Billion-Patient Vein Intervention Market: Import-Dominated, Immune to Volume-Based Procurement, Emerging as a Hot Investment Sector

On the morning of March 25, the Beijing-Tianjin-Hebei “3+N” Alliance announced the results of its volume-based linked procurement for coronary dilation balloon medical consumables. Following this centralized procurement, the average price of coronary dilation balloons in the alliance regions dropped from RMB 3,401 to RMB 319, representing a 90% average price reduction for identical products from the same manufacturers compared with 2020 levels. Prior to this, multiple provinces and municipalities (alliances) had already completed centralized procurement negotiations for coronary balloons.

With the national volume-based procurement (VBP) of coronary stents largely settled, regional VBP for coronary balloons is advancing vigorously. The normalization of VBP for high-value medical consumables has become a new industry norm. The widespread implementation of centralized procurement is driving comprehensive transformation in the high-value consumables sector, making innovative segments with high product barriers and immunity to VBP a focal point of industrial attention. Within the broader field of vascular intervention, peripheral intervention has emerged as a hot area of interest, driven by its large patient population and rapidly growing market.

The rapidly emerging peripheral intervention sector comprises two major domains: peripheral venous and peripheral arterial interventions. Currently, the peripheral venous intervention market is smaller than the peripheral arterial intervention market; however, from a future development perspective,There are over 100 million patients with venous diseases in China, accounting for approximately 60% of vascular surgery cases. The volume of interventional procedures is experiencing rapid growth, and the future market for peripheral venous interventions is projected to surpass that of peripheral arterial interventions.

Today’s venous market resembles the coronary stent market of two decades ago. The market is expanding rapidly, a trend recognized by the industry, with multiple companies beginning to establish a presence in the field of venous interventions. VCBeat (WeChat ID: vcbeat) believes that although the peripheral venous intervention sector is currently nearly untapped and presents high R&D barriers, the emergence of specialized R&D teams will likely give rise to several publicly listed companies in this field in the future.

For most people, peripheral venous intervention may be an unfamiliar term; however, venous diseases are actually very common. Varicose veins, deep vein thrombosis, and iliac vein compression syndrome are all high-incidence conditions in our daily lives.

Venous diseases are categorized into two types: chronic venous insufficiency and venous thromboembolism. Chronic venous insufficiency primarily includes venous valvular insufficiency, varicose veins, and post-thrombotic syndrome. Venous thromboembolism mainly comprises deep vein thrombosis (DVT) and pulmonary embolism (PE), with PE predominantly caused by DVT.

Venous diseases account for half of all vascular surgery cases. Clinically, venous diseases constitute approximately 60% of vascular surgery cases, frequently occur in the lower extremities, and have an incidence rate roughly six times that of arterial diseases. In terms of patient population alone, China has 11 million patients with coronary heart disease, 13 million with stroke, and 8.9 million with heart failure, while the number of patients with venous diseases exceeds 100 million. The prevalence of peripheral venous diseases is several times higher than that of other conditions.

In venous diseases with a patient base reaching the hundred-million level,Deep vein thrombosis, iliac vein compression syndrome, and varicose veins are the three major diseases with the most concentrated medical device R&D efforts and the highest level of industry attention.

Deep Vein ThrombosisDeep vein thrombosis (DVT) refers to the coagulation of blood in the deep veins, forming thrombi that impede corresponding venous return. When a thrombus dislodges, it can travel with the bloodstream into the pulmonary arteries, causing pulmonary embolism. Acute pulmonary embolism is frequently misdiagnosed or missed, with a mortality rate of 20% to 30%. The number of DVT cases in China increased from 1.1 million in 2015 to 1.5 million in 2019, representing a compound annual growth rate (CAGR) of 8.3%, and is projected to reach 3.3 million by 2030 (data sourced from Frost & Sullivan). Venous thromboembolism has become the third largest cardiovascular disease, following heart disease and stroke.

Another major disease of concern isIliac Vein Compression SyndromeIliac vein compression syndrome (IVCS) refers to a syndrome in which the iliac vein is compressed by the iliac artery crossing over its anterior aspect, leading to pathological changes such as intraluminal adhesions, luminal stenosis, or occlusion. These alterations impede iliac venous blood flow, resulting in a series of clinical symptoms. In 2019, the number of IVCS cases in China was 700,000, and it is projected to reach 2 million by 2030, representing a compound annual growth rate (CAGR) of 10.1% from 2019 to 2030. (Data source: Frost & Sullivan)

The most common venous diseases areVaricose Veins, in 2019, the number of people with varicose veins in China reached 399.4 million, accounting for 28.5% of the total population, and is expected to reach 477.6 million by 2030. (Data from Frost & Sullivan)

Historically, the treatment penetration rate for peripheral venous disease was low due to its relatively low mortality. However, peripheral venous interventions in China are now entering a phase of rapid growth.

