Frenzied Capital Rush into Mitral Valve Therapies: Over RMB 2 Billion Raised, Market Size Expected to Triple That of TAVR

Surgical intervention for valvular heart disease is among the most challenging procedures in the field of structural heart disease, and the advent of transcatheter interventional therapy has rewritten the history of this domain. This technological breakthrough, transitioning from open-heart surgery to minimally invasive interventions, has not only transformed the landscape of disease treatment but also turned heart valves into a lucrative market. Globally, the heart valve sector has given rise to Edwards Lifesciences, a company with a market capitalization nearing $50 billion. In China, the transcatheter aortic valve replacement (TAVR) sector alone has spawned three publicly listed companies: MicroPort CardioFlow, Venus Medtech, and Peijia Medical.

Where Will the Structural Heart Disease Market Beat Next? Undoubtedly, the Mitral Valve Is Currently the Most Heavily Bet-On Sector.

In the primary market, industry insiders have reported a surge in valuations and intense competition for projects in the mitral valve sector. According to the Artery Orange database, the field of transcatheter mitral valve interventions attracted over RMB 2 billion in funding between 2020 and 2021.

Among the strategic initiatives of industry giants, the mitral valve segment has also become a fiercely contested arena. Both Abbott and Edwards Lifesciences view the mitral valve as a future growth driver in the field of structural heart disease. Abbott’s CEO stated at the J.P. Morgan Healthcare Conference that the company is optimistic about opportunities in the mitral and tricuspid valve sectors. Edwards Lifesciences has also made the mitral valve a key focus of its R&D efforts. When announcing its 2020 financial outlook, the CEO of Edwards Lifesciences remarked, “In 2021, global sales of transcatheter mitral or tricuspid valve therapies are expected to approximately double.”

The surging interest in mitral valve interventions is driven by market expectations that the mitral valve market will be three to four times the size of the TAVR market, with the global market potential reaching hundreds of billions of yuan. As the door opens to this hundred-billion-yuan market for transcatheter mitral valve therapy, why are investors increasingly bullish on this early-stage sector? Which companies have secured their entry tickets? VCBeat (WeChat ID: vcbeat) interviewed industry insiders to provide an analysis.

It may be hard to imagine that, for the human heart alone, engineers have developed a wide array of precision devices—including stents, balloons, and artificial valves—supporting markets worth hundreds of billions.

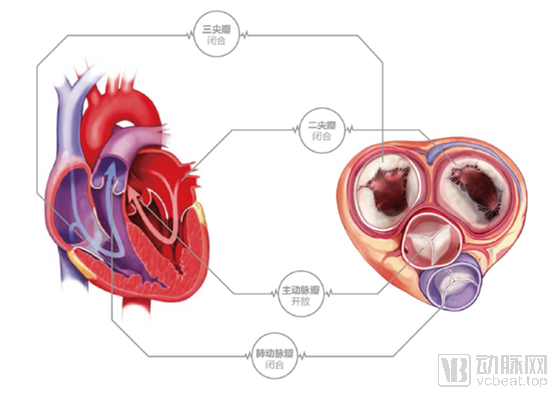

Among these multi-hundred-billion-dollar markets, valvular heart disease—a condition that has garnered increasing global industrial attention in recent years—is actually a type of structural heart disease. It involves the four cardiac valves (the aortic valve, mitral valve, tricuspid valve, and pulmonary valve). When one of these four valves is damaged or defective, resulting in valvular heart disease, structural and functional abnormalities occur, preventing the valve from fully opening (stenosis) or fully closing (regurgitation).

In recent years, transcatheter valve intervention has gradually replaced traditional open-heart surgery for the treatment of valvular heart disease, owing to advantages such as lower procedural risk, minimal invasiveness, shorter hospital stays, and faster recovery.

The aortic and mitral valves have received the most attention because, based on prevalence statistics, aortic stenosis and mitral regurgitation are the most common types of valvular heart disease, accounting for 9.2% and 45.4% of global cases, respectively, in 2019. Tricuspid valve disease (including tricuspid stenosis and tricuspid regurgitation) is another common type of valvular heart disease.

