Capital-Backed Pet Healthcare Firm Files IPO Prospectus Amid Industry Boom

Originally published on: Industrial Internet Thinking Soup, by Zhang Fan, COO of Xiao Yi Pei Qi. Reposted with authorization from VCBeat.

The Pet Economy Is Booming, and So Is Veterinary Care.

“As ducks are the first to sense the warming spring waters, capital is most acute in its instincts.” Led by Hillhouse Capital, multiple top-tier funds have maintained a long-term, steadfast bullish outlook on the pet industry, with sustained investment in the pet healthcare sector.

Fueled by capital, the pet healthcare industry has experienced rapid growth. However, attitudes within the sector toward capital vary widely: some players actively court and exploit it, others view it with anxiety and resistance, some adapt proactively, while still others remain detached observers.

A top-tier capital magnate once said, “Think big, think long,” while a luminary in veterinary medicine lamented, “Capital is ultimately just a passerby.”

Has Capital Truly Bolstered, or Merely "Constrained," Veterinary Healthcare?

Why Is Capital Bullish on Pet Healthcare?

· China's Pet Healthcare Industry

· International Pet Healthcare

How Does Capital Empower Pet Healthcare?

· The “New” in New Ruipeng

· Individual and Chain

How Should Veterinarians Navigate Capital?

· Pet Veterinarian Career Development Path

·Embrace Change Proactively

Emotional Needs, Consumption Upgrading, New Economy

As the wave of singlehood intensifies in China, the solo-living economy continues to surge. Amidst the country’s aging population and declining birth rates, pets are becoming an indispensable part of modern life, serving as companions and emotional anchors for those living alone.

The 2019 White Paper on the Pet Industry shows that the number of pet dogs and cats in urban areas of China has reached 99.15 million. The sudden outbreak of the COVID-19 pandemic in 2020 further highlighted people's need for emotional support, leading to a surge in pet adoption rates.

According to the 2020 White Paper on China’s Pet Industry and iiMedia Research’s Report on the Current Status and Development Trends of China’s Pet Economy in the First Half of 2020, China’s pet market size reached RMB 202.4 billion in 2019 and is projected to reach RMB 295.3 billion in 2020. Notably, the market size doubled over the five-year period from 2015 to 2019, with a compound annual growth rate (CAGR) of 20%.

Ultimately, pets fulfill people’s emotional and psychological needs. Pet owners constitute a relatively high-quality consumer segment within the broader market, characterized by certain income requirements and a willingness to treat their “furry children” as they would their own. This includes purchasing pet food, administering vaccinations and deworming treatments, performing spaying/neutering procedures, and seeking veterinary examinations, treatments, and surgeries when illness occurs.

Accounting for 21% of the pet economy, pet healthcare is an offshoot of the pet industry and serves as a nexus integrating the pet economy with community-based medical consumption services. Statistics show that its market size exceeded RMB 60 billion in 2020. Pet healthcare is no longer merely a traditional “veterinary” sector focused on treating animals; rather, it has become a new economic domain closely tied to consumption upgrading.

The market is large and fragmented, with an urgent need for upgrading.

Drawing on the experience of developed countries in Europe, America, and Japan, the pet healthcare sector has grown in line with natural market demand following the breakthrough of per capita GDP to the $8,000–$10,000 range. Moreover, after capital began flowing into the industry in 2015, it embarked on a path of rapid expansion.

Although China’s pet healthcare sector has expanded rapidly in recent years, with over 1,000 large branded chain clinics emerging, it has also seen the gradual development of more than 100 medium-to-large animal hospitals nationwide that are equipped with high-end diagnostic and treatment devices such as MRI and CT scanners and generate annual revenues exceeding RMB 10 million.

Based on the landscape of over 25,000 pet healthcare institutions across China as of late 2020, significant gaps remain in various aspects, including clinical expertise (with a severe shortage of high-quality veterinarians), management philosophies (particularly regarding digitalization and technological application), and average revenue per store (RMB 1.5–2 million in China versus USD 1.5–2 million in the United States).

