Shuidi Mutual Shuts Down: Is This the End for China's $9.2 Billion, 330-Million-User Mutual Aid Industry?

Which words can describe an industry at the forefront of rapid growth? Fierce competition among many players, and a battlefield shrouded in smoke.

Online mutual aid is precisely such an industry. From the germination of the “Zhongbao” model concept in 2011 to the competitive entry of tech giants such as Ant Group, Meituan, Baidu, Sina, and Didi, the online mutual aid sector experienced rapid growth. At its peak, the industry reached a point where “a new platform was launched every day.”

Data trends corroborate this boom. Survey data from Nankai University shows that,As of the end of May 2020, 330 million people in China had joined online mutual aid platforms, with the cumulative pool of mutual aid funds reaching approximately RMB 9.239 billion and the number of beneficiaries exceeding 70,000.In 2016, the number of members enrolled in online mutual aid programs was still less than 20 million.

However, just as online mutual aid platforms were surging ahead, the industry’s development trajectory took a sharp downturn.

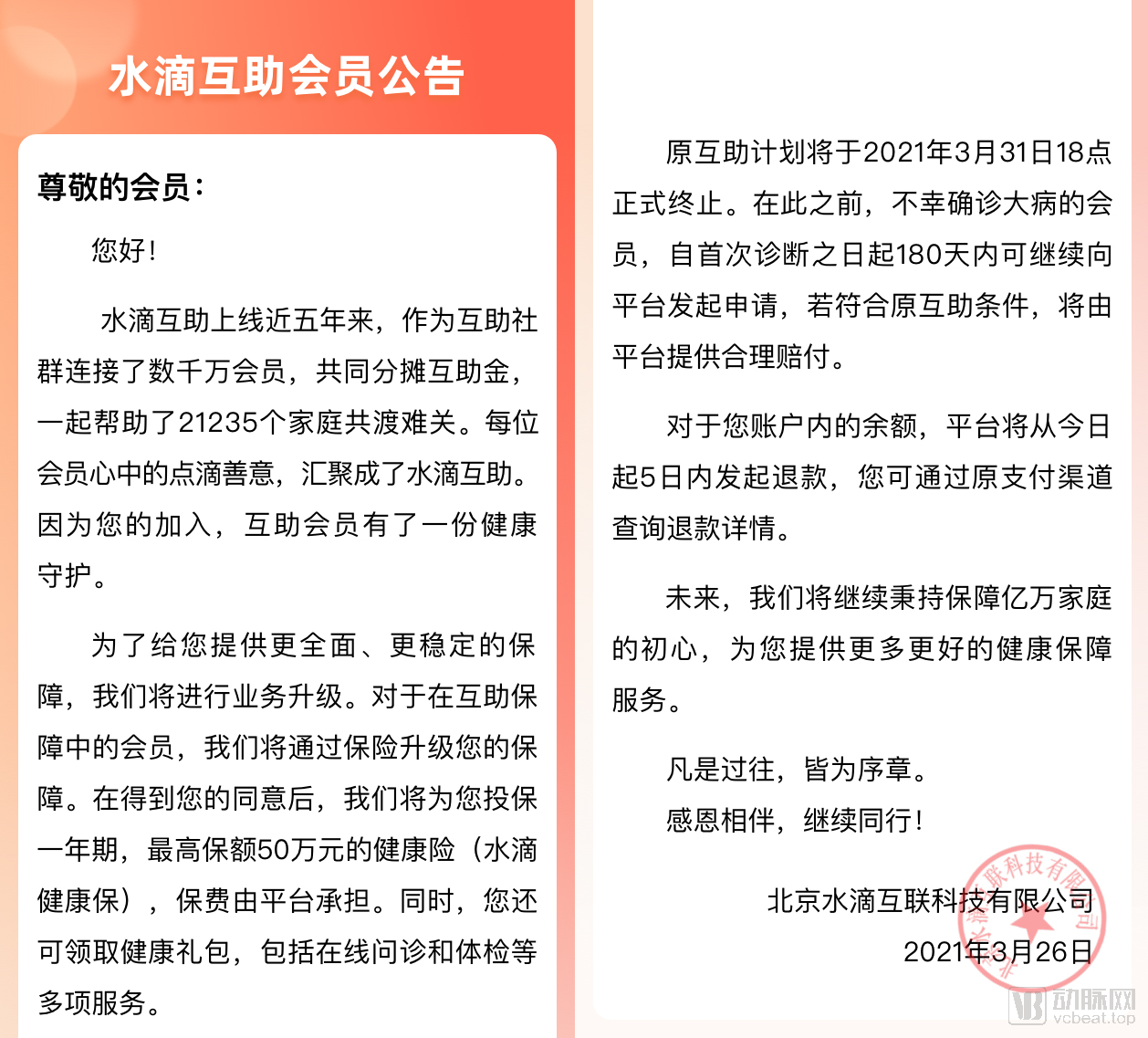

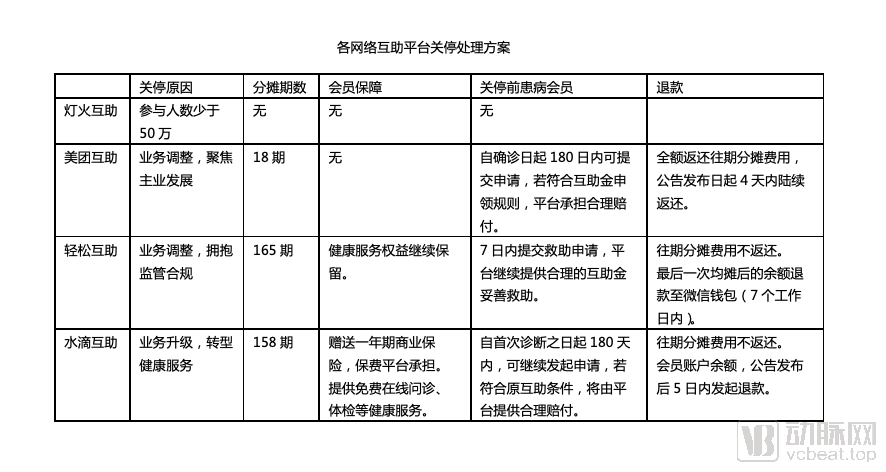

On March 26 at 18:00, Shuidi issued an official announcement stating that its original mutual aid program would be formally terminated on March 31, 2021, at 18:00.Prior to this, members who were unfortunately diagnosed with a critical illness may continue to submit claims within 180 days from the date of initial diagnosis. If they meet the original mutual aid eligibility criteria, the platform will provide appropriate compensation. For any remaining balance in user accounts, the platform will initiate refunds within five days from the date of the announcement.

