Disposable Endoscopy Trend Emerges in China, Offering Domestic Manufacturers a Strategic Opportunity to Leapfrog Global Competitors

This article firstPublished by: DAS Capital, Author: Jiefan She,Authorized for republication by VCBeat.

Preface

With the advancement of minimally invasive surgery and early diagnosis and treatment of cancer, the application of endoscopes in diagnosis and therapy continues to expand.

In 2020, the market size of endoscopes in China reached RMB 25.4 billion. Due to the technological monopoly held by imported endoscope manufacturers, the market share of domestically produced enterprises was less than 10%.

Are there opportunities for latecomers to overtake industry leaders in the endoscopy field, similar to those seen in the new energy vehicle sector? What development trends has technological progress brought to the medical endoscopy industry?

1. China’s Medical Endoscope Market Exceeds RMB 25 Billion, with Imported Brands Still Maintaining a Monopolistic Position

Endoscopes enter the human body through natural orifices or small surgical incisions. During use, the endoscope is introduced into the organ to be examined, allowing direct visualization of changes in the relevant areas. They are essential tools for precise diagnostic examinations and minimally invasive treatments in both internal medicine and surgery. Based on product structure and form, endoscopes can be classified into flexible and rigid endoscopes. According to the department of use and clinical scenarios, they are further subdivided into laparoscopes, thoracoscopes, arthroscopes, gastroscopes, colonoscopes, and flexible ureteroscopes, among others.

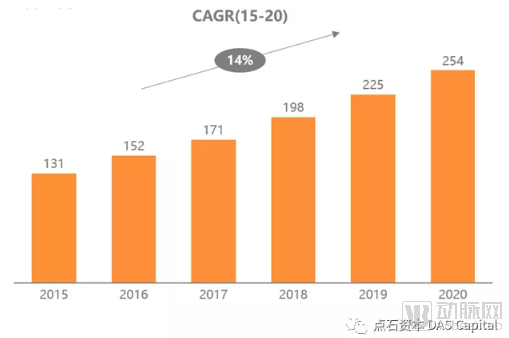

According to Frost & Sullivan data, the size of China’s endoscopy market reached RMB 25.4 billion in 2020, with a compound annual growth rate (CAGR) of approximately 14.2% from 2015 to 2020. During the same period, the global endoscopy market grew from USD 16.4 billion to USD 21.5 billion, at a CAGR of 5.5%. The Chinese market has been expanding much faster than the global average, and its share of the global market continues to rise. The underlying reason is that endoscopy systems combine characteristics of both medical equipment and consumables: the main console units are durable and not easily damaged, while the lifespan of endoscope inserts ranges from six months to ten years. Developed countries in Europe and the United States have already completed their initial deployment of endoscopy systems; absent significant technological breakthroughs, substantial market growth is unlikely.

Figure: Market Size of Endoscopes in China (RMB 100 million, based on ex-factory prices)

Meanwhile, China’s endoscopy market is far from saturated. As early cancer screening and minimally invasive therapies gain wider adoption, Chinese hospitals continue to increase their procurement of endoscopes—essential tools for diagnosis and treatment—driven by promotional efforts from foreign enterprises. Furthermore, demand is growing rapidly for gastroscopy and colonoscopy in early cancer screening, as well as for laparoscopic and natural orifice transluminal endoscopic surgery (NOTES), which help alleviate patient suffering and improve prognoses. This growth is fueled by China’s accelerating population aging and rising consumption levels.

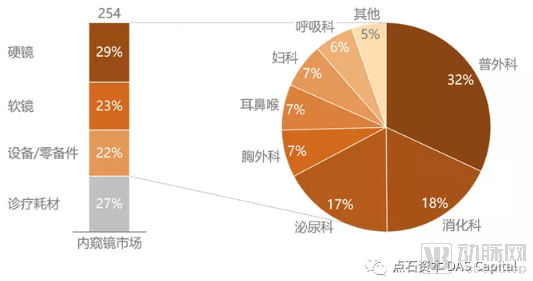

The Chinese endoscopy market, segmented by product type, includes not only rigid and flexible endoscopes but also corresponding equipment, spare parts, and procedure-specific consumables. Excluding the impact of surgical consumables and further segmented by clinical department, general surgery accounts for the largest share of the endoscopy market, corresponding to laparoscopes, choledochoscopes, and other such devices. Gastroenterology and urology follow in proportion, corresponding to gastroscopes, colonoscopes, duodenoscopes, ureteroscopes, percutaneous nephroscopes, cystoscopes, and other endoscope types.

