Comprehensive Overview and Product Portfolio of Orthopedic Surgical Robots: Industry Research Report

This article was first published on Siyu Medical Device Observation, authored by Liu Yanzhen, and republished with authorization from VCBeat.

On January 21, 2021, Johnson & Johnson’s DePuy Synthes announced that its orthopedic surgical robot product, VELYS™, had received FDA approval for market launch.

It is reported that this product was developed by the Orthotaxy team, which Johnson & Johnson acquired in 2018. Also launched alongside this product is the ATTUNE Total Knee System for complementary use. This system is the first in its class to feature a portable design, allowing it to be integrated into any operating room environment and positioned beside the surgical table, supporting plug-and-play functionality. The system offers robust planning capabilities, optimizes the surgeon’s workflow, and adapts to individual surgical preferences. VELYS™ assists surgeons in accurately resecting bone during total knee arthroplasty, enabling alignment and positioning of implants relative to soft tissues without requiring preoperative imaging. It eliminates the need for disposable instruments, significantly reducing surgical costs.

(Figure: VELYS™ System)

(Image source: Johnson & Johnson official website)

In the post-pandemic era, research and applications in the field of orthopedic robotics are rapidly maturing. International medical giants such as Johnson & Johnson and Medtronic are accelerating their capture of the medical device market. The regulatory approval and market launch of VELYS™ may help Johnson & Johnson regain a competitive edge in the orthopedic surgical robot market. It is foreseeable that competition in the orthopedic surgical robotics sector will intensify in the future.

Orthopedics is one of the earliest fields to adopt surgical robots and remains a focal point for current research and industrialization. The rigid structure of bone makes it particularly suitable for precise robotic positioning and manipulation, while continuous advancements in orthopedic surgical techniques have imposed increasingly stringent requirements on surgical precision. Furthermore, given the extensive use of intraoperative X-ray fluoroscopy in orthopedic procedures, minimizing radiation exposure to both patients and medical staff has become a significant value proposition of robotic applications. In recent years, personalized, precise, and minimally invasive treatment approaches have emerged as key directions in orthopedic surgery, making the application of surgical robot technology, medical imaging technology, and surgical navigation technology prominent areas of research in this field.

Orthopedic robotics is a highly competitive arena. Unlike the soft-tissue surgical robotics sector, where Intuitive Surgical’s da Vinci system has long maintained an absolute monopoly in the United States, the orthopedic robotics field is characterized by intense competition among multiple major players. Companies with established footprints in the orthopedic surgical robotics space include Stryker, Johnson & Johnson, Zimmer Biomet, Smith & Nephew, and Medtronic.

China’s orthopedic surgical robots started relatively late and are still in the early stage of industrialization. In recent years, many domestic companies have entered the robotics field, most of which are in their initial development stages, such as Tinavi Medical Technologies, MicroPort Scientific Corporation, Weigao Group, Rosenbot, and Santan Medical. Among them, listed companies like Weigao Group have expanded into orthopedic robots as a new business segment in recent years. The development of orthopedic surgical robots began relatively earlier; Tinavi, whose core business is orthopedic surgical robots, is the leading enterprise in this field in China. Companies like Rosenbot and Santan Medical were established in recent years, and their industries are still in the incubation period.

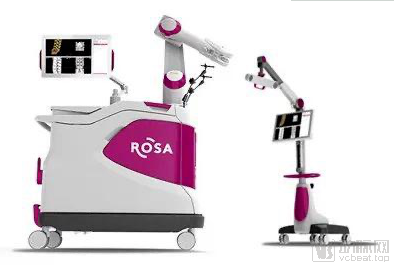

In March 2020, ROSA One, the surgical robot developed and manufactured by Medtech, a subsidiary of Zimmer Biomet, received approval from the National Medical Products Administration (NMPA) and officially entered the Chinese market. It became the only approved surgical navigation robot in China currently available for both neurosurgical and spinal surgeries, marking the formal commencement of its market deployment in the country. The system comprises a robotic arm base, a camera base, foot switches, navigation tools, and accessories, and is used to position surgical instruments during neurosurgical and spinal procedures.

(Figure: ROSA Surgical Robot System)

(Image source: Zimmer Biomet official)

Global orthopedics giant Smith & Nephew has also stepped up its game, announcing that its next-generation orthopedic surgical robot system, Cori, has received FDA clearance and officially launched in the U.S. market to capture greater market share. Reportedly, Cori can be used for total knee arthroplasty and unicompartmental knee arthroplasty. Compared with Smith & Nephew’s previous similar products, Cori offers higher operational efficiency and faster surgical procedures.

