The Fate of Mature Life Insurance Markets: Restructuring and Strategic Shifts Among America's Top 25 Insurers

Originally published on Yu: Huiguan Tianxia, republished with authorization by VCBeat

What Is the Destiny of the Life Insurance Industry? Life Insurance, Accident and Health Insurance, or Pension Insurance? Let’s Look to Other Developed Markets for Answers.

Today, we focus on the U.S. market.

Low interest rates, compounded by the COVID-19 pandemic, have intensified consolidation and reshuffling in the U.S. life insurance industry. According to statistical reports from the American Council of Life Insurers (ACLI), the number of life insurance companies in the United States has decreased from 814 to 761 over the past five years.

From the perspective of premium data, performance across major business types also diverged. According to preliminary data released by the National Association of Insurance Commissioners (NAIC), the total written premiums for 761 life insurance companies in the United States amounted to USD 1009.509 billion in 2020, representing a year-on-year increase of 6.80%.

Among these, annuity insurance is the largest business segment, with underwritten premiums of USD 289.682 billion in 2020, accounting for 28.7% of total business, a year-on-year decline of 3.76%;

Life insurance achieved premium income of $172.832 billion, accounting for 17.12% of the business, a year-on-year decrease of 0.71%;

Underwriting premium data for individual and group health insurance has not been disclosed, but over the past decade, its net premiums have grown at a compound annual growth rate of just 1.2%. While this may appear unremarkable, given the absence of universal healthcare in the United States, commercial health insurers cover 92% of the U.S. population, underscoring their significant market position.

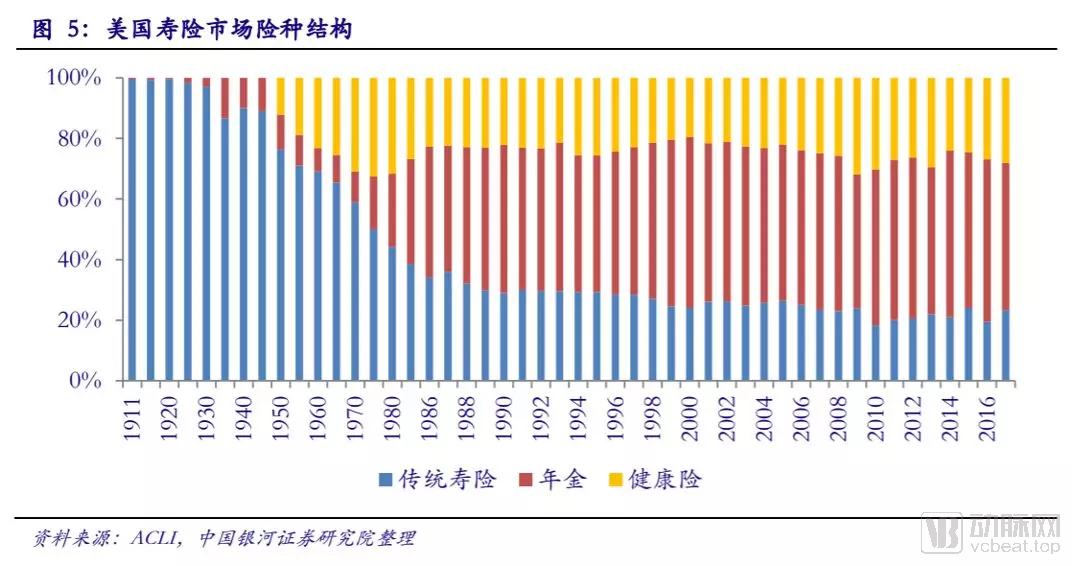

As can be seen, the U.S. life insurance industry has gradually declined, while accident and health insurance and annuities continue to maintain a steady growth trajectory. This trend is shaping the fate of relevant market participants: life insurance businesses are frequently being spun off, whereas annuity businesses are attracting significant capital interest. In the health insurance sector, companies are largely opting for horizontal mergers and acquisitions to bolster their strength in response to competition from cross-industry giants.

