Global Healthcare Industry Capital Report Q1 2021

I. The primary market in the healthcare sector witnessed unprecedented prosperity in Q1 2021. On one hand, total financing reached record highs: global healthcare funding in Q1 2021 doubled year-on-year, setting a new quarterly record. On the other hand, large-scale financing deals were highly frequent during the quarter, with 98 transactions exceeding $100 million; nearly 50% of all financing rounds were in the tens of millions of dollars.

II. From the perspective of sub-sectors, biomedicine remains dominant. Both domestic and global digital health sectors have accelerated their development spurred by the pandemic, with industry financing volumes multiplying. Biopharmaceuticals, healthcare informatics, and “Internet + Healthcare” continue to thrive; notably, the number of Series C companies in hot tracks has surpassed that of Seed/Angel-stage enterprises.

III. In early 2021, global investment institutions continued to maintain strong enthusiasm for the biopharmaceutical sector; Hillhouse Capital completed 13 investments, becoming the most active investor in Chinese healthcare startups during the first quarter.

IV. Shanghai Becomes the Top Choice for Capital in China’s Healthcare Industry, with the Jiangsu-Zhejiang-Shanghai Region Accounting for Half of All National Financing Deals.

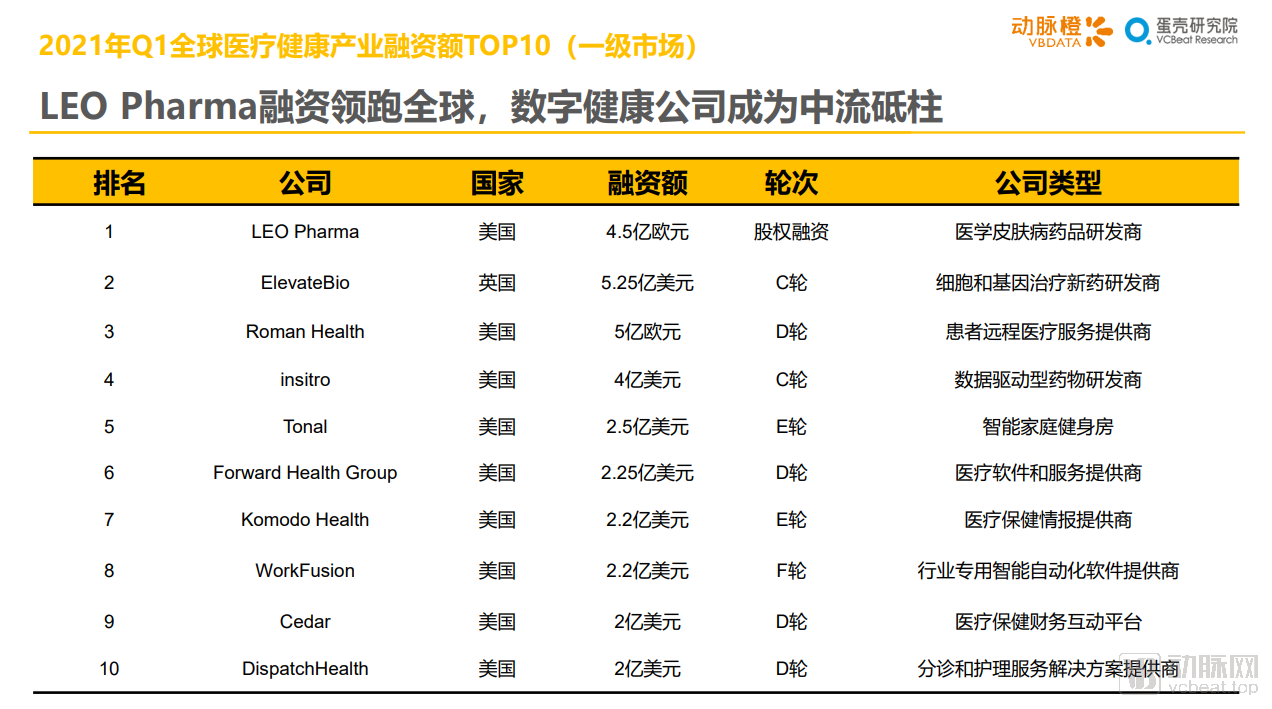

V. Top 10 Most Funded Companies in Q1 2021: Globally, digital health companies have become the backbone of the list; in China, biopharmaceutical companies remain the main force.

