Bridging the $54 Billion ART Supply-Demand Gap: Domestic Substitution and Service Empowerment as Optimal Value Drivers – 2021 Assisted Reproductive Technology (ART) Industry Research Report

Children are the source of joy for every family, yet 48 million couples in China face the risk of losing this happiness due to infertility.

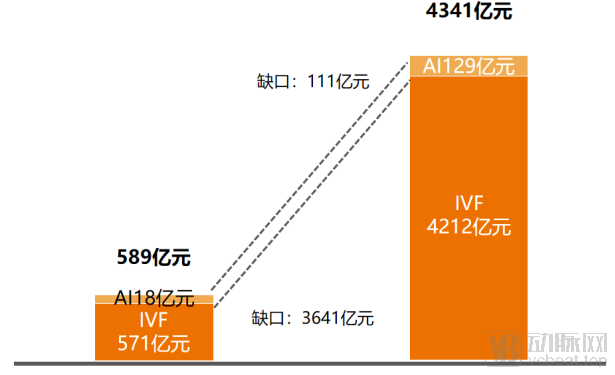

Due to external environmental factors and the postponement of first marriages and childbirth, China has joined the ranks of countries with high infertility rates, with the national prevalence of female infertility ranging from 12.5% to 15%. With technological advancements, assisted reproductive technology (ART) has brought hope to infertile couples. According to statistics published in the authoritative journal Reproductive Biology and Endocrinology, approximately 20% of infertile couples tend to choose ART services, creating a market demand valued at RMB 434.1 billion. In 2020, the number of ART cycles in China reached 1.303 million, including 952,000 in vitro fertilization (IVF) cycles and 351,000 artificial insemination cycles. In terms of market composition, IVF accounted for 97% of the total, with a market size of RMB 421.2 billion, making it the dominant segment in the ART market.

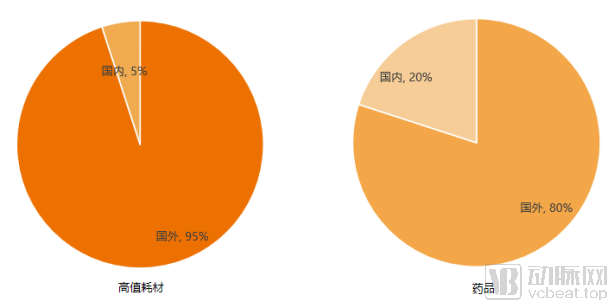

During in vitro fertilization (IVF) treatment, high-value consumables such as assisted reproductive culture media and PGT reagents are used in conjunction with medications for down-regulation, ovarian stimulation, ovulation induction, and luteal phase support. However, 95% of these high-value consumables and 80% of the medications are monopolized by foreign brands, making the substitution with domestically produced alternatives an urgent priority. Meanwhile, an analysis of the distribution of domestic assisted reproductive service resources reveals that public medical institutions account for over 90% of the market. While resources are abundant in eastern coastal provinces, they are scarce in central and western regions. Furthermore, most assisted reproductive medical institutions lack the qualifications to provide third-generation IVF services. The imbalance in resource distribution and the insufficiency of service capacity require immediate resolution.

In pursuit ofSolutions to the Two Major Challenges Above,VCBeat, in collaboration with the Weituo Bio Assisted Reproductive Technology Research Center, has released the “Anchoring Real Needs: Domestic Substitution and Service Empowerment – 2021 Assisted Reproductive Technology Industry Research Report.” Through on-site investigations of leading ART enterprises and in-depth interviews with ART experts, the report identifies strategic solutions to break through industry bottlenecks. It provides a detailed analysis of the pathways for domestic substitution of ART medical devices and pharmaceuticals, models for service empowerment in ART, forward-looking empowerment systems across the industry chain, and future trends in the ART sector, while also presenting case studies on Weituo Bio and Yikang Gene. By comprehensively examining these breakthrough strategies, the report aims to serve as a reference for innovative enterprises and medical institutions committed to advancing the development of the assisted reproductive technology industry.

Key Points

9.6 million infertile couples and a RMB 375.2 billion supply-demand gap paint the assisted reproductive technology market as a blue ocean.

Uneven Distribution of Assisted Reproductive Technology (ART) Resources: Abundant Resources in Eastern Provinces, Scarcity in Central and Western Regions, with Public ART Institutions Accounting for 90%

High Import Dependence for Assisted Reproductive Technology Devices and Pharmaceuticals: 95% of High-Value Consumables and 80% of Pharmaceuticals in Assisted Reproduction Rely on Imports.

The domestic substitution of medical devices for assisted reproductive technology follows a three-step approach: substitution of tubing, substitution of reagents exempt from clinical trials, and substitution requiring clinical trials. The substitution of pharmaceuticals for assisted reproductive technology centers on the replacement of ovulation-inducing drugs.

The new medical infrastructure, supported by the Internet, artificial intelligence, the Internet of Things, big data, and 5G, builds the digital ecosystem foundation for the assisted reproductive technology industry chain.

Serving 9.6 million couples with infertility

Assisted reproduction has become a specialized medical service with high demand in the 21st century. Assisted Reproductive Technology (ART) refers to techniques that involve manual manipulation of gametes (sperm and eggs), zygotes (fertilized eggs), and embryos using medical technologies and methods to achieve pregnancy.

Living environments, work-related stress, and the delayed age of first marriage and childbirth have led to a year-on-year rise in infertility rates. The prevalence of female infertility in China ranges from 12.5% to 15%. By the end of 2019, there were approximately 308 million women of childbearing age (21–49 years) in China, meaning that roughly 38.5 to 46.2 million women in this demographic were affected by infertility. When combined with men suffering from infertility, the number of infertile couples in China has now exceeded 48 million.