(Figure: Cori Orthopedic Surgical Robotic System)

(Image source: Smith & Nephew Official)

Cori integrates multiple modules, including an intelligent robotics platform, software, an intelligent operating system, and a data analytics system. Prior to knee implantation, visualization-based cutting preparation, mechanical calibration, and ligament data enable the customization of treatment plans for each patient.

Johnson & Johnson has placed greater emphasis on innovating its orthopedic surgical robot platform. During its second-quarter earnings conference call, the company announced a revision to its previous strategy for this platform, opting to seek U.S. market clearance for its general-purpose surgical robot platform via the 510(k) pathway. Johnson & Johnson clarified that clinical studies for the platform would commence in the second half of 2022. Recently, the approval of VELYS™ for market launch has further advanced Johnson & Johnson’s position in the orthopedic robotics sector.

Product innovation is inseparable from the development of new technologies. The unveiling of Medtronic’s latest intelligent robotic system for spine surgery, the Mazor X Stealth™ Edition, at the 2020 China International Import Expo (CIIE) highlighted the dynamic advancements in the orthopedic robotics industry. This system integrates Medtronic’s advanced algorithms, software, robotic arms, navigation technology, and surgical instruments to provide comprehensive support throughout the entire surgical workflow, including preoperative planning and simulation, precise surgical approach guidance, and real-time visualization. It supports a variety of spinal procedures, such as conventional open surgeries, minimally invasive surgeries, and complex scoliosis corrections, thereby assisting surgeons in achieving more precise, safe, and efficient outcomes.

(Figure: Mazor X Stealth™ Edition System)

(Image source: Medtronic official)

Stryker’s Mako joint surgery robotic system has been widely used worldwide, capturing a 9% global market share. Having obtained certification from the China Food and Drug Administration (CFDA), it is currently the only orthopedic surgical robot approved for performing joint replacement procedures in China. The Mako smart orthopedic robot developed by Stryker also performed its first surgery in China. In December 2020, the National Clinical Research Center for Orthopedics, Sports Medicine, and Rehabilitation utilized this system to complete China’s first intelligent orthopedic robot-assisted total biological knee arthroplasty, precisely achieving the highly challenging implantation of biological prostheses.

(Image content: MAKO surgical robot)

(Image source: Stryker)

In 2020, total knee arthroplasty robots in the domestic market achieved frequent successes. The Skywalker® Orthopedic Surgical Navigation and Positioning System developed by MicroPort and the “Orthopedic Surgical Navigation and Positioning System (TiRobot Recon)” developed by Tinavi Medical Technologies passed the National Medical Products Administration (NMPA)’s special review for innovative medical devices in May and November, respectively.

In May 2020, Suzhou MicroPort MedBot Robotics Co., Ltd., a subsidiary of MicroPort (Shanghai) Medical Robot Co., Ltd., announced that its independently developed Honghu® Skywalker® Orthopedic Surgical Navigation and Positioning System had passed the application for special review of innovative medical devices by the National Medical Products Administration (NMPA), thereby entering the “green channel” for special review.

(Figure: Honghu® Skywalker® Orthopedic Surgical Navigation and Positioning System)

(Image source: MicroPort)

Tianzhihang’s independently developed total knee arthroplasty surgical robot—the “Orthopedic Surgery Navigation and Positioning System (Model: TiRobot Recon)”—has passed the special review for innovative medical devices and entered the registration review and approval stage for innovative medical devices. The system assists surgeons in performing total knee arthroplasty by enabling personalized joint replacement planning based on patient-specific anatomy and kinematics, and by completing the bone cutting positioning required for accurate placement of knee prostheses. TiRobot Recon employs a robot-guided bone cutting approach that allows for positioned osteotomies without the need for intramedullary canal entry, pin insertion, or tool changes, thereby significantly improving cutting accuracy, reducing surgical trauma, and enhancing operational efficiency. Currently, no comparable products are available on the market in China.