Compared with other consumer sectors, the pet healthcare industry has significant entry barriers. Establishing a pet hospital or clinic requires obtaining an “Animal Medical Practice License.” In first-tier cities, animal medical facilities are subject to various restrictive standards, resulting in a large number of hospitals and clinics awaiting license approval. Due to variations in regulatory enforcement across different regions, numerous unlicensed animal clinics also operate widely.

On one hand, demand for pet-related consumer spending is growing at an annual rate of 20%; on the other hand, the supply of high-quality veterinary medical services will remain insufficient for the foreseeable future. The veterinary healthcare sector, which has previously experienced unregulated growth and easy profits, has now reached a stage that necessitates comprehensive industrial upgrading.

Aier Eye Hospital, Topchoice Medical, High Market Capitalization

From a capital perspective, compared with the consumer healthcare chain industry that provides medical services to humans, the veterinary healthcare sector faces fewer constraints than the “golden eyes and silver teeth” vertical ophthalmology chains (e.g., Aier Eye Hospital, with a market capitalization of RMB 250 billion) and dental chains (e.g., Topchoice Medical, with a market capitalization of RMB 90 billion) that have made significant waves in the secondary capital markets. As a result, pet healthcare chains may achieve larger scale and be more easily standardized and replicated.

Although the number of chain pet hospitals acquired through mergers and acquisitions has continued to grow rapidly in recent years, the chain penetration rate of pet hospitals remains low despite years of M&A activity. As of February 2020, there were approximately 22,800 pet hospitals nationwide in China, with leading chains such as New Ruipeng accounting for less than 7% of the market share.

Pet healthcare exhibits characteristics of both the consumer sector and the medical services industry. Particularly in pet healthcare, which relies heavily on veterinary services, the core determinants of successful operations are veterinarians’ clinical expertise, service attitude, management capabilities, and subjective initiative.

The pet healthcare industry, operating at a low level, struggles to meet the constantly growing and upgrading market demand. Industrial upgrading and consolidation in the pet healthcare sector is an inevitable trend foreseeable in the future.

However, regardless of the upgrade model adopted—whether transforming clinics through self-built and M&A strategies benchmarked against U.S. players like Banfield and VCA, empowering veterinary practices via a technology-driven internet model akin to Covetrus (with a $4 billion market capitalization), or developing a uniquely Chinese path for pet healthcare to support clinics—there remain positive, optimistic, and diverse market opportunities.

Over the next 3–5 years, the pet healthcare sector alone is projected to reach a market size of RMB 100 billion and sustain continuous growth. This high-certainty growth trajectory in an industry ripe for transformation and upgrading has attracted significant investment from top-tier capital firms such as Hillhouse Capital and Sequoia Capital.

Why Is Capital Bullish on Pet Healthcare?

As a relatively mature market, the global veterinary services market is highly fragmented.

VCA Inc. is the largest, with a market share of 2.74%, followed by Banfield Pet Hospitals, Greencross Limited, CVS Group Plc, Bergh Memorial Animal Hospital ASPCA, and Animal Medical Center.

In the U.S. pet healthcare chain market, development is relatively mature, and pet ownership penetration far exceeds that of China, with 68% of American households currently owning at least one pet. The American Society for the Prevention of Cruelty to Animals (ASPCA) estimates that the average annual cost of owning a dog is $1,843.

On February 27, 2020, the American Pet Products Association (APPA) announced that annual sales of pet products and services in the United States reached $95.7 billion in 2019, with veterinary care and product sales accounting for $29.3 billion, or 30.6% of the total. The United States has over 110,000 veterinarians (compared to 50,000–60,000 in China), with an average annual income of approximately $80,000 per veterinarian and 3–6 veterinarians per clinic.

In the United States, chain-based pet healthcare primarily takes two forms. The first is the chain pet clinic model, which involves establishing small-scale chain pet clinics within communities. These facilities mainly provide services such as vaccinations, deworming, sterilization, and other routine diagnostic care, with pharmaceutical sales accounting for a significant portion of their revenue. Banfield Pet Hospital is a representative example of this model, currently operating 975 locations and employing 3,500 veterinarians.