Figure: Segmentation of China's Endoscopy Market in 2020 (RMB 100 million, based on ex-factory prices)

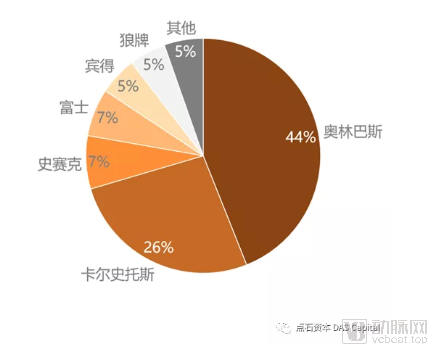

In terms of the competitive landscape, China’s endoscopy market is monopolized by Japanese and German manufacturers, with domestic companies holding a market share of approximately 5%. As the development of image sensors for traditional flexible endoscopes has been driven by Japanese enterprises, which maintain high technical barriers, Japanese companies such as Olympus, Fujifilm, and Pentax have essentially monopolized the flexible endoscope market. Meanwhile, the German company Karl Storz was the first to master rod lens technology for rigid endoscopes, allowing German manufacturers to maintain their leading position in this sector. Major Chinese manufacturers of flexible and rigid endoscopes, such as Sonoscape Medical, Aohua Endoscopy, and Mindray Medical, are unable to compete directly with imported brands in the high-end market. Their current primary focus is on hospitals below the tertiary level (i.e., secondary hospitals and below). Even in hospitals where their products have been adopted, these domestic endoscopes are rarely used as the primary equipment, as local companies continue to rapidly catch up with their international counterparts.

Figure: Competitive Landscape of the Endoscopy Market in China

2. The generational upgrade of imaging components has made the “consumabilization” of endoscopes possible

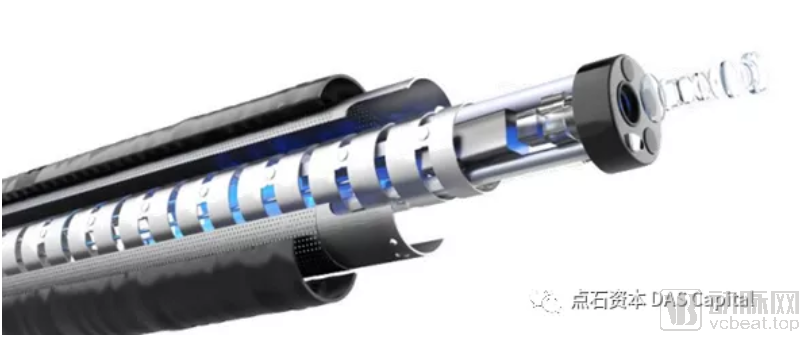

Domestic manufacturers have been slow to break through and overtake competitors in the endoscopy field, with high technical barriers being the direct cause of low domestic market penetration. The research, development, and manufacturing of endoscopes involve multidisciplinary and multi-sector collaboration. Flexible endoscopes, such as gastroscopes and ureteroscopes, comprise numerous components, feature highly complex supply chains, and entail intricate manufacturing steps that cannot be fully automated. Japanese endoscope manufacturers, represented by Olympus, have always treated production processes as top-secret proprietary knowledge and restrict the production of core products to Japan.