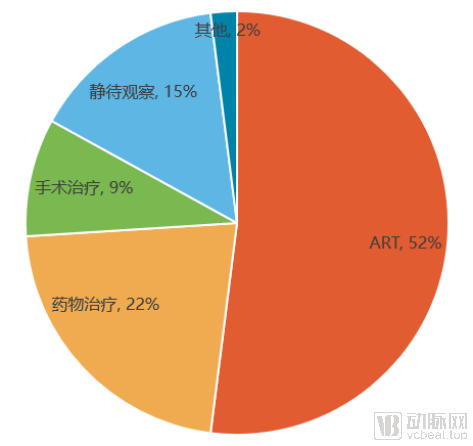

Based on the treatment pathways for infertility, therapeutic approaches are primarily categorized into three types: conventional pharmacological therapy, surgical intervention, and assisted reproductive technology (ART). For couples with mild conditions and no identified organic abnormalities in either partner, pharmacological therapy is the predominant approach. If organic abnormalities are present in one or both partners, such as varicocele in males or endometrial lesions in females, surgical intervention is required. For patients who are not suitable for pharmacological or surgical treatments, ART can be utilized to fulfill their reproductive needs. According to statistics published in the authoritative reproductive journal *Reproductive Biology and Endocrinology*, approximately 20% of infertile couples opt for ART services, corresponding to a real-world user base of 9.6 million couples. Furthermore, the journal reported the distribution of treatment modalities selected by physicians in China, with ART accounting for 52%, while pharmacological and surgical therapies accounted for 22% and 9%, respectively. This indicates that ART has become the primary choice for treating infertility in China.

Distribution of Treatment Options Selected by Chinese Physicians for Infertility

Currently, the most commonly used assisted reproductive technologies (ART) are artificial insemination (AI) and in vitro fertilization (IVF). Artificial insemination is categorized into husband’s sperm artificial insemination and donor sperm artificial insemination, based on the source of the sperm. IVF technology continues to evolve and has now advanced to third-generation IVF. This technology enables the exclusion of embryos with chromosomal numerical abnormalities, structural abnormalities, or those carrying single-gene genetic disorders, thereby allowing for the selection of high-quality embryos for transfer.

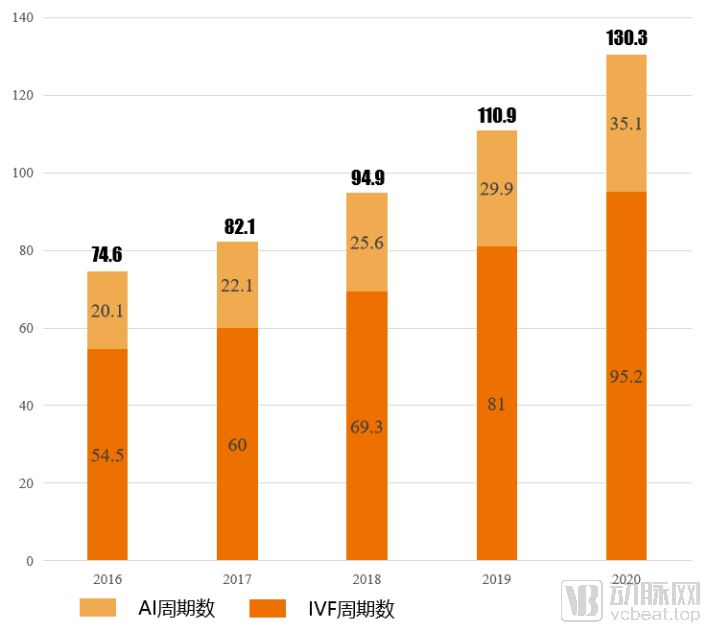

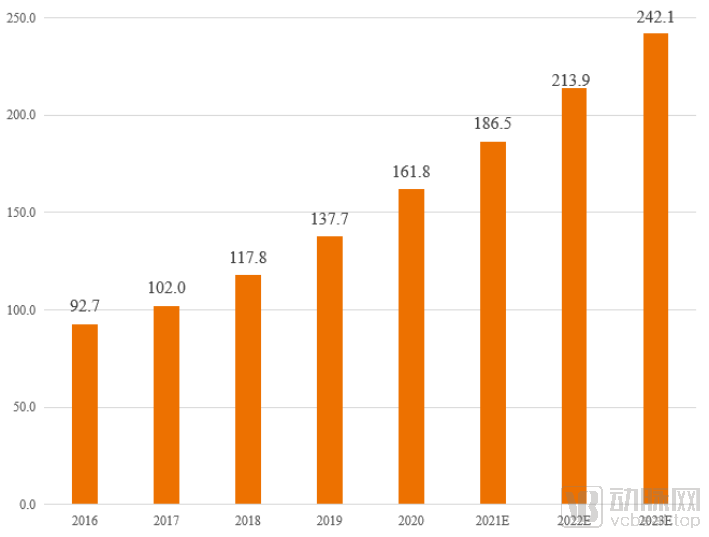

Data published in *Reproductive Biology and Endocrinology* indicate that the ratio of artificial insemination to in vitro fertilization (IVF) cases among Chinese physicians is approximately 7:19, with IVF typically selected after two to three unsuccessful artificial insemination attempts. Consequently, IVF constitutes the dominant force in the assisted reproductive technology (ART) market. By the end of 2020, the total number of ART treatment cycles in China reached 1.303 million, comprising 952,000 IVF cycles and 351,000 artificial insemination cycles. The compound annual growth rate (CAGR) for the total number of ART service cycles from 2016 to 2020 was as high as 15%.

Total Number of ART Service Cycles in China (2016–2020) (10,000 Cases)

There are currently 517 medical institutions in China approved to provide assisted reproductive technology (ART) services. Based on the total number of ART treatment cycles in 2020, the average number of cycles per institution exceeded 2,600. Public ART institutions account for more than 90% of all such facilities; due to their large scale and abundance of high-quality physicians, they handle over 95% of the total service volume. According to licensing qualifications, 396 institutions are currently authorized to provide in vitro fertilization (IVF) services, while only 70 institutions are authorized to provide preimplantation genetic diagnosis (PGD) services, representing 14% of all ART institutions.