The penetration rate of peripheral artery disease-related procedures in the United States is 5.4%, whereas in China it is only 0.2%. The penetration rate in the venous sector is even lower than that in the peripheral arterial sector. The entire venous intervention market is characterized by rapid development but severely inadequate penetration. It is currently in a phase of rapid growth and volume expansion.

An industry insider stated that in the past, many patients with venous diseases were excluded from treatment due to limited hospital admission capacity and constrained physician resources in the field of venous intervention. Currently, the state places significant emphasis on strengthening vascular surgery services at the primary care level. Tier-1 and Tier-2 hospitals across China are establishing vascular surgery departments, where venous therapy will become a core business line. Clinically, deep vein thrombosis (DVT) is the leading cause of pulmonary thromboembolism (PTE), which has a case fatality rate as high as 25%–30%. The establishment of Venous Thromboembolism (VTE) Prevention and Control Management Centers at various levels marks the fourth major national disease prevention and control initiative, following Pain Centers, Chest Pain Centers, and Stroke Centers. With the widespread setup and development of vascular surgery departments in hospitals nationwide, the volume of venous interventional procedures in China is rapidly increasing, and its market potential is expected to be no less than that of coronary interventions.

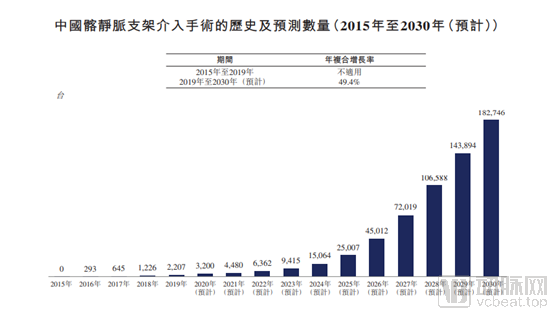

Taking iliac vein stenting as an example, the number of iliac vein stent interventions in China increased from 293 procedures in 2016 to 2,207 in 2019, and is projected to further rise to 182,746 by 2030, representing a compound annual growth rate (CAGR) of 49.4% from 2019 to 2030.

Data source: Frost & Sullivan

Driven by the rapid growth of venous interventional procedures, the entire peripheral vascular market is also expected to expand. According to research by Grand View Research, Inc., the global market for peripheral vascular medical devices was estimated to reach USD 8.92 billion in 2020, with a compound annual growth rate (CAGR) of 7.2% from 2014 to 2020. The United States remains the largest market globally. Due to the rise of emerging markets such as China and India, the Asia-Pacific peripheral vascular medical device market is projected to grow at a CAGR of 10.0%. In 2020, the size of China’s peripheral vascular medical device market was estimated to reach RMB 7 billion.

In the nearly untapped domestic market, where existing products are still almost monopolized by imports, this undoubtedly leaves significant room for domestically produced alternatives to emerge.

In addition to the significant potential for import substitution, the second major opportunity for domestically produced medical devices lies in the limited variety of products currently available in the entire venous intervention market.

VCBeat (WeChat ID: vcbeat) has compiled an overview of the current product pipeline development status for the three major diseases in the field of venous intervention: deep vein thrombosis, iliac vein compression syndrome, and varicose veins.

Deep Vein Thrombosis:

The primary minimally invasive interventional product for deep vein thrombosis is the inferior vena cava filter, which is inserted into large veins to capture large thrombus fragments and prevent them from traveling through the vena cava to the heart and lungs. Vena cava filters reduce the risk of associated mortality. Currently, inferior vena cava filters from seven companies—Cook, Cordis, BD, Volcano Corporation, Rex Medical, Weixin Medical, and Lifetech Scientific—have been approved for market launch in China.

Although there are numerous marketed inferior vena cava (IVC) filter products, there have been no significant technological breakthroughs in the filters themselves in recent years. Consequently, clinical issues such as inaccurate positioning, filter tilt, and difficult retrieval remain prevalent. In terms of product portfolios, the IVC filters from MicroPort Endovascular MedTech (Huitai Medical) and the retrievable IVC filters from Genesis MedTech have both entered the clinical trial stage.

Domestic Candidate Products for Inferior Vena Cava Filters

Iliac Vein Compression Syndrome:

Minimally invasive interventional products for iliac vein compression syndrome primarily consist of iliac vein stents. The function of an iliac vein stent is to expand the compressed iliac vein back to its original diameter and maintain smooth venous blood flow upon implantation. In China, only Cook Medical’s Zilver Vena self-expanding venous stent received regulatory approval in 2016; to date, no domestically produced products have been approved. The price of an iliac vein stent is as high as RMB 28,000.

Currently, four iliac vein stent candidates in China have entered the clinical trial phase, with one developed by a multinational corporation and the other three by domestic companies. It is reported that the Tianhong Shengjie iliac vein stent project has completed clinical enrollment of 256 cases.

