In-Depth Analysis of China's Ventilator Industry Status in 2021

Author: Zheng Yuan

In 2020, through the united and concerted efforts of the entire Chinese population, China became the first country in the world to successfully contain the spread of the COVID-19 pandemic and achieve a comprehensive resumption of work and production. Riding this momentum, the domestic ventilator industry entered a rare “golden period” of development, witnessing a surge in both export and domestic demand. According to incomplete statistics, by the beginning of this year, the industry had achieved export revenues exceeding RMB 30 billion and domestic sales surpassing RMB 15 billion, making outstanding contributions to the fight against the COVID-19 pandemic for both China and the global community.

However, opportunities and challenges coexist. The significant industry growth driven by the contingent factor of the COVID-19 pandemic has not fundamentally altered the overall technological disadvantage of China’s ventilator industry. In the normalized market competition of the post-pandemic era, it continues to face severe and urgent tests and challenges.

The overall technical level of China’s ventilator industry lags behind the international advanced standards by at least 20 years. Leading domestic manufacturers still employ “hot-wire” flow sensors at the inspiratory end of adult ventilators—a technology that has been phased out by mainstream international products. High-tech models, such as those for neonatal conventional and high-frequency ventilation, remain largely unavailable in the domestic market. Clinical feedback indicates that domestically produced ventilators exhibit low levels of automation in adapting to patients’ spontaneous breathing, resulting in pronounced patient-ventilator asynchrony and a high rate of reintubation.

Moreover, the overall localization rate of the complete device is low. Key components, such as flow sensors, voice coil motors, and oxygen cells, must be sourced internationally, leaving the industry still vulnerable to supply chain constraints imposed by international medical giants.

In 2019, the domestic market size of China's ventilator industry (calculated at ex-factory prices) was approximately RMB 12 billion. As the most critical equipment in life support respiratory systems, the high-end medical ventilator market is dominated by German and American industry giants, which hold 80–90% of the market share. There is a domestic gap in the production of neonatal high-frequency and conventional-frequency ventilators among Chinese-made products.

Chinese ventilator manufacturers occupy a second-tier position in the global export market. Prior to 2020, the life support systems divisions of leading domestic companies primarily exported anesthesia machines and ECG monitors, while ventilators saw dismal sales in the international market.

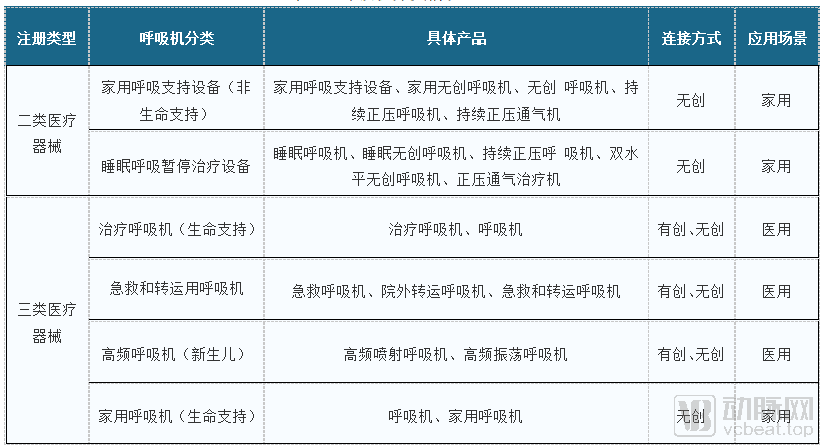

Table 1: Classification of Ventilators

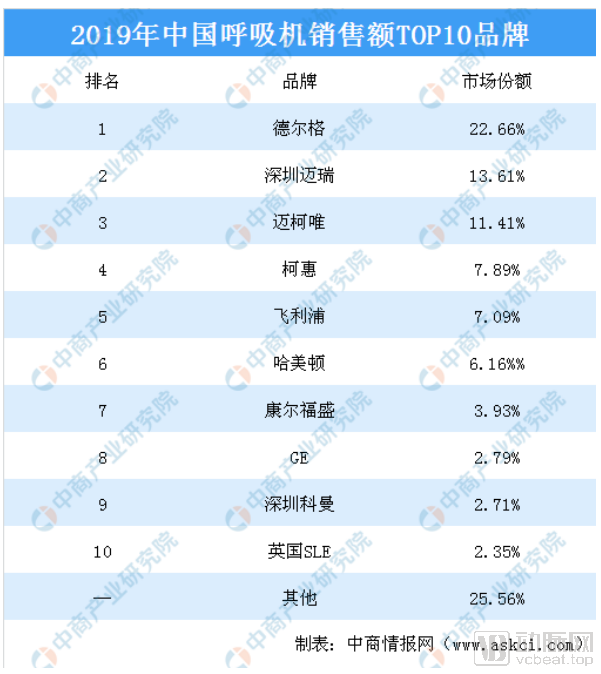

In 2019, the market size of China’s ventilator segments was as follows: medical adult ventilators, RMB 6 billion per year; medical neonatal ventilators, RMB 1.5 billion per year; and home-use ventilators, approximately RMB 4 billion per year. Ventilators are the most critical devices in life-support respiratory systems. Leading brands in the domestic market include Dräger (Germany), Maquet (Germany), GE, Medtronic Covidien (PB Tyco), Hamilton Medical (Switzerland), Philips Respironics, F&P Healthcare (Switzerland), and Löwenstein Medical (Germany). Among them, Dräger holds the largest market share, with annual sales in the Chinese market exceeding RMB 1 billion. Other major players, such as Maquet, GE, and Medtronic Covidien (PB Tyco), generate annual revenues of RMB 500–800 million. In the medical neonatal ventilator segment, only one domestic brand, Shenzhen Comen, has had its non-invasive neonatal ventilator product included, with estimated annual sales of around RMB 200 million.

