The Future of Innovative Therapies: Chinese Enterprises Step Into the Spotlight with New IPO Filing

WuXi AppTec

New Drug R&D and Production Service Provider

Pharmaron

Life Science R&D Service Provider

Lonza

Pharmaceutical R&D Developer

This article firstPublished in: Long Talks Value, Author: Long Talks Pharma,Authorized for republication by VCBeat.

Today, we briefly discuss the development opportunities brought to China's CDMO industry by the rapid growth in the field of cell and gene therapy. We believe that the future of the cell and gene therapy CDMO sector may well replicate the success achieved by WuXi Biologics in the biologics CDMO space.

01

Cell and Gene Therapy Industry

Cell therapy involves the infusion or implantation of normal or bioengineered human cells into patients to replace cells that have lost their normal function, while gene therapy refers to the introduction of normal genes into human cells to modify abnormal gene sequences.

The concepts of cell and gene therapy have existed for decades, but the true acceleration toward commercial realization has occurred only since 2017. This shift is driven by the gradual refinement of overseas regulatory frameworks on one hand, and technological breakthroughs enabling product commercialization on the other. We believe that cell and gene therapies will play an increasingly important role in the future of precision medicine. Unfortunately, however, there are very few companies in China with genuine R&D capabilities in cell and gene therapy; many of the firms hyped between 2015 and 2017 were primarily engaged in concept-driven speculation.

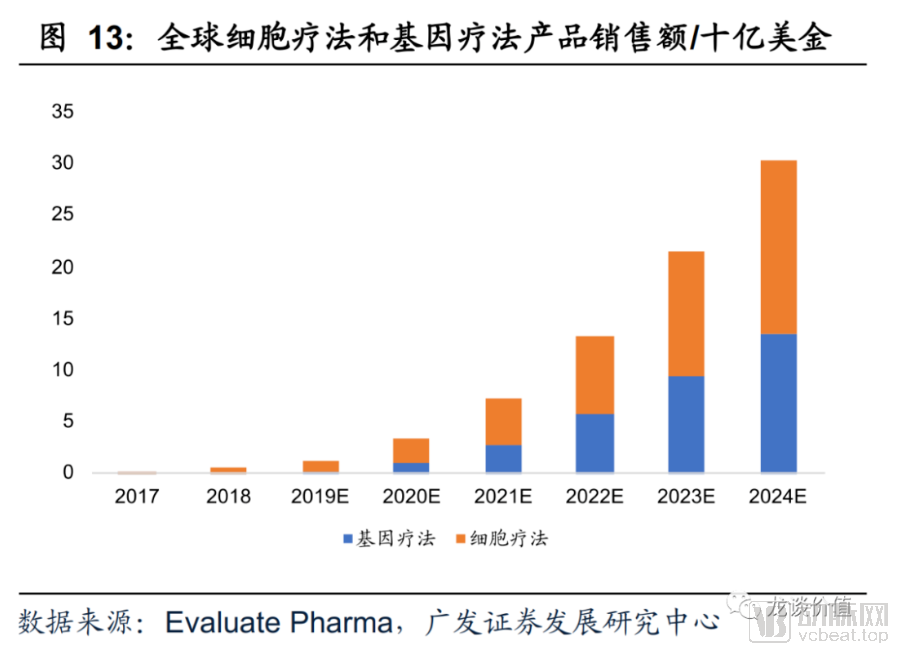

According to the “Pharma R&D Annual Review 2020” published by Pharmaprojects, the global pipeline of gene therapy investigational projects was projected to reach nearly 1,300 in 2020, representing a year-on-year increase of approximately 50%; the pipeline of cell therapy investigational projects approached 500 in 2020, marking a nearly 80% increase compared with 2019.

A large number of cell and gene therapy investigational projects are increasingly entering clinical stages. It is projected that over 1,000 cell and gene therapy programs will enter clinical trials in 2020, with more than 8,000 cell therapy and over 3,000 gene therapy clinical pipelines expected by 2026. This represents a tenfold expansion of the industry within five years. Multiple consulting firms predict that the global market size for cell and gene therapies will rapidly grow to reach the $30 billion level in the coming years.