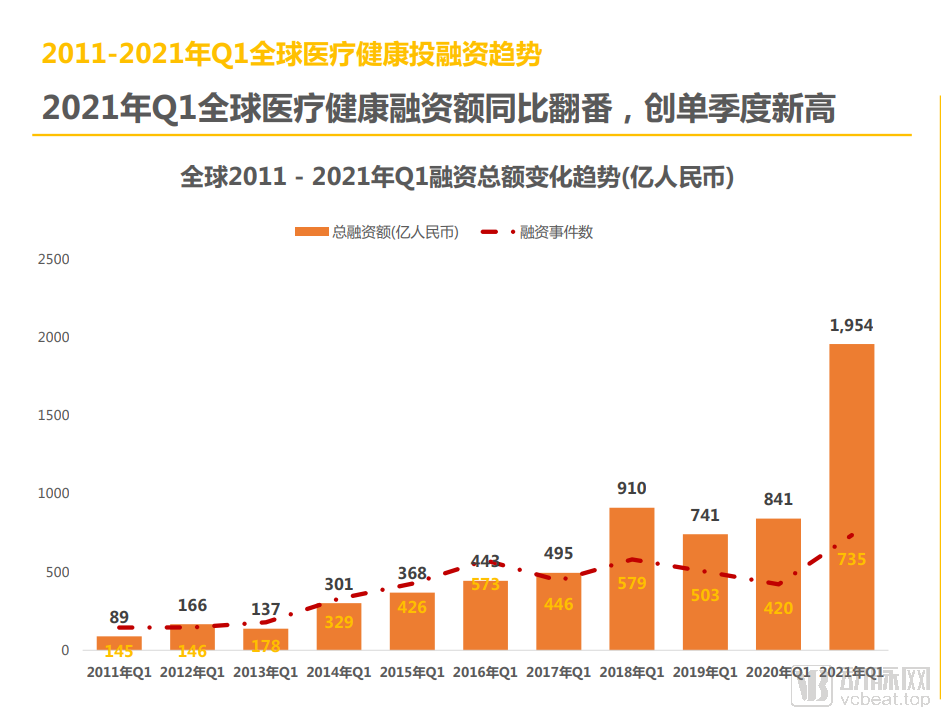

1.1 Global healthcare financing doubled year-on-year in Q1 2021, hitting a new quarterly record high

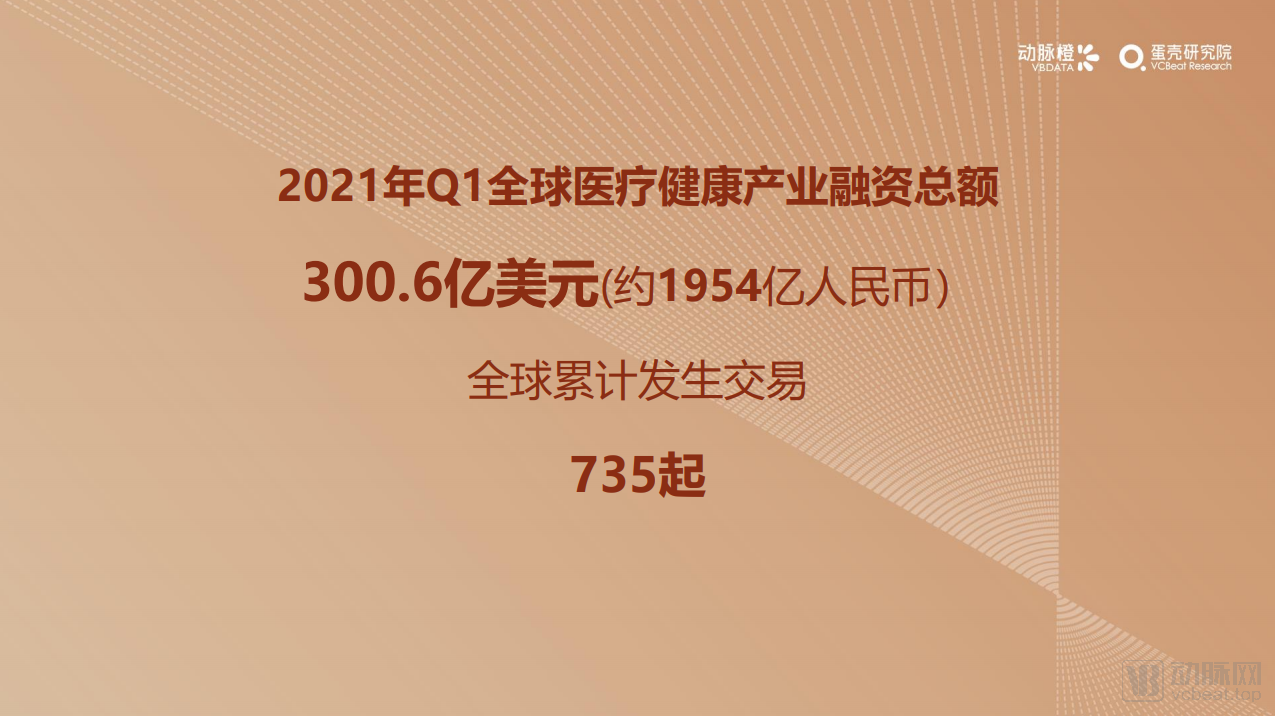

In Q1 2021, the global primary market for healthcare witnessed 735 financing deals, with the total amount reaching a record high of RMB 195.4 billion, representing a doubling in growth; the number of financing deals also surged by 75%. This indicates that the healthcare industry experienced a significant capital boom at the beginning of this year.

Under the guidance of widespread global easing policies in the post-pandemic era, financing conditions in the primary market across all industries have rebounded. The healthcare sector, directly stimulated by the pandemic, has become a particular favorite of investors. Major healthcare companies have experienced a strong performance recovery, with their potential and growth prospects further uncovered; this has accelerated capital inflows and facilitated numerous deals exceeding $100 million, significantly boosting total financing volumes.