Second is the chain pet hospital model, which involves establishing large-scale professional chain veterinary clinics equipped with comprehensive medical devices. In addition to routine diagnosis and treatment, these institutions offer specialized veterinary services, including surgical procedures, oncology, cancer care, cardiology, and veterinary diagnostics. Represented by VCA Antech, this model currently encompasses over 1,000 hospitals and more than 6,000 veterinarians.

According to data from the American Animal Hospital Association (AAHA), there were approximately 30,000 veterinary hospitals in the United States in 2018. Based on the combined store count of 2,000 for the two leading chains, Banfield and VCA, the market concentration of the top large-scale pet healthcare chains in the U.S. is calculated at 2,000/30,000 ≈ 6.7%, which remains at a relatively low level.

As the world’s largest integrated pet food and healthcare conglomerate, Mars, Incorporated employs a multi-brand strategy. It has not only pursued mergers and acquisitions in the pet food sector but also extended its reach across the entire pet industry value chain. The company owns five billion-dollar pet brands, including three pet food brands (Pedigree, Whiskas, and Royal Canin) and, through Mars Petcare, two pet hospital chains (Banfield and VCA).

(Cited from Unicorn Think Tank)

Mars, Inc. twice paid substantial premiums to acquire Banfield, a chain with over 1,000 pet hospitals, and VCA, a chain with more than 800 locations (including the approximately $9.1 billion privatization acquisition of VCA), thereby establishing its strategic footprint in the premium consumer goods sector for the world’s largest food producer.

In the international capital markets, several large family-owned conglomerates have been highly active. Germany’s JAB Holding Company, the world’s second-largest coffee group, has acquired a chain of nearly 1,000 veterinary hospitals across the United States, Canada, Australia, and New Zealand (including major chains such as NVA, VetPartners, and NVC).

From the perspective of future growth opportunities, China’s pet market still holds significant potential compared to those in Europe and the United States. Currently, the household pet ownership penetration rate in China is below 20%, whereas it stands at 69% in the United States and 44% in the United Kingdom. The number of pets in China is under 100 million, with a compound annual growth rate (CAGR) of 23%, far exceeding that of the United States (6%) and the United Kingdom (-1%). Annual per-pet consumer spending in China averages approximately RMB 3,969. In contrast, the U.S. and U.K. markets are relatively mature, with per-pet spending in the United States being about 1.5 times that of China, and in the United Kingdom, 3.6 times higher.

Global giants in the pet industry and major capital players are increasingly bullish on veterinary healthcare, building industrial moats and enhancing industry collaboration.

Benchmarking Against Global Standards: How Capital Has Bolstered the Pet Healthcare Sector in China

As of the end of 2020, China had more than 25,000 pet medical institutions (including some that had not yet obtained animal diagnosis and treatment licenses), and pet hospitals have become a vertical niche sector heavily targeted by capital investment.

Looking back, China’s pet industry truly entered a phase of rapid growth in 2015, when the country’s per capita GDP reached $8,000 and the trend of consumption upgrading became pronounced.

Bullish on the long-term core value of veterinary hospital chains in China’s high-end consumer sector, Hillhouse Capital has continued to inject billions in follow-on investments. Brands such as Bobitang, An’an, Chongyisheng, Meilian Zhonghe, and Ruipeng have experienced rapid growth, leading to a dramatic expansion in chain scale and sparking intense competition among industry players.

In 2016, Ruipeng, which operated 70 directly-owned chain stores, was listed on the National Equities Exchange and Quotations (NEEQ) as the largest pet hospital chain in China with the most branches. Dubbed “China’s First Pet Healthcare Stock,” it attracted hundreds of millions of yuan in investment from multiple institutions, and its network of hospitals expanded to more than 200 within just over a year.