Currently, the pharmaceutical giants with significant portfolios in cell and gene therapies are primarily Novartis, Gilead Sciences, and Celgene. These companies have rapidly entered the field through high-priced acquisitions of biotech firms, such as Novartis’s acquisition of Avexis, Gilead Sciences’ acquisition of Kite Pharma, and Celgene’s acquisition of Juno Therapeutics. These three companies are also the leading large pharmaceutical enterprises with the highest production capacities for cell and gene therapies at present.

In addition to biotech companies engaged in the research and development of cell and gene therapies, there is another promising area of focus: the cell and gene therapy CDMO sector. As an industry that fully leverages the engineer dividend and China’s comparative manufacturing advantages, the CDMO sector has begun to demonstrate its competitiveness in both large-molecule biologics and small-molecule drugs. Companies such as WuXi Biologics, STA Pharmaceuticals, and Asymchem are showcasing their growing global competitiveness after years of accumulation. In the future, Chinese leading enterprises may also secure a significant position in the cell and gene therapy CDMO landscape.

02

Cell and Gene Therapy CDMO

The primary reasons for the higher barriers and greater outsourcing rates in the biologics CDMO sector, compared to small-molecule drugs, are the higher costs associated with building biologics manufacturing capacity and the more stringent requirements for technical platforms. These factors result in higher capital expenditure and technological barriers for biologics CDMO companies.

Shanghai Pharmaceuticals plans to invest RMB 8 billion to build 120,000 liters of biopharmaceutical production capacity. In contrast, WuXi Biologics’ planned capacity (including acquisitions) has already exceeded 300,000 liters and is expected to come online around 2023–2024, implying capital expenditures nearing RMB 20 billion. Few other companies can replicate WuXi Biologics’ capabilities; only the two WuXi-affiliated listed companies (which have collectively raised over RMB 50 billion in equity financing since 2017) and a select few others, such as Tigermed, possess comparable influence and fundraising capacity in the capital markets. However, Tigermed has not yet made significant investments in the CDMO sector.

Moreover, the manufacturing processes for cell and gene therapies are more complex. The market adoption of cell therapies in recent years has actually fallen somewhat short of expectations, including the two cell therapy products approved after Gilead Sciences acquired Kite Pharma, as well as one product from Novartis (all three products are CD19-targeted CAR-T cell therapies).

This situation arises primarily because cell therapy, as a personalized treatment modality, incurs prohibitively high production costs, with manufacturing processes representing a key industry bottleneck. The combination of substantial R&D investment and elevated production costs also drives pricing to very high levels. According to a report by Frost & Sullivan, R&D expenditures for cell and gene therapies are generally far higher than those for traditional drugs, with discovery and preclinical R&D costs estimated at USD 900–1.1 billion and clinical-stage expenditures at USD 800–1.2 billion.

However, just as monoclonal antibody titers were relatively low in the past, biopharmaceutical manufacturing processes have been continuously improved in recent years, leading to significant advancements in monoclonal antibody expression levels. We believe that manufacturing processes for cell and gene therapies will also mature in the future.

Of course, this does not change the reality that its technical barriers are far higher than those of biologics. We believe that the CDMO outsourcing rate for cell and gene therapies will be even higher than that for biologics CDMOs in the future, and the industry concentration driven by these technical barriers is also expected to exceed that of the biologics CDMO sector.