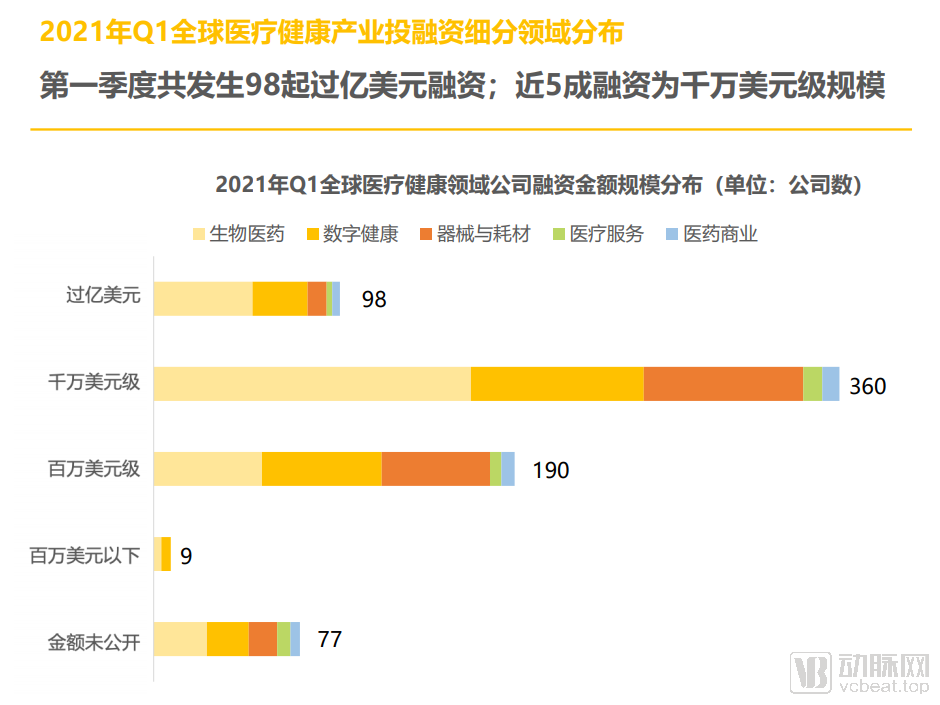

1.2 A total of 98 financing deals exceeding $100 million occurred in the first quarter; nearly 50% of the financings were in the tens of millions of dollars range.

In Q1 2021, there were a total of 98 financing deals exceeding $100 million, accounting for over 10% of the total financing amount in Q1 and reaching approximately half of the full-year 2020 figure; more than half of these deals involved biopharmaceutical companies.

Financing deals valued in the tens of millions of dollars were the most numerous, with biopharmaceutical companies accounting for the largest share, followed by digital health companies, which ranked second in terms of deal volume. In financing deals valued in the millions of dollars, digital health companies were the most prevalent, predominantly concentrated in seed and Series A rounds, indicating that capital was particularly focused on startups in the digital health sector during this quarter.

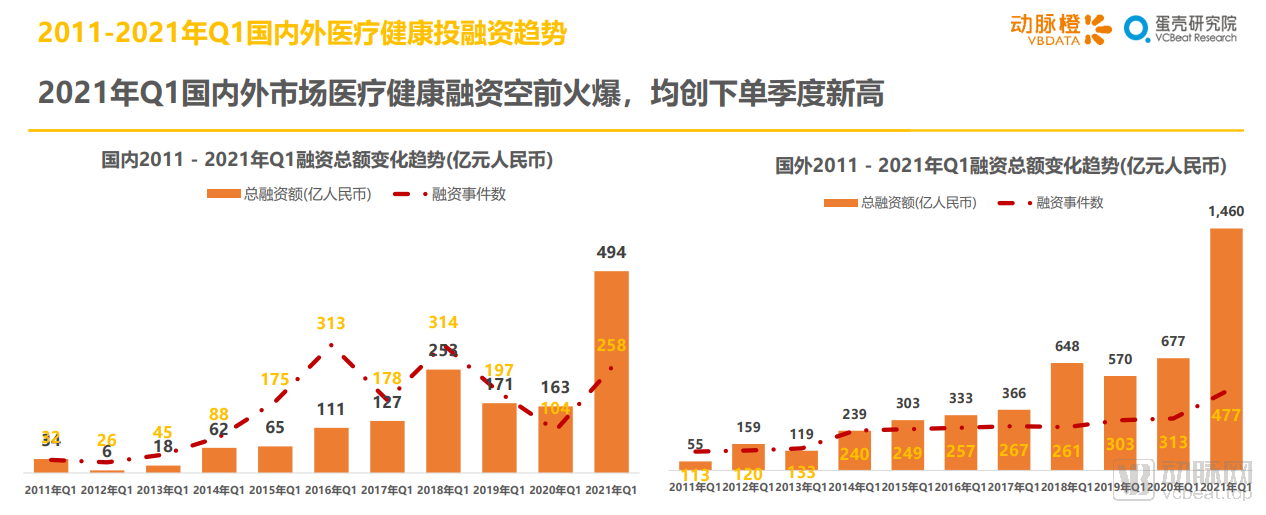

1.3 Healthcare financing in both domestic and international markets reached unprecedented levels in Q1 2021, hitting new quarterly highs

In Q1 2021, a total of 258 financing events occurred in China’s healthcare industry, with the total financing amount reaching RMB 49.4 billion, representing a year-on-year increase of approximately 203%. In Q1 of the previous year, the number of financing events in China’s healthcare industry declined sharply due to the impact of the pandemic, whereas this year the number of financing events doubled. In addition to the catalytic effect of the COVID-19 pandemic on the influx of capital into the healthcare sector last year, strong policy support in China has accelerated the enhancement of core competitiveness among domestic and international medical enterprises. These companies have shifted from being marketing-driven to R&D-driven, thereby attracting more talent and resources from the market.

