Cardiac Valve Sector Accelerates: Domestic Substitution Becomes Irresistible (Part I)

This article was first published on Siyu MedTech Insights, authored by Lily, and republished with permission by VCBeat.

Valvular heart disease, a form of structural heart disease, impairs patients’ quality of life and can be life-threatening in severe cases. Given the characteristics of China’s heart valve industry, the patient population is substantial: there are currently 36.3 million individuals with valvular heart disease in China, a figure projected to rise to 40.2 million by 2025. The field faces significant unmet treatment needs, with procedures concentrated in leading tertiary hospitals and low procedural penetration rates, indicating enormous market potential.

Driven by policies such as the centralized procurement and price reduction of high-value medical consumables, domestically produced medical devices are seizing a prime opportunity to accelerate import substitution, with Chinese-made bioprosthetic valves poised to rapidly replace imported alternatives. Currently, mechanical heart valves account for a larger share of usage in China; however, as clinical data on the durability of surgical bioprosthetic valves accumulates and market acceptance grows, the proportion of bioprosthetic valve utilization is steadily increasing. In terms of competitive landscape, multiple domestic companies have already established a presence in the heart valve sector. China’s heart valve industry stands at a critical development inflection point, representing a golden track for domestic products to replace imports.

(I) Structure and Diseases of Heart Valves

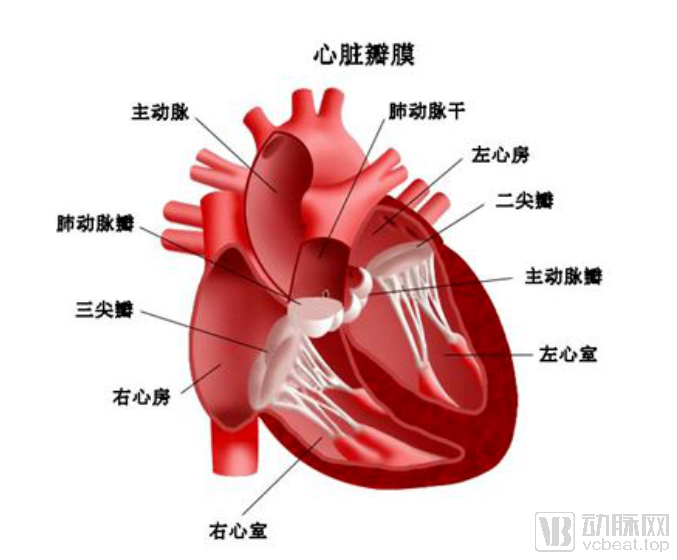

Heart valves refer to the valves located between the atria and ventricles or between the ventricles and arteries. Their primary function is to prevent blood regurgitation, ensuring unidirectional blood flow from the atria to the ventricles, or from the ventricles to the aorta and pulmonary artery. There are four valves in the human heart: the mitral valve, tricuspid valve, aortic valve, and pulmonary valve. Heart valves may develop pathologies such as insufficiency (regurgitation) or stenosis due to congenital defects or acquired conditions like inflammation. These disorders directly impair normal blood circulation, leading to functional cardiac damage.

(Figure: Schematic diagram of the heart structure)

Normal heart valves allow adequate blood flow when open and prevent backflow when closed. Due to congenital or acquired causes, heart valves may lose their normal anatomical structure and physiological function. Obstruction of blood flow during valve opening is termed valvular stenosis; regurgitation of blood during valve closure is termed valvular insufficiency. Sometimes, the same valve exhibits both stenosis and insufficiency. When two or more valves are affected simultaneously, it is referred to as combined valvular disease.

(II) Classification of Valvular Heart Disease

Valvular heart disease refers to cardiac dysfunction caused by anatomical or functional alterations of the heart valves. Based on etiology, valvular heart disease can be classified into congenital and acquired forms; according to valve function, it can be categorized into stenotic and regurgitant diseases. Additionally, it can be classified by the affected site, including aortic stenosis, aortic regurgitation, mitral stenosis, tricuspid regurgitation, and pulmonary regurgitation.

