Hillhouse and OrbiMed's Long-Term Bet on the Next $100B Aesthetic Consumer Healthcare Blue Ocean: Invisible Orthodontics

This article firstPublished by: Gazelle Club, Author:Kris Little Gazelle,Authorized for republication by VCBeat.

In today’s era, niche industries associated with “enhancing beauty” are destined to become “remarkable” sectors.

Amidst the fierce competition across numerous medical aesthetics sectors, where products and surgical procedures can improve skin quality, augment the nose, create double eyelids, or perform bone contouring, the one area that remains beyond their reach is: teeth.

The aesthetic appeal of one’s teeth significantly influences overall facial attractiveness. Misaligned or irregular teeth often compromise facial harmony. Given the close anatomical and functional relationship between the lips and teeth, dental morphology inevitably affects the appearance of the mouth, thereby diminishing perceived attractiveness.

Orthodontics is poised to become the next major growth sector, with “aesthetically pleasing, elegant” clear aligner therapy emerging as the standout opportunity within this trend.

Orthodontics fulfills most investors’ fantasy of a “prime sector,” being pure consumer healthcare, with a high industry ceiling, double-digit CAGR, and low penetration rate.

1. Pure consumer healthcare, free from policy constraints

The dental care sector comprises numerous specialized fields, with primary services including dental implants, orthodontics, prosthodontics, oral surgery, periodontics, and endodontics. Fees for consultation, examination, anesthesia, medications, and materials are charged separately for each service as applicable. Medical insurance typically reimburses only the costs of basic materials and treatment. In dental practice, medical insurance generally covers only restorative procedures (including basic materials and treatment fees), tooth extractions, and treatments for periodontal diseases such as periodontitis and gingivitis. Procedures related to cosmetic dentistry are largely excluded from coverage, including teeth cleaning, orthodontic treatment, and dental implants, primarily due to the high cost of materials involved.

"This is a sector excluded from national medical insurance coverage, fully self-paid, with stronger consumer attributes."

2. At least 3 times the space

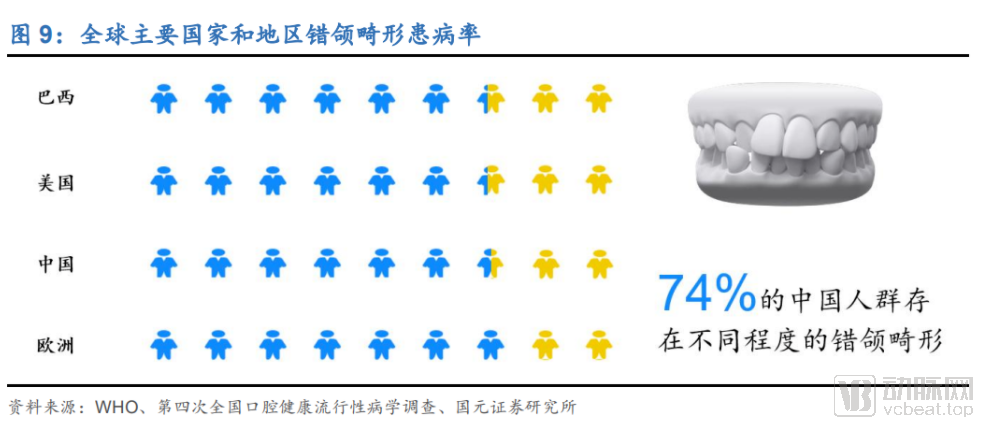

● Large patient population and vast market: According to surveys, the prevalence of malocclusion in China is as high as 74%, corresponding to approximately 1.036 billion individuals affected by malocclusion. The high prevalence rate of malocclusion in China indicates a particularly large potential patient base.

China’s orthodontics market has experienced rapid growth in recent years. According to Frost & Sullivan, the market size (based on terminal retail sales) surged from USD 3.4 billion in 2015 to USD 7.3 billion in 2019, representing a compound annual growth rate (CAGR) of 20.7%. Over the next decade, China’s orthodontics market is projected to maintain a CAGR of 14%, with its scale expected to reach approximately RMB 200 billion by 2030.