A total of 477 financing deals occurred in the overseas healthcare industry, with the total funding amount reaching $22.46 billion (approximately RMB 146 billion), marking the highest quarterly total on record and representing a year-on-year increase of approximately 116%. There were as many as 78 individual financing rounds exceeding $100 million this quarter. Financing in the overseas healthcare sector was primarily concentrated at Series C, with a few companies advancing to Series E; only WorkFusion, a healthcare informatics company, completed a Series F round.

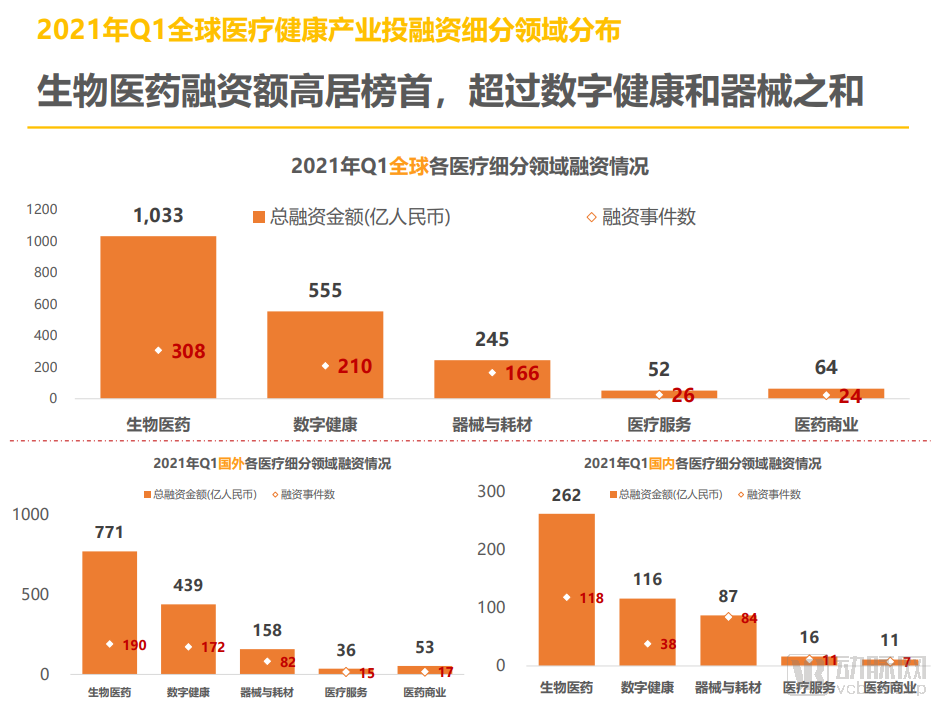

2.1 Biopharmaceutical Funding Tops the List, Surpassing the Combined Total of Digital Health and Medical Devices

In Q1 2021, the global biopharmaceutical sector once again led all subsectors with 308 transactions totaling RMB 103.3 billion (approximately USD 15.9 billion). The digital health sector followed closely with 210 transactions, while medical devices and consumables ranked third.

The average financing amount in the biopharmaceutical sector is significantly higher than that in other sub-sectors, with more than 50 individual financing deals exceeding $100 million this quarter.

A comparison of sector distributions between China and international markets reveals that both the number of financing deals and the total transaction value in digital health are significantly higher abroad, indicating a more advanced development stage for digital health overseas. In China, however, the medical devices and consumables sector remains a major hotspot, with the number of financing events far exceeding those in digital health.

