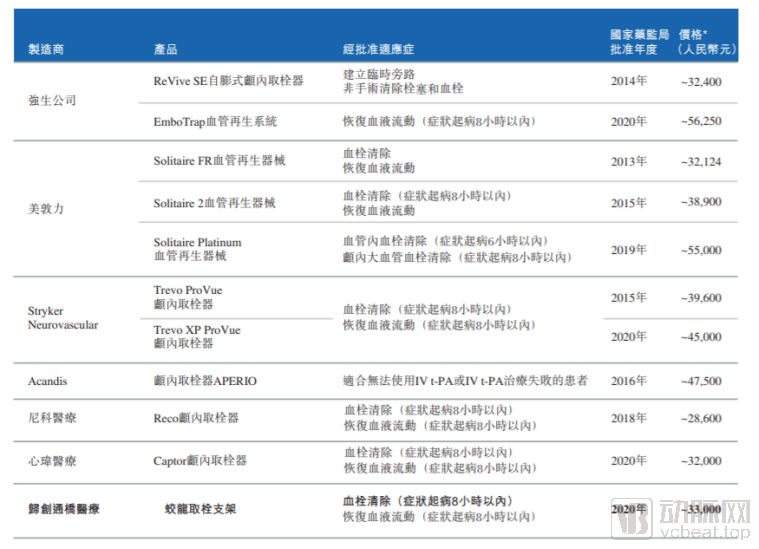

In addition, the prospectus of GenesisCare MedTech shows that,At the current stage, foreign companies such as Medtronic, Johnson & Johnson, and Stryker occupy 93% of China's neurointerventional market, while domestic enterprises are building complete product lines from scratch.For example, Zebra Medical currently has nine products in clinical or registration stages, and it is expected that 19 neurointerventional products will be approved by the end of 2025. Similarly, Mapqi Medical will launch and sell more than 30 new interventional products from 2021 to 2022.

(Image source: ZC Medical’s prospectus)

Contrary to the views of some consulting firms, China has a sufficient number of physicians qualified to perform neurointerventional procedures. Neurosurgeon Xue Chengjing stated: “Currently, county-level hospitals in China are already capable of performing neurointerventional procedures such as thrombectomy and thrombolysis."However, it must be acknowledged thatAs the volume of neurointerventional procedures surges, a shortage of relevant physicians will emerge.This is because neurointerventional procedures are more technically demanding than coronary stenting, and the training period is longer. It takes approximately 2–3 years to train a qualified neurointerventionalist before they can independently perform such procedures.

In terms of products, the neurointerventional market primarily comprises ischemic products for ischemic stroke and arterial stenosis, hemorrhagic products for aneurysms, and access products for establishing vascular access. Among these, ischemic products have a larger market potential due to the higher patient volume; hemorrhagic products feature higher technical barriers and greater procedural complexity owing to the intricate nature of the diseases; and access products, with lower technical barriers, have achieved partial domestic production in China. Statistics from VCBeat show thatCurrently, there is a large number of domestically produced microcatheter wires, thrombectomy stents, and coils on the market; for instance, six domestic coil products have been launched. In contrast, fewer products with higher technical barriers—such as balloons, covered stents, flow diverters, and intracranial stents—are available, with no domestic covered stents currently marketed. Regarding quality, neurosurgeon Xue Chengjing stated, “Domestic neurointerventional products have made significant progress in quality, narrowing the gap with imported products. In some cases, certain metrics of domestic products even surpass those of their imported counterparts.”

(Dense mesh stent, image source: TransMedics prospectus)

In terms of pricing,Domestic neurointerventional products are generally priced 15%-40% lower than imported ones.According to Zhongtian Medical, a company focused on the research and development of neurointerventional medical devices: “The pricing of domestically produced neurointerventional products is lower than that of imported products, first because the costs of labor, land, production, and transportation for domestic products are lower than those for imported products; second, because domestic companies set lower prices to increase the penetration rate of neurointerventional procedures and expand into broader market spaces.”

In terms of the number of companies, there are currently more than 24 enterprises engaged in the field of neurointervention.Given the substantial market size and diverse range of devices in the neurointerventional field, companies in this sector currently face limited competitive pressure.Although many companies have entered the field, most domestically produced neurointerventional products are still in the clinical stage and are 1–2 years away from market launch. An anonymous distributor stated, “Neurointerventional companies face less competitive pressure than coronary stent manufacturers did in their early days, which may also reduce the incentive for these companies to innovate and optimize their products.”

