How MicroPort Sustains a Near RMB 100 Billion Valuation Despite a $200M Loss Amid National Volume-Based Procurement

In the second half of 2020, the entire cardiovascular intervention market was shaken by the volume-based procurement of coronary stents. In 2021, the sword of centralized procurement will turn to orthopedics.

On April 1, the Joint Procurement Office for High-Value Medical Consumables Organized by the State issued the “Notice on Carrying Out Information Collection for Certain Orthopedic High-Value Medical Consumable Products.” The document states that, building upon the previously collected procurement data from medical institutions, and to further understand the market conditions for orthopedic high-value medical consumables, information collection for these products will be carried out in phases.Initiate the first batch of product information collection for high-value medical consumables, including artificial hip and knee joints.

How Devastating Is the Impact of Centralized Procurement? In 2020, Lepu Medical and Sinomed’s stock prices plummeted in the high-value cardiovascular consumables sector subjected to centralized procurement, and they have yet to recover. The orthopedics sector felt the chill of centralized procurement even earlier, experiencing across-the-board declines with a market capitalization loss exceeding RMB 10 billion.

Against the backdrop of the severe impact of centralized procurement on the high-value medical consumables industry, MicroPort, as a domestic leader in this sector, has two core businesses: cardiovascular interventional devices and orthopedic devices. Coupled with the impact of the COVID-19 pandemic on overseas markets, both of MicroPort’s major cash cows—cardiovascular interventional and orthopedic segments—were inevitably affected. In 2020, MicroPort reported its first annual loss in five years, with financial statements showing a deficit exceeding USD 200 million (approximately RMB 1.3 billion).

However, from 2020 to the present, MicroPort's stock price has risen from HK$10 to HK$49, an increase of nearly fivefold. As of April 7, 2021, its market capitalization had climbed to HK$89 billion, approaching the HK$100 billion mark.Furthermore, over the past two years, MicroPort has successfully spun off its subsidiaries, MicroPort Endovastec and MicroPort CardioFlow, for separate listings. Meanwhile, MicroPort MedBot and MicroPort EP are sequentially launching their initial public offerings (IPOs), with plans to list on the STAR Market.

While volume-based procurement (VBP) has driven down valuations for most high-value medical consumables companies, MicroPort Scientific Corporation offers a new case study on analyzing the industry impact of VBP. Amid the unstoppable trend of VBP for high-value consumables, how did MicroPort stage a comeback and chase after a RMB 100 billion market capitalization despite performance pressures? VCBeat (WeChat ID: vcbeat) provides a detailed interpretation of MicroPort’s 2020 financial report.

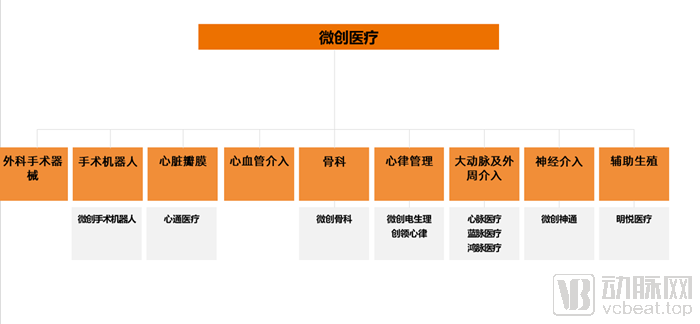

MicroPort Medical was founded in the field of coronary intervention and has since expanded its business segments to include cardiovascular intervention, orthopedic medical devices, cardiac rhythm management, aortic and peripheral intervention products, neurointervention, heart valves, surgical robots, surgical medical devices, and assisted reproduction. Its business scope covers high-growth sub-sectors of high-value consumables.