Figure: Schematic Diagram of the Structure of a Flexible Endoscope

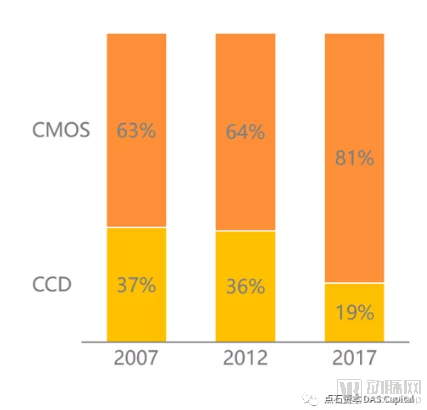

Regarding image sensors, endoscopes utilize two primary technologies: CCD (Charge-Coupled Device) and CMOS (Complementary Metal-Oxide-Semiconductor). Due to their superior image quality, CCDs were widely adopted during the early stages of electronic endoscope development. However, as CMOS technology has advanced in color performance, the gap in image quality between CMOS and CCD has narrowed significantly. Meanwhile, manufacturers have come to appreciate CMOS for its low power consumption, low noise, and suitability for high-volume, low-cost production. Consequently, leading endoscope manufacturers are gradually transitioning from CCD to CMOS image sensors.

Figure: Global Image Sensor Shipment Structure

During the CCD era, CCD sensors constituted the most significant cost component of electronic endoscopes, accounting for approximately 40% of the total cost. Due to the design principles of CCDs, signal output was susceptible to interference from individual pixels, leading to higher defect rates, increased manufacturing complexity, and elevated costs. At the peak of CCD technology, only six companies were capable of mass production: Sony, Fujifilm, Kodak, Philips, Panasonic, and Sharp. Among these, four were Japanese enterprises. Sony, the market leader with a share exceeding 50%, was a shareholder in Olympus, resulting in a close strategic alliance between the two. Furthermore, other CCD manufacturers imposed significant restrictions on exports to overseas endoscope manufacturers.

Due to the high cost of CCDs, endoscopes with long service lives and robust durability have become the preferred choice for both manufacturers and hospitals. The conflict between the pursuit of ultimate maneuverability in flexible endoscopes and the performance degradation after repeated use has significantly increased their manufacturing costs. In addition to CCDs, the requirements for other precision core components have also risen sharply. Suppliers of these components are concentrated in Japan and Germany, and China has not yet established a complete industrial chain, resulting in weak competitiveness for domestically produced endoscopes.

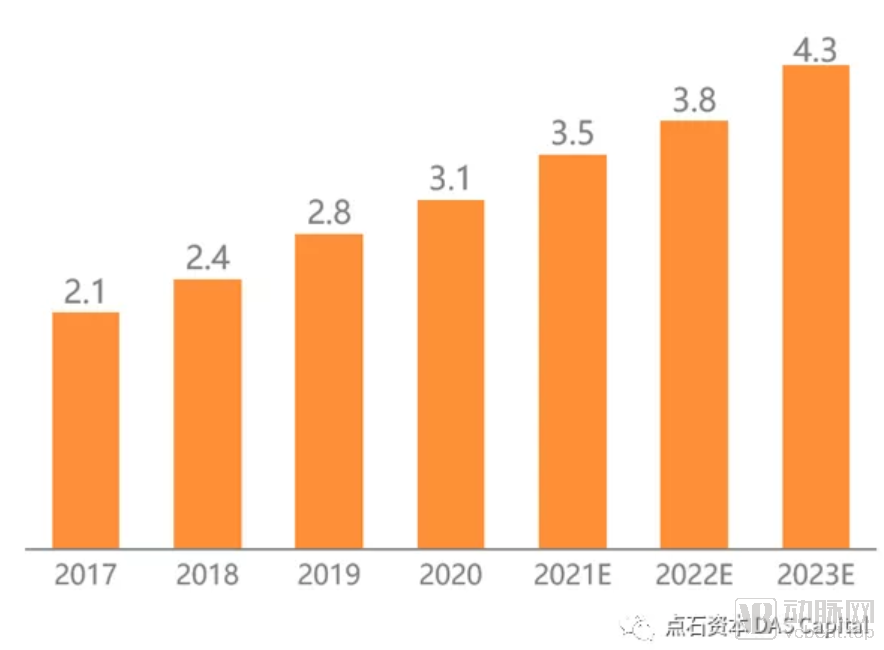

Figure: Global Shipments of Medical-Grade CMOS

The introduction of new CMOS technology has, to some extent, reduced enterprises’ reliance on CCD sensors. For instance, in 2015, Sonoscape Medical developed the HD-500, China’s first high-definition electronic endoscopy system based on a 2-megapixel CMOS sensor. More encouragingly, due to the more fragmented CMOS market, relatively lower technical barriers, and suitability for large-scale mass production, CMOS prices have shown a trend of declining by an order of magnitude, thereby making disposable endoscopes feasible.