In terms of policy, the “Healthy China 2030” Planning Outline has elevated stroke prevention and control to a national strategy and promoted the establishment of stroke centers.Currently, the number of stroke centers is growing at an annual rate of 37%, and this rapid growth is expected to continue over the next decade.Furthermore, national policies have imposed stricter compliance requirements on hospitals, medical device distributors, and dealers. This will promote the compliant development of neurointerventional products and help prevent issues such as overtreatment and physician bribery. It is worth mentioning thatFollowing the centralized procurement of coronary stents, China has normalized the centralized procurement of high-value medical consumables., which will also enable neurointerventional companies to lower product prices in exchange for higher sales volumes and greater market share. Meanwhile, similar to coronary stent manufacturers, neurointerventional companies will continue to innovate their products to sustain higher profit margins.

In terms of capital, an increasing number of investment institutions and tech giants are entering the healthcare sector by investing in medical enterprises. Among the many specialized fields within healthcare, neurointervention has recently emerged as a “hot favorite,” attracting significant attention. According to incomplete statistics from VCBeat, since the end of 2019, there have been more than 15 financing and M&A transactions in the neurointervention field. Notably, neurointervention companies such as WoBi Medical and WeiMi Medical have each completed two rounds of financing within a single year, demonstrating remarkable speed. It can be said that,The capital environment facing neurointervention is more favorable than that once experienced by coronary stents.

(Latest Financing Status of Neurointerventional Companies, Compiled by VCBeat)

From the distributor perspective, following centralized procurement of various high-value consumables, the market is predominantly left with large-scale distributors possessing substantial financial strength and superior professional capabilities. For neurointerventional companies, although these large distributors offer stronger promotional capabilities, their limited numbers will also makeNeurointerventional companies that enter the market early possess significant first-mover advantages.

Overall, neurointerventional companies have greater growth potential in terms of market, policy, capital, and competitive pressure, but they still need to make further progress in product quality, procedural adoption, distribution channels, and brand promotion.

Currently, China’s neurointerventional industry is still in its early stages of development. In 2017, the actual number of mechanical thrombectomy procedures performed in China was fewer than 15,000, with a penetration rate of only 0.56%. While this low penetration rate indicates substantial room for future growth, domestic neurointerventional companies must strengthen their promotional efforts and take proactive initiatives.

Regarding the issue of low penetration rates, some argue that the high prices of neurointerventional products limit affordability for patients, thereby hindering widespread adoption. Others contend that the scarcity of physicians qualified to perform neurointerventional procedures has impeded the promotion and dissemination of these products. Still others suggest that domestically produced neurointerventional products lag behind imported ones in quality. To uncover the more authentic underlying reasons, VCBeat conducted interviews with neurointerventional physicians, distributors, and neurointerventional companies.

From the perspective of the distributors we interviewed, China’s neurointerventional industry started late, and patient acceptance remains limited. There is still a quality gap between domestically produced neurointerventional products and imported ones, and the price reductions for domestic products have been relatively modest. “When coronary stents saw a 50% price cut compared to imported products, it made them affordable for many more people. Currently, performing a single neurointerventional procedure costs tens of thousands of yuan; severe cases require over one hundred thousand yuan, and even more critical cases can cost several hundred thousand yuan, placing a significant financial burden on many patients. Moreover, the cost of neurointerventional devices accounts for the majority of the total procedural expenses,” the distributor added. “Furthermore, there are relatively few physicians in China qualified to perform neurointerventional procedures, and challenges in promoting these surgical techniques hinder the development of the neurointerventional field.”

Offering a slightly different perspective, interventional neurologist Xue Chengjing stated, “Domestic neurointerventional products have shown significant quality improvements, with certain metrics of some products even surpassing those of imported alternatives. Regarding procedural costs, the use of relevant consumables depends on the patient’s pathological condition; overall, expenses are lower for patients in early stages and higher for those in advanced stages. Therefore, screening for cerebrovascular diseases in China needs to be strengthened.”

Regarding the issue of physician availability, Xue Chengjing stated, “Currently, there is a sufficient number of physicians in China capable of performing neurointerventional procedures, and such procedures are already being conducted at county-level hospitals. However, it takes 2–3 years to train qualified neurointerventional specialists due to the lengthy learning curve. While the projected explosive growth in neurointerventional procedures in the future may potentially impact product promotion, this is not currently the case.”

Public data shows that the volume of neurointerventional procedures in China increased from 77,400 in 2015 to 159,600 in 2019, with a compound annual growth rate (CAGR) of 19.8%.

From a physician’s perspective, disease-related factors also influence the penetration rate of neurointerventional procedures: the patient population with cerebrovascular diseases is smaller than that with cardiovascular diseases; moreover, cerebrovascular diseases have an acute onset and higher mortality rates, with some patients progressing from onset to death too rapidly for physicians to perform timely neurointerventional surgeries for treatment.

Furthermore, the current number of stroke centers in China remains limited, resulting in prolonged delays before patients with cerebrovascular diseases receive treatment. As the number of stroke centers increases, it will further drive the development of the neurointerventional industry.