This trend also appears to validate a viewpoint from Swiss Re’s sigma report: as economies mature, the primary growth drivers for life insurance will shift toward health insurance and pension insurance (including savings-oriented annuities).

For many years, the U.S. life insurance business has been in a state of continuous contraction. In fact, after 2000, the United States experienced the “9/11” attacks and the bursting of the tech stock bubble, and its economy began to enter a recession. To stimulate economic growth and prevent a recession, the Federal Reserve advocated an expansionary monetary policy, implementing long-term low tax rates and low interest rates, and the U.S. life insurance industry had already begun to decline.

Table 1 Compound Annual Growth Rate of Life Insurance Premiums in the United States by Decade

Data source: American Council of Life Insurers (ACLI).

In 2008, severely impacted by the subprime mortgage crisis, the U.S. life insurance industry slumped and began to experience negative premium growth. Premium penetration also declined from 5.3% in 2000 to 3.1% in 2019. From a company perspective, the return on equity (ROE) of U.S. life insurers dropped significantly after 2008, with the average ROE of the top-ranked life insurance companies by market capitalization falling below 10%.

Traditional life insurance business development has hit a bottleneck, with growth stagnating and the sector becoming a major source of losses, prompting insurance giants to successively divest their individual life insurance operations.

Two Companies Fully Halt Sales:

Voya Financial (VOYA FINANCIAL GRP): On December 31, 2018, Voya Financial, a major U.S. life insurance company, completely ceased sales of its individual life insurance business, shifting its focus to three core segments: retirement planning, investment management, and employee benefits programs.

John Hancock Financial: In September 2018, John Hancock Financial announced it would stop underwriting traditional life insurance policies and shift to selling new interactive insurance products based on fitness and health data tracked by wearable devices.

Two Insurance Giants Opt for Spin-offs:

Metropolitan Group (METROPOLITAN GRP): Recently, MetLife has completely divested its U.S. life insurance business, transferring it to Brighthouse Financial, a company established in 2016. Going forward, MetLife will focus more on serving corporate clients, including corporate insurance, annuities, and employee benefits.

American International Group (AMERICAN INTL GRP): On October 27, 2020, American International Group announced that it would take steps to spin off its life insurance business into an independent company, thereby allowing itself to focus on property and casualty insurance operations.

1 company to undergo a business merger:

Apollo Global Management: In January this year, alternative asset manager Apollo Global Management announced that it would merge with Athene Holding, a life insurance company it founded in 2009. The deal valued Athene at approximately $11 billion and was expected to close in January 2022.

1 Company Sells Off:

Allstate: On January 27, 2021, Allstate sold its life insurance business to the Wall Street investment firm Blackstone Group for $2.8 billion.

By 2020, this downward trend had yet to be reversed. According to data released by the National Association of Insurance Commissioners (NAIC), the U.S. life insurance industry recorded total written premiums of $172.832 billion for the year, representing a year-on-year decline of 0.71%.