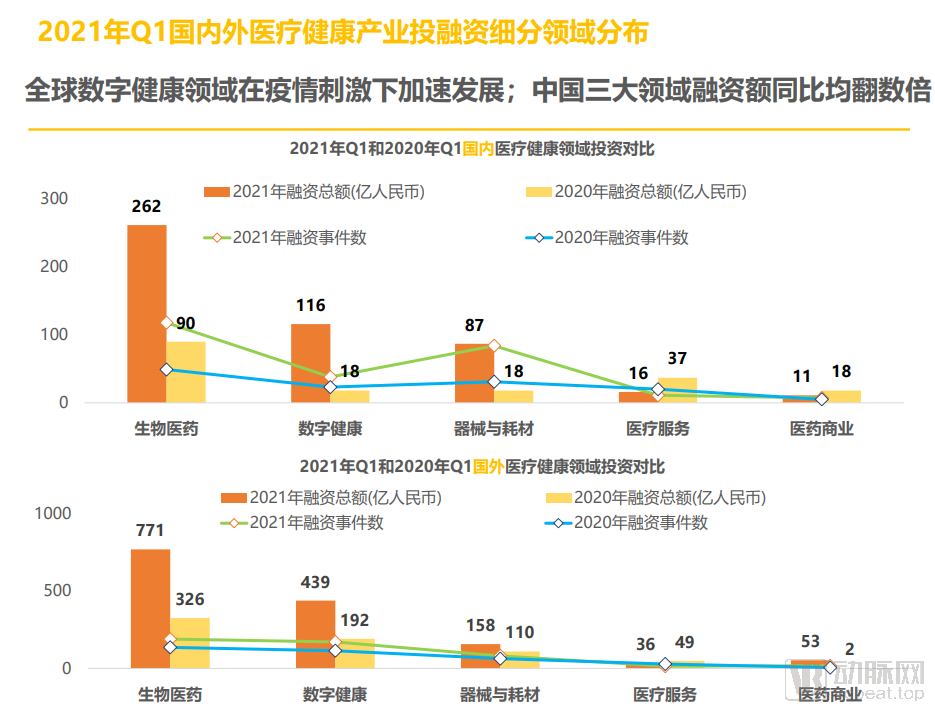

2.2 Global digital health sector accelerates development under pandemic stimulus; China’s three major sectors see year-on-year financing multiply several-fold

In Q1 2021, the total financing amounts in China’s three major subsectors—biopharmaceuticals, digital health, and medical devices & consumables—all increased several-fold. Notably, financing in the digital health sector surged fivefold year-on-year, primarily driven by 29 large-scale funding rounds each exceeding $100 million.

In China, the healthcare services and pharmaceutical commerce sectors saw a 27% quarter-on-quarter decline in financing amounts in 2021, along with a decrease in the number of financing deals. In terms of financing activities, transactions in the healthcare services sector during Q1 2021 were primarily concentrated at Series A, with no large-scale financings exceeding USD 100 million.

Similarly, financing in the digital health sector abroad has also seen a significant increase. The concurrent changes both domestically and internationally further corroborate the accelerated development of healthcare, particularly in the field of digital health, in the post-pandemic era.

2.3 Biopharmaceuticals, healthcare informatization, and “Internet+ Healthcare” remain hot; the number of Series C companies in popular sectors exceeds that of seed/angel-stage companies

In Q1 2021, tags such as biopharmaceuticals, healthcare informatization, Internet+ healthcare, and IVD garnered high levels of interest.

From the perspective of funding round distribution, Series A financing events occurred most frequently, totaling 211. The number of projects that completed Series C financing exceeded those in the angel/seed rounds, reflecting two characteristics:

First, large-scale innovation in the healthcare sector—from laboratory research to commercialization—may have slowed down, and various hot subsectors are becoming saturated. Consequently, the number of emerging projects that can attract capital favor is limited.