Table 2: Market Size of Ventilators in China

Table 3. Market Share of Major Brands in the Domestic Medical Device Market

Ventilator technology, in turn, leads the development trends of the anesthesia machine market. Only by advancing ventilator technology can the technical standards and brand reputation of anesthesia machines be enhanced. Otherwise, domestically produced anesthesia machines will remain trapped in the current “vicious cycle” of market development: severe product homogenization, insufficient technological innovation, product obsolescence, and a downward spiral into cutthroat price competition.

Constrained by technical barriers and limited R&D investment, the domestic ventilator industry has long been confined to the low-end segment, failing to meet the clinical needs of hospitals or achieve breakthroughs in sales.

The most critical core technology lies in ventilator design, which involves the seamless integration of software derived from respiratory algorithm formulas and hardware servo systems to deliver intelligent respiratory support tailored to changes in a patient’s spontaneous breathing. The most advanced ventilator technologies are monopolized by German companies.

Next is the issue of supply for critical hardware components, such as turbine motors, flow sensors, high-precision air proportional control valves, and oxygen cells. These can initially be sourced through international suppliers; as domestic ventilator production scales up and the upstream and downstream industrial ecosystems gradually mature, these supply chain challenges can be progressively resolved.

Regarding ventilator algorithm formulas involved in ventilator design, there is a gap of at least 20 years between China's ventilator industry and foreign technologies. This severely limits the user comfort experience of domestically produced products, making them unable to fully meet the actual needs of clinical use.

Due to outdated technology and an insufficient reserve of R&D talent, domestic ventilator manufacturers are unable to achieve rapid development or catch up with international competitors. To realize a fundamental technological leapfrog, it is essential to pursue a dual strategy: on one hand, adopt a development path centered on introducing international technologies, followed by absorption, digestion, and subsequent innovation; on the other hand, integrate resources across China’s medical, computer software, and electromechanical industries to launch concerted efforts in overcoming critical technical challenges.

In 2020, due to the outbreak of the COVID-19 pandemic, total sales from domestic and international exports reached RMB 45 billion, marking a significant surge.

Given China’s large population base and insufficient allocation of medical equipment, the recent pandemic has trained a substantial workforce of healthcare professionals proficient in ventilator use. Even excluding the exceptional surge driven by the 2020 outbreak, the domestic ventilator market is projected to achieve rapid annual growth of 20–30% over the next decade, based on the normal 2019 market size of approximately RMB 12 billion.

Moreover, ventilators are characterized by prolonged operational hours and high wear-and-tear, resulting in a typical product lifecycle of approximately five years and an annual replacement rate of around 20%. As critical devices within life support systems, the ventilator market undoubtedly represents a blue-ocean market poised for stable future growth.

By the end of 2020, Mindray Medical launched its new non-invasive neonatal ventilator, the NB350. However, its clinical efficacy remained to be validated by the market, and there had been no updates regarding the research and development of neonatal high-frequency and conventional ventilators. In June 2020, Aerospace Changfeng Medical introduced a domestically produced model, the Adult Ventilator 8250, which is a copy of the German Elisa ventilator. This model adopted the internationally mainstream “differential pressure” flow sensor, representing a significant advancement. Nevertheless, the overall technical level of the complete device still lagged behind high-end foreign products, with urgent improvements needed in automation and protective ventilation mode settings. Currently, there is still a gap in the domestic market for both conventional and high-frequency neonatal ventilator models. The Hongming Ventilator Project’s international team, an industry “newcomer” from the aerospace sector, is currently undertaking key technological breakthroughs.

During the 2021 “Two Sessions,” the Communist Party of China and the Chinese government issued a significant call to “address weaknesses and accelerate industrial upgrading.” The Chinese ventilator industry is currently experiencing a rare historical opportunity for development; however, the road ahead is long and fraught with challenges. Domestic ventilator manufacturers should remain vigilant in times of stability and strive for continuous progress. Only by strengthening scientific and technological breakthroughs and forging ahead to secure a leading position at the international frontier of technology can we illuminate the “technology tree” of China’s industrial upgrading.

China’s financial sector should also strengthen surveys of frontline clinical market demands, focus on the “pain points” in industry development, and effectively allocate social resources to support technological innovation, rather than creating an industry “crowding-out effect” for short-term gains.

Only through the concerted efforts of all Chinese people can a favorable environment for innovation and entrepreneurship be fostered, thereby advancing national industrial upgrading and realizing the “Chinese Dream” of the great rejuvenation of the Chinese nation.