In 2017, the situation reversed. Hillhouse Capital established Lingyu Group, a comprehensive platform dedicated to the pet industry, and began aggressively expanding its market presence. Backed by substantial capital, it rapidly rose from a latecomer to a market leader. According to statistical data, by 2018, China had more than 17,000 pet hospitals. In terms of market share, Hillhouse Capital ranked first with over 700 facilities, while Ruipeng Group ranked second with more than 400.

In March 2018, Zhang Lei, founder of Hillhouse Capital, met with Peng Yonghe in Hong Kong and proposed a merger. On January 23, 2019, the two giants of China’s pet industry market merged: approximately 450 veterinary hospitals under Ruipeng Pet Healthcare Group joined forces with around 700 veterinary hospitals from brands invested by Hillhouse, including Barbie Animal Hospital, An’an Pet Medical Care, and Chongyisheng. This move facilitated the largest-scale open integration of talent, experience, technology, data, and supply chains within the vast industry. Thus, the “aircraft carrier” of the pet industry—“New Ruipeng”—was born.

“Many people may focus more on New Ruipeng’s scale and industry influence, while Hillhouse has always emphasized ‘Think big, Think long,’ paying closer attention to whether such integration is conducive to the long-term development of the industry, whether it can promote systemic upgrades within the sector, and whether it can stimulate industry vitality and foster innovation,” said Zhang Lei, Founder and CEO of Hillhouse Capital. In September 2020, New Ruipeng Group officially announced its latest round of financing. Multiple leading domestic and international institutions, including Tencent, Boehringer Ingelheim, Country Garden Ventures, Xuehu Capital, OrbiMed, Aspex Management, and Lake Bleu Capital, injected hundreds of millions of U.S. dollars into New Ruipeng, valuing the company at RMB 30 billion.

Besides New Ruipeng, another giant in the pet hospital industry, Ruipai Pet, has also continued to attract capital attention.