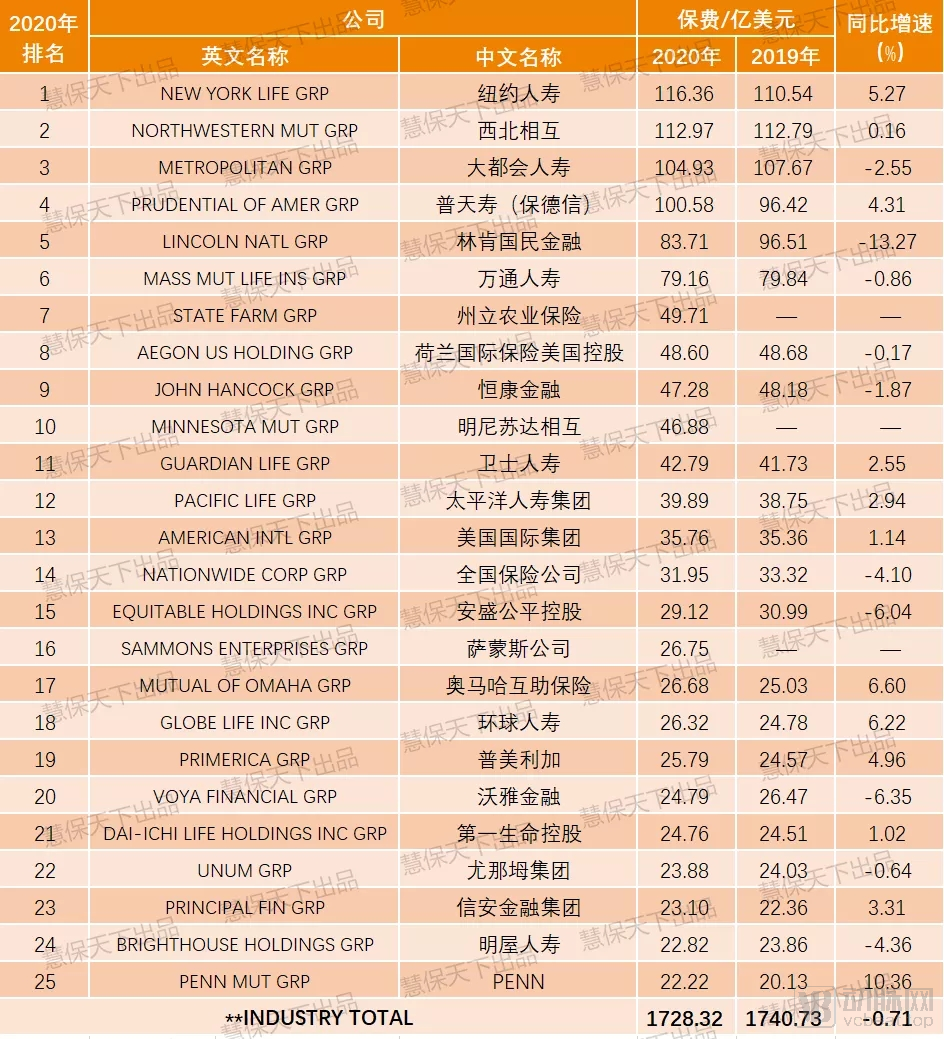

Despite the adverse conditions, not all life insurance companies “underperformed.” Among the top 25 companies operating in the life insurance sector, New York Life emerged as the largest life insurer in the United States in 2020, capturing nearly 6.73% of the national market share and recording $11.636 billion in premium income, with a year-on-year growth rate of 5.27%.

The three large life insurance companies that followed closely behindThe companies are Northwestern Mutual, Prudential (i.e., Prudential Financial), and MetLife, yet their performance varies significantly. Prudential posted a year-on-year growth rate of 4.31%; Northwestern Mutual recorded a year-on-year growth rate of 0.16%; while MetLife experienced a negative growth of 2.55%.

Overall, among the top 25 life insurance companies, excluding three for which no comparable data were available, 10 of the remaining 22 companies experienced negative growth in underwritten premiums.

This already largely represents the overall trend of the U.S. life insurance business, as the top 25 life insurers account for 79.40% of the U.S. life insurance market share.

Table 2: Underwritten Premiums and Year-over-Year Growth Rates of the Top 25 U.S. Life Insurance Companies, 2019–2020

Data Source: National Association of Insurance Commissioners (NAIC).

