Hengrui Pharma & Hansoh Pharma: Strategic Evolution and Pipeline Update Amid $100B+ Combined Market Cap

This article firstPublished by: Yao Shi Zong Heng, Author: Tao Ge from the Pharmaceutical Circle,Authorized for republication by VCBeat.

As a leading force in China’s pharmaceutical innovation, the Hengrui group has consistently remained in the spotlight. In recent years, Big Pharma companies like Hengrui have not only had to grapple with multinational pharmaceutical giants in international markets but also face intense competition from hundreds of biotech firms domestically. Despite significant pressures, they have maintained strategic focus and stability.

Although there is ample room for innovation and fast-follow development in novel drugs, most biotech companies fail to differentiate themselves through inadequate preclinical research or undifferentiated pipeline strategies. Relying entirely on capital market financing without sustainable internal revenue generation, they risk being held captive by investors, pursuing fast-follow strategies driven merely by commercial maneuvering. Against the backdrop of centralized volume-based procurement, competing head-on with powerful Big Pharma players, their fate may well be sealed: drifting further away from leading peers in the same therapeutic areas, such as Hengrui, Qilu, CSPC, Chia Tai Tianqing, and Hansoh. While a select few outstanding biotechs will undoubtedly emerge, the majority are likely to resemble meteors streaking across the night sky, with becoming enduring stars remaining an elusive dream.

Looking back, the Hengrui group has long proven its strategic vision, corporate management capabilities, and the founder’s resilience and pragmatism, sustaining continuous development through internal cash flow generation. Let us first examine Hansoh Pharmaceutical, known as “...”

Some companies are born with inherent flaws, but Hansoh Pharmaceutical replicated the Hengrui DNA from its inception. Hansoh Pharmaceutical was incorporated in the Cayman Islands (a British Overseas Territory) in December 2015 and listed in Hong Kong in 2019. In 1995, Jiangsu Hansoh, the primary operating subsidiary of Hansoh Pharmaceutical, was established in China. The founder and actual controller of Hansoh, Ms. Zhong Huijuan, is married to Mr. Sun Piaoyang, the actual controller of Hengrui Medicine.

Although Hansoh shares genetic ties with Hengrui, it is ultimately distinct from Hengrui. By differentiating itself from Hengrui to avoid direct competition and leveraging its own strategic layout, Hansoh has achieved growth. Like Hengrui, Hansoh initially started with generic drugs, and in recent years, its innovative drug pipeline has begun to yield results. Hengrui Pharmaceutical’s main business segments include oncology, anesthesia, and contrast agents. In contrast, Hansoh focuses on oncology drugs, central nervous system (CNS) drugs, anti-infective agents, and diabetes treatments. The company reported revenues of RMB 8.69 billion and net profits of RMB 2.569 billion in 2020, representing year-on-year increases of 0.1% and 0.5%, respectively. The revenue contribution from new products rose from 6.1% in 2019 to 23.7% in 2020.