● Low penetration of clear aligner orthodontics in China presents significant growth potential: According to Frost & Sullivan data, the number of orthodontic cases in China increased from 1.6 million in 2015 to 2.9 million in 2019, representing a CAGR of 15.3%. Among these, clear aligner cases rose from 47,800 in 2015 to 303,900 in 2019, with a CAGR of 58.8%, indicating rapid growth in both the clear aligner industry and consumer acceptance.

In 2019, among the 2.9 million malocclusion cases treated in China, only 10.5% utilized clear aligners, whereas in the United States, 33.1% of the 4.5 million treated cases employed this technology. The substantial disparity in clear aligner penetration rates between China and the U.S. has highlighted the significant investment potential within the clear orthodontics industry.

3. The Core of the Core: Sectors That Truly Enhance Beauty

The starting point and original intention of any medical intervention are to benefit the patient.

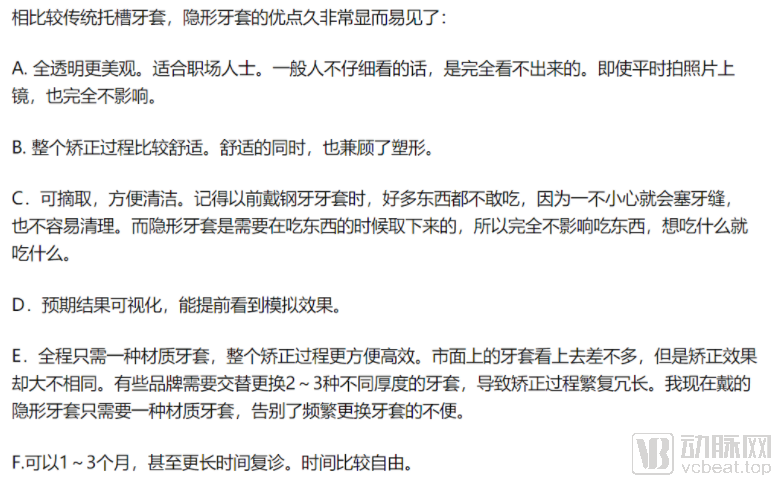

Advantages of Clear Aligners Over Traditional Braces: Selected Real User Experiences from Our Survey (See Figure Below).

Although clear aligner orthodontics is not exclusive to women, in today’s era where the “appearance economy” thrives and disposable income per capita continues to rise, market segments that tangibly enhance individuals’ aesthetic appeal are poised for significant growth. Below, we present selected before-and-after facial images of patients from a dental hospital’s clear aligner orthodontic case studies.

Looking at the overseas market, we have already seen well-known companies in the field of dental devices and consumables, such as Dentsply Sirona, Align Technology, Envista, and Straumann.

With its vast demand, growth potential, and advantages in industrial chain integration, the Chinese market is destined to give rise to industry giants.

The optimal investment strategy in the clear aligner industry chain is not to focus on the upstream, midstream, or downstream sectors individually, but rather to invest in the leading clear aligner manufacturers that span both the upstream and midstream segments.

Upstream – Aligner Film Materials: Aligner films (polymer plastic sheets) are a critical material for the production of clear aligners, accounting for approximately 20% of the total manufacturing cost. Currently, nearly 90% of clear aligner manufacturers source their film raw materials from two German suppliers, Scheu-Dental and Erkodent, before proceeding with the manufacturing of clear aligners.

The development of clear aligners in China has been relatively short-lived, with only a few leading manufacturers, such as Angelalign, Invisalign, Smartee, and Tongce Yinxiu, developing raw material films. The upstream film market is monopolized, and price fluctuations will affect midstream clear aligner manufacturers, weakening their bargaining power and impacting profits.

Upstream—Equipment: Upstream equipment includes intraoral scanners, vacuum forming machines, cutting machines, and 3D printers. Due to the entry of an increasing number of domestic manufacturers and technological breakthroughs in recent years, competition in the equipment segment has intensified, resulting in generally low bargaining power for upstream equipment suppliers against midstream clear aligner manufacturers.