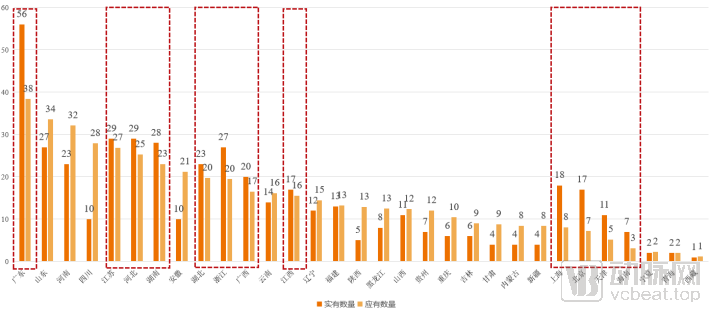

In China, the spatial distribution of assisted reproductive technology (ART) service resources is uneven. According to the planning standard of one ART center per 3 million people, eastern coastal provinces such as Guangdong, Shanghai, Beijing, Tianjin, Zhejiang, and Hebei have more ART institutions than planned, indicating relatively abundant ART service resources. In contrast, central and western provinces such as Henan, Sichuan, Anhui, Shaanxi, Guizhou, and Chongqing have fewer ART institutions than required by the plan, resulting in a relative scarcity of ART service resources. Particularly in populous provinces like Henan and Sichuan, the capacity for ART services has a greater impact on sustainable population development. The uneven spatial distribution of ART service resources creates market opportunities for enterprises. While serving first-tier cities, companies should actively expand into cities within populous provinces. For instance, Jinxin Fertility Group, a private ART medical service provider, established Chengdu Xinan Gynecological Hospital in Sichuan, performing approximately 8,000 ART cycles annually, thereby alleviating the shortage of ART service capacity in western China.

Distribution of the Number of Assisted Reproductive Technology (ART) Medical Institutions by Province (Units)

Based on the service capabilities of various assisted reproductive technology (ART) institutions, the top 10 ranked facilities are CITIC-Xiangya Reproductive and Genetic Hospital (Hunan), Peking University Third Hospital (Beijing), Shanghai Ninth People’s Hospital (Shanghai), Shandong University Affiliated Reproductive Hospital (Shandong), The First Affiliated Hospital of Sun Yat-sen University (Guangdong), Jiangsu Province People’s Hospital (Jiangsu), The First Affiliated Hospital of Zhengzhou University (Henan), Chongqing Health Center for Women and Children (Chongqing), Zhejiang University School of Medicine Women’s Hospital (Zhejiang), and Northwest Women’s and Children’s Hospital (Shaanxi). These medical institutions are predominantly public healthcare entities (with CITIC-Xiangya Reproductive and Genetic Hospital operating under a mixed-ownership model), and most are located in eastern provinces, further highlighting the uneven distribution of ART medical resources across China.

The industrial chain landscape has taken shape, but the localization rate of upstream pharmaceuticals and medical devices remains low.

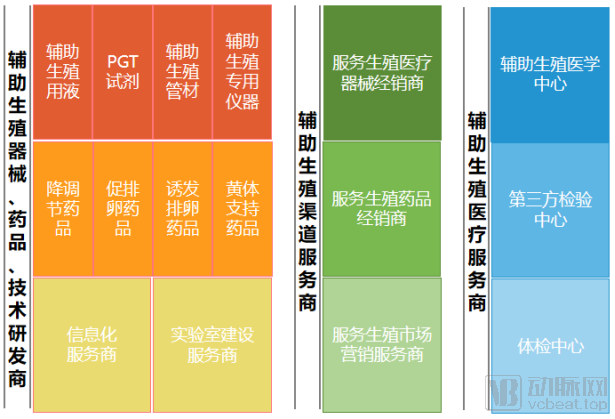

The upstream of the assisted reproductive technology (ART) industry chain comprises manufacturers of medical devices, pharmaceuticals, and R&D firms; the midstream consists of distributors of medical devices and pharmaceuticals as well as marketing channel providers; and the downstream includes ART healthcare service providers. Upstream enterprises primarily supply the medical devices, pharmaceuticals, and technologies required for ART services. Midstream enterprises focus on ensuring the supply of ART products and facilitating patient access. Downstream enterprises deliver ART medical services, helping patients with infertility achieve successful pregnancies. It is evident that, after years of development, the entire ART industry has established a clear system of division of labor.

The Ecosystem Landscape of the Assisted Reproductive Technology Industry Chain

Upstream medical devices in the assisted reproductive technology (ART) industry chain primarily include high-value ART consumables (such as embryo freezing/thawing media, embryo culture media, and PGT reagents), solid ART consumables, and specialized ART instruments. Pharmaceutical products encompass medications required for down-regulation, ovarian stimulation, ovulation induction, and luteal phase support. In terms of overall market share, 95% of high-value ART consumable devices and 80% of ART pharmaceuticals rely on imports. Notably, the embryo culture media market is monopolized by foreign brands, with no domestically approved products currently available on the market.

Domestic and International Market Share of High-Value Consumables and Pharmaceuticals in Assisted Reproductive Technology

Primary Reasons:

(1) Late industry inception and weak technological accumulation. The development of China’s assisted reproductive technology (ART) industry has lagged behind that of foreign countries, with the research and development (R&D) of related pharmaceuticals and medical devices starting relatively late. The R&D threshold for high-value consumables in ART is high, typically requiring 2–3 years, while the R&D cycle for ART pharmaceuticals is even longer, spanning 4–6 years. Therefore, the R&D of both pharmaceuticals and medical devices necessitates substantial technological expertise and time for accumulation.

(2) Stringent regulatory approval processes impact product market authorization. In China, high-value consumables for assisted reproductive technology (ART) are primarily regulated as Class III medical devices, with the entire approval process taking 1–2 years; if clinical trials are required, the timeline extends to approximately 3 years. In contrast, ART devices in the United States are generally classified as Class II medical devices, with an approval cycle of only a few months.