From the perspective of valvular lesion location, the mitral and aortic valves endure the greatest pressure and are most susceptible to involvement; consequently, the incidence of disease in these two valves is higher, whereas the incidence at the pulmonary valve position is very low.

According to statistics, the incidence of mitral and aortic valve diseases is rising rapidly among individuals aged 60 years and older. It is estimated that over 20% of patients with aortic stenosis have severe aortic stenosis, with a two-year survival rate of only approximately 50%. With the advent of population aging, the incidence of valvular heart disease has increased significantly.

(3) Treatment Methods for Heart Valve Disease

Heart valve disease can be managed with pharmacological therapy, but the therapeutic efficacy is often suboptimal. The majority of patients require surgical intervention for a definitive cure, which yields favorable outcomes and can completely alleviate symptoms. Surgical options include heart valve repair, heart valve replacement, and transcatheter heart valve implantation.

(Image source: public information)

Valve Repair Surgery: Surgical repair of damaged heart valves is the preferred treatment option, but it is suitable only for a small subset of patients, such as those with mitral valve disease.

Heart Valve Replacement: Surgical implantation of prosthetic valves to replace damaged native valves. Prosthetic heart valve replacement is generally performed when patients present with the following conditions: mitral stenosis, mitral stenosis combined with mitral regurgitation, severe tricuspid valve pathology, aortic stenosis, or mild aortic valve prolapse. The procedure typically utilizes either mechanical prosthetic valves made from synthetic materials or bioprosthetic valves made from biological tissues; mechanical valves have a larger market share in China. Postoperatively, patients must take anticoagulant medications as prescribed and undergo regular monitoring to maintain coagulation parameters within the therapeutic range. For patients with concurrent atrial fibrillation, radiofrequency ablation may be performed concomitantly with the valve surgery to alleviate symptoms and reduce the incidence of postoperative cerebral embolism.

Interventional Therapy for Heart Valves: With the advancement of interventional techniques, transcatheter heart valve replacement or repair—specifically Transcatheter Aortic Valve Implantation (TAVI)—has rapidly developed and been adopted in clinical practice. In this procedure, an interventional catheter is inserted via the femoral artery to deliver a prosthetic heart valve to the aortic valve region, where it is deployed to restore valvular function. As the procedure does not require open-chest surgery, it is minimally invasive and allows for rapid postoperative recovery. It is performed by experienced cardiologists. The primary indication for TAVI is severe aortic stenosis in patients who are not candidates for surgical valve replacement. Currently, the two most widely used TAVI devices are the Edwards balloon-expandable stent and the CoreValve self-expanding stent.

Transcatheter Aortic Valve Replacement (TAVR), as a minimally invasive interventional therapy, offers the advantages of low surgical risk and strong tolerability in high-risk patients, and has currently become the prevailing trend in the future management of heart valve diseases.

(1) Function of Prosthetic Heart Valves

For patients with severe valvular heart disease, prosthetic heart valve replacement is the most effective treatment. A prosthetic heart valve is an artificial organ that can be implanted within the heart to replace native heart valves (aortic, tricuspid, or mitral), enabling unidirectional blood flow and replicating the function of natural heart valves. When valvular pathology is too severe to be restored or improved by valve commissurotomy or repair surgery, prosthetic heart valve replacement is indicated.