For instance, intraoral scanners used for 3D imaging of tooth surfaces: the domestic brand Langcheng, which launched its product earlier, quoted a price of over RMB 200,000 in 2017, but the current price has fallen below RMB 100,000. According to the management of Meiya Optoelectronic, a Chinese listed company, intraoral scanners are no longer considered high-value equipment. Similarly, in the 3D printer market, well-known Chinese companies such as UnionTech, ZRapid, and Creality Drive have seen their product prices continuously driven down by intense market competition.

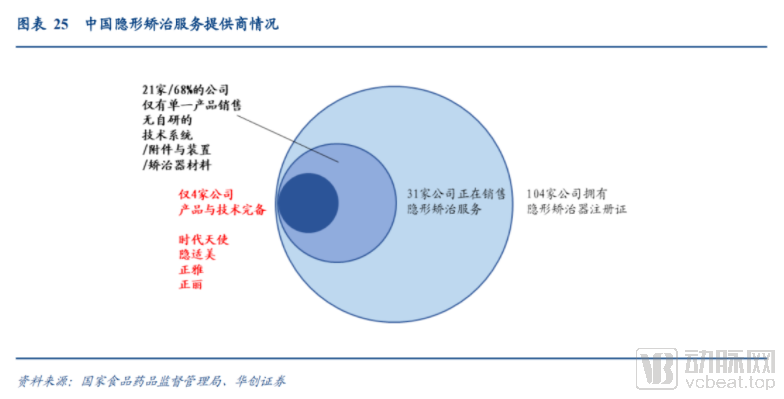

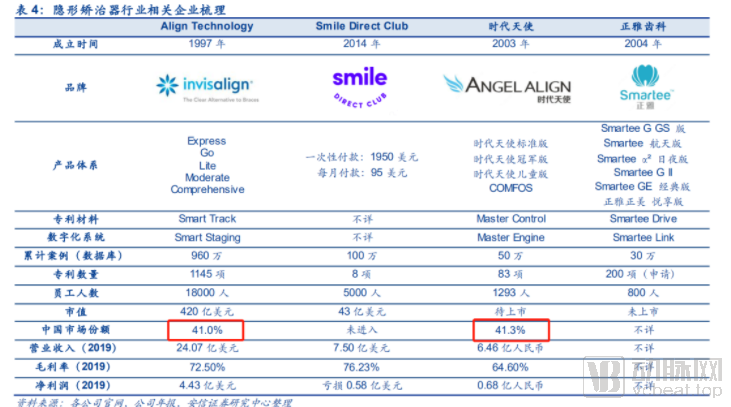

Midstream – Clear Aligners: At first glance, the midstream segment does not appear to offer the optimal investment opportunity; however, certain industry leaders have carved out a path toward an optimal solution. Currently, there are 104 manufacturers in China holding registration certificates for clear aligners, of which only 31 are actively selling clear aligner treatment services. In reality, most of these companies offer only a single aligner product. Only five companies currently possess comprehensive clear aligner products and technologies: Angelalign, Invisalign, Smartee, Topchoice Dental, and Zhengli Orthodontics.

Clear aligner manufacturers maintain profit margins of approximately 40%, with upstream thermoplastic sheet materials accounting for around 20% of total production costs, and R&D expenses for product upgrades comprising roughly 7%. Other costs include labor and supply chain integration. Upstream manufacturers are constrained by price fluctuations from material suppliers, and the entry of powerful new competitors such as Topchoice has begun to erode their bargaining power over downstream clinics. However, leading manufacturers that have broken through upstream bottlenecks have demonstrated remarkable resilience, delivering performance results that have earned market confidence.

Among them, the gross profit margins of the two industry leaders have drawn significant market attention. Align Technology shipped over one million units globally in 2018, achieving a gross profit margin exceeding 70% and a net profit margin above 18%. Angelalign’s gross profit margin for the first nine months of 2020 was 70.8%, with its net profit margin also surpassing 18%.

Downstream – Dental Chain Clinics: As we mentioned in yesterday’s article, “Ge Lan Aggressively Increases Holdings in Q1! ‘The Maotai of Dentistry’ Reports Its Worst Annual Results—Is It Time to Buy the Dip?”, domestic dental service chains in China are grappling with challenges in physician recruitment, patient acquisition, and profitability. Even the industry benchmark, Topchoice Medical, faces a growth ceiling due to difficulties in expanding competitively across provinces. Meanwhile, a review of overseas markets has not identified any comparable benchmark enterprises in the dental services chain sector.