In the midstream of the assisted reproductive technology (ART) industry chain, online platforms featuring “Internet + ART services” have emerged as a new force in marketing, giving rise to companies such as Bei Beike, Haoyunbang, Meiyou, Aiding Eugenics and Fertility Assistance, and HelloBaby. Some of these platforms focus on general health-oriented menstrual cycle management, targeting natural conception among the broader health-conscious population. Others aim to accumulate users by providing content and product offerings to individuals facing infertility through a “tools + community + e-commerce” model. Still others offer medical access services, connecting infertility patients with high-quality reproductive healthcare institutions and providing medical accompaniment services. These “Internet + ART” service platforms have driven patient traffic to ART medical service providers.

According to data released by the National Health Commission of China, only 70 institutions are qualified to provide preimplantation genetic diagnosis (PGD) services, accounting for 14% of the total number of institutions. The development of assisted reproductive technology (ART) institutions is uneven. In terms of institutional type, public medical institutions account for 90%. Regarding spatial distribution, ART centers are primarily located in the eastern and southern regions, with Guangdong and Jiangsu provinces having the highest numbers at 56 and 33, respectively. In terms of the number of in vitro fertilization (IVF) treatment cycles, only a few medical institutions, including CITIC-Xiangya Reproductive & Genetic Hospital, Peking University Third Hospital, Shanghai Ninth People’s Hospital Affiliated to Shanghai Jiao Tong University School of Medicine, Reproductive Hospital Affiliated to Shandong University, Jinjiang District Maternal and Child Health Hospital of Chengdu, IVF Medical Group, and Jinxin Fertility Medical Group, perform more than 10,000 cycles annually.

¥375.2 Billion Supply-Demand Gap Paints a Blue Ocean for Domestic Substitution Market

According to field research interviews, the cost per cycle of IVF is approximately RMB 60,000, while the cost per cycle of AI is approximately RMB 5,000. Currently, 9.6 million infertile couples in China require ART services. With a selection ratio of 19:7 for IVF versus AI, the market demand for IVF amounts to RMB 421.2 billion, and for AI to RMB 12.9 billion, bringing the total ART market demand to RMB 434.1 billion. In contrast, Frost & Sullivan reported that in 2020, the domestic IVF service market size was RMB 57.1 billion, the AI service market size was RMB 1.8 billion, and the total ART service market size was RMB 58.9 billion. This indicates a potential market gap of RMB 375.2 billion in China (with an IVF shortfall of RMB 364.1 billion and an AI shortfall of RMB 11.1 billion).

Potential Market Size of Assisted Reproductive Technology in China

In summary, China’s assisted reproductive technology (ART) industry is characterized by three key features: significant market growth potential, uneven distribution of ART service resources, and a high reliance on imported pharmaceuticals and medical devices.

(1) Significant market development potential: There are 9.6 million infertile couples in China, with an unmet market demand gap of RMB 375.3 billion.

(2) Uneven distribution and insufficient capacity of assisted reproductive technology (ART) services: Public ART institutions account for over 90% of the total, with only 70 facilities qualified to provide third-generation in vitro fertilization (IVF) services. While eastern coastal provinces have ample ART resources, central and western provinces suffer from a scarcity of such resources.

(3) Strong reliance on imports for assisted reproductive drugs and devices: 95% of high-value consumable medical devices and 80% of pharmaceuticals used in assisted reproduction are imported, indicating a low level of domestic production.

In the face of such substantial domestic market demand, it is essential to address the insufficient localization of assisted reproductive technology (ART) devices and pharmaceuticals by vigorously advancing the strategy of domestic substitution. Meanwhile, service empowerment should be leveraged to enhance the service capabilities of downstream ART medical institutions, thereby alleviating the uneven distribution of ART service resources and the inadequate service capacity prevalent in most medical institutions.

Domestic Substitution of Medical Devices: Assisted Reproductive Culture Media and PGT Reagents Emerge as Core Areas for Replacement

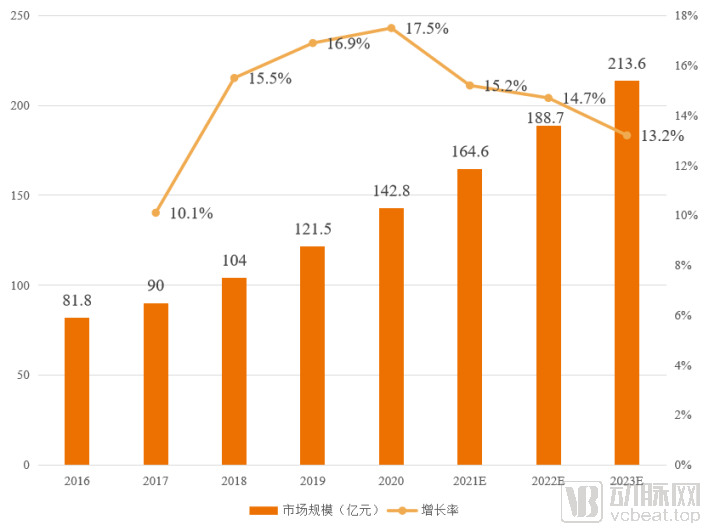

IVF medical devices have generated substantial market demand. Based on the total number of IVF cycles, the domestic market size in China reached RMB 16.2 billion in 2020. With the total number of IVF cycles expected to continue rising, we project that the market size for IVF medical devices will exceed RMB 24 billion in 2023, representing 1.5 times the 2020 figure.

Market Size of IVF Medical Devices (2016-2023) (in 100 million yuan)

In IVF medical devices, high-value consumables such as assisted reproductive fluids (including oocyte washing solution, sperm washing solution, freezing solution, thawing solution, fertilization solution, culture medium, and transfer medium) and PGT reagents (including reagents for PGT-A/preimplantation genetic testing for aneuploidy, PGT-SR/preimplantation genetic testing for structural rearrangements, and PGT-M/preimplantation genetic testing for monogenic disorders) account for a significant proportion of the costs.