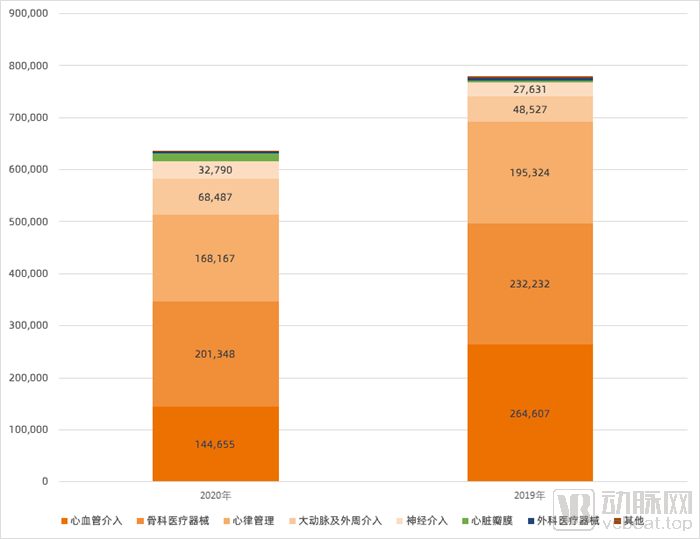

In 2020, MicroPort Medical generated USD 648.7 million (approximately RMB 4.25 billion) in revenue, with 22.3% derived from its cardiovascular interventional products business, 31.1% from orthopedic medical devices, 27.8% from cardiac rhythm management, 10.6% from aortic and peripheral vascular interventional products, 5.1% from neurointerventional products, 2.3% from heart valve business, and 0.7% from surgical medical devices. As both domestic and international markets were impacted by the pandemic to varying degrees,Total revenue decreased by 18.2% year-on-year. The net loss for the full year amounted to $223 million.

Regarding the reasons for the loss, the announcement indicated that the change was mainly attributable to: 1) a decline in revenue due to the impact of the COVID-19 pandemic and China’s centralized volume-based procurement policy for coronary stents; 2) increased investment in ongoing and newly initiated R&D projects; 3) the grant of incentive shares to certain employees, including an executive director, under the share award scheme during the reporting period; and 4) the absence of one-time investment income from the partial disposal of equity in MicroPort EP (Shanghai) Co., Ltd. recorded in the same period of the previous year.

Changes in MicroPort's Revenue from 2019 to 2020

Note: Only revenue from medical device sales is calculated; after-sales service and rental income are excluded.

In MicroPort’s revenue structure, the three major businesses that each accounted for more than 20% in 2020 were cardiovascular interventional products, orthopedic medical devices, and cardiac rhythm management.The cardiovascular interventional business maintains a leading position in China, while the orthopedics and cardiac rhythm management businesses derive their primary revenue from overseas.

Cardiovascular Intervention Business

MicroPort Medical started its business with coronary stents, and this sector remains its core business today. However, in 2020, MicroPort’s cardiovascular intervention segment experienced a setback in growth, causing it to fall from the company’s largest business unit to the second-largest.

In 2020, MicroPort’s cardiovascular interventional product business generated revenue of US$140 million, representing a 44.6% year-on-year decline. ComparisonIn terms of the cardiovascular interventional business in 2019, its share of total revenue dropped from 34% in 2019 to 23%, with revenue falling from USD 260 million in 2019 to USD 140 million in 2020.

In terms of gross profit margin, MicroPort’s gross margin was 71.1% in 2019 and declined to 67.2% in 2020. In addition to the cost increases caused by the pandemic, a major contributing factor was the price subsidy adjustment accrued for stent products that had been sold to channels but not yet implanted, based on the 2021 implementation prices under the pressure of centralized procurement.

MicroPort’s cardiovascular interventional revenue declined, primarily due to the impact of the COVID-19 pandemic and channel inventory price subsidies resulting from the national volume-based procurement (VBP) program. Amid fierce competition in China’s national VBP, MicroPort won bids for two products: the Firebird2® Cobalt-Chromium Coronary Rapamycin-Eluting Stent System and the Firekingfisher® Cobalt-Chromium Coronary Rapamycin-Eluting Stent System.MicroPort is the only domestic company with two selected products, and the total intended procurement volume of its selected products ranks first among all companies.

Even though MicroPort had sufficient advantages in the volume-based procurement program, its cardiovascular interventional business declined by 44%, which amply demonstrates the disruptive impact of volume-based procurement.

How Can MicroPort’s Cardiovascular Interventional Business Break Through Amid the Impact of Volume-Based Procurement?

Based on the current product portfolio, MicroPort Medical has four drug-eluting stents and four balloon products on the market for its cardiovascular interventional business. MicroPort Medical aims to broadly meet the differentiated PCI needs in the market through diverse product combinations.

MicroPort's Key Products in the Cardiovascular Intervention Field

In the field of vascular intervention, in addition to the two pillars of stents and balloons, MicroPort has also deployed a series of cutting-edge products.Products likely to be launched in the coming years include bioresorbable scaffolds, rotational atherectomy catheters, intravascular lithotripsy balloons, drug-coated balloons, and intra-aortic balloon pump (IABP) counterpulsation systems.Financial report data shows that the Firesorb® bioresorbable sirolimus-targeted eluting coronary stent system (“Huo Guan”) has initiated the Phase III Future-III clinical trial and completed enrollment of the first patient.