(Image content: TiRobot Recon)

(Image source: Tinavi)

2020 also witnessed the rapid development of domestic enterprises. In July, Tinavi Medical Technologies officially listed on the STAR Market, marking the arrival of the first surgical robotics company on this board. Tinavi is a company dedicated to the research and development, manufacturing, sales, and service of orthopedic surgical navigation and positioning robots. Over the years, it has become a leading enterprise in China’s orthopedic surgical robotics industry. Tinavi was the first company to obtain a Class III medical device registration certificate issued by the China Food and Drug Administration (CFDA) for an “Orthopedic Robot Navigation and Positioning System,” and the fifth company globally to secure regulatory approval for a medical robot. Previously, there were no publicly listed companies in this sector on China’s A-share market; Tinavi’s listing on the STAR Market filled this gap in the A-share landscape.

Strategic partnerships enable industry players to leverage each other’s strengths, learn from one another, and achieve mutual progress. Tinavi Medical Technologies Co., Ltd. (Tinavi) and Johnson & Johnson, in collaboration with Renji Hospital affiliated to Shanghai Jiao Tong University School of Medicine, jointly signed a strategic cooperation agreement and successfully held a training course on robot-assisted spinal surgery skills, along with the unveiling ceremony for the “Clinical Technology Application Center for Robot-Assisted Spinal Surgery.” This initiative has expanded and strengthened the advantages and operational expertise of Tiangui® orthopedic surgical robot-assisted procedures in East China. On December 13, Tinavi and Johnson & Johnson further established a Robot-Assisted Spinal Surgery Training Center in partnership with Qilu Hospital of Shandong University, aiming to popularize the advanced technologies and application experience of Tiangui® orthopedic surgical robot-assisted spinal surgery among spine surgeons across the province and throughout China, thereby benefiting a greater number of patients with spinal injuries and disorders.

The primary application areas of orthopedic robots include joint surgery, spinal surgery, and trauma orthopedics. Currently, multiple companies have achieved commercial deployment of robotic systems in joint and spinal surgery. However, due to the diverse classification of fracture surgeries and the resulting complexity of surgical requirements, existing robotic systems struggle to meet actual clinical needs. Consequently, robotic systems for trauma orthopedics have not yet achieved clinical application or widespread product commercialization.

Joint Surgery Robot

Joint surgical robots are the earliest orthopedic surgical robots to achieve technological and commercial applications. They can be classified into active operation type and active constraint type based on their operational control methods. Compared with active operation-type robots, active constraint-type surgical robots better leverage the advantages of robotic systems by ensuring boundary control during joint resection through active constraints, thereby enhancing surgical safety. Additionally, they utilize physician-guided drag operations to make the entire surgical procedure continuous and controllable. Therefore, active constraint-type surgical robots offer superior clinical operability, adaptability, and safety.

Following the tremendous success of Stryker’s MAKO system, Zimmer Biomet launched its ROSA Knee robotic system in 2019. In 2020, domestically developed total knee arthroplasty (TKA) robotic systems also achieved significant milestones. The Skywalker® Orthopedic Surgical Navigation and Positioning System, developed by MicroPort, and the “Orthopedic Surgical Navigation and Positioning System (TiRobot Recon),” developed by Tinavi Medical Technologies, passed the National Medical Products Administration (NMPA)’s special review process for innovative medical devices in May and November, respectively.

(Figure: Honghu® Skywalker™ Orthopedic Surgical Navigation and Positioning System)

(Image source: MicroPort official website)

Spinal Surgery Robot

Spinal surgical robots are currently primarily used for pedicle screw fixation. Leveraging medical imaging for preoperative planning, these systems achieve precise spatial positioning and either autonomously perform or guide surgeons in drilling the implantation channels. The primary goal of spinal surgical robots is to enable precise, minimally invasive procedures. By ensuring accurate robotic positioning, they reduce the size of surgical incisions, lower the risk of nerve injury, and maximize the precision and safety of surgical operations.

Israel’s Mazor Robotics pioneered surgical navigation systems and ancillary products in the spine surgery market, advancing procedures from traditional freehand techniques to precision robot-assisted operations. Renaissance is Mazor Robotics’ flagship product in the field of spine surgery.

(Figure: Renaissance Spine Surgical Robot)

(Image source: Medical Robots)

In 2020, in the field of spinal surgery robots, foreign companies such as Stryker and Zimmer Biomet reinvested heavily in R&D, while Medtronic strengthened its dominant position through mergers and acquisitions. In China, Tinavi had already obtained regulatory approval and launched its products, with orthopedic giants vying to capture the spinal surgery robot market. Zimmer Biomet’s ROSA One officially entered the Chinese market; Tinavi’s Tianji® orthopedic surgical robot surpassed 10,000 procedures; and Medtronic, a leading medical device company, unveiled its new intelligent spinal surgical robot (Mazor X Stealth™ Edition) at the Expo. It is conceivable that future competition will inevitably become more intense.