Fluids for assisted reproductive technology (ART) are predominantly sourced from foreign brands. The market for cryopreservation/thawing solutions and culture media is largely monopolized by international companies such as Vitrolife (Sweden), CooperSurgical (USA), Irvine Scientific (USA), Kitazato (Japan), Origio A/S (Denmark, acquired by CooperSurgical), William A. Cook (Australia), Wallace (UK), and FertiPro (Belgium). Recognizing the commercial opportunities in the ART fluids market, domestic enterprises are actively advancing product research and development. Weituo Bio, a leading Chinese company in the field of assisted reproduction, has independently developed vitrification freezing and thawing solutions that have sequentially obtained FDA certification and NMPA Class III certification. Its vitrification cryovials have received EU CE certification, making Weituo Bio the first domestic R&D enterprise to secure international certifications. Other products, including culture media, oocyte retrieval fluids, and gamete buffer solutions, are also accelerating their NMPA registration applications.

In 2020, the market size for PGT reagents in China reached RMB 2.16 billion, with PGT-A accounting for 56% of the share. This predominance is primarily due to the broad applicability of PGT-A screening, with over 500,000 IVF cycles utilizing PGT-A in 2020. PGT-M held the smallest market share, as the number of monogenic disease carriers in China ranges between 100,000 and 120,000, and the penetration rate of screening services remains below 10%. Frost & Sullivan projects that the PGT market size will reach RMB 8.51 billion by 2023, representing a compound annual growth rate (CAGR) of 58% from 2020 to 2023. This rapid growth is mainly driven by increased patient willingness to pay for PGT services in pursuit of healthy offspring. Currently, several domestic companies, including Yikon Genomics, BGI Medicine, Berry Genomics, Beckon Diagnostics, and Genetron Health, are engaged in providing PGT services. MALBAC® (Multiple Annealing and Looping-Based Amplification Cycles), a single-cell whole-genome amplification technology invented by Yikon Genomics, effectively addresses challenges such as low sensitivity, uneven sequence coverage, and high allele dropout rates during the amplification of trace DNA samples. This technology enables accurate amplification and sequencing of over 93% of the genome in single cells, achieving a success rate as high as 95%. MALBAC® has had a breakthrough impact on the development of PGT and has been cited numerous times in industry guidelines, consensus statements, and academic publications.

Domestic substitution of medical devices has been a focal point of the industry in recent years, with the Chinese government introducing a series of supporting policies to actively promote this trend. Based on the progress of domestic substitution, medical devices can be categorized into four stages: import monopoly, accelerated substitution, competitive parity, and domestic dominance. Medical devices for assisted reproduction are currently in the stage of accelerated substitution. Moreover, the compound annual growth rate (CAGR) of the total number of IVF cycles in China is projected to reach 14% over the next three years, with the total number of IVF cycles expected to exceed 1.4 million in 2023. This will create greater market demand for medical devices, indicating promising prospects for the domestic substitution of assisted reproductive medical devices.

However, the full domestic substitution of medical devices for assisted reproductive technology is not achieved overnight but proceeds in a gradual manner. Based on interviews with multiple industry experts, we believe that the entire process of domestic substitution can be divided into three phases:

Phase I: Primarily focuses on substituting low-value-added medical devices with relatively low technical barriers, such as oocyte denudation needles, oocyte retrieval needles, culture dishes, and embryo transfer catheters. These products are regulated as Class II medical devices, exempt from clinical trials, and subject to approval by provincial-level drug administrations, resulting in a streamlined approval process. However, due to the low technical threshold, these products suffer from severe homogenization, making it difficult to establish a competitive advantage in the market.。

Phase II: The primary focus is on substituting high-value-added medical devices with higher technical barriers, such as oocyte rinsing solutions, cryopreservation/thawing media, and gamete buffer solutions. Although these products are regulated as Class III medical devices, companies may apply for clinical trial exemptions by submitting clinical data from similar products (including fundamental principles, key technical performance indicators, and intended uses), thereby saving time and costs associated with clinical trials and accelerating product approval and market launch.

Phase III: This phase primarily involves the substitution of high-value-added medical devices with high technical barriers, such as culture media, PGT reagents, and assisted reproductive laser systems. These products are regulated as Class III medical devices, requiring clinical trials and approval from the National Medical Products Administration (NMPA). The entire approval process takes 1–2 years and costs approximately RMB 10 million.

Roadmap for the Domestic Substitution of Medical Devices in Assisted Reproductive Technology

Domestic Substitution of Pharmaceuticals: Ovulation-Inducing Drugs Become the Core of Substitution

Assisted reproductive drugs are primarily used for ovarian stimulation and luteal phase support. Ovarian stimulation drugs promote oocyte maturation and successful ovulation, while luteal phase support drugs help prevent uterine contractions and modulate immune function to avert embryonic rejection by the uterus. These drugs are mainly administered during in vitro fertilization (IVF) procedures. Based on the number of IVF cycles, the market size for IVF-related medications reached RMB 14.28 billion in 2020, with a compound annual growth rate (CAGR) of 15% from 2016 to 2020. As IVF penetration increases, the medication market is projected to exceed RMB 21 billion in 2023.