Mitral regurgitation accounts for 45.5%, a figure that underscores the significant burden of mitral valve disease among valvular heart diseases.Although we rarely notice the mitral valve when it is functioning normally, it continuously opens and closes in rhythm with life. The mitral valve is the cardiac valve that prevents blood from flowing backward from the left ventricle into the left atrium. During diastole, blood flows through the mitral valve into the powerful left ventricle; during systole, the mitral valve closes, and blood is ejected from the left ventricle through the aortic valve into the aorta, subsequently circulating throughout the body via the arterial system.

When mitral valve disease occurs, it can manifest as mitral regurgitation, mitral stenosis, or mitral valve prolapse, with mitral regurgitation accounting for 65% of the prevalence of all mitral valve diseases. Mitral regurgitation (MR) refers to the condition in which the mitral valve fails to close completely, resulting in the backflow of blood from the left ventricle into the left atrium during ventricular systole.

In China, the number of patients with valvular heart disease reached 36.3 million in 2019, among whom those with aortic stenosis, mitral regurgitation, and tricuspid regurgitation accounted for 11.8%, 29.2%, and 25.1% of all valvular heart disease patients, respectively. Valvular heart disease is becoming increasingly prevalent among the population aged 65 years and older in China. (Source: Report on Cardiovascular Diseases in China 2019)

An investor in a company specializing in transcatheter mitral valve interventions shared the following story: During the investment committee meeting for this project, they inadvertently discovered that the project’s legal counsel, external lawyers, the foundation’s attorneys, and even a colleague on the project team all had varying degrees of mitral regurgitation. Although the symptoms and severity differed among them, this incident highlighted that mitral regurgitation is a common condition.

In addition to the large patient population, another key characteristic of the mitral valve market is the low penetration rate of disease treatment. Due to the lack of effective therapeutic options and commercialized products, as well as the high surgical risk associated with the anatomical characteristics of the mitral valve itself, less than 1% of patients with mitral regurgitation worldwide underwent surgical intervention in 2019.

Transcatheter mitral valve therapies may help address the current underpenetration in the treatment of mitral valve disease. Transcatheter Mitral Valve Repair (TMVR) is a catheter-based technique that repairs the mitral valve through an interventional procedure without open-heart surgery. Transcatheter Mitral Valve Implantation (TMVI) refers to the implantation of a new mitral valve via an interventional procedure without open-heart surgery. Transcatheter mitral valve repair or replacement has emerged as two potential alternative treatment options for patients with severe mitral regurgitation (MR) who are inoperable or at high surgical risk.

The mitral valve market, characterized by its large scale yet insufficient penetration, demonstrates significant growth potential. According to Frost & Sullivan’s projections, driven by the rising demand for mitral valve repair and replacement, as well as innovative transcatheter mitral valve technologies,By 2030, the global market size for transcatheter mitral valve interventions is projected to reach $17.4 billion (approximately RMB 117 billion), ultimately growing to three to four times the size of the global TAVR market.

With continuous technological updates and iterations,A clear trend is that products capable of addressing these clinical limitations will benefit the most from the large yet unmet clinical needs in mitral valve therapy.This is also why investment institutions are willing to bet on transcatheter mitral valve products.

The frequent financing activities from the second half of 2020 to 2021 were driven by the critical pre-approval phase for transcatheter mitral valve devices. Abbott’s mitral valve repair product, having received FDA approval seven years earlier, finally obtained market authorization from China’s National Medical Products Administration (NMPA) in June 2020. In the subsequent months, multiple domestic companies made significant progress in clinical trials of transcatheter mitral valve technologies.

Some industry insiders estimate that the mitral valve market will be three times the size of the TAVR market; this projection is actually conservative for the Chinese market. While the incidence of aortic valve disease in China is lower than that in other countries, the prevalence of mitral valve disease is significantly higher. Therefore, we predict that the future mitral valve market in China will undoubtedly be several times larger than the TAVR market.