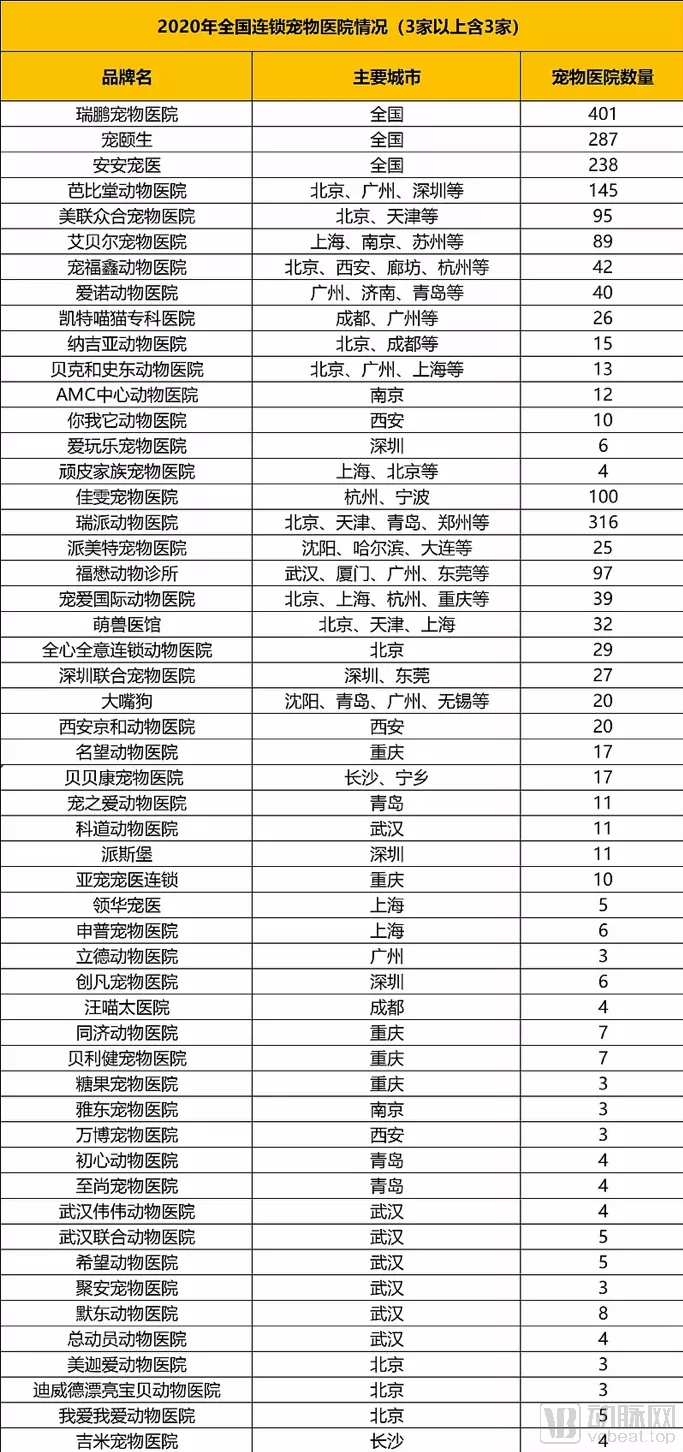

In May 2017, Ruipai Pet Care secured RMB 240 million in strategic investment from Goldman Sachs, Ringpu Biology, and other investors. In May 2018, it received RMB 350 million in strategic investment from Huatai New Industry Fund, Goldman Sachs, and Ruiji Biology. By the end of 2019, Ruipai Pet Care completed its Series C financing led by Mars Petcare. Currently, Ruipai Pet Care is valued at RMB 7 billion and operates more than 300 clinics. In addition to traditional chain brands, Meng Vet Clinic, in which Sequoia China has cumulatively invested over RMB 150 million, completed its Series B financing in 2020 with investments from Matrix Partners China and Yijing Investment. As a new-type chain characterized by standardized operations, brand development, and digital management, Meng Vet Clinic has expanded its network to more than 50 clinics within three years of establishment. 2020 National Statistics on Chain Pet Hospitals by Chongyejia

Image source: Pet Industry Home

1) Among these 51 chain pet hospital brands, Ruipeng Pet Hospital has the largest number of hospitals, with 401 locations. It is followed by Ruipai Pet Hospital, Chongyisheng, and An'an Pet Care, with 316, 287, and 238 locations, respectively.

2) Ruipeng Pet Hospital, Chongyisheng, An’an Pet Medical, Barbie Tang Animal Hospital, Meilian Zhonghe Pet Hospital, Aibeier Pet Hospital, Chongfuxin Animal Hospital, Ainuo Animal Hospital, Kate Meow Feline Specialty Hospital, Najia Animal Hospital, Baker and Stone Animal Hospital, AMC Central Animal Hospital, Niwoita Animal Hospital, Aiwanle Pet Hospital, and Wanpi Family Pet Hospital all belong to the New Ruipeng Group. Notably, the number of pet hospitals under New Ruipeng (1,423 pet hospitals across 15 chain brands) accounts for 8% of the total number of pet hospitals in China;

3) Ruipai operates 316 veterinary hospitals, accounting for 1.9% of the total number of veterinary hospitals in China.

4) Among the emerging players that have risen in recent years, Paimate Pet Hospital operates 25 clinics, Meng Veterinary Clinic has 32 (currently 50), Chongai International runs 39 (rumored to have been acquired by New Ruipeng Group), and Beijing Quanxin Quanyi Pet Hospital manages 29. The industry leader is New Ruipeng Group, followed by Ruipai. However, the combined market share of the top three brands amounts to only 8%, which is roughly equivalent to the proportion of chain hospitals in the industry (11%).

In other words, apart from these three major brands, the remaining players are almost exclusively small, non-chain veterinary clinics. However, it is important to note that established brands such as Ruipeng and Barbietang (under Hillhouse Capital) have been in operation for over two decades.

Adapted from healthcare supply-side reforms in human medicine, New Ruipeng’s core business segment—chain medical services—is structured around the “1 (Central Hospital) + P (Specialty Hospital) + C (Community Hospital)” development model.