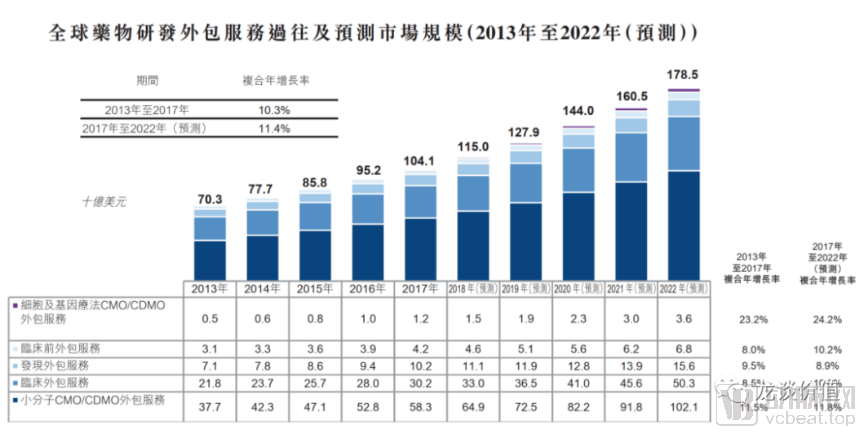

According to the prospectus for WuXi AppTec’s Hong Kong listing, the global market size for CRO/CDMO outsourcing services in cell and gene therapy is projected to reach $3 billion in 2021, with a compound annual growth rate (CAGR) of 20%–30%, significantly outpacing the overall growth rate of the global CRO/CDMO industry. Domestic manufacturers, including WuXi AppTec, Pharmaron, and Porton Pharma Solutions, are actively developing their technological platforms, suggesting that this sector may become the next key focus for Chinese CDMO companies.

03

Industry Companies

(1) Lonza

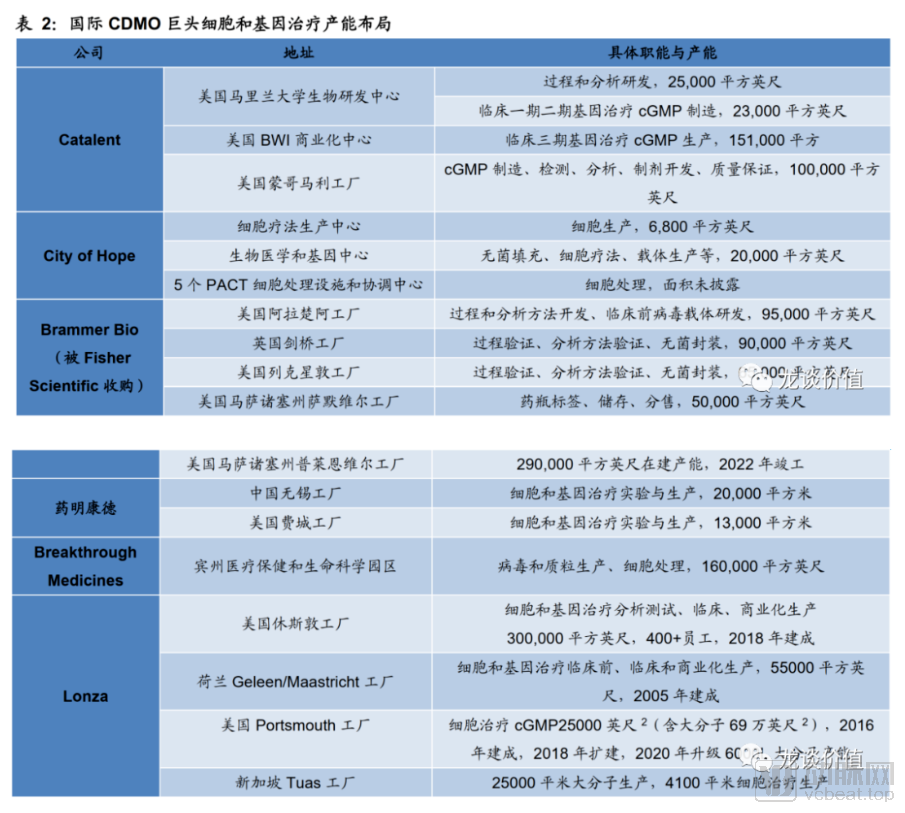

Lonza, founded in 1897 and headquartered in Switzerland, is the world’s leading CDMO. Its CMO/CDMO portfolio spans small-molecule active pharmaceutical ingredients (APIs) and intermediates, small-molecule CDMO services, large-molecule CDMO services, CDMO for novel modalities such as antibody-drug conjugates (ADCs) and cytotoxins, as well as cell and gene therapy CDMO services.