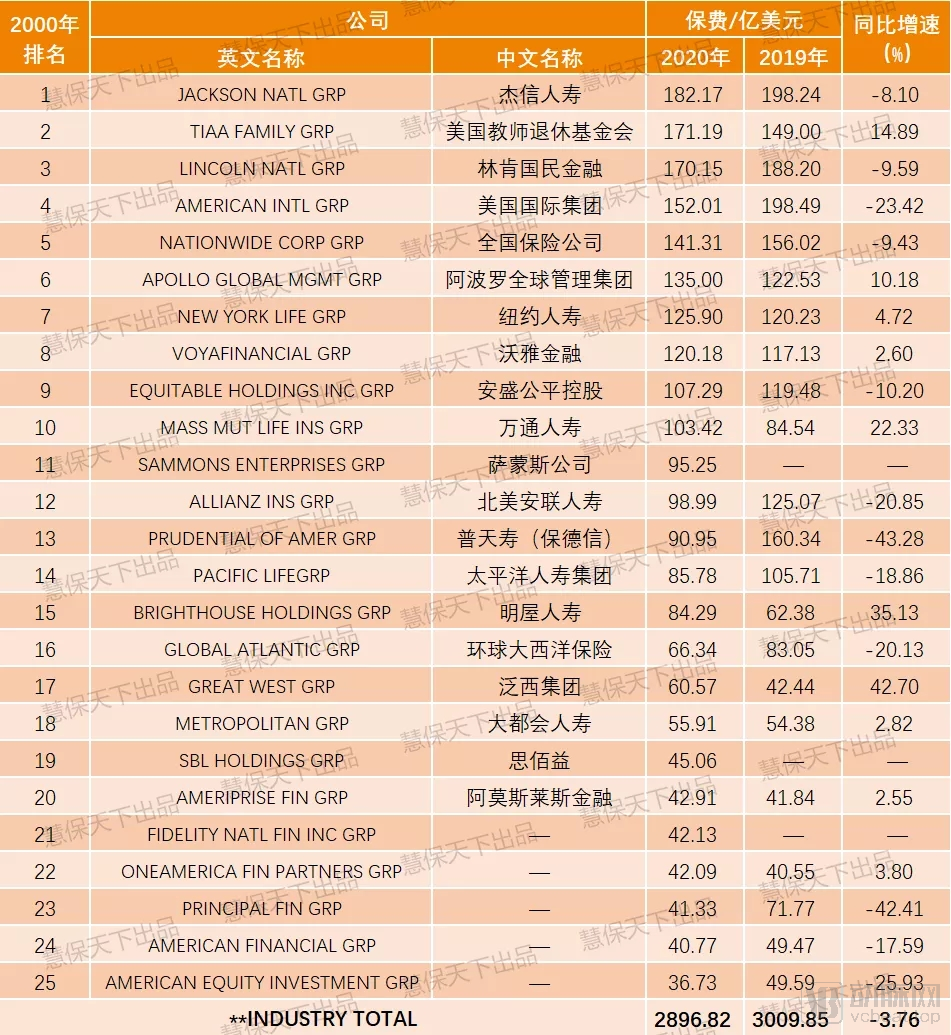

Annuities are the largest product category in the U.S. life insurance market. In 2020, all insurers registered with the National Association of Insurance Commissioners (NAIC) to sell annuities reported annual premiums of $289.682 billion to the NAIC Financial Database, a 3.76% year-over-year decline, accounting for 28.7% of total life insurance premium income, significantly surpassing life insurance, which accounted for 17.12%.

Among the top 25 insurers operating annuity insurance businesses, data for 22 were comparable; of these, 12 experienced varying degrees of decline in underwritten premium income.

The three insurance companies leading the market are Jackson National Life Insurance, a subsidiary of Prudential; TIAA (Teachers Insurance and Annuity Association); and Lincoln National Financial. In 2020, their annuity premium incomes were USD 18.217 billion, USD 17.119 billion, and USD 17.015 billion, respectively, with each holding a market share of over 6%. However, their growth rates varied significantly: both Jackson National Life Insurance and Lincoln National Financial experienced negative growth exceeding 8%, while TIAA maintained a positive growth rate of 14.89%.

Despite a decline in premium income, annuity insurance business remains favored by various types of capital, driven by the socioeconomic conditions in the United States.

Since 1986, spurred by incentives such as tax cuts, exemptions, and tax deferrals under the Tax Reform Act of 1986, and with the post-World War II “baby boomers” (generally referring to Americans born between 1946 and 1964) increasingly turning their attention to retirement planning, the U.S. annuity market entered a phase of rapid growth, ultimately becoming the largest segment of the life insurance industry in the United States.

Especially under the prolonged impact of low interest rates and the COVID-19 pandemic, acquiring high-quality annuity insurance assets has become a common strategy for many large financial groups:

Mass Mutual Life Insurance Group (MASS MUT LIFE INS GRP)

In January this year, Massachusetts Mutual Life Insurance Company (MASS MUT LIFE INS GRP) announced the acquisition of Great American Life Insurance Company and its affiliated subsidiaries for $3.5 billion, with the deal expected to close in the second quarter of this year.