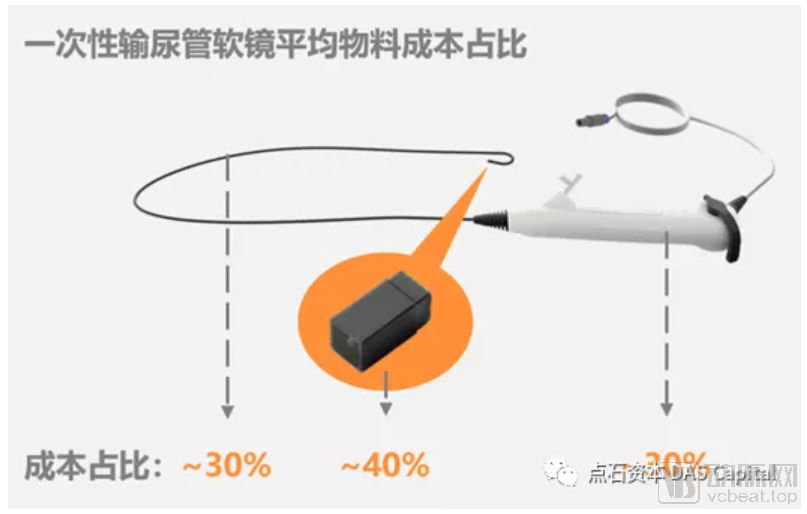

When the designed service life of an endoscope is reduced from hundreds or thousands of uses to a single use, eliminating the need for reparability, its cost structure undergoes dramatic changes. The overall design philosophy shifts from that of a precision mechanical device to that of a standard disposable medical catheter, accompanied by significant changes in material selection, with plastics replacing metals and a substantial reduction in the number of components. Traditional endoscope manufacturers have yet to fully respond to the disruption caused by single-use endoscopes, while emerging players such as Boston Scientific and Denmark’s Ambu, leveraging their experience in producing millions of medical consumables annually, have entered the spotlight. Meanwhile, Chinese manufacturers are rapidly catching up and have secured a place in the international market.

Figure: Illustration of the Average Cost of Disposable Flexible Endoscopes

3. Disposable endoscopes address the issues of cross-infection, time inefficiency, and insufficient infrastructure investment in primary healthcare facilities

Endoscopes are medical devices that come into direct contact with patients' skin, mucous membranes, and sterile tissues. However, the structure of endoscopes contains multiple small, long open channels, which provide an environment for the retention of microorganisms, secretions, and blood, as well as for cross-contamination. Consequently, cross-infection has become a difficult-to-avoid risk in medical accidents. Relevant academic studies indicate that endoscopes rank first among medical devices in terms of cross-infection risk. More than 70% of endoscopes suffer from inadequate cleaning, and nearly three-quarters of commonly used endoscopes are contaminated with bacteria.

In China, reports of substandard disinfection efficacy and failed biological monitoring for gastroscopes are common, while many more healthcare-associated infections (HAIs) go unreported due to delayed detection. During the recent COVID-19 pandemic, endoscopy units in multiple hospitals were suspended alongside dental and otorhinolaryngology departments, underscoring hospital administrators’ concerns about the risk of HAIs in endoscopy settings.