In terms of central hospital layout, Beijing’s Barbie Tang International Animal Medical Center and Wanpi Family Animal Hospital’s Deep Medical Center each cover an area of approximately 2,000 square meters or more. In the specialized hospital segment, there are Nagia Cat Specialty Hospital and Kate Meow Cat Specialty Hospital, among others. Furthermore, over 80% of New Ruipeng’s hospitals are small- to medium-sized community clinics.

(A pet healthcare brand under New Ruipeng Group)

In the field of veterinary medicine, New Ruipeng has developed the Runhe Supply Chain Group, Duoyue Education Group, and online consultation platforms represented by Awen Doctor and Chongyi Cloud. In particular, the Awen B2C e-commerce platform, which integrates offline stores as forward warehouses, has become the most significant driver of valuation growth for New Ruipeng in the post-pandemic era. As the saying goes, “In the world of martial arts, speed is paramount.” This principle is vividly reflected in the capital market, where “speed” across all dimensions is the defining characteristic.

With ample financial backing, the scale advantages, brand strength, and group synergies derived from a growing number of chain stores are highly evident, whether through investment in self-built outlets or large-scale mergers and acquisitions.

Standardization is the prerequisite for scaling, while digitalization is the prerequisite for standardization. From a capital perspective, only businesses that can be replicated on a large scale can achieve rapid growth, realize economies of scale, reduce costs, and enhance value. New Ruipeng’s digital innovations encompass business intelligence and operational digitalization. In terms of business fundamentals, a hospital’s operating profit equals foot traffic multiplied by conversion rate, multiplied by average revenue per customer, and then multiplied by the average profit margin. Each parameter has specific metrics and strategies for improvement. New Ruipeng believes that replacing manual decision-making with machine-driven decisions is more conducive to improving hospital efficiency. By leveraging a “central brain” to assign tasks to terminals, standardized instructions can be delivered directly to the frontline with a single click.

If chain hospitals are viewed as a unified entity, leveraging digitalization as the foundation and highly developed organizational collaboration to enhance overall efficiency, increase average revenue per customer, and improve gross profit margins, the logic is sound. However, in actual operation, while the New Ruipeng Group has seen rapid growth in the number of stores and asset scale, some stores have experienced declining profits, reflecting a transitional phase where the single-store profitability model fails to hold. When the strategy of “standardized operations empowered by digitalization” is applied to the pet healthcare industry, what problems have emerged?

Pet hospitals are entirely private, consumer-oriented medical institutions that receive no government policy-based subsidies. Moreover, the average R&D cost for veterinary drugs is significantly higher than that for human pharmaceuticals, inevitably resulting in higher fees compared to public healthcare facilities. This situation, compounded by deceptive practices employed by some unscrupulous hospitals or veterinarians seeking short-term gains, has led to a widespread public misconception that pet hospitals generate exorbitant profits.

From a broad industry perspective, driven by the rapid growth in consumer demand and the relatively limited supply of veterinary medical resources, a diligent veterinarian with three to five years of work experience can establish a profitable pet clinic. With dedicated management, there is a 90% probability of achieving profitability.

Under the support of capital, the core logic of large-scale chains is standardized replication, which enables economies of scale, improves efficiency, and reduces costs.

From the perspective of standard operating procedures (SOPs) for veterinary medical processes, standardized protocols can indeed elevate hospitals with poor operational performance and veterinarians with subpar clinical skills to an industry “normal” level.

But can pet medical services be fully standardized?

Unlike commodity-driven chain pharmacies, veterinary hospitals are fundamentally service-oriented establishments that provide medical care for animals classified as “pets.”

From a medical perspective, unlike specialized clinics in fields such as ophthalmology and dentistry, veterinary hospitals—whether large-scale animal hospitals or community-based pet clinics—are nominally specialized institutions, yet veterinarians in practice provide generalist diagnosis and treatment for a broad spectrum of pet diseases.

From a service perspective, the emotional value of pets is fundamentally different from that of livestock. Pets are more like non-verbal “fur babies,” requiring not only the veterinary surgeon’s medical expertise but also their patience and compassion.

