Domestic Neurovascular Intervention Leaders Accelerate Import Substitution Despite Just 3.8% Market Share: A Special Report

On January 27, Mindray Medical submitted its prospectus to the Hong Kong Stock Exchange.

On March 23, ZC Medical submitted a listing application to the Main Board of the Hong Kong Stock Exchange.

As Mindray Medical and Jiaochuang Tongqiao successively filed their prospectuses, the neurointerventional sector in which they operate has garnered increasing attention.

On the other hand, Peijia Medical went public in May 2020 with an IPO price of HK$15.36 per share. On April 9, 2021, its stock price reached HK$26, representing a nearly 70% increase from the IPO price, while its total market capitalization exceeded HK$17.3 billion. The availability of smooth exit channels and the visibly vast market size have made primary market financing and investment in the neurointerventional field exceptionally robust.

According to incomplete statistics from VCBeat, at least 24 innovative companies and 25 investment institutions have already placed bets on the neurointerventional field. From early 2020 to the present, there have been at least 15 financing events in the neurointerventional sector, with total funding exceeding RMB 1.5 billion.

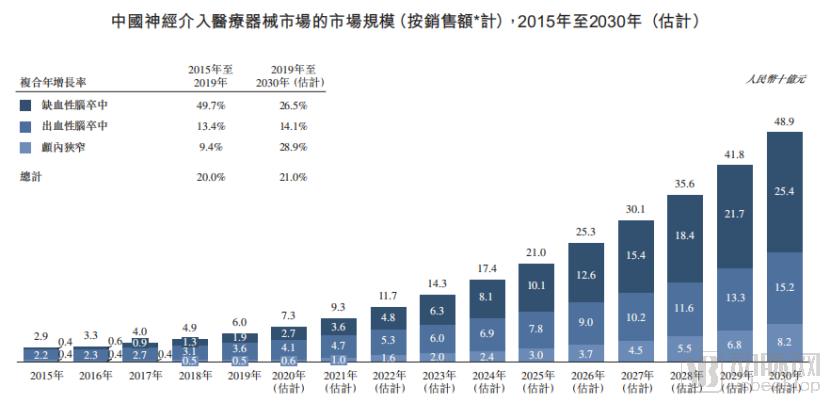

Why Is the Neurointerventional Industry Garnering Significant Attention? Due to the substantial market potential in neurointervention, domestic companies can replicate the success story of coronary stents. According to the prospectus of Mindray Medical (Note: Correction based on context, it should be "Xinwei Medical" as per original text): The market size of neurointerventional medical devices in China increased from RMB 2.9 billion in 2015 to RMB 6.0 billion in 2019, with a compound annual growth rate of 20%, and is projected to reach RMB 7.3 billion by 2020.

(Image source: Xinwei Medical's prospectus)

Based on the domestic substitution trajectory of coronary stents, the neurointerventional field already boasts a more favorable market environment, and domestic substitution will proceed more rapidly.

From a policy perspective, the state is actively promoting the localization of high-end medical devices and encouraging hospitals to procure domestically produced products. In terms of the market, China has 13 million stroke patients, with approximately 2 million new cases annually, representing a substantial patient population. Regarding capital, innovative enterprises in the neurointerventional field are currently well-funded and highly favored by investment institutions.

In addition, the prospectus of Zylox-Tonbridge Medical Technology Co., Ltd. shows that the number of neurointerventional procedures in China increased from 77,400 in 2015 to 159,600 in 2019, with a compound annual growth rate (CAGR) of 19.8%, and is expected to reach 1.781 million by 2030.

Based on the above conditions,High-quality domestically produced neurointerventional products, once launched, will pose a significant threat to foreign brands such as Medtronic and Johnson & Johnson.