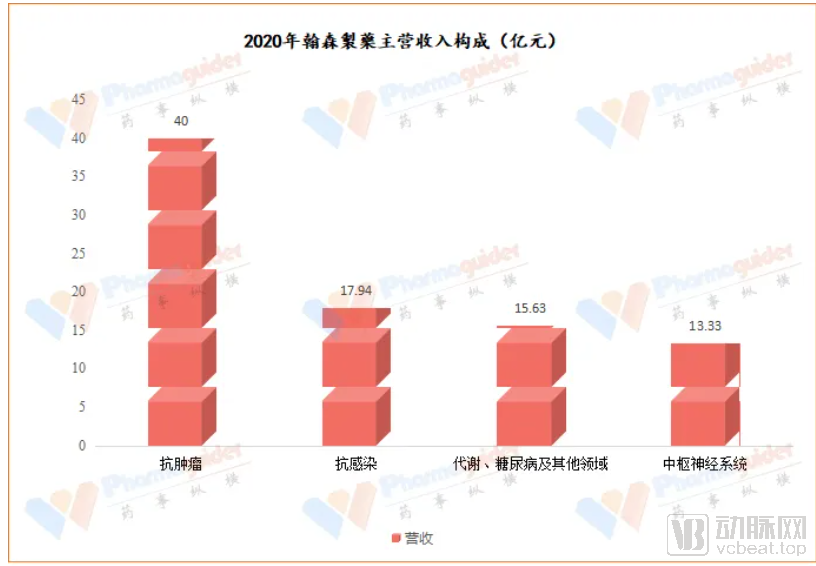

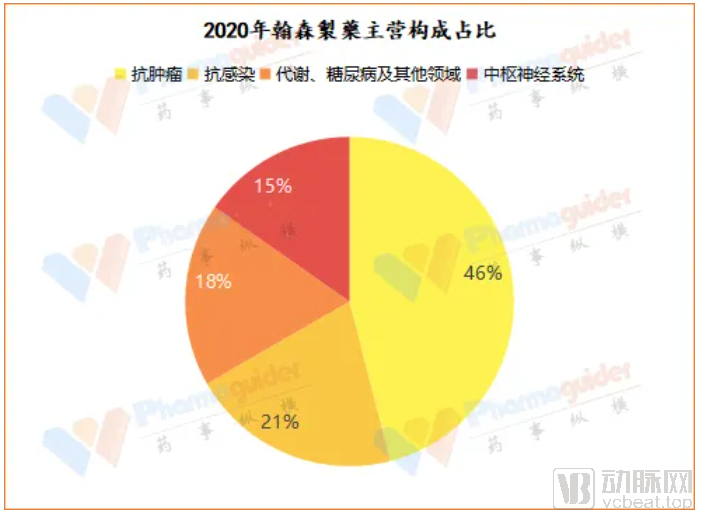

Business Composition

Data Source: Hansoh Pharmaceutical Annual Report; Chart by Yaoshi Zongheng

In 2020, the company’s oncology drug revenue reached RMB 4 billion, accounting for 46% of total revenue. This performance was primarily driven by the rapid sales ramp-up of the blockbuster new drug Almonertinib, which substantially offset the impact of Pemetrexed’s inclusion in the volume-based procurement program. The R&D team expanded to over 1,600 members, with R&D expenditures totaling RMB 1.25 billion, representing an 11.7% year-on-year increase and accounting for 14.4% of total revenue.

Source: Hansoh Pharmaceutical Annual Report; Chart by Yaoshi Zongheng

Hansoh has established a comprehensive R&D platform and mastered a portfolio of proprietary technologies by continuously increasing its investment in research and development (R&D) year over year. The company has successfully launched a series of innovative drugs and first-to-market generics, while maintaining a robust pipeline of candidates in development. Currently, Hansoh has more than 100 projects in its R&D pipeline, among which three Class 1 innovative drugs—HS-10352 tablets, HS-10353 capsules, and HS-10356 tablets—and one Class 2 biological innovative drug, HS-20090 injection, have received approval for clinical trials.

In 2020, the Company had a total of 10 new drugs approved for marketing domestically and internationally, including its independently developed innovative drug Ameile (Almonertinib Mesylate Tablets), the Class 2.2 innovative drug “Olanzapine Orally Disintegrating Film,” and three first-to-file generic drugs. The Company submitted 18 new clinical trial applications and obtained clinical trial approvals, and filed 23 new drug applications (NDAs), including its independently developed Class 1.1 new drug “Aimeifenfu Tenofovir Tablets” and the licensed-in biologic innovative drug project, the CD19 monoclonal antibody Inebilizumab Injection. The CD19 monoclonal antibody is expected to be approved for marketing in the second half of this year.

Image source: Hansoh Pharmaceutical official website

The company projects that its flagship anti-tumor product, Almonertinib (Ameile), will achieve RMB 5 billion in sales within three years of being included in the National Reimbursement Drug List. The independently developed innovative drug, Aimefu Tenofovir Alafenamide Tablets, has submitted a New Drug Application (NDA) and received priority review status, with acceptance by the National Medical Products Administration (NMPA) in September 2020. This product is indicated for the treatment of chronic hepatitis B, offering improved efficacy and significantly reduced toxicity and side effects compared to the previous-generation drug Tenofovir Disoproxil Fumarate (TDF).

Key Focus Areas for Future Business Development (BD) and R&D: Concentrating on Hansoh’s areas of strength to strengthen the pipeline. With a patient-centric approach, we will focus on unmet clinical needs specific to China, developing new products in-house or through in-licensing. BD and internal R&D will work synergistically, with BD serving as a complement, while our internal R&D capabilities facilitate the advancement of BD projects. In addition to internal R&D investment, we are actively seeking external opportunities for in-licensing and acquisitions to enhance our pipeline. For example, in April 2020, the Company entered into a collaboration with NiKang Therapeutics to in-license a preclinical innovative antiviral drug project. This move will enrich the Company’s portfolio in the field of anti-infectives within the Greater China region.

Focus on High-Potential Candidates: From an innovation perspective, Hansoh Pharmaceutical prioritizes high-potential candidates, whether through in-house R&D or in-licensing. Its new product pipeline primarily comprises four innovative drugs and more than ten products launched within the past three years. These products span four major therapeutic categories, with oncology agents constituting the core focus.

