Diabetes Drug Market Heats Up: Eli Lilly and Novo Nordisk Intensify Rivalry as Sanofi Exits; Semaglutide Expands Indications

This article firstPublished on: Sina Medicine, Author: April Chen,Reprinted with authorization from VCBeat.

Driven by lifestyle changes and an accelerating aging process, the global prevalence of type 2 diabetes is on the rise, turning the corresponding therapeutic drug sector into a substantial market. Since 2008, the FDA has required additional evidence demonstrating that type 2 diabetes treatments do not increase the risk of cardiovascular events, necessitating data from larger-scale clinical trials. This requirement has discouraged smaller companies from attempting to enter the diabetes treatment market independently, while industry giants have begun exploring broader indications for diabetes medications.

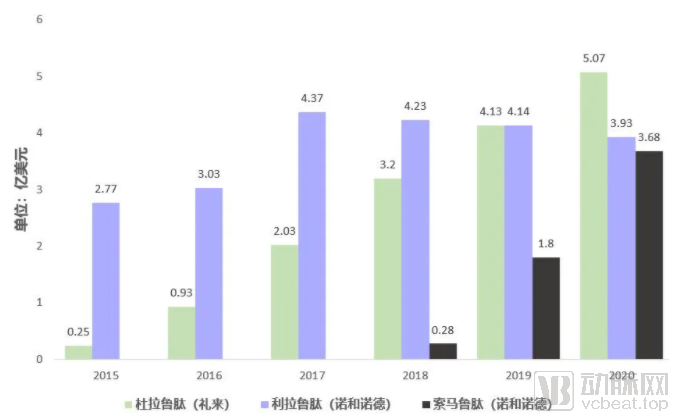

The primary competitors in the GLP-1 receptor agonist sector are Eli Lilly and Novo Nordisk, with their products engaged in intense competition. Eli Lilly’s dulaglutide (brand name Trulicity®), launched in 2014, became a blockbuster drug with annual sales reaching $5 billion within just six years, surpassing Novo Nordisk to become the top-selling GLP-1 medication. Consequently, Novo Nordisk’s single-product performance has temporarily lagged behind that of Eli Lilly. Liraglutide (marketed as Victoza for diabetes and Saxenda for obesity), launched by Novo Nordisk in 2009, was formerly the best-selling GLP-1 drug, peaking at $4.37 billion in sales in 2017. However, 2020 data indicate that this product has entered a period of market decline. In contrast, semaglutide, also from Novo Nordisk (available as the subcutaneous injection Ozempic and the oral formulation Rybelsus), has experienced rapid growth, emerging as another blockbuster drug with $3.72 billion in sales within three years. This medication is available in both injectable and oral formulations.

GLP-1 Drug Sales

Eli Lilly’s next blockbuster product in its type 2 diabetes pipeline is tirzepatide, which has already posed a strong challenge to semaglutide. Unlike GLP-1 receptor agonists, tirzepatide acts as a dual agonist at the receptors for glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1).

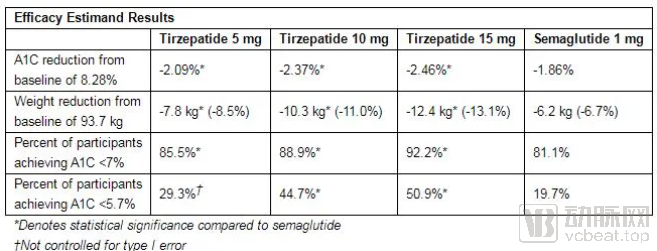

On March 4, 2021, Eli Lilly’s Phase III clinical trial SURPASS-2, which conducted a head-to-head comparison of tirzepatide and semaglutide, achieved success. The reductions in glycated hemoglobin (HbA1c) with tirzepatide at doses of 5 mg, 10 mg, and 15 mg were 2.09%, 2.37%, and 2.46%, respectively, surpassing the 1.86% reduction observed with semaglutide. In terms of weight loss, the three tirzepatide doses resulted in weight reductions of 7.8 kg, 10.3 kg, and 12.4 kg, respectively, exceeding the 6.2 kg reduction seen with semaglutide. The proportion of patients achieving an HbA1c level below 5.7% was also significantly higher with tirzepatide than with semaglutide. Efficacy-wise, tirzepatide demonstrated improved outcomes with increasing doses. Patient non-adherence due to side effects has become a significant issue in diabetes treatment. For instance, although high doses of semaglutide and dulaglutide offer superior efficacy, most patients prefer lower doses. At lower doses, tirzepatide appears to be more effective than semaglutide.

SURPASS-2 Trial Results

All three tested doses of tirzepatide significantly reduced blood glucose levels and body weight. The lowest dose, 5 mg, will be used for the marketing authorization application. Post-launch, it is expected to mitigate the competitive pressure exerted by semaglutide on dulaglutide.

Novo Nordisk’s primary revenue stems from insulin products, including rapid-acting, long-acting, and premixed formulations, followed by GLP-1 medications. However, insulin sales have declined, partly due to price reductions and new U.S. legislation requiring the company to offer larger discounts to Medicare.