Currently, MicroPort NeuroTech and Peijia Medical, which have established a presence in the neurointerventional field, have released their 2020 annual reports. Meanwhile, Xinwei Medical and Jiantong Shenqi (Guichuang Shentong) have also disclosed their 2020 financial performance in their prospectuses. In light of these data, how are the leading players in the neurointerventional sector faring? What characteristics define their revenue and R&D investment patterns? Furthermore, what future market landscape do their development strategies reveal?

VCBeat (WeChat ID: vcbeat) provided a detailed analysis of the prospectuses or 2020 financial reports of the aforementioned four companies.

The current neurointerventional market mirrors the coronary stent market of two decades ago, with multinational corporations such as Medtronic, Johnson & Johnson, and Stryker dominating the majority of market share. Meanwhile, domestic enterprises are only just beginning to emerge, with most Chinese-made neurointerventional products still in the stages of research and development, clinical trials, or regulatory submission for registration.

However, leading domestic companies such as MicroPort NeuroTech, Peijia Medical, Genesis Medtech, and NevaMed have launched multiple neurointerventional products and achieved substantial revenue.

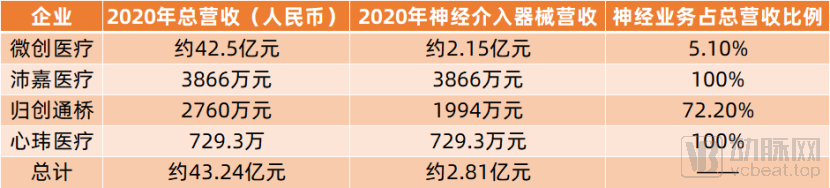

For example, in 2020, MicroPort NeuroTech generated $32.9 million (approximately RMB 215 million) in revenue from its neurointerventional business; Peijia Medical reported total revenue of RMB 38.66 million, a year-on-year increase of 106.7% from RMB 18.7 million in 2019, with all income derived from its neurointerventional operations; VitaeBridge Neurovascular achieved total revenue of RMB 19.94 million from its neurointerventional devices, primarily driven by sales of its core products, the Jiaolong Intracranial Thrombectomy Stent and intracranial support catheters; and Xinwei Medical recorded revenue of RMB 7.293 million in the first nine months of 2020.

(VCBeat Statistics)

MicroPort, Peijia Medical, GenesisCare, and HeartCare in 2020Neurointerventional DevicesTotal revenue amounted to approximately RMB 281 million, with MicroPort Medical accounting for 76.5%.

Based on the aforementioned data, MicroPort NeuroTech generated RMB 215 million in revenue, accounting for the largest share, while HeartCare Medical generated RMB 7.293 million, representing the smallest share. In terms of revenue alone, MicroPort NeuroTech is currently the leading enterprise in the neurointerventional field. The reason why MicroPort NeuroTech, with its multi-sector layout, takes the lead, whereas HeartCare Medical, which focuses exclusively on the neurointerventional field, has the lowest revenue, is that MicroPort has a larger number of listed neurointerventional products among the four companies, an earlier market entry, and the strongest brand influence.

MicroPort’s 2020 annual report indicates that it currently has six neurointerventional products on the market. Its flagship product, Tubridge® Vascular Reconstruction Device, the first of its kind approved for listing in China, gained market recognition and achieved rapid growth in 2020. The new product, Numen® Coil Embolization System, obtained medical device registration certification in 2020 and commenced sales. Additionally, sales of the distributed product, ASAHI Neuro Guidewire, experienced rapid growth.

Peijia Medical is the company with the largest number of approved neurointerventional products, having launched eight such products. Benefiting from its product portfolio and aggressive marketing efforts, Peijia Medical ranks second in revenue among domestic neurointerventional companies.

Interestingly, despite having only two neurointerventional products on the market, Zhongyi Medical (ZCMB) generated RMB 19.94 million in revenue. This is because its marketed intracranial thrombectomy stent, as the company’s core product, has benefited from robust marketing efforts and widespread recognition among clinical experts.

As for Xinwei Medical, this is because it only began selling its products in the first quarter, resulting in a short promotion period and a limited number of launched products.