Second, an increasing number of companies whose business models have passed initial validation are able to reach Series C financing, and more mature companies are also more favored by capital, which is particularly evident in the biopharmaceutical sector.

3.1 In recent years, the overall investment frequency of leading healthcare investment institutions has increased year by year

3.2 In early 2021, investment institutions worldwide continued to maintain strong enthusiasm for the biopharmaceutical sector

In Q1 2021, OrbiMed and Cormorant Asset Management were the most active investors in global healthcare, with each firm completing 17 investments in a single quarter.

Specifically, in Q1, OrbiMed invested in 11 biopharmaceutical companies, including Graphite Bio, and four medical device companies, including Delfi Diagnostics.

Compared with previous years, the enthusiasm of top-tier institutions for investing in the healthcare sector in 2021 continued the heat seen since 2020. Investment activities generally surged significantly; even Perceptive Advisors, ranked tenth, made more than 10 investments in a single quarter.

Notably, oncology company Pyxis Oncology and vaccine developer Affinivax were co-invested by more than four active institutional investors, emerging as the focal points of strong institutional interest this quarter.

3.3 Hillhouse Capital Completed 13 Investments, Becoming the Most Active Investor in Domestic Healthcare Startups in Q1

Hillhouse Ventures, the arm of Hillhouse Capital focused on early-stage startups, has maintained the investment momentum it has built since its inception last year. With 13 deals, it emerged as the most active investor in China’s healthcare sector this quarter. To date, it has surged ahead, completing more than 50 investments in the healthcare field.

Sequoia Capital China, Lilly Asia Ventures, and Hong Kong-based 8VC tied for second place with 11 financing deals.

4.1 Global: The US Leads the World, with China and the US Accounting for 85% of Global Financing

In Q1 2021, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, India, and Denmark.

In Q1 2021, the United States led the world with 358 financing deals totaling $18.072 billion (approximately RMB 117.468 billion), followed closely by China; together, the two countries accounted for 85% of the total global financing amount.

Meanwhile, Asia is playing an increasingly indispensable role in driving innovation within the healthcare industry. Since 2020, India has emerged as one of the top five global hotspots for healthcare investment and financing. The widespread adoption of smartphones and the internet in India has spurred a surge in “Internet + Healthcare” innovations across the region.

4.2 China: Shanghai Remains at the Top, with Jiangsu, Zhejiang, and Shanghai Accounting for Half of All Financing Events

The five regions with the most concentrated healthcare and medical investment and financing activities in China in Q1 2021 were, in order, Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang.

In 2020, Shanghai surpassed Beijing for the first timeBecomeThe Hottest Regions for Primary Market Investment in Healthcare. In Q1 2021, Shanghai also ranked first in both the number of financing deals and the total amount raised, with a cumulative total of 71 financing events and funds raised reaching RMB 15.031 billion, nearly RMB 5 billion ahead of Beijing, which ranked second.

The Jiangsu-Zhejiang-Shanghai region remains the backbone of China’s healthcare innovation, with 138 financing deals accounting for half of all healthcare financings in China in Q1 2021.

4.3 United States: California Remains Dominant, with Massachusetts and New York Emerging as Secondary Hubs

In Q1 2021, California, USA, recorded a cumulative total of 358 financing deals, raising $20.66 billion (approximately RMB 132.25 billion), making it the most active region globally for healthcare venture capital investment transactions.

Massachusetts has surpassed the more economically developed New York State to become the second-largest U.S. state for healthcare and medical investment and financing, thanks to its renowned biotechnology industry cluster and abundant medical resources; however, it still lags far behind California in terms of scale.

5.1 Top 10 Global Fundraisings: LEO Pharma Leads Globally, Digital Health Companies Emerge as the Backbone

5.2 Top 10 Financing Deals in China: CDMO WuXi XDC Completes Largest Q1 Funding Round, Biopharmaceutical Companies Remain the Main Drivers of High-Value Financing