Great American Life Insurance Company, founded in 1872, is a leader in the U.S. annuity insurance market. Through this transaction, MassMutual’s existing annuity business capabilities will be significantly enhanced, supported by Great American’s distribution channels and customer base.

Global Atlantic Group (GLOBAL ATLANTIC GRP)

In February this year, U.S. private equity giant KKR completed the acquisition of Global Atlantic Group for nearly $5 billion. Global Atlantic serves more than 2 million policyholders, offering individual life insurance products and providing annuity products to individuals through a network of banks, brokerage firms, and insurance institutions.

Since the acquisition, KKR has taken over management of Global Atlantic’s investment portfolio, delivering stable and robust returns, thereby further solidifying its position in the U.S. annuity market.

Ameriprise Financial (AMERIPRISE FIN GRP)

On April 12, Amos Reiss Financial announced that it had signed a definitive agreement to acquire BMO’s EMEA (Europe, Middle East, and Africa) asset management business from Bank of Montreal Financial Group (BMO) for $845 million, aiming to increase the overall contribution of wealth and asset management to its diversified operations.

Table 3 Underwritten Premiums and Year-on-Year Growth Rates of the Top 25 U.S. Annuity Insurance Companies, 2018–2019

Data Source: National Association of Insurance Commissioners (NAIC).

The National Association of Insurance Commissioners (NAIC) has not released underwriting premium data for accident and health insurance in 2020, nor detailed data on the top 25 companies in this sector. In terms of net premiums, the compound annual growth rate (CAGR) of U.S. health insurance net premiums over the past decade was merely 1.2%, which appears unremarkable. Nevertheless, the U.S. accident and health insurance market, particularly the health insurance segment, remains significant and should not be underestimated.

As the United States is the only developed country without universal health coverage, commercial health insurance plays a crucial role in providing health risk protection. According to reports, commercial health insurance covers 55% of the U.S. population, Medicare covers 20%, and Medicaid covers 17%, meaning that a combined 92% of the population is covered by either commercial health insurance or government-sponsored health programs.

In the article “Is UnitedHealth Group Worth 1.5 Times Ping An? The Top 100 Listed Insurers by Market Capitalization Worldwide Revealed, with Health Insurers Outperforming Traditional Life Insurers Across the Board,” Huibao Tianxia also pointed out that among the top 100 listed insurers globally, although there are only ten health insurance companies, their combined market capitalization reaches RMB 4.1514 trillion, averaging RMB 415.1 billion per company—significantly higher than that of other types of listed insurers.

In the U.S. life insurance market, health insurance giants have also delivered standout performances. In 2020, the three major health insurers—UnitedHealth, CVS, and Cigna—all ranked among the top 15 life insurers. UnitedHealth ranked fourth with $58.126 billion in underwritten premiums; CVS Health Group came in sixth with $39.292 billion; and Cigna Health recorded $22.071 billion in underwritten premiums, jumping from 16th place in 2019 to 13th.

Moreover, consistent with the robust performance of the U.S. economy in recent years, the three health insurance giants—UnitedHealth Group, CVS Health, and Cigna—have also demonstrated sustained positive performance over the past four years. Their revenues have shown steady overall growth, and while profit growth has experienced slight fluctuations, they have largely maintained strong profitability.

Also, due to their steady development, these companies have carried out a series of M&A transactions in recent years. Through horizontal mergers and acquisitions, they have strengthened their capabilities to resist cross-industry disruption and competition from industry giants such as Amazon and Walmart:

In November 2017, CVS and Aetna completed a merger valued at $69 billion, with Aetna becoming a subsidiary of CVS post-merger.

In 2018, Cigna and Express Scripts completed a $52 billion merger (with Express Scripts becoming a subsidiary of Cigna post-merger).

Table 4 Top 25 U.S. Life Insurance Companies, 2018–2019

Data source: National Association of Insurance Commissioners (NAIC).