Figure: ECRI’s Top 10 Health Technology Hazards

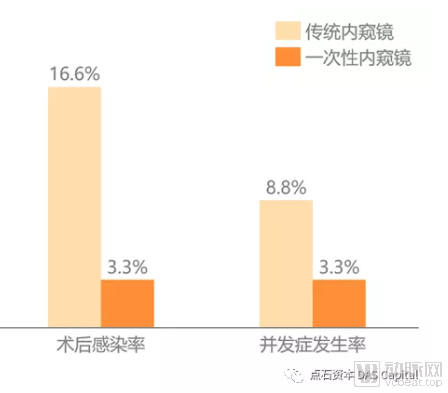

A study published in January 2021 showed that, when comparing reusable and single-use flexible ureteroscopes, the single-use endoscope group had shorter hospital stays and antibiotic treatment durations, as well as lower overall complication rates and postoperative infection rates. Among the 90 patients who used single-use endoscopes, none developed uremia or had positive blood cultures, whereas three cases were positive in the control group. This strongly demonstrates that the use of single-use ureteroscopes significantly reduces postoperative complications and infection rates.

Figure: Disposable Endoscopes Reduce Postoperative Infection Rates After Flexible Ureteroscopy

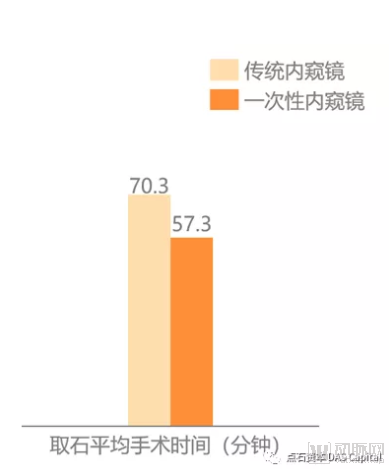

Moreover, under the heavy workload in Chinese hospitals, repeated reprocessing of multiple endoscopes can lead to performance degradation or even damage. In contrast, using single-use endoscopes ensures that each device is in optimal condition upon unpacking, thereby improving surgical efficiency to some extent.

Figure: Disposable endoscopes reduce operative time for flexible ureteroscopy

Meanwhile, natural orifice endoscopic diagnostic and therapeutic procedures are highly suitable for widespread adoption in county-level and other primary healthcare institutions, as they impose lower demands on anesthesia and surgical expertise compared to open surgery. In developed countries, a significant proportion of endoscopic examinations and surgeries are performed in outpatient settings or specialized endoscopy centers. In contrast, inadequate infrastructure investment has constrained the development of endoscopic diagnosis and treatment in primary healthcare facilities in China.

Taking flexible ureteroscopic lithotripsy as an example, if a hospital intends to introduce this procedure, it would need to purchase two imported flexible ureteroscopes and one processor unit, with a procurement cost of approximately RMB 2 million. In contrast, by opting for single-use endoscopes, the hospital would only need to acquire several domestically produced single-use flexible ureteroscopes and one processor unit, keeping the procurement cost under RMB 100,000. Single-use endoscopes are highly conducive to promoting endoscopic surgeries in primary care hospitals.