(Image source: public information)

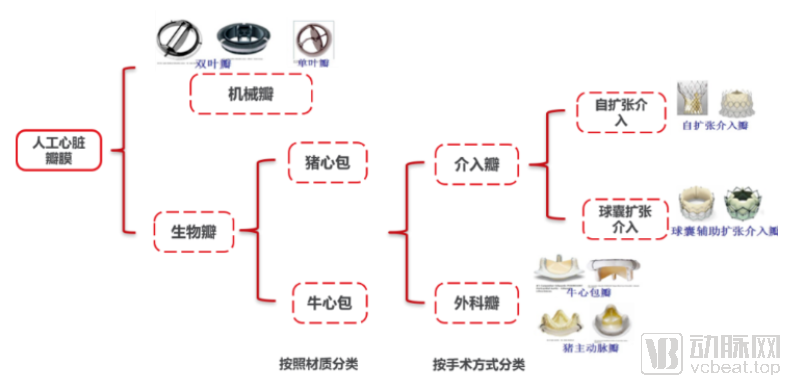

(II) Classification of Prosthetic Heart Valves

Based on the materials used in their construction, prosthetic heart valves can be classified into mechanical valves and bioprosthetic valves. Bioprosthetic valves are further subdivided into stented and stentless bioprostheses. Currently, stentless bioprostheses are rarely used; therefore, bioprosthetic valves are broadly categorized into transcatheter valves and surgical valves. Surgical valves are implanted via open-heart surgery, whereas transcatheter valves are delivered through minimally invasive vascular access. Depending on the delivery system, transcatheter valves can be further divided into balloon-expandable and self-expanding types.

(Image source: Publicly available information)

Mechanical valves are made of pyrolytic carbon material, and currently, the new type of bileaflet valve is mainly used, with two leaflets that can open and close simultaneously. The advantage of mechanical valves is their long lifespan, theoretically lasting a lifetime. However, the biggest disadvantage is that patients must take anticoagulants for life, which carries potential risks such as thrombosis and bleeding. If a mechanical failure occurs, the consequences can be extremely serious. Even now, complications related to postoperative anticoagulation therapy have not been resolved.

Bioprosthetic valves are fabricated from biological tissues, such as those derived from porcine or bovine sources. They offer favorable hemodynamic properties and a low incidence of thrombosis, thereby eliminating the need for lifelong anticoagulation; postoperative anticoagulation is required for only 3 to 6 months. The primary drawback is calcification over time, which carries a potential risk of reoperation for valve replacement.

In light of the advantages and disadvantages of mechanical and bioprosthetic valves outlined above, clinical practice has increasingly favored bioprosthetic valves. Unlike patients with mechanical valves who require lifelong anticoagulation, those receiving bioprosthetic valves generally need anticoagulation therapy for only 3–6 months postoperatively, provided they do not have concurrent atrial fibrillation. After this period, they are no longer exposed to the risks associated with coagulation abnormalities.

(I) A Large Patient Population with Valvular Heart Disease

The population affected by heart valve disease is vast, with substantial treatment needs. Among patients with heart disease, valvular disease has a high incidence rate. According to statistics, approximately 209 million people worldwide suffer from heart valve disease, resulting in about 2.6 million deaths annually. It is estimated that 19.3 million and 26 million people globally suffer from aortic stenosis and aortic regurgitation, respectively.

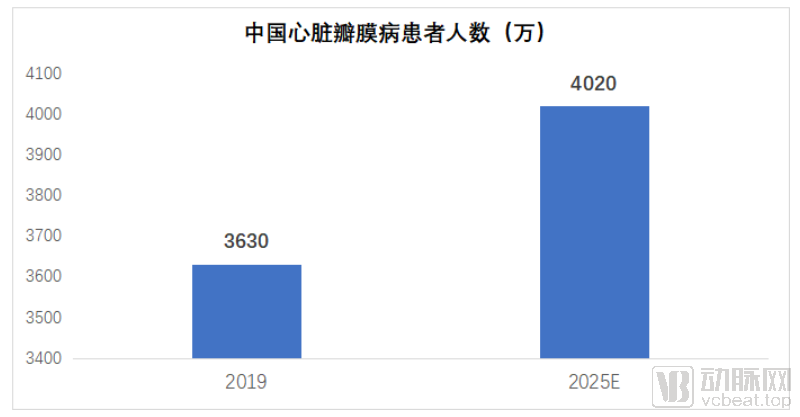

In China, according to the data in the figure below, there were 36.3 million patients with heart valve disease in 2019, and this number is projected to increase to 40.2 million by 2025. Essentially, valve disease is an age-related condition; as the population ages, the prevalence of valve disease gradually increases. With further aging of China’s population in the future, the number of patients with valve disease is expected to continue to rise.