(Figure: Tiangji® Orthopedic Surgical Robot System)

(Image source: Official website of the Tiangji Orthopedic Surgical Robot)

Orthopedic robotics is a relatively mature branch within the field of surgical robots. According to data published by Medgadget, the orthopedic surgical robot market was valued at approximately $300 million in 2020 and is projected to reach $3.5 billion globally by 2027.

The primary application areas of orthopedic robots include trauma orthopedics, spinal surgery, and joint surgery. In terms of application scenarios, surgical robots in the fields of spinal surgery and joint surgery have reached a relatively mature stage of development. However, the research and development of fracture reduction robots present significant challenges, resulting in relatively slow progress; to date, no such products have entered clinical application worldwide. Currently, orthopedic robots are mainly applied in spinal surgery and joint surgery. Based on the market size of these two sectors, the industry is experiencing rapid growth.

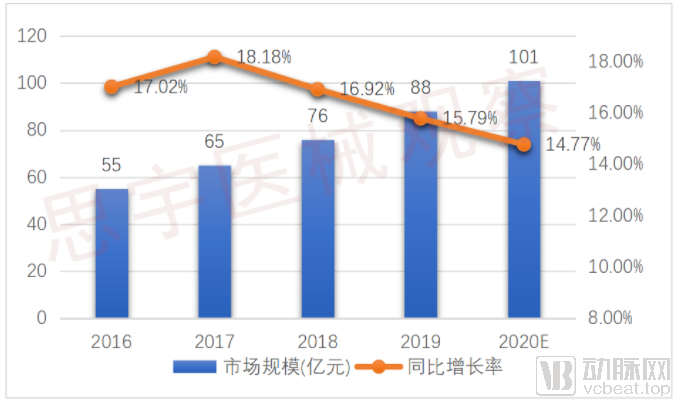

Field of Spine Surgery

In 2019, the sales volume of the spinal market was approximately RMB 8.8 billion, representing a 15.79% increase from 2018, indicating that the spinal market maintained rapid growth.

(Figure: Market Size of Spinal Surgery in China (in RMB 100 million))

(Data source: public information)

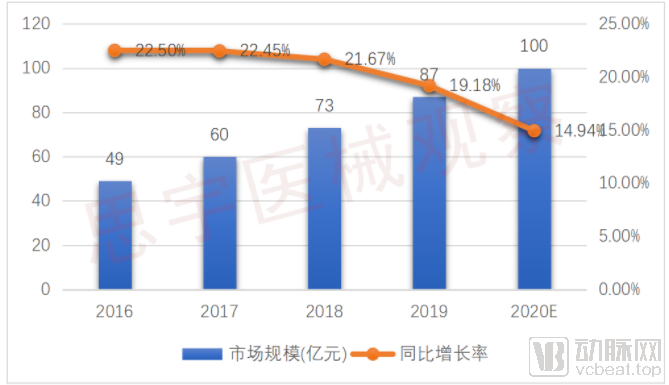

Joint Surgery

In 2019, the sales volume of the joint market was approximately RMB 8.7 billion, representing a year-on-year growth of 19.18% compared to 2018.

(Figure: Market Size of Joint Surgery in China (in RMB 100 million))

(Data source: public information)