Market Size and Growth Rate of IVF Medications, 2016–2023

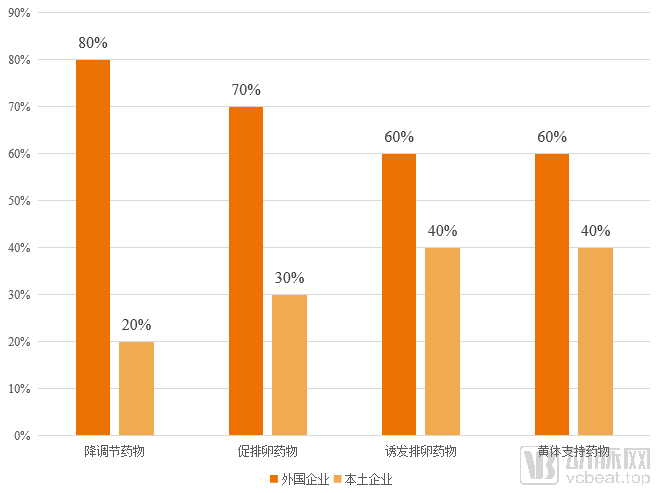

In terms of medication usage during the IVF process, ovulation induction agents account for the highest proportion at 62%, followed by luteal phase support agents at 20%, down-regulation agents at 15%, and ovulation trigger agents at 3%. Among companies in the assisted reproductive technology (ART) pharmaceutical sector, foreign enterprises are represented by Merck Serono and MSD, while domestic Chinese companies are represented by Livzon Pharmaceutical, Xianju Pharmaceutical, and GeneScience Pharmaceuticals. The two foreign companies collectively hold a 60% share of the ART pharmaceutical market, whereas Livzon Pharmaceutical accounts for 20% and Xianju Pharmaceutical for 5%. Therefore, foreign enterprises still maintain an absolute advantage in the ART pharmaceutical market, underscoring the need for domestic pharmaceutical companies to further strengthen R&D and innovation to increase the market share of Chinese brands.

Market Share Distribution of Domestic and International Companies in the IVF Medication Market in 2020

Among the various medications used in IVF, there is a significant gap between the market shares of domestic and foreign enterprises for down-regulation agents and ovulation induction drugs, with both exceeding 40%. The gap for ovulation-triggering agents and luteal phase support medications is smaller, at 20%. Merck Serono’s product portfolio covers the entire IVF process and holds a substantial market share. As an innovative prescription drug subsidiary under Merck, Merck Serono focuses on R&D in reproductive health and endocrinology, neurodegenerative diseases, and oncology, with annual R&D expenditures exceeding €1 billion (approximately RMB 7.76 billion). Reproductive health and endocrinology constitute the company’s largest business segment, accounting for about one-third of its total operations. Its assisted reproductive technologies (ART) drugs, including Cetrotide, Gonal-f, Ovidrel, and Crinone, have been sequentially launched in China, capturing an exceptionally high market share. Livzon Pharmaceutical Group, a leading domestic enterprise in ART medications, is also actively increasing its R&D efforts. According to its annual report, the company has invested over RMB 30 million in related R&D and launched ART drugs such as Beiyi, Lebaode, and Lishenbao, achieving a favorable market share. In addition to Livzon, Xianju Pharmaceutical has entered the luteal phase support market by launching Yimaxin Progesterone Capsules and Progesterone Injection, securing a 20% share of the luteal phase support medication market.

As can be seen, there is significant potential for domestic substitution of assisted reproductive technology (ART) medications:

In terms of market share, domestic companies account for only one-third of the ovulation induction drug market, which represents the largest segment (62%) of IVF medication usage. Therefore, companies represented by Livzon Pharmaceutical and GeneScience Pharmaceuticals need to further expand their presence in the ovulation induction drug market to increase their market share. Meanwhile, more domestic enterprises should enter the assisted reproductive medicine sector to boost their market shares across various stages, including down-regulation, ovulation induction, triggered ovulation, and luteal phase support.

In terms of R&D innovation, domestic companies (with R&D expenditures in the tens of millions of yuan) lag significantly behind Merck Serono (with R&D expenditures of 7.76 billion yuan). It is essential to further increase R&D funding, enrich the pipeline of assisted reproductive drugs, and accelerate drug approval and market launch applications. By introducing a wider variety of assisted reproductive medications, domestic firms can gradually replace foreign competitors in the market.

In summary, the core of domestic substitution for assisted reproductive technology (ART) medical devices lies in replacing high-value consumables such as ART culture media—including freeze/thaw solutions and embryo culture media—and PGT reagents with domestically produced alternatives. This transition will not happen overnight; it is divided into three distinct phases based on factors such as technical barriers and the complexity of clinical trials. Meanwhile, the core of domestic substitution for ART pharmaceuticals focuses on ovulation induction drugs. In response to the substantial domestic demand for ART services, a cohort of enterprises with strong independent R&D capabilities has emerged in both the medical device and pharmaceutical sectors, positioning them as the primary drivers of domestic substitution in assisted reproduction.。

Uneven Distribution of Assisted Reproductive Technology (ART) Medical Service Resources and Variable Service Capabilities

Severe Polarization in Assisted Reproductive Technology (ART) Institutions: Fewer than 10 facilities perform over 10,000 IVF cycles annually, while the vast majority handle only a few hundred. CITIC-Xiangya Reproductive and Genetic Hospital ranks first, performing more than 40,000 IVF cycles per year and capturing a 6% market share. This disparity is primarily attributable to insufficient service capacity among most ART institutions, with key factors influencing service levels including service qualifications, technical platforms, management and operations, and service team development.

(1) The application process for PGD accreditation is lengthy and highly challenging: Obtaining PGD accreditation involves four stages, spanning a total period of 9–10 years, during which institutions must sequentially secure licenses for artificial insemination, in vitro fertilization (IVF), and finally PGD accreditation. Moreover, the approval system imposes stringent requirements on both soft and hard infrastructure, including the qualifications of assisted reproductive technology (ART) institutions, physicians’ credentials, IVF cycle volumes and pregnancy rates, staffing levels, facility size, and site configuration. Consequently, by the end of 2019, only 70 ART institutions in China had obtained PGD accreditation.

(2) Inadequate technical platforms and limited service offerings: Currently, more than 400 assisted reproductive technology (ART) institutions in China are only able to provide first- and second-generation in vitro fertilization (IVF) services. These institutions lack sufficient capacity in building technical platforms for cryopreservation/thawing, embryo culture, embryo screening, and embryo transfer. To better meet the application requirements for preimplantation genetic diagnosis (PGD) accreditation, they need to increase investment and enhance their capabilities in developing these technical platforms.