Meanwhile, MicroPort is also attempting to expand its business scope by partnering with renowned overseas medical companies to jointly develop domestically produced medical angiography X-ray machines, thereby shifting its focus from therapeutic products to vascular interventional diagnostic products.

Orthopedic Medical Devices

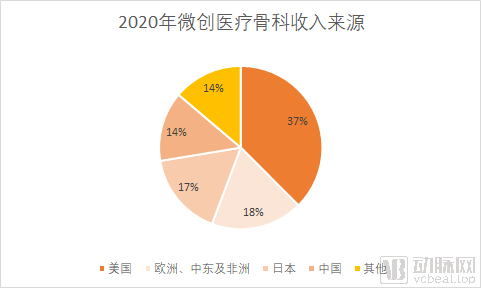

Next, let’s examine MicroPort’s second-largest business segment: orthopedic medical devices.MicroPort’s orthopedics business originated from the $290 million acquisition of Wright Medical’s joint reconstruction division in 2014. Today, MicroPort’s orthopedics portfolio encompasses joint reconstruction, spine and trauma care, as well as other specialized implants and instrumentation products.In 2020, MicroPort’s global orthopedics business generated $201 million in revenue, a year-on-year decrease of 13.7%.

The year-on-year decline in orthopedics revenue was primarily driven by pandemic-related sales impacts in overseas markets. In the Chinese market, MicroPort’s orthopedics business achieved growth. Revenue from MicroPort’s orthopedics operations in China amounted to USD 29.9 million, representing a 10.1% year-on-year increase.

The growth in MicroPort’s domestic orthopedics business was driven by a 93.3% surge in revenue from its joint reconstruction segment. In 2020, MicroPort aggressively promoted the SuperPATH® minimally invasive hip replacement technique, which enables rapid patient recovery. In the spine sector, MicroPort’s spine division maintained robust growth, with five products receiving regulatory approval in 2020.

Within the overall revenue structure, the proportion of income from orthopedic medical devices rose to 32%, making it MicroPort’s largest business segment. Although volume-based procurement has also been introduced in the orthopedics sector,However, the majority of MicroPort’s orthopedic business revenue is derived from overseas markets. In 2020, revenue from China accounted for 14%, and the overseas market helps MicroPort’s orthopedic segment better mitigate the risks associated with centralized procurement.

Cardiac Rhythm Management Business

One of MicroPort's major business segments, accounting for over 20% of its revenue, is cardiac rhythm management.Cardiac rhythm management primarily encompasses products for the diagnosis, treatment, and management of arrhythmias and heart failure, mainly including pacemakers, defibrillators, and cardiac resynchronization therapy (CRT) devices. MicroPort’s cardiac rhythm management business originated from the acquisition of LivaNova’s CRM division in 2017 for HK$1.5 billion. At the time of the acquisition, LivaNova’s CRM business had already achieved revenues of US$249 million in 2016. In 2020, MicroPort’s cardiac rhythm management business generated only US$180 million in revenue, representing a year-on-year decline of 16.2% due to the global pandemic. Of this, overseas revenue amounted to US$172 million, while revenue from its China operations was US$8.1 million. MicroPort’s domestic cardiac rhythm management business in the Chinese market is operated by Shanghai Chuangling.

For MicroPort, the greatest value of acquiring LivaNova’s CRM business lies in gaining access to CRM technology and entering the global CRM market, which is valued at tens of billions of U.S. dollars. In China, the cardiac rhythm management market is predominantly monopolized by imported brands, with Medtronic firmly holding over 50% of the market share, followed closely by other overseas giants such as Abbott (formerly St. Jude Medical), Boston Scientific, and Biotronik.MicroPort acquired the full product portfolio of CRM and has primarily entered the pacemaker market. In 2020, MicroPort ranked first in the Chinese domestically produced pacemaker market, with sales revenue from domestically produced pacemakers increasing by 24.7% year-on-year.

In terms of the R&D layout for cardiac rhythm management products, MicroPort’s pipeline in the clinical development stage includes the Axone™ pacing lead, the MRI-compatible Vega™ lead, the ARC-enabled 2D Navigo™ left ventricular lead for cardiac resynchronization therapy, and the Invicta™ defibrillation lead.

In the significant heart failure market within rhythm management, MicroPort is also collaborating with French companies on remote monitoring applications to collect data, leveraging data intelligence to improve care for heart failure patients and ultimately achieve the goal of predicting cardiac decompensation events.

Cardiovascular intervention, orthopedic devices, and cardiac rhythm management collectively contribute over 80% of MicroPort’s revenue. Businesses such as aortic and peripheral interventions, heart valves, neurointerventional devices, and surgical medical devices account for less than 20% in total; however, this does not diminish their strategic importance. Although these segments currently generate limited revenue, their future growth potential is comparable to that of cardiovascular intervention.