Initiating Global Development: The company boasts a robust R&D team, an efficient clinical development team, and a mature sales system. In addition to its interest in product in-licensing and development, the company places significant emphasis on platform construction and empowerment. It possesses not only the capability to introduce external products into the market but also the capacity to expand its own products globally. We aim to initiate global development at an earlier stage. For instance, last July, through a strategic collaboration with EQRx, both parties agreed to jointly promote the overseas launch of almonertinib, a third-generation EGFR-TKI. This deal included a $100 million upfront payment along with regulatory and development milestone payments. Almonertinib is a third-generation epidermal growth factor receptor tyrosine kinase inhibitor (EGFR-TKI) developed by Hansoh Pharmaceutical. It was approved for marketing in China last March for the treatment of patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) who have progressed after prior EGFR-TKI therapy and test positive for the T790M mutation.

Biologics as a Key Future Growth Direction: The company places significant emphasis on the research and development (R&D) of large-molecule drugs, positioning biologics as a strategic priority for future growth. Hansoh Pharmaceutical began laying the groundwork for the R&D and manufacturing of biologics three years ago. Currently, its Shanghai Biologics R&D Center has been completed and is operational, while the manufacturing facility in Changzhou is under construction, with trial production expected to commence in the third quarter of this year. Regarding the product pipeline, HS-20090 is currently undergoing Phase I clinical trials, with Phase III studies anticipated to launch in the second half of this year. Additionally, two other biologic candidates, including an antibody-drug conjugate (ADC) project, have submitted Investigational New Drug (IND) applications. For the CD19 monoclonal antibody program, which initially received approval for the indication of neuromyelitis optica spectrum disorder (NMOSD), the company will actively collaborate with U.S. partners to expand research into additional indications.

Hansoh and Viela Bio, Inc. have submitted a Biologics License Application (BLA) for “Inebilizumab Injection,” which they are jointly developing and commercializing in China; the application was accepted by the National Medical Products Administration (NMPA) in October 2020. This product, which features a novel mechanism of action for the treatment of neuromyelitis optica spectrum disorders (NMOSD), was approved for marketing by the U.S. FDA in June 2020.

2021 Highlights: The company plans to submit 8–10 Investigational New Drug (IND) applications for innovative drugs annually, with 1–3 launched on the market.

1. HS-10234 is expected to be approved for launch in the first half of this year, with the potential to participate in this year’s National Reimbursement Drug List (NRDL) negotiations. Given the large population of hepatitis B patients in China, it has the potential to become a blockbuster drug with peak sales of RMB 2 billion.

2. The CD19 monoclonal antibody is expected to be approved for market launch in the second half of this year. Currently, one of its approved indications is NMOSD, which falls within the central nervous system therapeutic area.

3. Peihua Xihaimitide, with the NDA application expected to be submitted in the second half of 2021.

Summary: Hansoh’s strategy primarily relies on its internal cash-generating capabilities, with continued increased R&D investment in the oncology field. It adopts a synergistic approach combining business development (BD) and in-house research, enriching its pipeline through internal development, licensing-in, and acquisitions. In other generic drug sectors, it differentiates itself from leading players while identifying high-potential products. Additionally, Hansoh has launched global R&D initiatives, positioning biologics as a key future growth direction.

As a Chinese Big Pharma, Hengrui Medicine carries its own prestige and commands a strong presence. The case of PD-1 amply demonstrates that latecomers can surpass the pioneers. As a well-known blue-chip stock, we will skip over its basic fundamentals and focus instead on its product portfolio and future development strategy.

Against the backdrop of centralized volume-based procurement (VBP), small and medium-sized pharmaceutical companies are struggling, and Big Pharma is no exception; under intense pressure, the largest players bear the brunt. Hengrui Medicine is currently at a juncture where only its oncology portfolio is experiencing rapid growth, while its traditional business faces downward pressure. The company aims to mitigate the decline in its traditional business through internal strategic realignment, prioritizing innovation and internationalization as its core development strategies.