(Image source: public information)

(2) Low Penetration Rate Among Patients Undergoing Heart Valve Surgery, with Significant Growth Potential

In recent years, the artificial heart valve market has experienced significant growth driven by the rising prevalence of heart disease, an aging population, and technological advancements in prosthetic heart valves. However, in practice, the therapeutic demand for heart valves in China remains far from being met, with very low penetration rates.

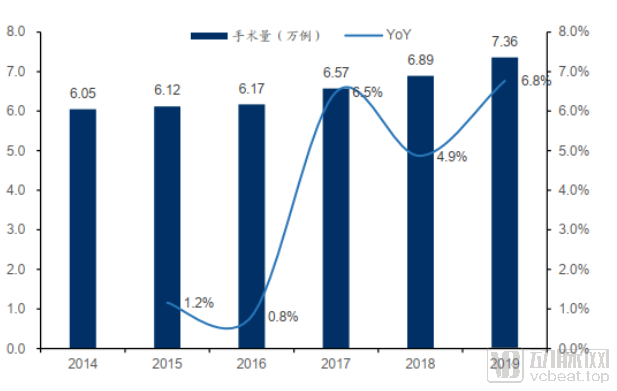

According to statistics, a total of 254,000 cardiovascular surgeries were performed in China in 2019, representing a 5.3% increase, with annual growth remaining at a low rate. Among these, the proportion of heart valve surgeries showed a steady rise: a total of 73,600 heart valve surgeries were completed nationwide in 2019, up 6.8%, with a five-year CAGR of 4.0%. The volume of heart valve surgeries has been growing at a low single-digit rate annually.

(Figure: Number of Heart Valve Surgeries in China (10,000 cases))

(Image source: public information)

From a hospital perspective, cardiac surgical procedures in China are increasingly concentrated in large central hospitals. In 2019, 62 hospitals each performed more than 1,000 cardiac surgeries, collectively completing 152,846 cases, which accounted for 60.2% of the national total. In contrast, 390 hospitals each performed fewer than 100 cases, with a combined total of 14,107 surgeries, representing only 5.56% of the national volume. Due to the high technical difficulty of open-heart valve replacement surgery, cardiac valve procedures are primarily concentrated in top-tier hospitals.

The demand for valve replacement across China remains unmet. The annual surgical volume at leading hospitals has nearly reached saturation, which limits the growth rate of cardiac valve surgeries nationwide. However, with academic promotion by domestic manufacturers and enhanced physician training, there is still significant room for growth in the volume of surgical valve replacements.

(3) Significant Potential for Bioprosthetic Valves to Replace Mechanical Valves

In the global market, bioprosthetic valves dominate the landscape of artificial heart valves. Since 2000, large-scale, long-term evidence-based medical data have increasingly supported the use of bioprosthetic valves, leading to a year-on-year increase in their adoption. By around 2010, the global share of bioprosthetic valves surpassed that of mechanical valves. Particularly in developed countries in Europe and the United States, where degenerative valve disease constitutes the primary patient population, the usage rate of bioprosthetic valves has exceeded 75%, with an even higher proportion observed in the United States.

