2020-2021 China Future Healthcare 100: Decoding Life Through Data

VCBeat

Internet Medical Health Media

Launched in 2015, the “Future Healthcare Top 100” ranking series is the first list in China focused on innovative healthcare companies that are not publicly listed. It was introduced by VCBeat, VB100, and Eggshell Research Institute. The initiative aims to identify Chinese innovators who truly represent the future of healthcare, uncover the core driving forces behind China’s future healthcare industry, and promote innovation and transformation within the health and medical sector.

Building on previous editions, this year’s rankings and awards feature refined classification criteria, expanded award categories and selection quotas, and, for the first time, separate individual and institutional awards. Centered on the two major award programs—the Pengcheng Awards and the Weilan Awards—the selection highlights the leadership and innovative vitality driving the development of the healthcare industry.

2020-2021 Future Healthcare Top 100: The main list comprises the Top 100 Chinese Innovative Medical Devices, Top 100 Chinese Innovative Medical Services, Top 100 Chinese Digital Health, and Top 100 Chinese Innovative Pharmaceuticals, categorizing and evaluating non-listed companies in the healthcare sector.

The Main Lists are selected using the VB100 Value Assessment Model, with the company’s latest valuation as the core assessment metric. The evaluation comprehensively considers performance across four primary indicators—human resources, knowledge resources, key partner resources, and market performance—encompassing a total of 17 secondary indicators. Through a process that includes company applications, institutional recommendations, cross-verification, and expert review, five Main Lists are curated, featuring a total of 500 listed companies.

2020-2021 Future Healthcare 100 · Pengcheng Award: “Pengcheng” symbolizes a bright and promising future. The award’s signature color is orange, the primary brand color of VCBeat (Beijing Danhuang Technology Co., Ltd.), representing prosperity, strength, wisdom, and vitality. It embodies the spirit and demeanor of enterprises and institutions in the healthcare sector that strive for innovation and progress.

The Pengcheng Awards primarily target investment institutions, service providers, and enterprises in the healthcare sector. The awards comprise seven institutional categories: Annual Medical Device Investment Institution, Annual Biopharmaceutical Investment Institution, Annual Healthcare Services Investment Institution, Annual Digital Health Investment Institution, Annual Strategic Healthcare Investment Institution, Annual Emerging Healthcare Investment Institution, and Annual Healthcare Financial Advisory Institution; as well as four enterprise categories: Enterprise of the Year, Leading Enterprise of the Year, Innovative Enterprise of the Year, and High-Potential Enterprise of the Year.

2020-2021 Future Healthcare Top 100 · Weilan Award: “Weilan” signifies a promising future. The award’s signature color is azure blue, the primary color of VB100, symbolizing courage, composure, rationality, and perseverance. It represents the qualities and spirit possessed by innovative healthcare professionals, investors, and entrepreneurs.

The Weilan Awards primarily recognize innovative and pioneering professionals in the healthcare, investment, and entrepreneurial sectors. The awards feature six individual categories: Healthcare Investor of the Year, Young Healthcare Investor of the Year, Leader Entrepreneur of the Year, Innovative Entrepreneur of the Year, Emerging Entrepreneur of the Year, and Innovative Hospital Director of the Year.

2020-2021 Future Healthcare 100 · Main List

2020-2021 Future Healthcare Top 100 · Pengcheng Award

2020-2021 Future Healthcare 100 · Weilan Awards

Interpretation of the Future Healthcare Top 100 List

1. Affected by the pandemic, consumer healthcare services reliant on brick-and-mortar stores have declined, while demand for veterinary care remains robust.

2. Overall valuations in the healthcare industry have declined, with capital becoming more rational; companies commanding high valuations place greater emphasis on early-stage accumulation of resources, funding, and technology, as well as business model exploration.

3. In addition to the agglomeration effect of industrial clusters, the healthcare sector in central and western China is significantly driven by policy orientation.

4. 24 Unicorns Valued at Over RMB 338.9 Billion: Digital Health Sector Prolific in Unicorn Creation, Shanghai Emerges as a Hub

5. The medical services sector had the highest total valuation, reaching RMB 294.845 billion, with over 80% of the listed companies having been established within the past five years.

6. Digital health companies require the shortest time to make the list and are more likely to achieve high valuations during their growth stage.