This is the fourth mutual aid platform to shut down, following Baidu Mutual Aid, Meituan Mutual Aid, and Qingsong Mutual Aid.As of now, among the top three mutual aid platforms in China, only Ant Group’s “Xianghubao” remains (the other two, “Shuidi Huzhu” and “Qingsong Huzhu,” have just been shut down).

Thus,The online mutual aid industry, which had advanced vigorously for a decade, has reached a turning point.

This is closely linked to the increasingly stringent regulatory environment. In September last year, the China Banking and Insurance Regulatory Commission (CBIRC) released the “Study on Analysis of and Countermeasures against Illegal Commercial Insurance Activities,” explicitly pointing out that some online mutual-aid platforms have a large membership base and operate without proper licenses, posing significant risks to the public. Certain platforms employing upfront fee models accumulate pooled funds, creating a risk of operator absconding. Improper handling or inadequate management could further trigger social risks.

Will other platforms shut down or continue operations in the face of these challenges? Can online mutual aid services be relaunched in the future? These are questions of concern both within and outside the industry. However, until regulatory policies become clear, these issues remain unresolved.

HoweverIt is worth pondering that an industry’s ability to surge forward in the market for many years must be underpinned by inherent value.What value does online mutual aid bring? What is the logic behind the fierce competition among tech giants and capital investors? How might it evolve in the future?

Next, with these questions in mind, let us return to the arena of online mutual aid to witness the tumultuous decade that has unfolded.

In China, “difficulty and high cost in accessing medical care” has long been an unavoidable social issue.The emergence of online mutual aid is designed to enable people to share risks through internet-based platforms when facing critical illnesses.