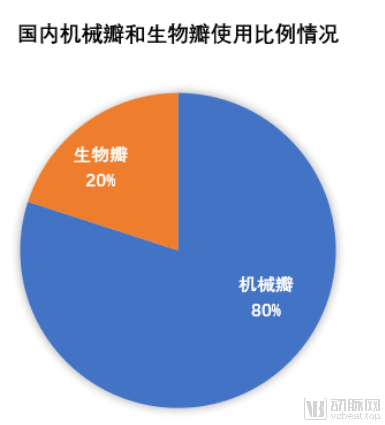

Abroad, bioprosthetic valves are predominant; however, in China’s heart valve replacement procedures, mechanical valves dominate the domestic market, with approximately 80% of patients opting for mechanical valves. The development of bioprosthetic valves has fallen short of expectations, primarily due to immature technology, high costs, limited durability, and substantial R&D expenses.

(Image source: public information)

However, with continuous improvements in the manufacturing technology of bioprosthetic valves, production costs and market prices are decreasing, while the service life of these valves is gradually extending. As patients age, the proportion of bioprosthetic valve selection during surgery steadily increases; approximately 50% of patients aged 60–70 years opt for bioprosthetic valves, rising to over 60% among those older than 70 years. Furthermore, the demographic profile of patients undergoing valve replacement surgery in China is shifting toward an older population, with a significant increase in the proportion of patients aged over 60. As the average age of valve replacement recipients rises, the utilization rate of bioprosthetic valves is expected to grow accordingly. Meanwhile, intensified market education has led to greater patient awareness of the advantages of bioprosthetic valves, thereby enhancing market acceptance.

In 2010, the global share of bioprosthetic valves surpassed that of mechanical valves, with usage in developed countries in Europe and the United States reaching 70%. However, as of 2018, the clinical application rate of surgical bioprosthetic valves in China was only approximately 20–25%. The annual domestic consumption of bioprosthetic valves stood at around 18,000–20,000 units, with an annual growth rate of approximately 12%, roughly twice the growth rate of valve replacement surgeries. Therefore, driven by various policy resources, it is expected that the future structure of valve usage in China will align with that of European and American countries, gradually completing the substitution of mechanical valves with bioprosthetic valves.

(4) Imported Bioprosthetic Valves Dominate the Market, with Accelerated Domestic Substitution of Imports

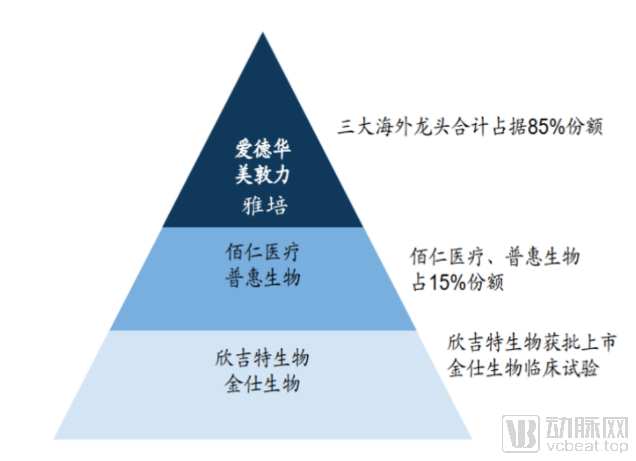

In China's bioprosthetic valve market, imported products currently account for 85% of the market share. Domestically produced surgical valves are priced lower and have demonstrated proven quality. Driven by policies aimed at reducing prices for high-value medical consumables, the substitution of imported products with domestic alternatives is expected to accelerate.

Foreign leading brands dominate the market. In the bioprosthetic valve segment, the three major overseas leaders—Edwards Lifesciences, Medtronic, and Abbott—collectively hold an 85% market share, with Edwards’ bovine pericardial bioprosthetic valves accounting for the largest share at 40%. Domestic surgical valves constitute the Chinese-produced segment, with BaiRen Medical and Puhui Biology holding the remaining 15% share. Xinjite Biotechnology’s surgical valves were launched in mid-2020, while Jinshi Biotechnology’s products are currently in clinical trials. There are relatively few domestic companies developing biological surgical valves.