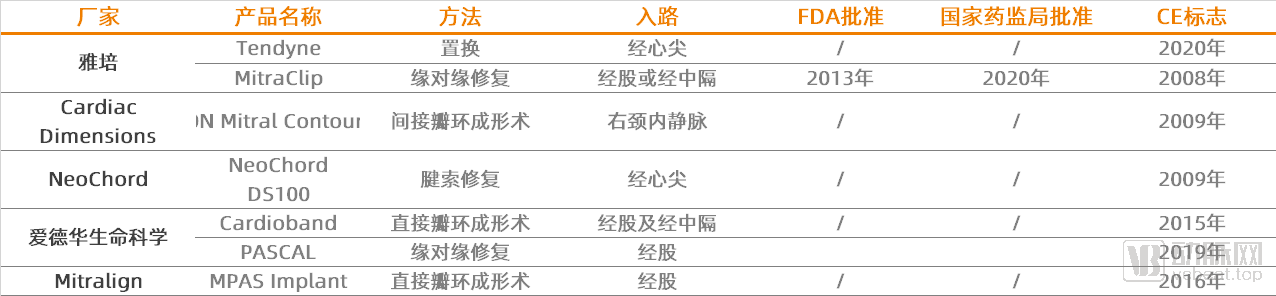

The vast market potential in the mitral valve space has attracted a host of medical device giants, including Abbott, Edwards Lifesciences, Medtronic, MicroPort Scientific, and Blue Sail Medical, while also drawing numerous startups. However, to date, Abbott remains the only company holding tickets to enter the major global markets.

Globally, there are only six approved mitral valve repair products and one approved mitral valve replacement product on the market. Abbott’s edge-to-edge repair product is the only one to have received approval from the U.S. FDA, China’s National Medical Products Administration (NMPA), and CE certification.

Commercialization Status of Global Transcatheter Mitral Valve Products

Product development in the mitral valve field is challenging, and there are relatively few products on the market. This is primarily because the anatomy and location of the mitral valve pose greater difficulties for the development of transcatheter interventions, with numerous hurdles in product design and development yet to be overcome.

First, mitral valve treatment is complex. The etiology of mitral valve disease often involves the combined effects of valvular insufficiency, other cardiovascular failures, or cardiovascular damage. Therefore, the management of mitral valve disease is more complex.

From the perspective of location and structure, the position of the mitral valve (situated between the left atrium and left ventricle) and the characteristics of the mitral annulus increase the difficulty of preparing for prosthetic valve implantation and impose higher requirements on the design of delivery systems. Compared with the aortic valve, the mitral valve is subjected to higher left ventricular systolic pressure, making it more susceptible to structural damage; therefore, enhanced durability is required. The mitral annulus is relatively large, which may necessitate the implantation of larger stents during mitral valve replacement and repair. However, large stents may cause adverse effects such as obstruction of the left ventricular outflow tract and thrombus formation. Consequently, improved stent design is essential. In terms of shape, the saddle-shaped configuration of the mitral annulus increases challenges related to sizing and positioning, thereby potentially elevating device-related risks and complications in mitral valve repair and replacement procedures.

From the perspective of technical approaches to addressing these issues, transcatheter mitral valve repair (TMVR) and transcatheter mitral valve implantation (TMVI) represent two major directions. Among them, TMVR can be categorized into the following types based on technical principles: ① transcatheter edge-to-edge mitral valve repair; ② transcatheter mitral annuloplasty, including direct and indirect annuloplasty; ③ transcatheter implantation of artificial mitral chordae tendineae; and ④ ventricular-annular remodeling. Currently, mitral valve repair surgery has become relatively mature, with mortality rates for various repair procedures around 1%, five-year reoperation rates below 10%, and recurrence rates under 20%, indicating that both safety and efficacy have reached high standards. TMVI carries higher risks.

Currently, the major global medical giants, including Abbott, Edwards Lifesciences, and Medtronic, are all adopting a strategy of simultaneous deployment in both replacement and repair products.