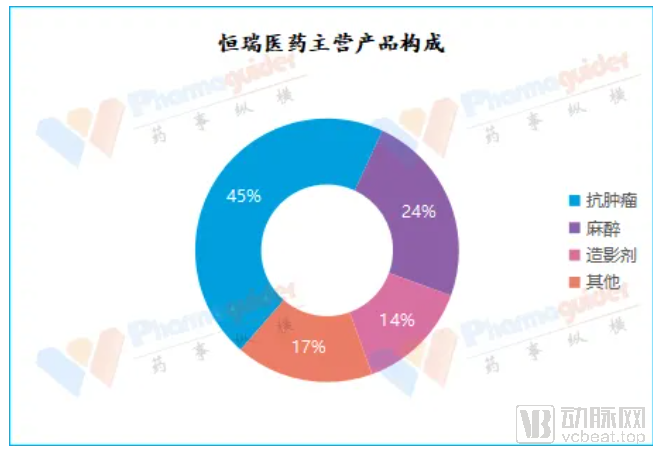

Source: Hengrui Financial Reports; Chart by Yaoshi Zongheng

“Four Verticals and One Horizontal” Business Unit Structure: In the past two years, the company has established business units for Oncology, Medical Imaging, Anesthesiology, and General Products, as well as a Strategic Development Business Unit responsible for market access, public affairs, international exchanges, and industry-academia-research collaboration. The company has strengthened its medical affairs system and academic marketing team, emphasized strategic cooperation and resource integration, accelerated the transition from old to new growth drivers and the promotion of innovative drugs, and expedited its layout in the OTC market, the third terminal market, and county-level markets.

R&D Team Structure: The company currently has approximately 4,000 R&D personnel, including 1,000 at the Lianyungang Research Institute, 1,000 in Minhang, Shanghai, and another 2,000 dedicated to clinical operations. The establishment of an overseas clinical team has been prioritized. Last year, the company set up its own R&D teams in New Jersey, USA, and Switzerland, Europe, with a total overseas staff of around 50 (30 in the US and 20 in Europe). The company aims to expand this overseas team to 100 members this year, with the goal of conducting future clinical trials using its in-house team. Zhang Lianshan, Vice General Manager and also Global President of R&D, oversees the company’s entire R&D pipeline, with a primary focus on oncology. Clinical R&D Department II mainly focuses on anesthetics, contrast agents, and new drugs with improved formulations.

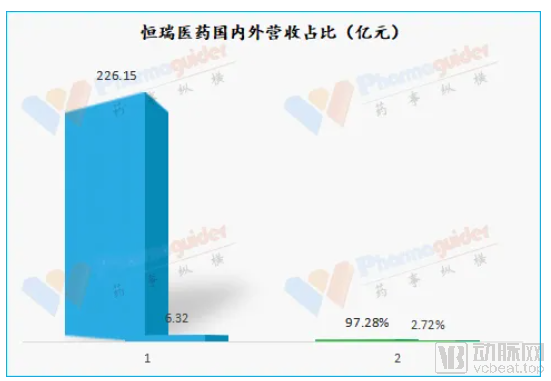

Based on Hengrui’s domestic and international revenue, the 2019 annual report disclosed that overseas revenue accounted for less than 3%. As early as 2009, Hengrui began conducting clinical trials abroad, but none of its products have yet been launched internationally. Previously, the company’s core focus remained on the domestic market, without making substantial efforts to advance globalization. Currently, Hengrui has established an initial presence in China; to achieve greater growth, it must accelerate its internationalization strategy.

In February and March of this year, Hengrui Medicine issued two announcements regarding overseas clinical trials: its PARP inhibitor, fluzoparib capsules, received approval from the U.S. FDA to conduct an international multicenter Phase III clinical trial; and a PD-1 monoclonal antibody-based combination therapy was approved for a Phase II clinical trial in the United States. Additionally, the FDA approved clinical trials for Hengrui’s camrelizumab and famitinib. These developments indirectly reflect the accelerated pace of the company’s internationalization.

Hengrui has prioritized building its clinical teams in the United States and Europe over the past one to two years, relying more on its own workforce by recruiting local professionals. The company is now moving to establish overseas sales teams to advance localization. Currently, 20 generic drug products are being marketed abroad, but no innovative drugs have yet been launched internationally—a key focus for the next three to five years. The overseas clinical team currently comprises several dozen employees, while structured teams for preclinical development and regulatory affairs have not yet been established; these areas will be strengthened in the future.

Source: Hengrui Financial Reports; Chart by Yaoshi Zongheng

Regarding the internationalization of generic drugs: According to the 2020 semi-annual report, Dexmedetomidine Hydrochloride and Sodium Chloride Injection was approved in the United States; the company submitted registration applications to the U.S. FDA for three active pharmaceutical ingredients (APIs), one intermediate, and two finished dosage forms; registration efforts in other emerging markets were also gradually strengthened.

Internationalization of Innovative Drugs: According to the 2020 semi-annual report, the company licensed its proprietary camrelizumab for injection, used in tumor immunotherapy, to South Korea’s CrystalGenomics Inc. for compensation. The company currently has 20 formulated products, including injections, oral preparations, and inhalation anesthetics, approved in Europe, the United States, and Japan, with one formulated product receiving temporary approval in the United States.