Yet the service itself is the most difficult to standardize.

Much like Haidilao, which is renowned for its service, years of standardization have made it difficult for its service to command a premium; indeed, a growing number of consumers have grown weary of its overly standardized approach.

The clientele of veterinary medicine can be broadly categorized into two groups. One group has relatively high consumption demands, often willing to pay premium fees for more advanced and attentive services. The other group, which constitutes the majority, has basic consumption needs, seeking reasonable diagnostic and treatment services along with fair pricing.

Amidst diverse customer demands and bolstered by capital infusion, the pet healthcare sector could have offered a richly varied landscape, with differentiated diagnostic and treatment services, distinct market segments, and tiered pricing structures to meet the needs of various types of pet owners.

A large pet healthcare chain has accomplished in just six years what foreign pet healthcare chains took 60 years to achieve.

During the rapid integration of acquired clinics, an excessive emphasis on standardization has led to a significant surge in compliance and management costs. The resulting conflict between managerial perspectives and frontline operational philosophies has caused considerable disadaptation among practitioners in the pet healthcare industry.

Should veterinary medicine be more of an assembly-line business, or should it earn reasonable returns and respect through diligent and responsible diagnostic and treatment services?

Shortage of High-Quality Veterinarians Constrains the Development of China’s Pet Healthcare Industry.

Currently, only 38.4% of practitioners in pet hospitals hold a bachelor’s degree or higher, with the majority having educational qualifications below an associate degree. The mass production of specialized talent is challenging; each year, only a few thousand students majoring in relevant fields graduate from agricultural and forestry universities across China. Due to various factors, only a portion of these graduates enter the pet healthcare industry.

Becoming a licensed and qualified veterinarian is no easy task. Currently, there are 50,000 to 60,000 practicing veterinarians in China, with an annual pass rate of 18% for the Veterinary Qualification Examination. Based on the minimum staffing requirement of three licensed veterinarians per pet hospital, the country’s pet healthcare sector currently requires approximately 80,000 to 100,000 veterinarians. As demand continues to grow alongside the development of the pet healthcare industry, a significant talent shortfall emerges each year.

Theoretically, in the pet healthcare market, which faces a significant talent shortage, graduates from specialized institutions should accumulate extensive clinical experience to gradually develop into independent general practitioners or specialists in specific fields. They can then earn equity incentives at their practices or seize opportunities to open their own pet clinics through hard work.

Individuals who choose to become veterinarians are inherently compassionate toward animals, committed to mastering clinical skills, dedicated to refining their diagnostic and treatment philosophies, and focused on delivering truly high-quality care to pets.

Driven by capital, large chains have adopted “internet-style” strategies in their growth, leaving a significant number of veterinarians confused about their values: whether to join these large chains and become mere “cogs in the machine,” or to follow the “open-and-flip” model of opening clinics only to sell them off.

The following paragraphs are excerpted from the personal account of a senior veterinarian:

· In 2016, major capital players exerted significant influence, aggressively acquiring veterinary clinics predominantly operated by individual practitioners, thereby causing unrest among veterinarians and a decline in professional ethics.

· “Opening hospitals, selling them, then opening and selling again…” has clearly become a business model.

· Over the past two years, what I’ve heard most frequently is not about who performed another groundbreaking surgery or set another domestic first, but rather the “capital-fueled wealth myths” of certain individuals selling their hospitals, buying luxury cars, marrying beautiful women, and living lives far removed from those of ordinary veterinarians.

·Veterinarians are not wealthy, yet they exhibit an extraordinary dedication to their craft. There is a certain sparkle in everyone’s eyes... Is it “idealism”? And what is the “sparkle” that shines in veterinarians’ eyes today?

· “Detached from the down-to-earth commitment to serving customers and lacking the perseverance to relentlessly refine technology, a company finds its progress unable to keep pace with its ambitions and its performance failing to match its expansion. The frenzy bought at the cost of reckless capital spending will ultimately prove to be nothing more than a game and a dream.”