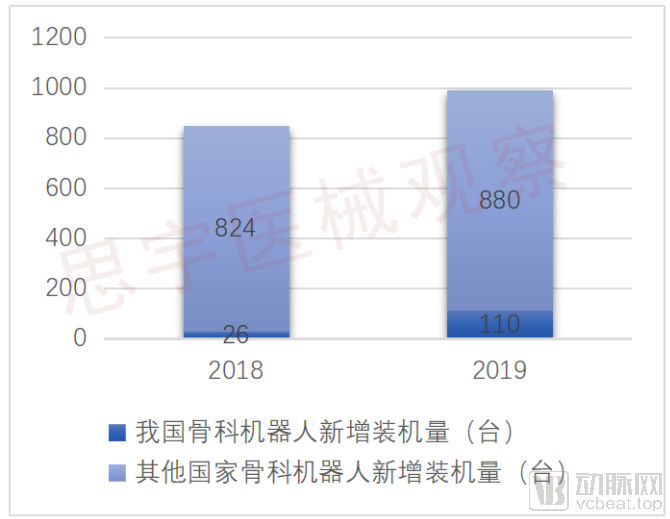

According to statistics from Persistence Market Research, the global revenue of orthopedic robotics companies was approximately $1.037 billion in 2018, with around 700–1,000 new orthopedic robotic systems installed worldwide that year. In contrast, China’s new installations of orthopedic robots totaled approximately 26 units in 2018, accounting for less than 4% of the global total. In 2019, the number of newly installed orthopedic robotic systems globally reached approximately 990 units, and global orthopedic robotics companies achieved total revenues of around RMB 1.1 billion. In China, approximately 110 orthopedic surgical robots were newly installed in 2019, among which Tinavi Medical Technologies accounted for about 76%, representing roughly 11.1% of the global market share.

(Figure: New Installations of Orthopedic Surgical Robots)

(Data source: Persistence Market Research)

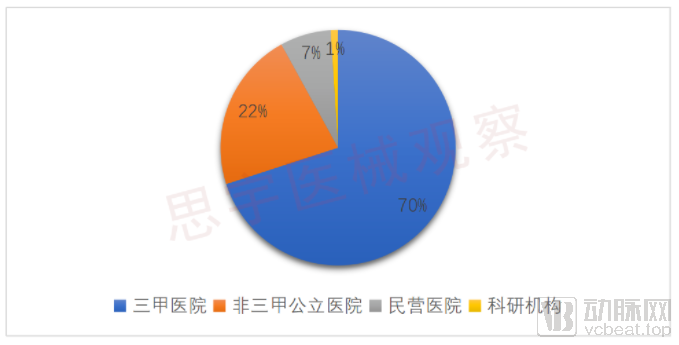

Due to the high unit cost of orthopedic surgical robots and their exclusion from national medical insurance coverage, adoption has been concentrated primarily in Grade 3A hospitals and a limited number of private hospitals. Taking the installation data of Tinavi’s “Tiandi” orthopedic navigation robot as an example, 52 out of the 74 healthcare institutions it serves are Grade 3A hospitals, accounting for over 70%. The development of orthopedic surgical robots in China remains in the market introduction stage, with significant room for improvement in physician acceptance and market penetration.

(Figure: Downstream Distribution of Orthopedic Robots in China)

(Data source: Tinavi's prospectus)

There are many visions for the future of orthopedic surgical robots. Medical robots will become more minimally invasive, intelligent, and precise. New technologies such as 5G communication, 3D printing, smart materials, medical big data, artificial intelligence, and virtual/augmented reality will be continuously integrated into the technical framework of medical robots, promoting the development of orthopedic surgical robots. Intelligent and personalized medical technologies are becoming the trend of development.

From the perspectives of product and technology, the technology of orthopedic surgical robots will gradually improve, leading to better development in this field.

In November 2020, the Telemedicine Center of China Medical University successfully performed a remotely controlled minimally invasive spinal surgery on a patient located one hundred kilometers away, assisted by the Tianji orthopedic surgical robot and leveraging 5G technology. Characterized by high speed and low latency, 5G communication technology, in conjunction with the orthopedic surgical robot, enabled remote planning and remote operation.

(Figure: 5G Communication-Enabled Remote Operation of Minimally Invasive Spine Surgery)

(Image source: TiJi Orthopedic Surgical Robot WeChat Official Account)

In January 2021, Zhisu Health’s first 3D-printed cervical interbody fusion cage received U.S. Food and Drug Administration (FDA) 510(k) marketing clearance, making it the first Chinese technology company to have a 3D-printed orthopedic implant product FDA-cleared.

(Figure: 3D-printed artificial vertebral body)

(Image source: Official website of Zhisu Health)

At the industry level, medical robotics, after more than three decades of development, has moved beyond its toddling infancy and entered a vibrant adolescence. The basic framework of the industry has taken shape, yet many uncertainties remain. In the future, continuous maturation and specialization of upstream and downstream supply chains, along with supportive ecosystems, will be essential to foster a dynamic innovation ecosystem for the medical robotics industry.

In addition to the product itself, it is essential to build a comprehensive surgical solution centered around robotics. The impact of robots on the medical device sector extends beyond the value delivered by the device itself; it represents a reform and integration of the industry’s development, shifting it from fragmented, point-specific advancements toward a holistic model based on clinical departments or surgical procedures. This transition presents both opportunities and challenges for all companies in the medical device field.