China's Largest Doctor Community Yimaitong Files for Hong Kong IPO: Can Its 2.4 Million Doctors Support Its Valuation?

On March 29, Medlive Technology Co., Ltd. filed an application for listing on the Main Board of the Hong Kong Stock Exchange, with Goldman Sachs and Haitong International serving as joint sponsors.

Medlive’s predecessor, Tecan Software Technology, was originally established in 1996, making it one of the early pioneers in the digital health sector. Throughout the history of digital health development, companies founded around the same time as Medlive include DXY, MedSci, Xunyi WenYao, and Haodf Online. Leveraging the internet as a medium, these companies initiated early explorations into digital healthcare business models.

Over the past two decades, having witnessed the ebbs and flows of the digital health sector, Medlive, as a medical knowledge service provider, has evolved from a physician-focused tool into a physician community.Currently, Medlive has attracted 2.4 million registered practicing physicians, accounting for 58% of all practicing physicians in China.With more than half of China’s licensed physicians as its users, Medlive generated RMB 213.5 million in revenue in 2020, representing a compound annual growth rate (CAGR) of 59.9% from 2018 to 2020. Its net profit for 2020 reached RMB 85.2 million, with a CAGR of 145.0% from 2018 to 2020.

The medical knowledge platform sector, in which Medlive operates, has attracted significant capital interest, with numerous large-scale financing rounds. In 2017, U.S. private equity giant KKR acquired WebMD Health, the largest healthcare knowledge services website in the United States, for $2.8 billion. In China, DXY secured a $500 million investment from Trustbridge Partners, Tencent, and Hillhouse Capital in 2020, while ByteDance acquired Baike Mingyi Network for RMB 500 million.

Although Medlive holds core physician resources within the medical ecosystem and experienced the post-2015 digital health boom, it did not choose to introduce external capital, having only accepted a strategic investment from M3, Japan’s largest physician community, in 2013.

Tian Lixin, founder of Medlive, stated that prior to M3, other investors had also approached him; however, at that time, Tian did not accept their proposals or the “Internet mindset” they advocated.

Today, the investment frenzy in digital health has subsided, and the wave of capital inflow has receded. This may allow us to better reflect on the essence of physician communities. Is a physician community a viable business model in China? How high is its growth ceiling? How does Medlive monetize its physician resources? VCBeat (WeChat ID: vcbeat) has analyzed Medlive’s prospectus to provide insights.

Although Medlive has attracted more than half of China’s physicians to register, it was not the earliest online physician community in the country. Medlive’s predecessor, Tekeng Software Technology, was initially positioned as a developer of dictionary software. In June 1996, siblings Tian Liping and Tian Lixin established Tekeng Software Technology with the aim of providing robust medical knowledge tools for healthcare professionals; Tian Lixin graduated from Tsinghua University with a major in Engineering Physics. In 1998, they developed a professional medical translation software product, the “Comprehensive Medical Dictionary,” which greatly facilitated Chinese physicians’ reading of English-language materials.

Following the approach of developing software tools for physicians, they launched their second medical software product, Drug Reference, in 2000 to assist clinicians in decision-making; in 2004, they introduced their third medical software product, Medical Literature King, to meet physicians’ needs for literature search and management.

Medlive was not officially launched until 2006. The impetus for Medlive’s establishment was its “split” from DXY.

From 2004 to 2009, the predecessor of Medlive was an exclusive partner and a key client of DXY. All its internet-related operations were conducted on the DXY platform. However, Tian Lixin later recognized that delivering high-quality medical information services necessitated a dedicated internet platform. Against this backdrop, Medlive was established, positioning itself to serve the physician community with a knowledge base at its core. Its professional medical content encompasses clinical guidelines, research literature, drug references, clinical advances, and customized content.

At the time of Medlive’s founding, the business model of medical information platforms already had numerous successful cases worldwide. In the United States, in addition to WebMD Health, there were companies such as Doximity and Epocrates; in Japan, there was M3.

This model has been validated in the global market, primarily because there is room for digital transformation on both the demand and supply sides.

On the demand side, physicians face a strong need for continuous learning as medical knowledge continues to evolve. Chinese physicians, in particular, encounter multiple challenges in meeting the demands of continuing medical education and clinical decision support, such as limited time and resources for learning and research.

On the supply side, physicians play a pivotal role in the healthcare market’s value chain as the primary decision-makers for prescribing medical products. Pharmaceutical companies need to leverage marketing strategies to convey information on disease symptoms, treatment options, and product specifications to physicians, thereby enhancing their awareness and understanding of specific drugs and medical devices, and influencing their prescribing decisions.