(Compiled and tabulated by VCBeat)

According toBased on the estimated neurointerventional market size of RMB 7.3 billion in 2020 and the combined neurointerventional business revenue of RMB 281 million for four companies, as disclosed in Xinwei Medical’s prospectus,MicroPort, Peijia Medical, Acotec Scientific, and HeartCare Medical collectively account for 3.8% of China’s neurointerventional market.

Based on the aforementioned data, multinational brands continue to dominate the majority of the domestic neurointerventional market. Consequently, there is substantial room for import substitution in China’s neurointerventional market, presenting significant development opportunities for domestic neurointerventional enterprises.

Based on the revenue data from four companies, the path toward domestic substitution in the neurointerventional sector is just beginning. The low market share of domestically produced neurointerventional products is attributable to the limited number of such products currently launched on the market, with a greater proportion still in clinical trial or registration stages.

(Compiled and tabulated by VCBeat)

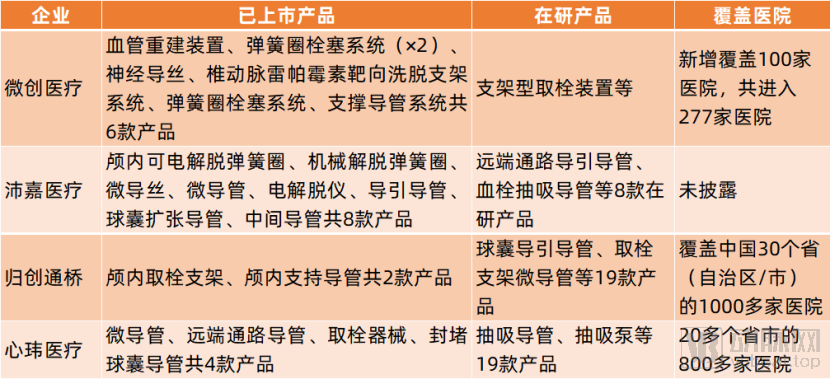

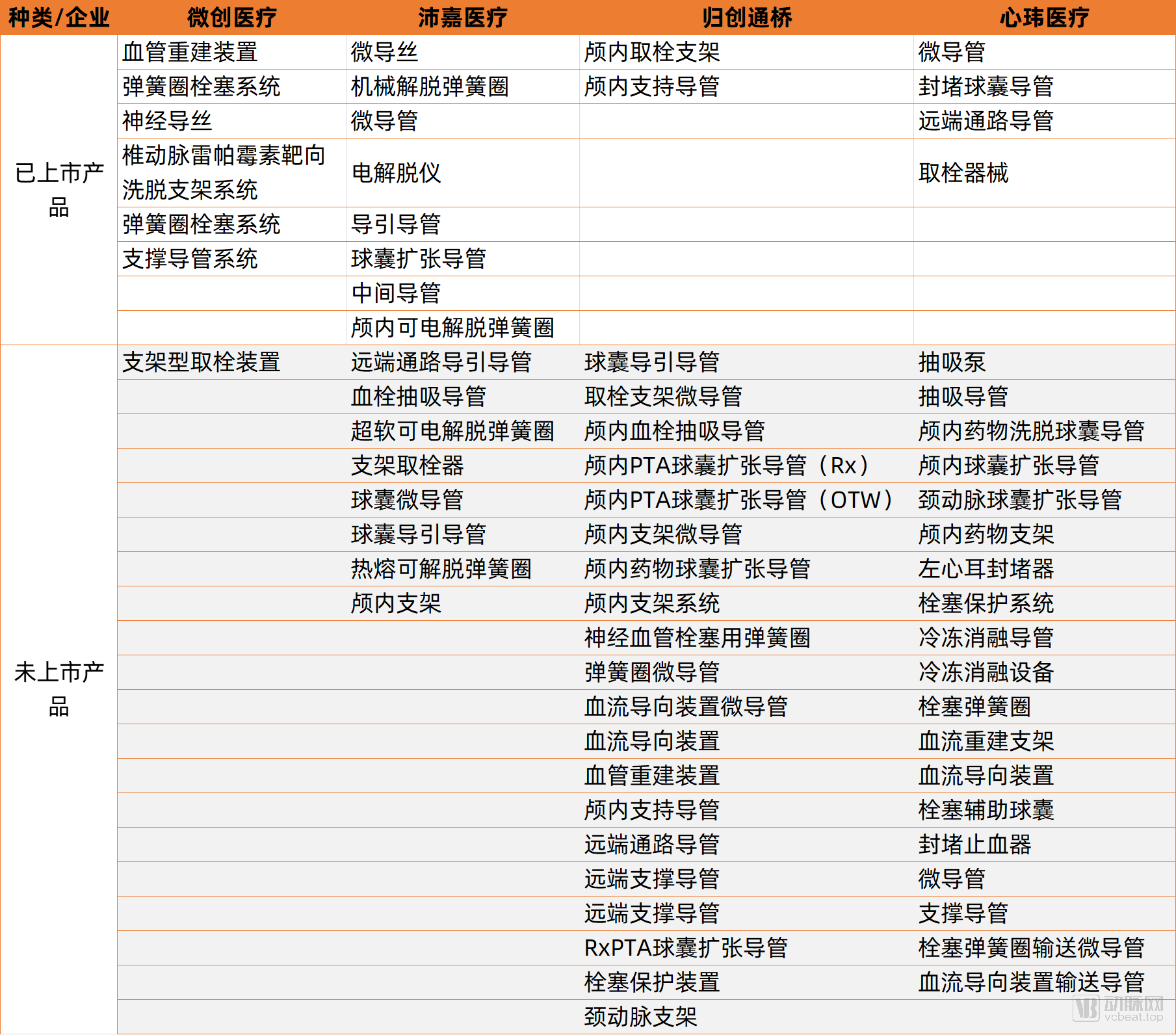

As shown in the figure above, except for MicroPort Medical, most products of the other three companies are in the clinical, registration, or R&D stages, with launched products accounting for a smaller portion.Based on data from various companies’ annual reports, it is projected that a wave of innovative neurointerventional products will be launched in the next 2–3 years. This will significantly enhance the competitiveness of domestic enterprises and accelerate the process of import substitution with domestically produced alternatives.The following provides a detailed analysis from the perspectives of each company’s product portfolio and market promotion.