Whether in neurointervention, heart valve procedures, or peripheral intervention,The markets covered by MicroPort’s businesses are all characterized by rapid growth but severely inadequate penetration.In MicroPort’s 2020 annual report, despite the impact of the pandemic, its aortic and peripheral vascular interventional products business, neurointerventional products business, and heart valve business all achieved rapid growth, with year-on-year increases of 40.9%, 17.5%, and 383.4%, respectively.

Heart Valve

In the Fastest-Growing Field of Heart ValvesIn 2020, MicroPort's heart valve business generated $15.2 million in revenue. MicroPort's VitaFlow transcatheter aortic valve and delivery system was approved in 2019 and achieved nearly RMB 100 million in sales revenue in 2020.

Year-on-year, VenusA-Valve, launched by Venus Medtech in 2017, generated RMB 272 million in revenue in 2020 (+17.2%). Venus Medtech expects to complete approximately 2,200 TAVR procedures for the full year.

As can be seen, within the TAVR sector, Venus Medtech currently holds a significant market share by virtue of its first-mover advantage. However, MicroPort’s subsidiary, VitaFlow Medical, is rapidly catching up with considerable momentum. Financial report data show that by the end of 2020, VitaFlow Medical had covered 144 hospitals across 28 provinces and municipalities in China. Among the top 20 hospitals performing transapical aortic valve replacement, VitaFlow had entered 18. It has achieved a leading market share in certain key hospitals and secured the number one market position in several provinces.

Beyond the aortic valve segment, VitaFlow Medical has established a multi-pipeline product portfolio, including five transcatheter mitral valve products under development, aiming to penetrate the larger market for mitral regurgitation.

Intervention in the Aorta and Peripheral Vessels

In the field of aortic and peripheral vascular interventions, MicroPort generated USD 68.5 million in revenue, representing a year-on-year increase of 40.9%. The growth of MicroPort Endovastec was primarily driven by its Castor® single-branched thoracic aortic stent graft.

In the field of peripheral intervention, MicroPort’s Reewarm® PTX drug-coated balloon dilation catheter was launched in China in 2020, and the first clinical implantation of its venous stent system was also completed.

Neurointervention

In the neurointerventional field, MicroPort generated $32.9 million in revenue in 2020. Neurointervention was the hottest sector for medical device investment in the primary market in 2020, underscoring the intense competition. MicroPort aims to establish a comprehensive stroke solution portfolio by offering a diversified range of products.

In the neurointerventional sector, MicroPort’s core product is the Tubridge® flow diverter stent. Flow diverter stents are primarily used for the treatment of aneurysms; they function by redirecting blood flow, preventing it from entering the aneurysm sac after implantation. This leads to gradual thrombosis within the aneurysm, ultimately resulting in its resolution. The sustained and rapid growth of the Tubridge® flow diverter stent has driven the expansion of MicroPort’s neurointerventional business.

In the neurointerventional field, Peijia Medical, Genesis MedTech, and HeartCare Medical—all competitors in the same sector as MicroPort—have either listed on the STAR Market or initiated their IPO processes, signaling that competition in this segment will intensify in the future.

MicroPort has invested in Rapid Medical as part of its product portfolio strategy in neurointervention. Rapid Medical’s Tigertriever® thrombectomy stent has been admitted to the green channel for approval of innovative medical devices. The thrombectomy stent is poised to become a key product in MicroPort’s neurointerventional pipeline.

Beyond their high growth, another notable feature of MicroPort’s heart valve, neurointerventional, and aortic and peripheral intervention businesses is that these niche sectors have served as the breeding ground for MicroPort to spin off listed companies.In the field of heart valves, VitaFlow Medical has been listed on the Hong Kong Stock Exchange; in the field of aortic and peripheral vascular interventions, MicroPort Endovascular has been listed on the STAR Market. In these high-growth sectors, MicroPort Medical established several new subsidiaries or secured financing for existing ones in 2020, laying the groundwork for future IPOs.

In 2020, MicroPort Scientific Corporation and its affiliated companies cumulatively secured approximately USD 1 billion in external financing. This included approximately RMB 3 billion for the surgical robotics business, approximately USD 130 million for the heart valve business, approximately USD 75 million for the cardiac rhythm management business, approximately RMB 580 million for the orthopedic medical device business, approximately RMB 300 million for the electrophysiology business, and approximately RMB 90 million for the assisted reproductive technology business.In March 2021, MicroPort Scientific Corporation announced that MicroPort Vision had received a capital injection of RMB 385 million, increasing MicroPort’s stake to over 85%. This move may signal MicroPort’s further expansion into the ophthalmology sector.In the peripheral vascular sector, MicroPort increased its capital injection into its subsidiary, Shanghai Lanmai Medical Technology Co., Ltd., during the reporting period, and newly established a wholly-owned subsidiary, Shanghai Hongmai Medical Technology Co., Ltd.