Previously, the marketing of prescription drugs primarily relied on visits by medical representatives, industry conferences, and academic promotion. Under intense regulatory pressure, the model of medical representative visits is facing increasingly stringent compliance challenges, prompting pharmaceutical companies to undergo a transformation in their marketing strategies. With the rapid development of the internet and the emergence of digital tools, digital marketing has undoubtedly provided a complementary solution to the traditional marketing system.

Compared with offline visits and academic conferences, digital marketing is more cost-effective and can reach a broader range of physicians more efficiently. With the acceleration of the digital era and the price pressures faced by pharmaceutical companies under the trend of medical insurance cost containment, the market penetration rate of digital marketing is rising rapidly.

Compared with the United States and Japan, China’s healthcare marketing efficiency is lower. On one hand, due to the scarcity of medical reference tools available to support clinical decision-making, the penetration rate of digital medical information services remains low in China, a problem that is even more pronounced in the vast grassroots market. Meanwhile, Chinese doctors have consistently been more accustomed to learning about new drugs, as well as novel diagnostic and therapeutic methods, from pharmaceutical and medical device companies through direct contact with medical representatives.

However, in Japan, digital push notifications are quite prevalent, with 85% of Japanese physicians receiving them through professional physician platforms. In 2020, digital healthcare marketing expenditures accounted for 2.3% of total healthcare marketing spending in China, compared to 9.5% in Japan.

With the application of technologies such as AI and big data, digital marketing can now deliver customized content to physicians, making professional physician platforms more effective for digital healthcare marketing. Digital marketing is being increasingly adopted by pharmaceutical companies, and its market size is projected to reach hundreds of billions.

According to the Frost & Sullivan report,China’s digital healthcare marketing market grew from RMB 4.4 billion in 2018 to an estimated RMB 15.4 billion in 2020, representing a compound annual growth rate (CAGR) of 86.7%, and is projected to reach RMB 113.3 billion by 2025.The compound annual growth rate was 49.2%. In 2018 and 2020, the digital healthcare marketing market accounted for 0.8% and 2.3%, respectively, of the total healthcare marketing market in China, and is expected to further increase to 11.4% by 2025.

In the future trillion-yuan market of digital marketing, numerous enterprises are vying for a share. Currently, medical platforms offering digital marketing services generally fall into the following three major categories:

Professional Physician Platform: Physician users acquired by providing professional medical information and services. Revenue is primarily generated through physician subscription fees and digital marketing services provided to pharmaceutical companies. Representative platforms include Medlive and DXY.

E-commerce Platform:It primarily provides online retail pharmacy and medical services to consumers and patients. Alibaba Health and JD Health are representative of this model.

Internet Hospital:Provide online medical services for patients, including online consultations, prescriptions, and chronic disease management. WeDoctor and Haodf Online are representative examples.

In the niche of professional physician platforms where Medlive operates,Physician coverage, activity, and stickiness are core competitive advantages. A high-quality physician community should feature broad coverage, high activity, and strong stickiness.. For pharmaceutical companies, the number of physicians aggregated on a third-party platform and their level of engagement are also important metrics when selecting such platforms.

For Medlive, in terms of broad coverage, it has approximately 3.5 million registered users, among whom about 2.4 million are licensed physicians, accounting for roughly 58% of all licensed physicians in China. According to Frost & Sullivan, Medlive is the largest professional physician community in China. However, there is still room for improvement when compared with major international physician communities; both Japan’s M3 and the United States’ Doximity have physician coverage rates exceeding 60%. In terms of monthly active users (MAU), Medlive’s average MAU exceeded 1 million in the fourth quarter of 2020, with a monthly activity rate surpassing 28%, achieving a relatively high level of user engagement.

For a commercial company, the most critical capability remains its ability to achieve commercial monetization.

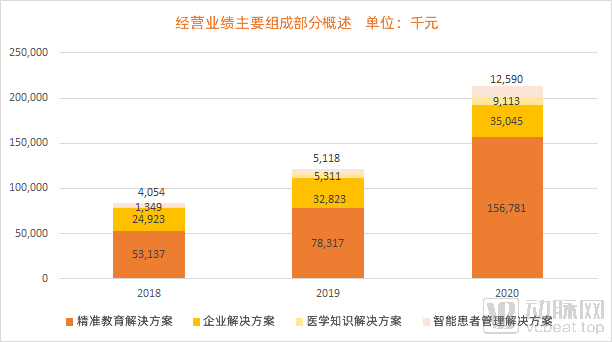

Medlive has three major business segments in its commercialization efforts:

Precision Education and Enterprise Service Solutions, among the precision education and enterprise service solutions, precision education includes digital marketing consulting, digital content creation, and digital distribution; enterprise solutions include digital market research, EDC, RWS support, and patient recruitment.

Medical Knowledge Solutions, including professional medical information covering continuing medical education and clinical decision support.

Intelligent Patient Management Solutions, including internet hospitals and chronic disease management services for specific conditions.