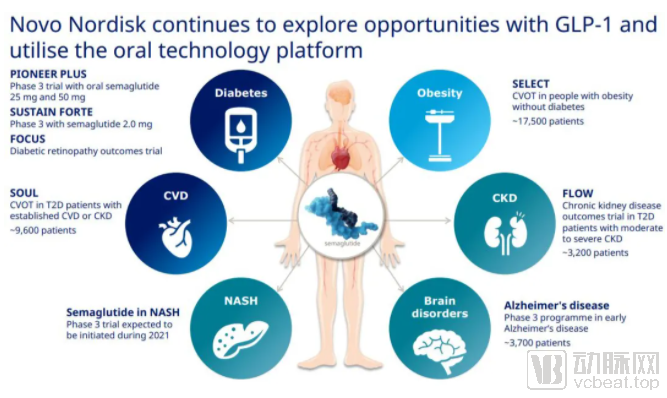

Semaglutide is regarded as the most potent GLP-1 receptor agonist (GLP-1RA), and Novo Nordisk will further explore its greater potential. In early 2020, evidence that both formulations of semaglutide reduce cardiovascular events solidified its position among glucose-lowering agents. At that time, the U.S. Food and Drug Administration (FDA) approved a new indication for Ozempic (subcutaneous semaglutide) to reduce the risk of major adverse cardiovascular events (MACE)—including cardiovascular death, non-fatal myocardial infarction, or non-fatal stroke—in adults with type 2 diabetes mellitus and established cardiovascular disease (CVD). The label for Rybelsus (oral semaglutide) was also updated to reflect cardiovascular risk reduction; the PIONEER 6 cardiovascular outcomes trial demonstrated that Rybelsus significantly reduced the risk of MACE compared with placebo (hazard ratio [HR] 0.79).

Novo Nordisk's GLP-1 Drug Development Program

In addition, in the field of diabetes, the PIONEER series of trials will continue. Among them, PIONEER Plus explores high-dose oral semaglutide at 25 mg and 50 mg once daily (QD), SUSTAIN FORTE explores high-dose injectable semaglutide at 2 mg once weekly (QW), and the FOCUS trial investigates the impact of subcutaneous semaglutide on diabetic retinopathy in patients with type 2 diabetes (T2D).

Broad explorations are also underway for relevant indications. Large-scale clinical trials are being conducted in patients with type 2 diabetes and comorbidities, including the SOUL trial, which enrolls nearly 10,000 patients with type 2 diabetes and cardiovascular events or chronic kidney disease (CKD), and the FLOW trial, which focuses on patients with type 2 diabetes and moderate-to-severe CKD.

For other non-diabetic conditions, the SELECT trial enrolled obese patients without diabetes; a Phase III trial targeting patients with early Alzheimer’s disease is also set to launch, and NASH trials are expected to commence in 2021.

In December 2019, following the appointment of its new CEO, Sanofi announced the discontinuation of research into novel therapies for diabetes and cardiovascular diseases, shifting its focus toward autoimmune disorders and oncology. Historically, the diabetes franchise had been one of Sanofi’s largest business segments, with its flagship product, Lantus (insulin glargine), achieving peak annual sales exceeding $7 billion. However, the company is now compelled to exit this therapeutic area. Sales of Sanofi’s other diabetes medications, lixisenatide and insulin glulisine, appear negligible, leaving Lantus to fend for itself as its market share is gradually eroded. Unfortunately, Sanofi’s competitors in the diabetes space, notably Novo Nordisk and Eli Lilly, have robust pipelines featuring blockbuster new drugs. In contrast, Sanofi not only suffers from a sparse pipeline but has also seen its heavily invested collaborative projects fail entirely. This includes the SGLT1/2 inhibitor Zynquista, co-developed with Lexicon Pharmaceuticals, where collaboration was terminated following the failure of trials aimed at expanding its indications.

2020 Sales of Major Products in the Type 2 Diabetes Field

As evident from the sales rankings, in addition to GLP-1 drugs, the sales of two SGLT-2 inhibitors have increased significantly, thanks to the expansion of their indications for heart failure. In May 2020, AstraZeneca’s dapagliflozin became the first SGLT-2 inhibitor approved for symptomatic chronic heart failure with reduced ejection fraction (HFrEF). This indication was subsequently approved in China in April 2021. Boehringer Ingelheim’s empagliflozin followed closely; in October 2020, Boehringer Ingelheim submitted a registration application to the Chinese National Medical Products Administration for empagliflozin, an SGLT-2 inhibitor under its diabetes alliance portfolio, for the treatment of adult patients with heart failure with reduced ejection fraction, with or without diabetes. This achieved simultaneous regulatory submission and launch alignment with Europe and the United States. For patients with heart failure with preserved ejection fraction (HFpEF, LVEF >49%), who constitute a larger population, no drugs have currently been approved. Treatment typically relies only on symptom relief and off-label use of medications indicated for HFrEF, a challenge that has proven difficult to address. Key clinical trial data for these two drugs in HFpEF are expected to be released in the first half of this year: EMPEROR-Preserved (NCT03057951) for empagliflozin and DELIVER (NCT03619213) for dapagliflozin.