Despite the impact of the COVID-19 pandemic on neurointerventional procedures, MicroPort’s neurointerventional business maintained rapid growth, with revenue increasing by 17.5% year-on-year after excluding the impact of exchange rate fluctuations.

MicroPort’s 2020 annual report indicates that the performance growth in its neurointerventional segment was primarily driven by: market recognition and rapid adoption of its flagship product, Tubridge® Flow Diverter, the first such device approved for marketing in China; regulatory approval and commercial launch of its new product, the Numen® Coil Embolization System; and rapid sales growth of the distributed ASAHI neuro-guidewire. By the end of 2020, the Tubridge® Flow Diverter had expanded coverage to an additional 100 hospitals, reaching a total of 277 hospitals.

According to MicroPort's annual report,We believe thatIts primary revenue in the neurointerventional field is derived from the agency product, the ASAHI neuroguidewire, andTubridge® Vascular Reconstruction Device。

Based on the product portfolio outlined in the table above, MicroPort has a relatively limited product line, with only one product currently under development. MicroPort’s Bridge® Vertebral Artery Sirolimus-Targeted Eluting Stent System, Numen® Coil Embolization System, and U-Track® Support Catheter System have all obtained registration certificates from the National Medical Products Administration (NMPA). Rapid Medical, in which MicroPort has invested, has also made new progress; its Tigertriever™ Stent Retriever entered the Green Channel in 2020.