In terms of performance across these business segments, the small-molecule active pharmaceutical ingredient (API) and intermediate business has been gradually declining. This is primarily due to the gradual shift of this sector toward emerging market countries, with India and China capturing a significant share of the market. Companies such as WuXi AppTec, Asymchem, Pharmaron, Porton Pharma Solutions, Jiuzhou Pharmaceutical, and Apeloa Pharmaceutical are all on the rise. Nevertheless, the small-molecule CDMO business continues to perform well, driven mainly by the company’s innovative business model and its strategic layout in the field of emerging small-molecule drugs. Dosage forms and drug delivery systems also represent areas of competitive advantage for the company.

The large-molecule biopharmaceutical CDMO sector is in a phase of rapid growth. The key players in this field include Lonza, WuXi Biologics, Samsung Biologics, and Boehringer Ingelheim (BI). Lonza, WuXi Biologics, and Samsung Biologics each have valuations of approximately RMB 300 billion, which are relatively comparable. However, we project that WuXi Biologics will grow at a rate significantly higher than that of Lonza, ultimately becoming the global leader in the biopharmaceutical CDMO industry.

Emerging product sectors, such as antibody-drug conjugates (ADCs) and cytotoxins, have entered an acceleration phase. When I began researching ADC drugs in 2019, there were only five or six approved ADCs globally, one of which was subsequently withdrawn. In the past two years, ADC research has gradually reached a harvest stage, reminiscent of the trajectory seen with immune checkpoint inhibitors two to three years ago. Correspondingly, demand for contract development and manufacturing organization (CDMO) services has grown rapidly. In China, WuXi AppTec and WuXi Biologics are collaborating in this field: WuXi AppTec is responsible for the cytotoxin component, while WuXi Biologics handles the monoclonal antibody portion, with the final antibody-drug conjugate assembled in WuXi Biologics’ facilities. Domestic manufacturers are expected to remain competitive in this sector.

The current market size of the cell and gene therapy sector remains relatively small, and the industry’s CXO segment is still in its early stages of development; however, it is experiencing very high growth rates. Lonza ranks first globally in CDMO capacity for cell and gene therapies.

Lonza’s 2019 revenue was CHF 5.92 billion (equivalent to RMB 41.44 billion at an exchange rate of 1 CHF to 7 RMB), approximately 3.2 times that of WuXi AppTec. However, its revenue growth rate was only 6.8%, significantly lower than WuXi AppTec’s 34%. In 2019, Lonza’s net profit amounted to CHF 763 million, representing a year-on-year increase of 15.8%, with a net profit margin of 12.89%. Core EBITDA (excluding restructuring, acquisitions, and divestitures) reached CHF 1.62 billion, a year-on-year increase of 7.2%, while the Core EBITDA margin rose steadily from around 20% in 2013 to approximately 27% in 2019. Based on this, we can reasonably conclude that it is entirely feasible for companies such as WuXi AppTec, Asymchem, WuXi Biologics, and Samsung Biologics to maintain core net profit margins in the range of 25%–30% in the future.

Lonza is also trending towards building production capacity in the Chinese market. Although over 80% of Lonza’s business comes from European and American markets, the rise of innovative pharmaceutical companies in China has made the Chinese market an indispensable segment. Consequently, Lonza has begun to establish production capabilities in locations such as Nansha and Guangzhou.

(2) WuXi AppTec

WuXi AppTec’s cell and gene therapy CDMO capacity is second only to Lonza, and WuXi AppTec is further expanding its capacity through additional acquisitions and facility expansions. At the time of WuXi AppTec’s initial public offering on the A-share market, it was already recognized as the second-largest global player in cell and gene therapy CDMO; however, this significance was not fully appreciated back in 2018.

WuXi AppTec initially expanded by acquiring the U.S.-based AppTec, which had a 25-year history in cell bank development. Since 2015, it has significantly expanded its production capacity, focusing primarily on CAR-T cell therapies for oncology, as well as research on adeno-associated virus (AAV) vectors and plasmid vectors. Currently, it maintains a 20,000-square-meter production facility in Philadelphia, USA.