This model first emerged in China in 2011. At that time, Mr. Zhang Mading, who had previously worked at Taiping Life Insurance and Guotai Junan Securities, founded the Anti-Cancer Commune (later renamed “Kang’ai Commune”) with the aim of addressing the medical cost burden for cancer patients. Within the commune, tens of thousands of members entered into a mutual agreement to mitigate the financial risk associated with a potential cancer diagnosis: if any member was diagnosed with cancer, the others would contribute funds to help raise several hundred thousand yuan for treatment. As the costs were shared among many participants, the individual contribution remained very low, significantly alleviating the financial pressure on cancer patients while providing peace of mind to those who remained healthy.

It can be seen that,Online mutual aid creates a risk contract pool through collective contributions, which then provides coverage on a cost-sharing basis for individuals facing medical expenses due to illness, accidents, or other hardships.This is quite similar to traditional insurance, except that it relies on mobile internet. As a result, it features low user entry barriers (with upfront fees as low as a few yuan), low intermediary costs (avoiding the high operational expenses of insurance companies), and self-propagating characteristics (whereas traditional insurance requires marketing), representing a certain degree of innovation in its business model.

By 2014, Kang’ai Gongshe had incorporated as a company, and its online mutual aid project entered the operational phase. Meanwhile, Yu Liang, a former media professional, detected business opportunities in the then-booming “crowdfunding” sector. He joined forces with five technicians to launch a startup from a hutong residence near the northeast second ring road in Beijing. Shortly thereafter, the project “Qingsong Chou” (Easy Fundraising) emerged from this team.

At this very moment, the favorable winds of policy began to blow.

In 2014, the State Council issued a document to encourage the accelerated development of the insurance industry, explicitly proposing to “encourage the development of mutual cooperative insurance in various forms.”In early 2015, the China Insurance Regulatory Commission (CIRC) promulgated the Interim Measures for the Supervision of Mutual Insurance Organizations, aiming to expand social insurance coverage across China and diversify the organizational forms of the domestic insurance market.

Entrepreneurs and investors who have spotted the opportunity are beginning to extend their reach into this sector.