(Figure: Landscape of the Chinese Bioprosthetic Heart Valve Market)

(Image source: public information)

The proportion of bioprosthetic valves, particularly those manufactured in China, is expected to rise rapidly. BaiRen Medical’s surgical heart valve is the only domestically produced product supported by long-term, large-scale evidence-based medical data. Leveraging durability and safety profiles comparable to those of leading international competitors, it is well-positioned to capture a major share of the Chinese market.

(V) Company Profile and Market Competition

Leading global companies in the heart valve market primarily include Edwards Lifesciences, Medtronic, and Abbott (which acquired St. Jude Medical). Other notable players include Sorin Group (now part of LivaNova), CryoLife (which acquired ON-X Life Technologies), Braile Biomédica, Boston Scientific (which acquired the Swiss company SYMETIS), and Jenavalve Technology (Germany).

As the world’s largest heart valve market, the United States is home to leading global heart valve companies such as Edwards and Medtronic. Europe, the second-largest market for prosthetic heart valves globally, has also given rise to a number of outstanding heart valve companies, including the UK’s LivaNova and Switzerland’s SYMETIS.

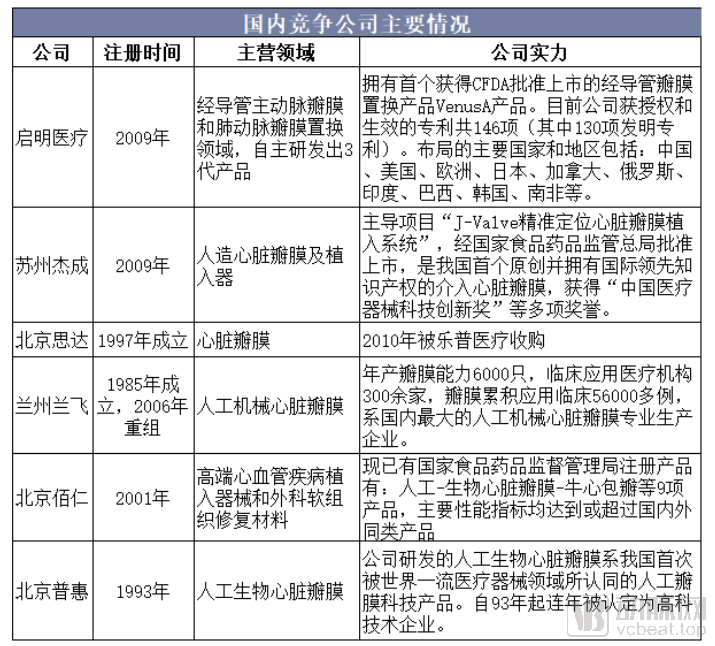

In recent years, a number of domestic companies have emerged in China, including Beijing Bairen Medical, Suzhou Jiecheng Medical, Hangzhou Venus Medtech, Lepu Medical, Beijing Puhui Bio, and Ningbo Jian Shi Biotech. Manufacturers of heart valve devices in China are predominantly concentrated in economically developed regions such as Beijing and the Yangtze River Delta. These areas boast high-quality medical resources and scientific research talent (such as Academician Ge Junbo’s team), and patients in these regions demonstrate a higher level of acceptance toward emerging transcatheter heart valve interventions.

(Image source: public information)

Among them, VenusA-Valve, the transcatheter heart valve system from Hangzhou-based Venus Medtech, and J-Valve, the transcatheter biological heart valve from Suzhou-based Jiecheng Medical, were approved for market launch in 2017 through the special approval pathway for innovative medical devices. Edwards Lifesciences’ SAPIEN valve application was withdrawn; clinical trials for its latest-generation transcatheter aortic valve system, Sapien 3, commenced only in early 2018. MicroPort’s VitaFlow is currently under regulatory review, while Medtronic’s application has been withdrawn. Peijia Medical’s transcatheter aortic valve system, TaurusOne, is in clinical trials. Venus Medtech’s transcatheter aortic valve received approval in 2017, more than two years ahead of its competitors, giving it a significant first-mover advantage.