However, it is evident that Peijia Medical, Genesis MedTech, and HeartCare Medical are all engaged in the research and development of, or already have marketed, products such as coils, drug-eluting stents, neuro-guidewires, support catheters, and thrombectomy stents—areas where MicroPort has established its presence. Consequently, MicroPort will face intense competition in the neurointerventional field in the future.

At this stage, MicroPort continues to reap the benefits of its early entry into the neurointerventional field: as the tiered diagnosis and treatment system drives market penetration into lower-tier markets, the market share of its Tubridge® Vascular Reconstruction Device has continued to rise. The device gained coverage in an additional 100 hospitals in 2020, reaching a total of 277 hospitals by the end of that year.

In addition, MicroPort obtained six registration certificates in four overseas countries in 2020 and is poised to launch global marketing campaigns. This global expansion may provide MicroPort with new growth drivers, marking its proactive entry into international market competition. The company will begin to compete directly with multinational giants such as Medtronic and Johnson & Johnson, and the quality of its neurointerventional products will be tested in the international marketplace.

In 2020, Peijia Medical’s total revenue reached RMB 38.66 million, representing a year-on-year increase of 106.7% from RMB 18.70 million in 2019, with all revenue derived from its neurointerventional business.

Peijia Medical’s annual report shows that in 2020, a total of eight of its products received registration certificates and were launched for commercial sale, namely: Jasper® Electrolytically Detachable Coils for Intracranial Aneurysms, Presgo® Mechanically Detachable Coils, Presgo® Microguidewires, Presgo® Microcatheters, Jasper® Electrolytic Detachment Unit, Heralder® Guiding Catheters, SacSpeed® Balloon Dilatation Catheters, and Tethys® Intermediate Catheters.

Among these, certain products have obtained registration certificates in overseas markets and are expected to expand into international markets. For instance, the Jasper® Intracranial Electrolytically Detachable Coils have received approval from the NMPA, CE certification, and registration approvals in Brazil, Indonesia, and Ecuador. Additionally, the Presgo® Mechanically Detachable Coils and Presgo® Microguidewires have obtained NMPA approval, CE certification, and registration approval in Brazil. Furthermore, the Presgo® Microcatheter has also secured registration approval in Brazil.

Although multiple products of Peijia Medical have received approval abroad, all of its revenue in 2020 came from China. It is expected that Peijia Medical will actively expand in the future.Brazil, Europe, etc.Overseas Markets.

From a revenue perspective, Peijia Medical’s neurointerventional business ranks second among domestic manufacturers. This is attributable to its early market entry and rapid R&D progress, with eight neurointerventional products launched for commercial sale in 2020. Although Peijia Medical has not disclosed the number of hospitals it covers, its revenue figures indicate that it necessarily serves a substantial number of core hospitals.

Another distinguishing feature of Peijia Medical is its emphasis on research and development (R&D). According to the annual report, its R&D expenditure in the neurointerventional field increased from RMB 22.91 million in 2019 to RMB 46.08 million in 2020. The substantial rise in R&D spending was primarily attributable to three factors: first, the consolidated R&D expenses of the neurointerventional business acquired in 2019 were included in Peijia Medical’s 2019 consolidated financial statements; second, employee costs increased; and third, the company continued to invest in R&D projects.

Driven by increased R&D investment, its product portfolio has achieved breakthroughs: three products—the Heralder® distal access guiding catheter, the Tethys® AS thrombectomy aspiration catheter, and the Jasper® ultra-soft electrolytically detachable coils—are currently in the regulatory submission phase, while the Shenyi® stent retriever is nearing completion of its clinical trials.

In addition, Peijia Medical’s annual report indicates that its SacEase® balloon microcatheter, Fluxcap® balloon guiding catheter, heat-detachable coils, and NeuroStellar® intracranial stent are all in the design phase. This also suggests that Peijia Medical will continue to invest in product research and development in the future.

Perhaps Peijia Medical’s future competitive advantages will lie in its R&D-driven comprehensive product pipeline and its marketing-centric global market promotion capabilities.