(3) Inadequate institutional management and operational capabilities, resulting in low operational efficiency: The management and operation of assisted reproductive technology (ART) medical institutions encompass multiple aspects, including hospital infrastructure development, patient service management, medical staff management, and equipment and supplies management. Particularly in patient-facing and physician-facing services, many institutions suffer from non-standardized service processes and a lack of personalized care, leading to poor patient experience. Furthermore, the informatization of medical staff management is insufficient, resulting in untimely dynamic monitoring of clinical practices; consequently, traceability in the event of medical malpractice is delayed.

(4) High-quality physicians and laboratory technicians are concentrated in leading institutions, resulting in an unbalanced distribution: Physicians and laboratory technicians are the core elements determining the quality of assisted reproductive technology (ART) medical services. The "Technical Standards for Human Assisted Reproductive Technology" require clinical physicians to possess professional knowledge in clinical female reproductive endocrinology and gynecological ultrasound techniques, as well as technical competencies in follicular ultrasound monitoring, ultrasound-guided transvaginal oocyte retrieval, and open abdominal surgery. Laboratory technicians must have theoretical knowledge in cell biology, embryology, genetics, and related disciplines, along with cell culture skills, and must master the laboratory skills required for human assisted reproductive technologies. It takes seven to eight years to train an experienced ART physician or laboratory technician. However, since general ART medical institutions perform a limited number of IVF cycles annually, these professionals cannot efficiently utilize their experience, making them more inclined to join leading institutions.

As can be seen, assisted reproductive technology (ART) institutions face challenges in licensing, talent acquisition, technical capabilities, and operations, necessitating external empowerment to enhance their service delivery.

Upstream Enterprises Empower Downstream Healthcare Institutions to Enhance Service Capabilities

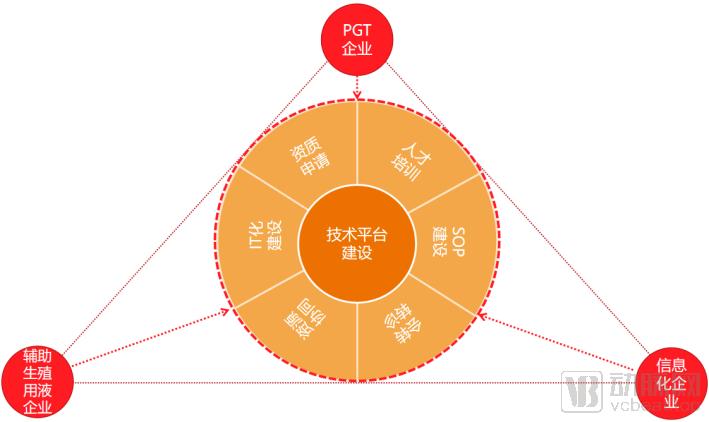

Upstream medical device companies in the assisted reproductive technology (ART) industry chain—primarily those specializing in preimplantation genetic testing (PGT) and ART culture media—as well as information technology firms, are transitioning from mere vendors of technologies and products to service providers offering integrated solutions tailored to the needs of ART medical institutions. The forward empowerment provided by upstream enterprises remains centered on technical platform construction services, leveraging the long-accumulated technological advantages of PGT and ART culture media companies. Building upon these technical platform services, they are expanding their offerings to include IT infrastructure development, PGT accreditation support, medical personnel training, establishment of standard operating procedures (SOPs) for medical services, construction of consultation and referral platforms, and coordination of medical resources.

Upstream Companies in Assisted Reproductive Technology Empower Downstream Enterprises

(1) Technical Platform Construction: The technical platform for assisted reproductive services is primarily a laboratory-based platform, encompassing techniques such as oocyte and sperm retrieval, fertilization, embryo culture, embryo screening, cryopreservation/thawing, and embryo transfer. Among these, embryo screening and cryopreservation/thawing technologies have become key focus areas for construction in various assisted reproductive medical institutions, as they significantly impact pregnancy rates.

(2) IT Infrastructure Development: The intelligent management of laboratories and the automation of embryo culture, screening, and transplantation can enhance the treatment efficiency of IVF. Medical device companies are collaborating with information technology firms to jointly develop intelligent laboratory management systems and IVF automation systems for assisted reproductive technology laboratories.

(3) License Application: The application process for PGD accreditation takes 9–10 years, with stringent requirements regarding the number of IVF cycles, pregnancy rates, staff size, and facility setup. Upstream medical device companies can leverage their technical advantages to provide proper guidance to assisted reproductive technology institutions on how to optimize operations, thereby increasing IVF pregnancy rates and completing a higher volume of cycles.

(4) Personnel Training: Embryo culture, embryo cryopreservation/thawing, and embryo selection are core components of the IVF treatment process and key factors influencing embryo implantation rates; therefore, high standards are required for laboratory technicians.

(5) SOP Development: Standardizing service processes can directly improve the patient experience; therefore, the development of Standard Operating Procedures (SOPs) for assisted reproductive technology (ART) medical services is a key component of service empowerment. The focus of SOP development in ART services is to systematize and standardize various service components, including appointment scheduling and consultation, diagnostic assessment, examinations and tests, and treatment planning.

(6) Referrals and Consultations: During the development of platforms for referrals and consultations in assisted reproductive technology (ART), information technology companies collaborate with medical device manufacturers. These manufacturers can integrate their accumulated expert resources into cloud-based consultation and referral platforms, thereby strengthening the pool of specialist expertise. Furthermore, experts can deliver genetic counseling training to ART physicians at general hospitals through cloud-based training programs, enhancing their professional competencies and enabling them to provide higher-quality genetic counseling services to patients.

(7) Resource Coordination: Issues in assisted reproduction often extend beyond reproductive health to involve gynecological, andrological, and pediatric concerns. Therefore, multidisciplinary consultations involving specialists from reproductive medicine, gynecology, andrology, and neonatology are required during diagnosis and treatment to improve diagnostic accuracy.