4. Market Outlook for Disposable Endoscopes: Focusing on 70 Million Minimally Invasive and Non-Invasive Procedures

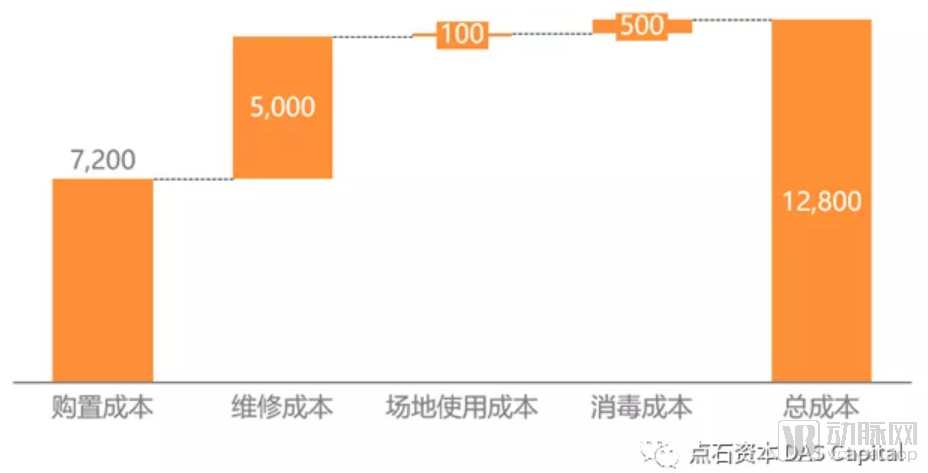

After years of exploration by foreign-funded and domestic enterprises, single-use endoscopes have proven more cost-effective than reusable endoscopes in multiple application areas. For instance, in traditional flexible ureteroscopy, considering the lifespan and maintenance frequency of reusable scopes, the cost per procedure exceeds RMB 12,000, whereas the hospital procurement price for single-use flexible ureteroscopes in China is generally below RMB 10,000. Additionally, this allows hospitals to better control costs associated with endoscopic procedures.

Figure: Average Cost per Procedure for Reusable Flexible Ureteroscopes (CNY)

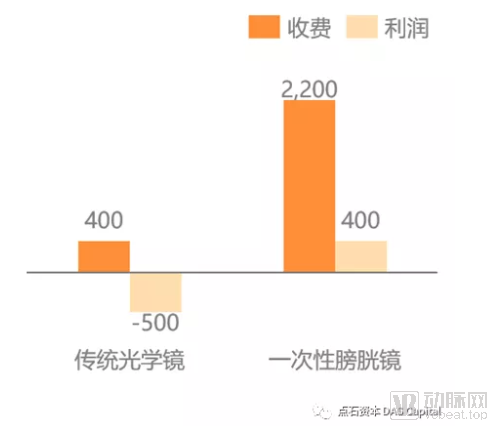

Similarly, for cystoscopy, imported flexible electronic cystoscopes remain poorly adopted in China due to their prohibitive costs, with rigid optical cystoscopes still dominating the market. Disposable semi-rigid electronic cystoscopes, featuring a smaller diameter and hydrophilic coating, offer improved patient experience. Meanwhile, departments have seen enhanced profitability per procedure, thanks to the higher reimbursement rates associated with electronic endoscopy.

Figure: Example Comparison of Fees and Profits Between Traditional Optical Cystoscopes and Disposable Cystoscopes (CNY)

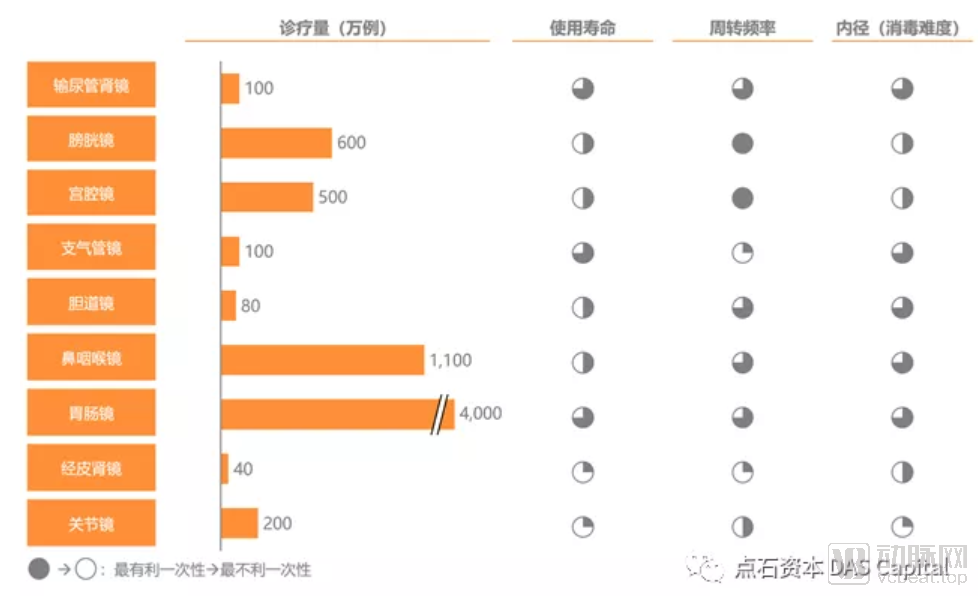

Considering factors such as service life, turnover frequency, and sterilization difficulty, endoscopes that entail high procurement, maintenance, and sterilization costs, have short single-use durations, and require rapid turnover all possess the potential to become “disposable consumables.” These types of endoscopes correspond to a potential diagnostic and treatment volume of nearly 70 million cases in China, creating a blue-ocean market for domestic manufacturers of single-use endoscopes.