In 2020, the total revenue from neurointerventional devices at GuiChuang Tongqiao reached RMB 19.94 million, primarily driven by sales of its core products, the Jiaolong Intracranial Thrombectomy Stent and intracranial support catheters. The gross profit margin for its neurointerventional devices was 69.3%. Previously, as these neurointerventional devices had not yet been launched for commercial sale, they generated no revenue.

As can be seen, although ZendoVascular launched only two products in 2020, it already generated nearly RMB 20 million in revenue. This is because ZendoVascular invested heavily in marketing and promotion, and its team possesses experience in successfully commercializing seven interventional medical device products, giving it a competitive advantage in market promotion.

Benefiting from Zhenchuang Tongqiao’s financial support, network resources, and promotional expertise, the company has, to date, established a distribution network in collaboration with 17 domestic distributors, covering more than 1,000 hospitals across 22 provinces, four autonomous regions, and four municipalities directly under the Central Government in China. Additionally, it has partnered with eight overseas distributors to market its products in countries such as France, Poland, and Turkey.

Based on ZC Medical’s product portfolio, the company has a total of 21 neurointerventional device products. Currently, 12 of ZC Medical’s neurointerventional products are in clinical trials or registration stages, with market launch expected within the next two to three years. Additionally, ZC Medical anticipates that 19 of its neurointerventional products will receive regulatory approval for market launch by the end of 2025. Beyond the domestic market, ZC Medical is also expanding into overseas markets; for instance, its flagship product, the Jiaolong Intracranial Thrombectomy Stent, has obtained CE certification in Europe.

According to the prospectus of Genesis MedTech, its R&D expenditure was RMB 53 million in 2019 and RMB 72.1 million in 2020, accounting for 1,078.5% and 260.8% of its total revenue, respectively. Based on Genesis MedTech’s product pipeline layout and R&D investment, it is evident that the company will continue to allocate substantial funds to research and development in the future to achieve a comprehensive portfolio of neurointerventional products, thereby gaining a competitive advantage.

It is reasonable to expect that, leveraging its robust marketing capabilities and a pipeline of multiple products nearing market launch, Zuochuang Tongqiao will have significant growth opportunities.

According to the prospectus of Perfy Medical, Perfy Medical generated revenue of RMB 7.293 million in the first nine months of 2020, with all income derived from its neurointerventional product, SupSele.TMMicrocatheters and ExtraFlexTMDistal access catheters, with a gross profit margin of 41.1%. This is because Mindray Medical’s neurointerventional products were launched late, with sales and promotion only beginning in the first quarter of 2020. Another reason is the limited number of marketed products, with only microcatheters and distal access catheters currently available for sale.

In the first nine months of 2020, CereVasc Medical invested RMB 20 million in the research and development of neurointerventional technologies, resulting in a loss of RMB 67.745 million. However, CereVasc Medical’s self-developed product, CaptorTMThrombectomy Devices, FullblockTMThe occlusion balloon catheter was approved by the NMPA in August and December 2020, respectively, and CaptorTMThe thrombectomy device was launched for sale in December 2020, while FullblockTMOcclusion balloon catheters are poised for large-scale production and sales.

In addition, Mindray Medical's core products, including thrombectomy devices and left atrial appendage occluders, have achieved breakthroughs, with an additional 19 products in development scheduled for successive launches.

From the perspectives of product approval, product quality, and market promotion, 2021 may be a year of significant performance growth for Perfy Medical. According to Perfy Medical’s prospectus, the company expects to launch nine neurointerventional products in 2021. In terms of product quality, CaptorTMThe thrombectomy device demonstrates non-inferiority in safety and efficacy compared to Medtronic’s flow restoration devices. In terms of market promotion, Xinwei Medical has established a distribution network in collaboration with 27 distributors, covering more than 800 hospitals across over 20 provinces and municipalities in China.