Pharmaceutical companies have always been the largest payers for Medlive, with data from Medlive’s prospectus showing that its top five customers are all pharmaceutical companies.

In terms of monetization, according to data from Medlive’s prospectus, Medlive ranked first among digital healthcare marketing service providers on physician platforms in China in 2020, with a market share of 21.4%.

Medlive’s operating revenues from 2018 to 2020 were RMB 83.5 million, RMB 121.6 million, and RMB 213.5 million, respectively, with a compound annual growth rate (CAGR) of 59.9% during this period. The company achieved rapid growth in 2020, primarily driven by a doubling of revenue from its Precision Education solutions. In 2019, revenue from Precision Education amounted to RMB 78 million, accounting for 64.4% of total revenue; in 2020, it rose to RMB 157 million, representing 73.4% of total revenue.

In 2020, the rapid revenue growth of precision education was significantly impacted by the COVID-19 pandemic. During the outbreak, which began in late 2019, physical distancing measures severed the offline connections established between pharmaceutical sales representatives and physicians, rendering traditional marketing methods virtually inoperable. In contrast, digital pharmaceutical marketing based on online platforms remained largely unaffected, enabling pharmaceutical companies to maintain continuous communication with physicians through these digital channels.

In the pharmaceutical industry’s digital marketing sector, there has never been a shortage of market participants, and this niche is home to many specialized producers of medical knowledge. Medlive’s ability to achieve the highest market share in this space is inseparable from its major shareholder, Japan’s M3.

After its launch in 2006, Medlive operated solely on self-generated funds, with annual revenue remaining at the tens of millions of yuan level. M3’s strategic equity investment not only provided capital to Medlive but, more importantly, brought clients and advanced solutions in the realm of digital marketing for pharmaceutical companies.

M3 is a Japanese company primarily engaged in operating medical information websites, with its scale and revenue firmly ranking first in the industry. The name M3 stands for Medicine, Media, and Metamorphosis. M3’s overarching mission is to transform the pharmaceutical and healthcare sector by leveraging media and internet technologies.

Medlive, with the support of its major shareholder M3, has achieved significant improvements in customer acquisition and technological advancement.

Among professional physician platforms in China, only a few possess the delivery capabilities required by pharmaceutical and medical device companies—namely, the ability to conduct targeted marketing through multiple digital channels based on criteria such as specialty, credentials, and geographic location. With M3’s backing, Medlive can be said to have gained a “dimensionality-reduction strike” advantage in the early stages of this market.

Leveraging M3’s brand recognition in the Japanese market, Medlive quickly established business relationships with numerous multinational pharmaceutical and medical device companies operating in China during its early stages. On the technology front, by harnessing M3’s technological capabilities, Medlive launched eMessenger in 2014, one of the earlier precision-targeting applications for physicians in China.

Tian Lixin, founder of Medlive, stated: “M3 can provide us with certain assistance; for instance, in the realm of e-marketing, they possess outstanding capabilities in research, consulting, and planning. In Japan, the majority of physicians are loyal users of M3, and globally, M3 is also a leader.”

Currently, digital marketing is transitioning toward intelligence, with artificial intelligence and big data gradually permeating the pharmaceutical digital marketing industry chain. Medlive has also made strategic arrangements in this area, increasing its investments in artificial intelligence, big data, knowledge graphs, and natural language processing to strengthen its technological advantages.

Looking ahead, in addition to consolidating its existing competitive advantage in digital marketing to further increase market share, Medlive is also striving to unlock greater value from its extensive physician resources. In 2021, Medlive launched an internet hospital, aiming to leverage its vast network of physicians to integrate internet hospital services with other service offerings—such as chronic disease management services—thereby providing patients with intelligent management solutions.

However, after several years of development, the landscape of the internet healthcare industry has largely stabilized. Since 2020, public hospitals have also begun to vigorously build their own internet hospitals. Medlive entered this space in 2021 and thus did not enjoy a first-mover advantage. Although Medlive possesses extensive physician resources, DXY, which also started as a physician community, launched its internet healthcare services earlier and adopted a model focused on providing in-depth services to doctors, thereby capturing a significant share of user mindshare. Consequently, Medlive faces considerable pressure in seeking breakthroughs within the internet hospital sector.

Tian Lixin, the founder of Medlive, was among the first entrepreneurs in the digital health sector and is a seasoned veteran in the field. Nevertheless, the challenges he faces are far from simple. Looking ahead, achieving broader physician coverage—particularly breaking into the vast primary care market—remains a significant hurdle for Medlive. Meanwhile, the efficacy of digital marketing has long been subject to skepticism, and enhancing industry recognition is another critical issue on Medlive’s path to future growth. Whether Medlive can replicate the success of WebMD Health still faces numerous challenges.

Reference: Medlive: Dedicated to Serving Physicians – Heima.com