Will the future market be dominated by replacement products or repair products? An investor stated, “We tend to believe that repair will remain the mainstream approach in the future. The primary reason is that, based on cardiac surgery data, the proportion of repair procedures is significantly higher than that of replacement procedures. Repair surpasses replacement because the mitral valve occupies a highly specialized anatomical position, where intraventricular pressure reaches its peak throughout the entire heart chamber. Consequently, achieving secure fixation and stable landing for interventional devices poses considerable technical challenges.”

From the perspective of access routes, the choice between transapical and transfemoral approaches for mitral valve repair and replacement represents a major dimension of product differentiation. In transcatheter aortic valve replacement (TAVR), the transfemoral approach offers higher safety and has become the preferred option for most patients. However, for mitral valve interventions, further clinical data are needed to validate whether the transfemoral or transapical approach is optimal.

In comparison, the transfemoral approach is less invasive but demands a higher level of technical proficiency from physicians and imposes more stringent requirements on delivery system design. The transapical approach shortens the surgical access route, significantly reduces operative time, features a shorter learning curve for physicians, and allows for more direct and stable manipulation.

To achieve greater breakthroughs in the field of mitral valve replacement/repair, multiple mitral valve repair and replacement products are currently under development.

Although the commercialization of transcatheter mitral valves has lagged behind that of transcatheter aortic valves, the intensity of competition in the overall market is no less than that in the aortic valve market., each one sharpening its weapons and feeding its horses, arriving with aggressive momentum.

Major Mitral Valve Products Under Development in China

Currently, the major players in the Chinese market can be categorized into three groups: the first comprises global medical device giants such as Abbott and Edwards Lifesciences; the second consists of startups focused on the mitral valve sector, such as Hanyu Medical and Nuomai Medical; and the third includes domestically listed companies in the heart valve field, such as MicroPort CardioFlow, Venus Medtech, and Peijia Medical, which have already achieved commercialization progress in the transcatheter aortic valve sector.

In this nascent market, Abbott and Edwards Lifesciences currently hold the upper hand. Abbott’s MitraClip, launched in 2008, remains the only approved transcatheter mitral valve repair product in the U.S. market to date. The MitraClip has become the primary growth driver for Abbott’s structural heart business. According to JP Morgan data, the MitraClip generated approximately $690 million in sales in 2019 and is projected to generate around $670 million in revenue in 2020. Meanwhile, Abbott’s overall structural heart business achieved approximately $1.4 billion in revenue in 2019.

In the valve sector, Edwards Lifesciences, which has achieved success with its aortic valve products, has not overlooked the mitral valve arena and has already launched the PASCAL transcatheter mitral valve repair system. In a presentation at J.P. Morgan, Michael Mussallem, Chairman and CEO of Edwards, highlighted the opportunities in mitral and tricuspid valve interventions. When announcing the company’s 2020 financial results last month, he projected that global sales of transcatheter mitral and tricuspid therapies (TMTT) would approximately double by 2021.

Other emerging giants in the mitral valve field include Boston Scientific, which acquired Millipede for $325 million in 2018. Millipede’s products are used for minimally invasive interventional treatment of mitral regurgitation.

Another category of companies worth noting is domestic startups, such as Hanyu Medical and Newpulse Medical. These Chinese startups are making rapid clinical progress, have accumulated a certain level of technical expertise, demonstrate strong execution capabilities, and have secured access to key clinical expert resources in China, positioning them to become highly competitive players in the valve sector.

On March 19, Hanyu Medical completed the enrollment of the last patient in the pre-market clinical study for ValveClamp, the world’s first transapical mitral valve clip device. The product is expected to be launched next year. MicroPort’s mitral valve replacement system, Mi-thos®, officially entered registrational clinical trials on February 3, 2021.

However, it is worth noting that domestic startups in China are also imitating the mitral valve products of Abbott and Edwards Lifesciences. Since Abbott’s MitraClip patent has expired, there are few obstacles for Chinese companies to produce generics. However, Edwards Lifesciences’ PASCAL system remains under patent protection; therefore, complete imitation would entail potential intellectual property (IP) risks.

The third category of companies comprises those with commercialized products in the TAVR field, primarily including MicroPort CardioFlow, Peijia Medical, and Venus Medtech.