Domestic Candidate Products for Iliac Vein Stents

Varicose Veins:

In the interventional treatment of varicose veins, ablation therapy is an emerging technique that has garnered significant attention. This approach utilizes heat generated by laser, microwave, or radiofrequency energy to damage and ultimately occlude the target veins. Currently, all peripheral ablation products marketed in China are supplied by multinational corporations, including Medtronic’s ClosureFast and Closure RFS systems, as well as F Care Systems NV’s EVRF endovenous radiofrequency ablation system. Regarding research and development pipelines, peripheral radiofrequency ablation systems and catheter products from three domestic companies—Prior Medical (Xianruida), JetMed (Guichuang Tongqiao), and Hengrui Medicine—have entered clinical stages.

List of Domestic Varicose Vein Ablation Candidate Products

An analysis of marketed and pipeline products for the three major venous conditions—deep vein thrombosis, iliac vein compression, and varicose veins—reveals two key characteristics of the venous intervention market. First, in terms of product offerings, the current market lacks the diversity and specialization seen in other segments of vascular intervention, leaving substantial room for product improvement. In clinical practice, physicians are even forced to use peripheral arterial devices off-label to treat venous diseases. Second, although the high-potential venous intervention market has attracted considerable attention from many companies, few have established comprehensive strategies centered specifically on venous diseases.

Why Are There Fewer Companies in the Venous Disease Sector Compared to Other Areas of Vascular Intervention? Relatively High R&D Barriers Are a Major Reason.

Wang Yonggang, Chairman of Tianhong Shengjie, told VCBeat: “Taking the development of iliac vein stents as an example, it is commonly believed that because venous walls are thinner than arterial walls, iliac vein stents do not require high radial force. However, the left common iliac vein is anatomically positioned between the lumbosacral spine posteriorly and the right common iliac artery anteriorly. When the iliac vein is subjected to anterior-posterior compression by these surrounding structures, the venous wall experiences repetitive compressive stress, thereby necessitating stents with higher radial strength.”

In terms of product design, there are few mature products in the field of venous intervention, so direct copying is not feasible; product development and design must start on an equal footing with international companies.

Wang Yonggang stated, “The design of iliac vein stents should minimize the impact on contralateral blood flow; sufficient radial force must be ensured at the iliac ostium, while adequate flexibility must be maintained given that the iliac vein runs closely along the pelvis. We believe these are key clinical pain points that require focused attention in the design of iliac vein stents, an approach that is largely consistent with that of major international medical device companies.”

Product development in the field of venous intervention tests not only a company’s ability to develop individual products, but also its depth of clinical understanding, capability for coordinated product development, and clinical execution strength. This requires companies to have access to abundant clinical expert resources and to engage in deep collaboration with them. China’s high-value consumables industry is transitioning from imitation to innovation; merely mimicking individual products is no longer sufficient to establish a competitive advantage in an increasingly fierce market.

In the field of venous disease, Wang Yonggang believes that the ultimate differentiator will be comprehensive strength across multiple dimensions, including innovation capability, depth of clinical understanding, R&D capability, and execution ability.

This is also why Tianhong Shengjie does not focus solely on a single product, but positions itself as a one-stop comprehensive product platform in the field of intravenous therapy.

Wang Yonggang stated, “We structure our product portfolio based on clinical needs. Venous diseases can be broadly categorized into four types: venous obstruction, stenosis, thrombosis, and reflux. While many companies are developing inferior vena cava filters for the prevention of pulmonary embolism (PE), Tianhong Shengjie has chosen to prioritize the development of iliac vein stents, as the company believes that vessel recanalization is the most critical aspect of clinical treatment. Indeed, addressing vessel recanalization is the most urgent priority in clinical practice.

In terms of overall product design, Tianhong Shengjie’s strategy focuses on developing products for the three major venous diseases—obstruction, reflux, and thrombosis—to meet the needs of lumen preparation, venous implantation, interventional therapy, and integrated prevention and treatment. The therapeutic coverage spans from the iliofemoral deep veins to the peripheral veins, vena cava, and pulmonary arteries. In the future, leveraging its expertise in venous products, the company will gradually expand into arterial therapy products, aiming to develop into a comprehensive platform for the treatment of vascular diseases.

Currently, Tianhong Shengjie has obtained four NMPA product registration certificates. The company’s registration plan for the next three years includes a series of products such as the iliac vein stent system, vena cava filter, thrombectomy catheter, thrombolysis catheter, high-pressure balloon, and thrombus aspiration catheter.

Although China’s venous intervention sector started relatively late, the country now boasts a well-developed medical device industry chain and a concentrated pool of R&D talent. Domestic manufacturers are deeply addressing clinical pain points in their R&D strategies, aligning closely with international counterparts. The future of domestically produced solutions in the field of venous intervention looks promising.