Most veterinarians who are passionate about the field of companion animal medicine are professionals with their own values, determined to leverage their skills to deliver high-quality medical services, earn reasonable compensation, and achieve professional growth.

Individual and chain pharmacies each have their own advantages and distinct paths to survival.

The pressure exerted by large branded chains through mergers and acquisitions, along with their close-quarters strategic positioning competition, has gradually eased since the COVID-19 pandemic. Nevertheless, capital-driven large-scale chains continue to consolidate and upgrade the industry through M&A activities, and their advantages in core competencies are undeniable.

With the emergence of demand for upgraded pet healthcare services in higher-tier cities and the sustained, rapid growth of pet healthcare consumption in lower-tier cities, a clear trend toward independent practice is evident. Particularly in small and medium-sized cities, where initial investment is relatively low, market demand is robust, and the payback period is short, experienced veterinarians who are adept at learning and research are increasingly choosing to open their own clinics.

Stores meticulously operated by experts who are truly dedicated to mastering veterinary skills and refining veterinary services offer the highest quality of care. In contrast, non-branded clinics that merely go through the motions and exploit customers with deceptive practices provide the worst service. Positioned in the middle are branded chain clinics; however, there is significant variation in their diagnostic and treatment capabilities, so finding a competent veterinarian largely depends on luck.

From the perspective of current actual pet diagnosis and treatment standards and pet owner experience: individual flagship stores ≥ branded chain stores ≥ independent non-branded stores.

From the perspective of individual pet hospitals, more worthwhile areas to explore include how to achieve annual revenues of RMB 5–10 million per single location while sustaining a strong reputation, how veterinarians can become leading experts in veterinary medicine, and how clinics can upgrade their operations.

Pet healthcare has, in fact, entered a new stage characterized by competition in deep-level services. Defining clear positioning, strengthening core competencies, and improving operational efficiency are essential challenges that every veterinarian aiming to run a successful pet hospital must address.

Dean Xia of China Agricultural University: “Change is an unstoppable trend, as change is the only constant in this world.”

The development of the times is an irreversible trend. The influx of capital into the pet healthcare industry has not only intensified competition and driven mergers and acquisitions, but also introduced advanced concepts of internet and digital empowerment for vertical industries. Regardless of whether these changes are welcomed, they have de facto altered the original competitive landscape of the industry, giving rise to a diversified competitive environment.

From an industry perspective, capital has indeed helped cultivate a large pool of talent, increased the overall income of veterinarians, and significantly narrowed the gap in hardware and standards between China’s pet healthcare sector and advanced international counterparts.

The pet healthcare sector is on a clear upward trajectory, yet uncertainty remains regarding the path of its growth.

Amid such complex changes and developments, individual hospitals face challenges from the systematic strategies of large chain brands. They must focus on businesses with predictable outcomes, enhance industry efficiency, reduce industry costs, and improve service quality through various forms of upgrading and service outsourcing. This represents the core value brought by capital entry into the industry.

Veterinarians should focus on their professional expertise. In terms of clinic launch and operations, they can leverage internet-based service platforms to explore business strategies beyond veterinary medicine, adopting advanced management, marketing, and service concepts driven by digitalization. Only through self-upgrading can they effectively compete with large chain brands and keep pace with the times.

If the clinical services themselves are difficult to standardize, professional service providers are required to implement systematic strategies for improvement. This applies whether addressing procurement convenience and cost-efficiency, equipment maintenance, and working capital support through a supply chain that is easier to standardize; enhancing process management efficiency through digital upgrades of clinics; or conducting brand-integrated marketing campaigns, driving customer engagement and retention, and recruiting and training physicians and medical assistants.

The extension of internet technology and concepts from the consumer sector (C-end) to the business sector (B-end), which enhances operational efficiency and reduces costs, is equally an inevitable trend in the veterinary healthcare industry.

To run a successful veterinary hospital, rather than solely focusing on refining medical skills, it is advisable to actively embrace change and collaborate with industrial internet companies that truly serve and empower the industry. This approach can increase revenue while reducing costs—why not take advantage of such an opportunity?