WuXi AppTec operates a 13,000-square-meter R&D and GMP manufacturing facility for cell and gene therapy products in Wuxi, Jiangsu; a 4,800-square-meter viral vector CDMO platform in Zhoupu, Shanghai; and a 600-square-meter process development department in Waigaoqiao, Shanghai.

In early March 2021, the Company announced the completion of its acquisition of OXGENE, a UK-based gene therapy technology company. OXGENE has become a wholly-owned subsidiary of WuXi Advanced Therapies, the Company’s cell and gene therapy CDMO platform, and serves as WuXi Advanced Therapies’ first R&D and production base in Europe. OXGENE’s proprietary next-generation technology platform addresses the complexities associated with viral vector production for cell and gene therapies. This acquisition will further enhance the capabilities of the cell and gene therapy R&D and manufacturing platform, helping WuXi AppTec improve production efficiency and reduce costs for cell and gene therapy products.

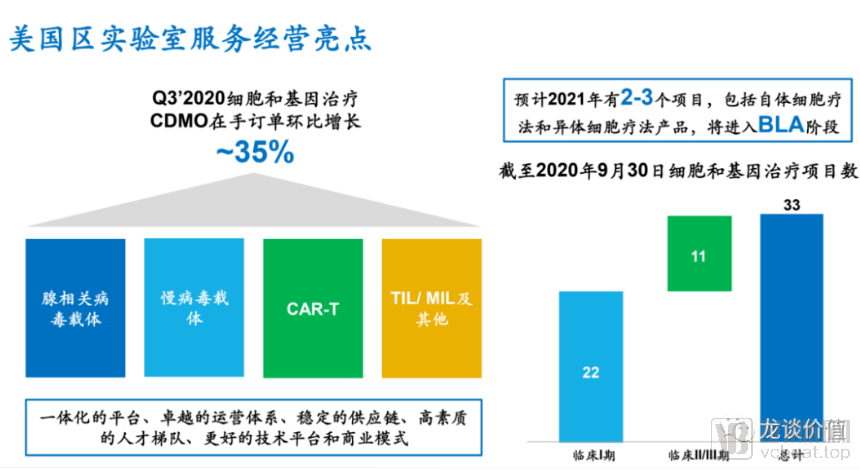

As of the end of the third quarter of 2020, WuXi AppTec had 33 cell and gene therapy CDMO projects in clinical stages, including 11 in Phase II/III clinical trials and 22 in Phase I clinical trials. The company expects that 2–3 projects will enter the BLA stage in 2021, signaling that the cell and gene therapy CDMO sector is on the verge of a commercialization boom.

In the future, WuXi AppTec may well surpass Lonza to become the global leader in the cell and gene therapy sector. This is why I believe that both companies within the WuXi ecosystem are exceptionally strong, with no clear superiority of one over the other. As everyone now recognizes the bright prospects of biologic CDMOs, it is possible that in 5–10 years, cell and gene therapy CDMOs will occupy the same prominent position that biologic CDMOs hold today.

(3) Pharmaron

Pharmaron is the leading preclinical CRO company in China, second only to WuXi AppTec. This year, the company has been following in WuXi AppTec’s footsteps, attempting to replicate its growth model by continuously extending its business downstream into the clinical CRO and CDMO sectors.

After establishing integrated end-to-end CRO and CDMO capabilities in the small-molecule field, the Company also expanded into the biologics, cell, and gene therapy CDMO sectors. In 2018, it established Ningbo Pharmaron Biologics to oversee its large-molecule biologic CDMO operations. In the first half of 2020, the Company acquired a 50% equity stake in AccuGen Group, which primarily provides research, development, and manufacturing services for cell and gene therapy products.

On March 1, 2021, Pharmaron announced the acquisition of 100% equity interest in UK-based ABL, a subsidiary of AbbVie, for $120 million. ABL possesses state-of-the-art drug development and clinical manufacturing facilities, providing research and development services for large-molecule drugs, cell therapies, and gene therapies.