Chang Zhaohua, Chairman of MicroPort, once stated that, in addition to manufacturing medical products, MicroPort is also a company that produces listed companies.Through this business model, the company has achieved sustained growth. Evidently, under MicroPort Scientific’s strategy of “incubating listed companies,” many of its financing activities are aimed at preparing for the future spin-off listings of its subsidiaries.

MicroPort’s Core Business Segments and Major Subsidiaries

Although MicroPort has maintained high growth across many of its business segments, the medical device market differs significantly from the pharmaceutical market.Medical device products have limited per-unit market space; many such products have been on the market for only a short time, and market cultivation requires a certain period. In the short term, due to relatively high product prices,The market is difficult to scale up quickly. To support a hundred-billion-yuan market capitalization in the future, MicroPort needs to continuously expand its product line. In addition, with the normalization of China’s volume-based procurement policy, the profit margins of mature products are being constantly compressed. Only through diversified product line layout can risks be mitigated.

In 2020, MicroPort made significant inroads into new territories it had not previously entered. Among its strategic bets on the future, MicroPort first made substantial strides into the high-barrier sector of surgical robotics, leveraging its robust clinical resources to rapidly advance the industrialization of its products.

In the field of surgical robots, MicroPort has covered five major tracks upon entry: laparoscopic, orthopedic, vascular interventional, natural orifice, and percutaneous interventional surgical robots. Within just one year, MicroPort has achieved numerous breakthroughs in the surgical robot sector.

In January 2020, MicroPort® Toumai® Laparoscopic Surgical Robot completed the enrollment for all registration clinical trials, becoming the first domestically produced laparoscopic surgical robot to complete patient enrollment in multi-center registration clinical trials in the field of urology. In June 2020, the Honghu® Skywalker™ Orthopedic Surgery Navigation and Positioning System completed the enrollment of the first case in its First-in-Man (FIM) clinical trial. In addition, MicroPort’s self-developed Dragonfly Eye DFVision® 3D Electronic Laparoscope and Medical Endoscope Cold Light Source were successfully exempted from clinical trials, and registration applications have been submitted.

In the course of developing its orthopedics and cardiac rhythm management businesses, MicroPort Medical has pursued a dual-pronged strategy combining overseas investment with independent research and development—a approach that has also been replicated in its surgical robotics business.

In 2020, MicroPort Medical invested in the French vascular interventional robotics company Robocath, the Singaporean percutaneous puncture robotics company NDR, and the Singaporean transprostatic puncture robotics company Biobot, thereby entering the fields of vascular interventional robotics and percutaneous interventional robotics. Among these, the vascular interventional robot has already initiated type testing in China.

In 2020, MicroPort’s assisted reproductive technology (ART) business also secured financing. Its ART subsidiary, Mingyue, obtained RMB 130 million in strategic funding. Established in November 2018, Mingyue specializes in medical technology solutions for the ART field, with its services covering all stages of the ART cycle, including oocyte and sperm retrieval, cryopreservation and storage of gametes and embryos, culture and handling of gametes and embryos, and embryo transfer.

In the public’s traditional perception, MicroPort was seen as the leader in China’s stent market, but this label clearly no longer captures the full scope of its current business. Today, MicroPort’s business structure resembles that of a global giant in high-value medical consumables, which also explains why its stock price has continued to rise even after its cardiovascular interventional business was impacted by centralized volume-based procurement.

A Perspective on MicroPort Scientific: 2020 was a year of rapid expansion for MicroPort, characterized by continuous business diversification, sustained financing rounds, and successive listings of its subsidiaries. Like a snowball gaining momentum and size, MicroPort moved ever closer to a market valuation of RMB 100 billion. However, as this momentum accelerated, the company faced greater tests of its underlying R&D capabilities and clinical execution. In 2020, MicroPort’s R&D expenditure reached USD 190 million (approximately RMB 1.2 billion), representing a 27.2% year-on-year increase and accounting for more than 20% of its sales revenue.

Although MicroPort spares no expense in R&D, it operates in a crowded field. Against the backdrop of capital markets opening a “fast track” for healthcare technology companies, going public is not the endgame. Ensuring this fleet sails far and steady remains a formidable challenge for MicroPort.