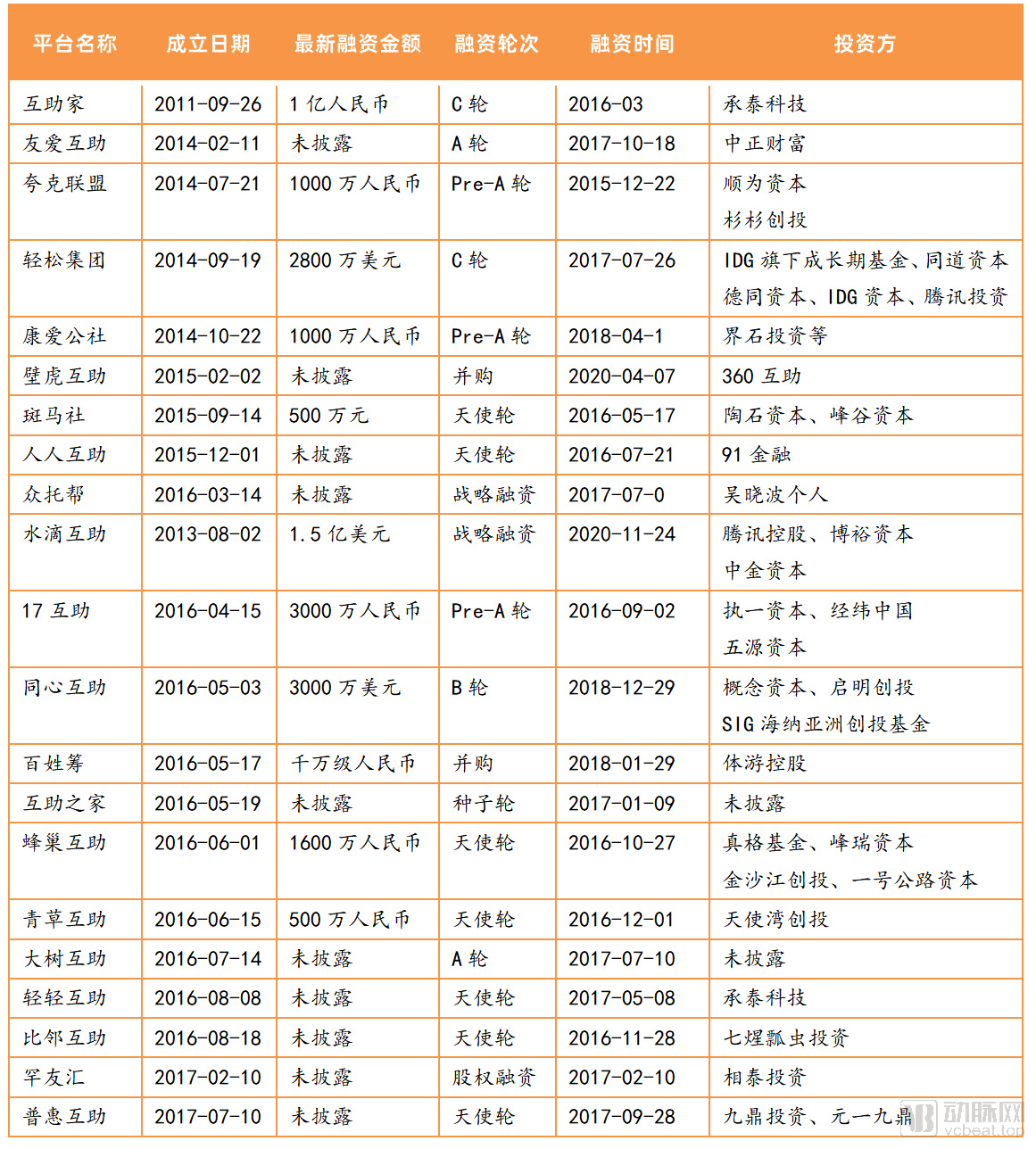

According to incomplete statistical data,At its peak in 2016, there were nearly 200 online mutual aid platforms, with many newly established companies securing financing ranging from millions to tens of millions of yuan.Interestingly, due to the sheer number of participants, a wide variety of animals and plants were featured in the naming conventions.

Overview of Online Mutual Aid Platforms That Have Secured Financing (Data Source: Tianyancha)

It was also in this year that Shen Peng, Meituan’s 10th employee, left Meituan Dianping to found Shuidi Inc. As the company’s inaugural offering, Shuidi Mutual Aid was officially positioned as an online mutual-aid community, providing members with low-threshold, cost-effective pre-event risk protection services. All members join the community in accordance with platform rules, engaging in mutual assistance to collectively mitigate risks such as cancer and accidents.

Leveraging its superior operational and product capabilities, Waterdrop Inc. rapidly expanded into China’s third-, fourth-, and fifth-tier cities as well as township markets. Amid the capital winter of the first half of 2019, it became a focal point of industry attention by securing over RMB 1.6 billion in consecutive financing rounds. During this period, its mutual aid business also experienced rapid growth. As of November 2020, Waterdrop Mutual Aid had provided assistance to more than 16,000 families, disbursing over RMB 1.75 billion in mutual aid funds.

The strong traffic performance and high-quality insurance scenarios presented by online mutual aid have prompted internet giants to take action as well.

In 2018, Ant Group and Xinmei entered the market through group insurance, launching the product “Xianghubao” (later renamed “Xianghubao”), which attracted 20 million users within just one and a half months and rapidly became China’s largest online mutual aid platform. Subsequently, internet companies such as JD.com, Didi, Suning, Meituan, Sina, Baidu, 360, and Xiaomi quickly followed suit. For a time, online mutual aid became a battleground where tech giants fiercely competed.

The underlying reason is that,Leveraging its low-barrier and inclusive nature, online mutual aid can drive insurance customer acquisition for tech giants and enable them to reach lower-tier markets.

After intense competition, the market landscape for online mutual aid began to take shape. Among them,The “big three” at the top are Xianghubao under Ant Group, Shuidi Huzhu under Shuidi Inc., and Qingsong Huzhu under Qingsongchou.The former has over 100 million enrolled individuals, while the latter two are in the tens of millions.

In the second tier are Meituan, Baidu, Didi, Suning, 360, Bige Mutual Aid, e-Mutual Aid, Kang’ai Commune, Quark Alliance, and Zhongtuo Bang, with participant numbers ranging from hundreds of thousands to tens of millions. Online mutual aid programs once enjoyed unparalleled prominence.