Figure: Market Opportunity Estimation for Disposable Endoscopes

5. Leading Manufacturers of Disposable Endoscopes in China and Internationally

Boston Scientific (USA)

As a giant in the high-value medical device industry, Boston Scientific’s deployment of single-use endoscopes began with urological and gastrointestinal endoscopy, which are most closely related to its core business. The company launched LithoVue, the world’s first single-use ureteroscope, and has since expanded its product portfolio to include the EXALT Duodenoscope, bronchoscopes, gastroscopes, and the SpyGlass cholangioscope. Its premium market positioning, coupled with favorable reimbursement rates in the United States, has resulted in generally high prices for Boston Scientific’s single-use endoscopy products.

Ambu (Denmark)

Ambu is dedicated to the development, production, and sales of diagnostic and life support equipment required by hospitals and emergency services. In 2009, Ambu launched aScope, the world’s first single-use bronchoscope, becoming the undisputed leader in the field of single-use bronchoscopes. Starting with bronchoscopes, Ambu has gradually completed its full industrial layout for single-use endoscopes. In the most recent fiscal year, the company’s sales of single-use endoscopes exceeded one million units.

Figure: The History of Ambu Disposable Endoscopes

As of now, four companies in China have obtained a total of five NMPA registration certificates for single-use endoscopes, all of which were issued in 2020.

Pusheng Medical

Pusheng Medical, established in Zhuhai in 2014, obtained the registration certificate for its single-use flexible ureteroscope in June 2020. The company had previously secured CE and FDA certifications and commenced overseas sales. Its future product pipeline will also include single-use nasopharyngolaryngoscopes, single-use bronchoscopes, and single-use cystoscopes.

Ruipai Medical

Established in 2015 at Guangzhou International Bio Island, Raypee Medical is a global provider of comprehensive solutions for single-use minimally invasive surgical procedures, with its product development roadmap covering urology, gynecology, otolaryngology, gastroenterology, pulmonology, and general surgery. In 2020, Raypee Medical obtained registration certificates for its single-use flexible ureteroscope and single-use electronic cystoscope, making it the company with the largest number of Class III medical device registration certificates in the field of single-use endoscopes.

Innovex

Innovex, founded in Shanghai in 2009, primarily focuses on the research and development and sales of high-value consumables related to digestive endoscopy and urology. In 2014, it established its subsidiary, Anqing Medical, which specializes in medical endoscopes. The company aims to create a closed-loop system between endoscopic equipment and consumables, providing comprehensive solutions for minimally invasive surgeries. In 2020, Anqing Medical received approval for its single-use flexible ureteroscope, which has already been marketed overseas.

Happiness Factory

Anhui Xingfu Gongchang Medical Equipment Co., Ltd. was established in 2017. Building upon the introduction of patented technologies from Silicon Valley, USA, and through subsequent digestion, absorption, and improvement, the company has developed an internationally leading R&D platform for single-use electronic endoscopes. It is primarily engaged in the research, development, and manufacturing of single-use flexible electronic ureteroscopes and flexible cystoscopes. In January 2020, the company obtained China’s first registration certificate for a single-use flexible ureteroscope.

In 2020, endoscopy giant Olympus secured the 21st spot on the Global Top 100 Medical Device Companies list for another year, generating $5.89 billion in revenue from a single product line alone. Behind these enviable revenue and profit figures lies the Japanese giant’s monopoly over the traditional endoscopy sector. Leveraging China’s vast blue-ocean market, Chinese entrepreneurs in the disposable endoscopy space have encountered their best opportunity to overtake competitors on the curve. Let us await with anticipation as domestic innovations overcome myriad challenges to become global leaders in disposable endoscopy, thereby benefiting patients worldwide.