After finding solutions to the two major pain points in the assisted reproductive technology (ART) industry—namely, the low level of domestic production of upstream pharmaceuticals and medical devices, and the insufficient capacity of downstream ART medical services—the industry is expected to exhibit the following development trends in the future.

New Healthcare Infrastructure Builds the Digital Ecosystem Foundation for the Assisted Reproductive Technology Industry Chain

To provide intelligent R&D and manufacturing solutions for upstream pharmaceutical and medical device developers and manufacturers. Intelligent R&D encompasses target discovery, compound synthesis, compound screening, drug repurposing, equipment prototype design, clinical trial process management, and big data analysis in clinical settings. Intelligent manufacturing includes digital mold technology, production process design, intelligent material formulation, and intelligent quality control in production.

Provide midstream pharmaceutical and medical device distribution enterprises with digital supply chain solutions and e-commerce platform development plans. The digital supply chain encompasses supply chain process reengineering, smart warehousing, intelligent dispatching, and end-to-end supply tracking and traceability. E-commerce platform development includes SKU management, intelligent customer service, personalized product displays, and big data analytics for sales.

Provide pharmaceutical and medical device companies with digital marketing and internet community-based marketing solutions. Digital marketing for pharmaceuticals and medical devices includes departmental meetings, virtual medical representatives, case collection, physician tools, and academic live streaming. Internet community-based marketing includes popular science education in reproductive medicine, patient communication, adherence management, and targeted matchmaking with assisted reproductive technology institutions.

Provide downstream assisted reproductive technology (ART) medical institutions with intelligent laboratory construction solutions and specialized ART internet hospital construction solutions. The intelligent laboratory features include automated oocyte and sperm retrieval, automated embryo cryopreservation and thawing, and an integrated system for embryo culture, screening, and transfer. The specialized ART internet hospital construction encompasses online appointment scheduling, online consultations, online multidisciplinary consultations and referrals, e-prescribing, and post-consultation management.

Operational Management and Channel Development as Preferred Strategies for Differentiated Growth in Private Assisted Reproductive Services

Private assisted reproductive technology (ART) institutions should leverage their inherent advantages by focusing on operational management and channel development to implement differentiated competitive strategies. In terms of operational management, emphasis should be placed on brand building and patient management. By jointly establishing medical service centers with renowned domestic or international ART institutions or experts, these institutions can enhance their appeal to patients through institutional or expert endorsements. Meanwhile, institutions should utilize internet-based communication tools, such as short videos, to cultivate "influencer" ART specialists, thereby increasing brand visibility. A membership system should be adopted for patient management, offering exclusive value-added services to members, such as full-process medical accompaniment, private physician services, VIP consultation rooms, and VIP wards. This approach ensures that member patients enjoy the optimal medical experience, thereby strengthening patient loyalty and fostering positive word-of-mouth promotion.

The above is an excerpt from the main content of the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free.

I. Industry Overview: Significant Market Potential, Imbalanced Distribution of Service Resources, and Low Localization Rate of Pharmaceuticals and Medical Devices

1. Serving 9.6 million couples with infertility, with public institutions playing a dominant role

2. The industrial chain structure has been established, but the localization rate of upstream pharmaceuticals and medical devices remains low

3. A Supply-Demand Gap of RMB 375.2 Billion Outlines the Blue Ocean for Domestic Substitution

II. Domestic Substitution: Phased and Categorized Progressive Replacement, with a Long Road Ahead for the Localization of Pharmaceuticals and Medical Devices

1. Domestic Substitution of Medical Devices: Culture Media for Assisted Reproduction and PGT Reagents Emerge as Core Areas for Substitution

2. Domestic Substitution of Pharmaceuticals: Ovulation-Inducing Drugs Become the Core of Substitution

3. Case Study: Weituo Bio

III. Service Empowerment: Building a Comprehensive Forward-Looking Empowerment Matrix with Laboratory Development as the Cornerstone

1. Uneven Distribution of Assisted Reproductive Medical Service Resources and Varying Service Capabilities

2. Upstream enterprises provide forward-looking empowerment to enhance the service capabilities of downstream medical institutions

3. Case Study: Yikang Gene

IV. Future Trends: Dual Drivers of Technology and Policy, with Digital Technologies Building Intelligent Services

1. Technological Innovation and Approval Reforms Drive Accelerated Expansion of Domestic Brands’ Market Share

2. New Healthcare Infrastructure Builds the Digital Ecosystem Foundation for the Assisted Reproductive Technology Industry Chain

3. Operational Management and Channel Development as Preferred Strategies for Differentiated Growth in Private Assisted Reproductive Services

Special thanks to Ms. Lin Xiaozhen, Chairwoman of Weituo Biology; Mr. Ren Jun, Chief Technology Officer of Yikang Gene; and Ms. Li Wenhui, General Manager of the Reproductive Health Division, for their strong support in the preparation of this report.

References:

1. “2018 Assisted Reproductive Technology Industry Research Report,” VCBeat

2. “Pharmaceutical Industry: 48 Million Infertile Couples Outline the Blueprint for a Trillion-Yuan Assisted Reproductive Technology Market, Seller’s Market Drives Premium for Leading Players,” Dongxing Securities

3. “Significant Track Advantages: An Emerging Star in International Assisted Reproductive Technology,” Guojin Securities

4. “Focus on the Application of PGD and PGS Technologies in Assisted Reproduction,” Huachuang Securities

5. “Comparative Study on the Practicality of Programmed Freezing and Vitrification Techniques,” by Yu Xiaoguang

6. “Effects of Sequential Culture System and Single Culture System on Fertilization of Human Oocytes and Early Embryonic Development,” by Li Youzhu, Yan Xiaohong, et al.

7. “Jinxin Fertility Prospectus”

8. “Beikang Medical Prospectus”