BD: Progress was relatively slow last year due to the impact of the pandemic. Hengrui is also undergoing a strategic shift in its business development approach. Previously, the company perceived BD projects as overly expensive; now it recognizes that higher costs are justified by corresponding value. The BD team has currently grown to 20 members. We continue to evaluate product opportunities and plan to acquire competitive products at premium prices in the future, while also considering risk mitigation through capital market instruments.

In the future, we will acquire projects and teams through mergers and acquisitions (M&A) and in-licensing. We may initially make equity investments and integrate them into our portfolio once they demonstrate strong growth and profitability. We are also considering establishing funds with venture capital (VC) and private equity (PE) firms to incubate companies.

Project Initiation: Previously, Hengrui rarely considered international markets during product project initiation. For instance, in the analgesic market, where the largest market is the United States, the company focused solely on the Chinese market. Currently, Hengrui’s product project initiation must take international markets into account. Clinical development or clinical trial designs will adopt separate strategies tailored to the differences between the two markets. This approach is currently being implemented in the therapeutic areas of analgesia and oncology.

R&D: Previously focused on fast-follow strategies and small-molecule drugs, the company can no longer guarantee sustained leadership and must achieve internal strategic balance. Currently, more than half of the pipeline consists of fast-follow (FF) assets; going forward, the company aims to develop first-in-class (FIC) and best-in-class (BIC) therapies, although identifying novel targets remains challenging. The Intelligence Discovery Team monitors global scientific advancements and patent publications. The Exploration Team conducts proof-of-concept studies, with incubation supported by the internal technical team. While there was previously a shortage of accumulated talent, the company is now recruiting disease biologists. Efforts began in 2016–2017, and platforms for bispecific antibodies and antibody-drug conjugates (ADCs) have been established, though they are still in their early stages.

The landscape for innovative drugs has also changed, and Hengrui will evaluate the relationship between R&D investment and output/profit. Previously, the company was at the forefront of target discovery in China, but it has now fallen somewhat behind. Going forward, it will focus on earlier-stage targets to maximize the creativity of its R&D team. On one hand, it will advance internal R&D; on the other, it will consider conducting R&D through newly established subsidiaries or collaborations with other companies (or via equity investments).

Key Product R&D Milestones in 2021:

Hetrombopag, a me-too drug, is already under priority review and, if all goes well, could be approved this year.

CDK4/6: Has reached the Phase III endpoint; if all goes well this year, it may receive approval.

Two diabetes indications; the marketing application for retagliptin phosphate tablets was submitted last June. In late September of last year, the new drug application (NDA) for retagliptin phosphate tablets, a Class 1 innovative drug, was submitted and accepted by the Center for Drug Evaluation (CDE). The product is expected to be launched this year.

Combination of cisplatin and gemcitabine as first-line treatment for nasopharyngeal carcinoma; Hengrui’s PD-1 inhibitor had its sixth indication included in the priority review last year, with market launch expected this year.

PD-1 + Famitinib Granted Breakthrough Therapy Designation;

PD-1 for squamous non-small cell lung cancer and esophageal cancer met clinical endpoints, with marketing application submitted;

2021 Product Line Forecast:

The oncology product line is expected to maintain robust growth. The anesthesia product line will certainly perform significantly better than last year, driven by the effective control of the pandemic and the priority review of the general anesthesia indication for remimazolam tosylate for injection. As for contrast agents, revenue may face pressure this year due to the impact of centralized volume-based procurement. Overall, the full-year performance can be benchmarked against the unlocking targets of the equity incentive plan, which set a baseline annualized growth target of 18%.

In response to new changes in the policy and market environment, Hengrui Medicine has proactively embraced transformation, rapidly adjusting its strategies and directions in business development (BD), project initiation, and R&D. Meanwhile, staying firmly committed to its two core strategies of “innovation” and “internationalization,” the company has sought breakthroughs in key areas and pursued steady, focused growth. In the development of innovative drugs, Hengrui has basically established a virtuous cycle wherein clinical trial applications for innovative drugs are submitted annually, and new innovative drugs are launched every one to two years.

Hansoh Pharmaceutical maintains a high level of R&D investment in the oncology field, closely following Hengrui Medicine, while building a differentiated product portfolio in other therapeutic areas to distinguish itself from Hengrui.

Both companies prioritize innovation investment, strengthen their R&D teams, position themselves at the forefront of cutting-edge developments, enrich their pipelines through a combination of internal and external strategies, and actively advance their internationalization agendas. In the face of new changes, the new development strategies of both large and small Hengrui entities warrant our consideration.