However, behind the rapid surge, problems with online mutual aid platforms continue to emerge.

On August 7, 2020, Baidu’s Denghuo Mutual Aid Program announced its closure after just 300 days of operation.

According to Baidu’s announcement, the Denghuo Mutual Aid Program was hastily discontinued because the number of participating members fell below 500,000.Therefore, to safeguard user rights and interests, the Denghuo Mutual Aid Plan has been suspended.

From the perspective of the industry's current situation, this is not merely an excuse from Baidu. It should be noted that although online mutual aid platforms have low operational costs and low user participation costs,However, as time goes by, the incidence rate among members will gradually rise, inevitably leading to an increase in shared costs.This will lead to a discrepancy between users’ expectations and their actual cost-sharing levels, thereby triggering churn among participating members. Such attrition, in turn, causes the shared costs for remaining members to continue rising, creating a vicious cycle.

Taking Xianghubao as an example, the platform’s critical illness mutual aid plan showed that the per-member contribution for the first period in August 2019 was RMB 1.47, which rose to RMB 3.01 in the first period of October 2019, and further surged to RMB 5.28 in the first period of January 2021.

Last December, the number of participants sharing costs in Xianghubao experienced a significant month-on-month decline of nearly 2% for the first time.

Therefore, as time progresses, rising per-capita contributions and a declining number of participants are inevitable challenges that online mutual aid platforms must confront.

Not only that,, online mutual aid platforms still face issues such as exaggerated advertising and lack of transparency.In the marketplace, online mutual aid plans offered by certain platforms operate in a legal gray area and are plagued by issues such as exaggerated marketing and selective disclosure of information—for instance, their official websites’ public disclosure pages lack any prompts regarding inquiries or complaints.

This is, in fact, related to the role played by online mutual-aid platforms."In the operation of online mutual aid services, the platform assumes only operational and managerial responsibilities and does not provide a risk guarantee."Therefore, in the actual processes of customer acquisition and claims settlement, online mutual aid platforms have neither the willingness nor the incentive to conduct rigorous screening of users’ health status. Instead, due to the linkage between management fees and the total amount of cost-sharing, as well as considerations of customer acquisition costs, there may be a tendency to relax entry and exit criteria. Over time, this will inevitably lead to serious problems of moral hazard and adverse selection.

Furthermore, the operational risks of mutual-aid platforms have also come under scrutiny. According to a report by Caixin,Currently, most online mutual aid platforms are operating at the break-even point.Generally, the management fee for online mutual aid programs is 8% of the amount allocated per contribution period. These funds are used to cover case investigations, reviews, and the administration of mutual aid fund inflows and outflows, among other related expenses. However, relying solely on this commission-based fee makes it difficult for many platforms to maintain cash flow, unless they supplement their revenue with subsequent commercial insurance products, health management services, and other offerings. Only leading platforms have the resources to rapidly establish such additional business lines.

In addition,The biggest issue lies in the fact that the powerful traffic effect of online mutual aid has turned it into a rapidly growing pool of funds and endowed it with vast amounts of user information. All of these matters concern public interest.

Don’t forget that P2P lending, which aggregated vast amounts of capital and users, serves as a cautionary tale; its collapse had profoundly negative societal repercussions.

It is precisely for these reasons that the signals from regulators are becoming increasingly clear.

Earlier this year, following the shutdown of Meituan Mutual Aid, Xiao Yuanqi, Chief Risk Officer and Spokesperson for the China Banking and Insurance Regulatory Commission (CBIRC), stated at a press conference held by the State Council Information Office, “We believe that the primary reasons for its closure were the deviation of Meituan Mutual Aid from Meituan’s core business and the continuously increasing risk of adverse selection. Moving forward, we will continue to closely monitor mutual aid operations conducted by internet companies, assess their operational models and risk profiles, and take appropriate measures as warranted.”

Amid the grim situation, multiple platforms have long been attempting to regularize their mutual aid businesses. An insider told VCBeat that Shuidi Inc., whether through acquiring a stake in Anxin Property & Casualty Insurance or engaging in repeated communications with regulators, has sought to obtain an internet insurance company license, but progress has not been smooth.