Overall, factors such as product pricing, patient awareness, early screening for cerebrovascular diseases, and the number of stroke centers have influenced the penetration rate of neurointerventional procedures. These areas represent key challenges that neurointerventional companies must address.

For neurointerventional companies, advancements in imaging technology have gradually increased the detection rate of vascular diseases, enabling earlier screening for cerebrovascular disorders. Since neurointerventional procedures for early-stage cerebrovascular disease incur lower costs, a larger patient population combined with reduced treatment prices will further drive the development of the neurointerventional industry. Additionally, multiple factors—including policy support, capital investment, and market dynamics—are currently fueling the growth of neurointerventional enterprises.

Compared with coronary stent companies, neurointerventional enterprises enjoy a more favorable external development environment, but they still need to learn from coronary stent companies in terms of corporate decision-making.

An anonymous distributor stated, “First, domestic neurointerventional companies need to strengthen technological innovation and improve product quality so that their performance metrics reach world-leading levels. Second, they should adopt reasonable pricing strategies to benefit more patients with cerebrovascular diseases in China while also enabling companies to achieve higher profits. Finally, by training more physicians capable of performing neurointerventional procedures, the overall market can be expanded, thereby reducing competition and allowing all stakeholders to share in the benefits.”

In fact, most enterprises follow this approach. For example, Zhejiang Juchuang Tongqiao Medical Technology Co., Ltd. (JCTM), which is about to list on the Hong Kong Stock Exchange, has developed the “Jiaolong” Intracranial Thrombectomy Stent and completed a multicenter, single-blind, randomized trial. The trial results demonstrated that, compared with world-class thrombectomy devices, the Jiaolong Intracranial Thrombectomy Stent exhibited higher efficacy, increasing the successful recanalization rate by 7.5%, along with improved safety. In addition, JCTM is developing innovative products and optimizing existing ones to enhance their quality.

In terms of market expansion, GuiChuang Tongqiao currently relies on its distributor network to cover more than 1,000 hospitals and plans to reach additional hospitals that have not yet performed neurointerventional procedures, thereby expanding the neurointerventional market. As an increasing number of neurointerventional companies extend their coverage to new hospitals while avoiding or reducing competition in already-covered institutions, the penetration rate of neurointerventional procedures will rise more rapidly, further growing the neurointerventional market.

In terms of marketing and brand promotion, strategies among neurointerventional companies show some convergence. For instance, they actively participate in domestic and international conferences related to neurointervention; organize physician training sessions, educational seminars, and product exhibitions; engage in academic promotion at medical conferences by supporting renowned clinicians in delivering lectures and promoting neurointerventional procedures; collaborate with professional media platforms to participate in educational seminars and case presentations, thereby enhancing product visibility; conduct research and clinical collaborations with top-tier hospitals and physicians to strengthen R&D and innovation; partner with more distributors possessing strong professional capabilities to cover a broader range of hospitals and expand sales and service networks; and regularly visit physicians to showcase products, gather feedback, and optimize or innovate products based on their recommendations.

In addition, neurointerventional companies such as Zhongtian Medical are planning to establish comprehensive product portfolios covering either the full range of ischemic stroke devices or complete categories encompassing ischemic, hemorrhagic, and access-related products. This strategy is driven by the fact that a full suite of products can reduce surgical risks associated with switching between devices from different manufacturers, thereby further improving clinical outcomes. It also facilitates more efficient supply chain management and postoperative monitoring for hospitals, while enabling companies to adopt more flexible pricing strategies to respond to market competition.

Distributors interviewed believe that the marketing team also has a significant impact on commercialization. For example, Jetton’s intracranial thrombectomy stent and intracranial support catheter were launched in 2020; its neurointerventional sales costs increased from RMB 0 in 2019 to RMB 6.1 million in 2020, while payroll expenses for its marketing team rose from RMB 2.5 million in 2019 to RMB 13.2 million in 2020. Based on payroll expenditure calculations, the number of marketing staff at Jetton increased approximately sixfold compared with 2019 due to the launch of its neurointerventional products.

In summary, for neurointerventional companies to replicate the success trajectory of coronary stents, they must achieve the following:First, increase R&D investment to drive continuous innovation and product optimization. Second, implement reasonable pricing to make treatments more affordable for patients with cerebrovascular diseases. Third, train more physicians and expand hospital coverage to improve the accessibility of neurointerventional procedures. Fourth, strengthen brand promotion to enhance the recognition of domestically produced neurointerventional products among neurointerventionists. Fifth, build a professional and highly competent marketing team to drive the sales of neurointerventional products.

Due to space constraints, not all respondents’ views are included in this article. We extend our sincere gratitude to the experts, companies, and practitioners who contributed to this piece.