Why is it said that Topchoice Medical must clash with Invisalign and Angelalign? Or rather, the war has already begun.

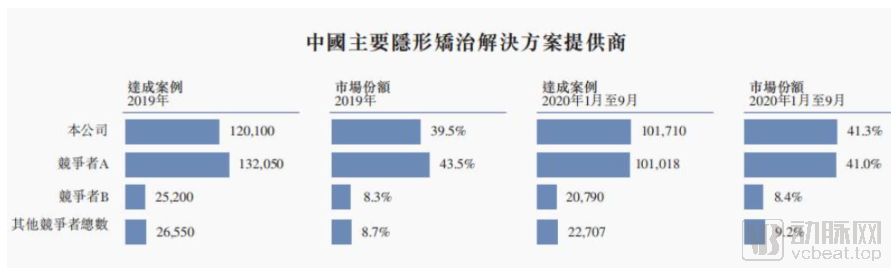

▲ Competitive Landscape in Angelalign’s Prospectus

In the global market, Invisalign has secured the industry’s top position with a cumulative total of 9.6 million completed clear aligner cases. Meanwhile, the domestic market in China features a relatively concentrated competitive landscape. According to data from Frost & Sullivan, Invisalign and Angelalign hold market shares of 41.0% and 41.3%, respectively, while the third-ranked player, Smartee, accounts for only around 8%.

Facing this trillion-yuan market, dental chain giant Topchoice has long set its sights on it.

This is also quite normal, as Topchoice Medical possesses its own unique advantages in both products and channels.

As early as six years ago, Topchoice Medical’s clear aligner brand, “Yinxiu,” began its research and development efforts. It has now established its own aligner production line, proprietary medical platform, and second-generation chairside printing technology, and will further reduce its reliance on assistance from clear aligner manufacturers in the future.

For years, Invisalign and AngelAlign have leveraged their proprietary aligner film technologies to deliver a superior wearing experience—particularly in terms of comfort with rigid aligners—setting them apart as a distinct tier above other domestic brands that rely on materials from Scheu Dental and Adent.

TopChoice Medical has also invested significant effort in the R&D of aligner materials. During a recent investor survey, management stated, “We currently have self-developed single-layer and double-layer aligner materials and no longer use materials from Germany’s Scheu Dental. Our materials offer superior flexibility and overall performance compared to Angelalign. Our single-layer aligners may be slightly stiffer than Invisalign’s material but softer than Angelalign’s. From root movement control to AI applications, we hold a certain lead over Angelalign.”

Beyond the technical and product differences that can be explained by patient wearing experience, the second core factor is channel coverage.

Topchoice Medical’s “Orthodontic Whirlwind Plan” has been fully rolled out across its affiliated hospitals. The company is deliberately strengthening the operation of its orthodontics segment to drive volume growth for its “Yinxiu” brand. Although the number of Topchoice-affiliated hospitals open in 2021 is expected to reach 70—a modest channel scale—this is not its core competitive advantage. What truly sets it apart is the combination of “physician resources + equity linkages.”

Hangzhou Yiyi (the entity behind Yinxiu) has formulated a robust equity incentive plan, with Topchoice Medical aiming to make Yiyi a company owned by dentists across China. Under this plan, equity is granted based on the number of Yinxiu cases performed by each dentist. The first batch of stock options has already been issued, with over 1,000 dentists who have previously conducted Yinxiu procedures receiving their grants. Looking ahead, the company aims to extend equity ownership to 100,000 dentists.

The charge led by Topchoice Yinxiumei against the two clear aligner giants, Invisalign and Angelalign, has begun.

The Future: A New King Ascends, or the Old Guard Prevails?

Angelalign’s Hong Kong IPO is also poised for launch. As the only pure-play listed company in clear aligner orthodontics, backed by Shuangbai Investment (with Hillhouse Capital as an LP) as a major shareholder and OrbiMed’s long-term strategic positioning since 2010, we believe investor expectations will be fully priced in at the moment of listing. After all, this sector sits at the intersection of “beauty” and “intelligence” within consumer healthcare.