Therefore,Following Qingsong Chou’s shutdown of its Qingsong Mutual Aid platform, Shuidi also announced the closure of Shuidi Mutual Aid. Both companies are currently rumored to be planning initial public offerings (IPOs), and abandoning their mutual aid businesses is aimed at preventing potential compliance issues from becoming “stumbling blocks” to their listings.

Taking Ant Group’s prospectus released last October as an example, the “Listing Risks” section explicitly stated: “If Xianghubao fails to meet regulatory compliance requirements for any reason and is deemed unsuitable for continued operation by Ant Group as a listed company, Ant Group will divest the Xianghubao business.”

In other words, if Ant Group relaunches its IPO plan this year, the Xianghubao business is also likely to be spun off or shut down. Should this occur, the last of the “big three” online mutual aid platforms may cease to exist.

Of course, it is still too early to declare the endgame. Continued observation is required regarding the subsequent actions of existing online mutual aid plans such as Xianghubao, Suning Ninghubao, Didi Diandi Mutual, 360 Mutual Aid, Zhongtuobang, and Quark Alliance.

However, one thing is certain: under the trend of increasingly stringent national regulatory policies, the inflection point for the online mutual aid industry has arrived.

In the announcement released by Shuidi Mutual Aid yesterday, it was stated that “to provide users with more comprehensive and stable coverage, we will upgrade our service model to offer health protection services.” Specifically, Shuidi Mutual Aid has introduced Shuidi Health Insurance for its members, with a one-year coverage period fully funded by the platform. The company also commits to providing members with free online medical consultations, health check-ups, and other health-related services.

In fact, during an earlier speech, Shen Peng, founder and CEO of Shuidi Inc., stated that “a significant portion of Shuidi Mutual Aid’s members are from China’s third-, fourth-, and fifth-tier cities.” These users recognize the limited coverage provided by social insurance, but due to financial constraints, they find commercially priced health insurance plans less appealing. Consequently, online mutual aid platforms like Shuidi Mutual Aid serve as supplementary products bridging the gap between social insurance and commercial health insurance, providing coverage for this demographic.

In other words,As inclusive products, online mutual aid platforms primarily serve to expand coverage and cultivate users’ habits of adopting protection products beyond social insurance. The real “prize” these platforms aim to capture, however, is the commercial health insurance market behind them.

Relevant data indicate that China’s direct premium income for health insurance exceeded RMB 800 billion in 2020, with the premium scale projected to surpass RMB 1 trillion for the first time in 2022 and reach RMB 2.021 trillion by 2025, underscoring the market’s substantial growth potential.

Additionally,From the perspective of market competition, online mutual aid has also faced a formidable rival in the past one to two years—Huiminbao.It is a supplementary medical insurance system for catastrophic and critical illnesses, established on the basis of social medical insurance, featuring government leadership, commercial insurance administration, voluntary enrollment, and multi-channel financing.

Unlike online mutual aid schemes, which lack regulatory oversight, Huiminbao constitutes a formal insurance product., it performs better in terms of risk management, stability, and government endorsement. Furthermore, insurance companies bidding for government-backed inclusive health insurance projects are subject to strict profit margins, granting them a pricing advantage. This has fueled the aggressive expansion of inclusive health insurance into new cities since last year. As of February this year, inclusive health insurance had covered nearly 200 cities across China, with over 25 million enrollees and total premiums exceeding RMB 1 billion.

Similar to the role of online mutual aid,"Hui Min Bao" also serves as a bridge connecting basic medical insurance and commercial health insurance, with a certain degree of substitutability between them.Consequently, leveraging the aforementioned advantages, major internet insurance platforms have significantly increased their investments in Huiminbao (city-specific supplementary medical insurance), while the market position of online mutual aid has declined.

From this perspective, the historical role of online mutual aid has been fulfilled, and similar products have emerged in the market. Therefore, whether online mutual aid iterates and upgrades under new regulatory policies or is replaced by other inclusive insurance products, it has already left an indelible mark on the development journey of China’s health insurance industry.

Moving forward, the industry must consider how to support the development of China’s multi-tiered medical security system through a greater number of higher-quality products.

Finally, what mindset should we adopt toward an industry that has delivered value to people suffering from serious illnesses but is now drifting away from the spotlight?

"Though tinged with regret, it is nonetheless imbued with profound respect."