MicroPort CardioFlow’s strategy in the mitral valve market combines independent R&D with overseas mergers and acquisitions. In terms of international collaborations, MicroPort CardioFlow has invested in 4C Medical and ValCare, both of which specialize in the research and development of medical devices for mitral and tricuspid valves. The transcatheter mitral valve replacement system developed by 4C Medical features fully recapturable and retrievable capabilities.

Peijia Medical has also made progress in the field of mitral valve interventions. In December 2020, Peijia and HighLife signed a licensing and technology transfer agreement for transseptal mitral valve replacement products. Under this agreement, HighLife granted Peijia Medical an exclusive license to its TMVR patented products under development, with Peijia Medical holding the rights to manufacture, develop, and sell these products in the Greater China region. The TMVR technology developed by HighLife employs a transseptal approach to treat patients with mitral regurgitation and is currently undergoing international clinical trials at more than 20 research centers across three continents. Regarding independently developed products, on December 4, 2020, Peijia successfully conducted phased animal studies for its mitral valve repair product. This product utilizes novel patented technology to treat mitral regurgitation via a transseptal approach.

In May 2020, Venus Medtech entered into a collaboration with Opus Medical Therapies to jointly develop, manufacture, and market products for transcatheter mitral valve replacement (TMVR) and transcatheter tricuspid valve replacement (TTVR). Furthermore, as both Dejin Medical and Venus Medtech are part of the Denovo Medical platform, Dejin Medical has developed a transcatheter mitral valve repair product in the mitral valve field—the MitralStitch® Mitral Valve Repair System.

At this stage, clinical data for mitral valve products have not yet been released. Moving forward, the key competitive factors in the mitral valve sector will be product innovation, meeting clinical needs, and risk mitigation.

To some extent, as the competitive landscape in the TAVR sector has solidified and multiple companies have completed their IPOs, the mitral valve space has become crowded, with industry attention even beginning to spill over into the tricuspid valve field.

Tricuspid Regurgitation (TR) refers to the condition in which the tricuspid valve fails to close completely, causing blood to flow backward from the right ventricle into the right atrium during systole. In 2019, the global number of patients with tricuspid regurgitation reached 49.6 million, with a compound annual growth rate (CAGR) of 2.1% from 2015 to 2019. In the same year, the number of TR patients in China reached 9.1 million. However, due to the significant challenges in developing effective therapies for tricuspid valve disease and the complexities associated with surgical interventions, only three commercial transvenous tricuspid valve (TTV) repair products are available in Europe to date, none of which have been approved in the United States or China.

It is worth noting that the mitral and tricuspid valves share certain structural similarities. Changes in the geometry and characteristics of the right ventricle can directly affect tricuspid regurgitation, while mitral regurgitation is largely influenced by the geometry and properties of the left ventricle. Therefore, studies have suggested that certain mitral valve repair and treatment techniques may be applicable to the management of tricuspid valve disease.

Michael Mussallem, CEO of Edwards Lifesciences, believes that the global market size for transcatheter mitral and tricuspid therapies (TMTT) will reach $3 billion by 2025 and continue to grow significantly. Mussallem asserts that, in terms of patient population, the market size for tricuspid valve disease will be comparable to that of mitral valve disease.

However, industry insiders have pointed out that, compared with the mitral and aortic valves, the key issue for the tricuspid valve lies in the significant uncertainty surrounding its market size. If the incidence of tricuspid valve disease is primarily driven by severe end-stage heart failure, then as the markets for aortic and mitral valve interventions continue to mature, the pool of patients eligible for tricuspid valve therapies will gradually shrink. Therefore, the future market potential for tricuspid valve interventions may not offer the same broad growth prospects as those seen in the mitral and aortic valve sectors.

Although there are still many visible risks and challenges in the fields of mitral and tricuspid valves, which are mainly concentrated on technical aspects, we can remain optimistic about overcoming these technical difficulties.But as Cleveland put it: “On the technology front, I have always been a helpful optimist. I never dare to oppose it, because it seems that a group of shrewd engineers with sufficient venture capital can overcome almost anything.”