Overall, MicroPort is currently enjoying first-mover advantages with its global market presence, yet it faces the threat of intense competition. Peijia Medical has a large number of commercialized products and a robust pipeline of products under development, requiring time to mature and unlock its full potential. Both JetMed and HeartCare Medical have comprehensive product portfolios; however, their current number of commercialized products is limited. A significant wave of their products is expected to launch over the next two to three years, significantly impacting China’s neurointerventional market.

It can be said that while each of the four companies possesses its own unique advantages, they all converge on the same outcome: future leading enterprises in neurointervention will inevitably be characterized by “a robust product pipeline, superior product quality, and strong marketing capabilities.”

In terms of product portfolios, Peijia Medical, Acotec Scientific, and HeartCare Medical have all adopted a comprehensive lineup of neurointerventional products.

From the corporate perspective, a comprehensive product portfolio can reduce surgical risks associated with switching between products from different manufacturers, thereby further improving clinical outcomes; facilitate more efficient supply chain management and postoperative monitoring for hospitals; and enable more flexible pricing strategies to respond to market competition.

On the other hand, a comprehensive product portfolio also demonstrates that companies with deep insights into the intricacies of neurointerventional products have the confidence to develop related offerings leveraging their innovation and R&D capabilities. An analysis of the strategic layouts of the aforementioned four companies reveals similarities in their neurointerventional product portfolios, which indirectly suggests that an increasing number of startups will develop neurointerventional-related products. In this context, the current comprehensive product portfolios of these companies will enhance their ability to compete in the market.

However, it is important to recognize that the ultimate winners in market competition are most likely those with superior product quality. Therefore, while deploying comprehensive product portfolios, enterprises should also prioritize technological and product innovation to compete on quality.

Another commonality among MicroPort, Peijia Medical, Genesis MedTech, and Xingwei Medical lies in their global expansion strategies.

MicroPort Scientific obtained registration certificates for six neurointerventional products in four overseas countries in 2020, and is poised to launch global marketing efforts.

Peijia Medical’s intracranial electrolytically detachable coils have obtained CE certification and registration approvals in Brazil, Indonesia, and Ecuador; its mechanically detachable coils and micro-guidewires have obtained CE certification and registration approval in Brazil; its microcatheters have obtained registration approval in Brazil, with market expansion into Europe and Brazil imminent.

Zhuangchuang Tongqiao’s core product, the Jiaolong Intracranial Thrombectomy Stent, has also obtained European CE certification. Meanwhile, Zhuangchuang Tongqiao has established partnerships with overseas distributors, collaborating with seven distributors in 2019 and eight in 2020, with products primarily exported to countries such as France, Poland, and Turkey.

Captor is currently planning to apply for registration with the U.S. FDA by Braincare Medical.TMThrombectomy Devices.

From this perspective, Peijia Medical and Genesis MedTech have made the most rapid progress in their global expansion, while MicroPort Medical is more likely to leverage its resource advantages to facilitate the internationalization of its neurointerventional products. In contrast to these three companies, HeartCare Medical has adopted a steady and prudent strategy, first solidifying its foundation in the domestic market before gradually expanding into overseas markets.

Chinese neurointerventional companies are expanding globally, with a high likelihood of breaking into the global market by leveraging their cost advantages. Given superior product quality, domestically produced neurointerventional devices from China, which offer lower costs, are undoubtedly more competitive. Furthermore, in the face of pressure from centralized procurement, competing in the global market presents a better option for enhancing profits and increasing revenue.

Based on the strategic layouts of the four leading enterprises, the future growth trajectory for China’s neurointerventional companies will involve establishing comprehensive product portfolios across the entire neurointerventional spectrum and actively participating in global competition.

Witnessing the bold strategic moves of neurointerventional companies at this stage, veteran medical device professionals might well be moved to tears. Proactively mitigating risks and engaging in global competition signify:The era of China’s domestically produced medical device industry, once characterized by weak R&D capabilities and insufficient innovation, is fading into the past, while a new era defined by robust R&D and high innovation capacity is striding forward with confidence!