7. Guangdong and Jiangsu Have Become the Third Major Incubation Hubs for Medical Devices, Following Beijing and Shanghai

8. The in vitro diagnostics sector remains hot, while domestic medical robots are accelerating their practical application

9. Anticancer Drugs Show Promising Prospects, and the Cell Therapy Market Is Growing Rapidly

10. Cross-industry Internet Giants Enter the Wearable Device Market, Intensifying Competition

Based on the four main lists of the 2020-2021 Future Healthcare Top 100 previously released, we will conduct a comprehensive analysis of data for 400 companies, including their valuations, geographic locations, most recent funding rounds, key business sectors, and founding dates.

1. Medical Services Top the List in Total Valuation, with Innovative Pharmaceuticals a Close Second

The combined valuation of the four lists—Medical Services, Innovative Devices, Digital Health, and Innovative Pharmaceuticals—exceeded RMB 1 trillion. Among these, the Medical Services list had the highest total valuation. Companies in the medical services category primarily include integrated online healthcare service platforms, as well as consumer-oriented medical service providers specializing in dentistry, medical aesthetics, maternal and infant care, pet healthcare, assisted reproductive technologies, tumor-related nursing services, and consumer-grade genetic testing.

Unlike physical clinics in sectors such as medical aesthetics and dentistry, which are struggling to survive, online chronic disease management platforms have experienced substantial user growth due to the impact of the COVID-19 pandemic. During the outbreak, the risk of cross-infection associated with offline medical visits and restrictions on travel for healthcare made services offered by chronic disease management platforms—such as epidemic prevention education, online consultations, psychological counseling, follow-up visits for chronic conditions, and medication delivery—highly popular. According to data released by the National Health Commission in March, the volume of internet-based diagnoses and treatments at hospitals under its administration increased 17-fold year-on-year during the epidemic, while consultation volumes on some well-known internet healthcare platforms rose more than 20-fold.

Moreover, as the “loneliness economy” continues to gain momentum, pet-ownership attitudes evolve, and consumption upgrades take hold, China’s pet-owning population is expanding rapidly, making the pet economy a new hotspot. In 2020, investor enthusiasm for the pet healthcare market remained strong; although the number of financing deals was lower than the peak in 2018, several large-scale funding rounds emerged.

In the pharmaceutical sector, recent years have witnessed a significant increase in the number of innovative drugs approved in China and a marked shortening of approval timelines, thanks to reforms in the country’s drug review and approval system. As a result, China’s innovative drug industry has entered a period of rapid development. Driven by numerous favorable policies, not only has the market launch of innovative drugs accelerated, but their commercialization process has also gained momentum. Commercialization capabilities are becoming increasingly critical in future market competition. Whether in national reimbursement drug list (NRDL) negotiations, channel selection, or academic promotion, stakeholders are facing new changes brought about by evolving rules of the game.

Overall, the valuations of companies on the Digital Healthcare List lag behind those in the medical services and innovative pharmaceuticals sectors. Ping An Health Insurance Technology also topped the list in 2019. Digital healthcare companies primarily originate from fields such as artificial intelligence, medical big data, health informatics, cloud computing, and wearable technology. Notably, the wearable devices sector welcomed a new major player, Amazon, in 2020. In China, the “Chinese force” in wearable health devices has been further strengthened by the addition of high-potential companies such as OPPO, VIVO, and Goertek.

The trend of import substitution for medical devices, particularly high-end medical devices, is strengthening. Meanwhile, in the primary market, both the number of financing events and the total amount raised in the medical device sector saw a significant increase in 2020. Therefore, although companies in the medical device sector are at a disadvantage in terms of valuation compared to the other three major sectors, the gap is gradually narrowing.

2. Incubation Hubs in Jiangsu and Guangdong See Renewed Surge, Leading the Development of the Pharmaceutical and Medical Device Industries

As in 2019, Beijing and Shanghai remain the premier incubation hubs for healthcare companies overall, offering multifaceted advantages in technology, talent, and capital that provide robust support for corporate growth.

However, in the fields of medical devices and pharmaceuticals, Guangdong and Jiangsu have emerged as the third-largest incubation hubs, respectively, after Beijing and Shanghai. In addition to hosting large-scale medical device industrial parks, Jiangsu Province benefits from its location within the Yangtze River Delta medical industry cluster. It has gathered biotechnology industrial parks such as the Nanjing Bio-pharmaceutical Valley and the Suzhou BioBAY (Suzhou Industrial Park Biopharmaceutical Industry Park), providing technical, talent, and infrastructural support for the research and development of innovative drugs in Jiangsu.

In Guangdong, Guangzhou Science City + Knowledge City, Guangzhou International Bio Island, Zhuhai Biomedical Technology Industrial Park, and the National Health Technology Industrial Base are all bolstering the development of the pharmaceutical industry.

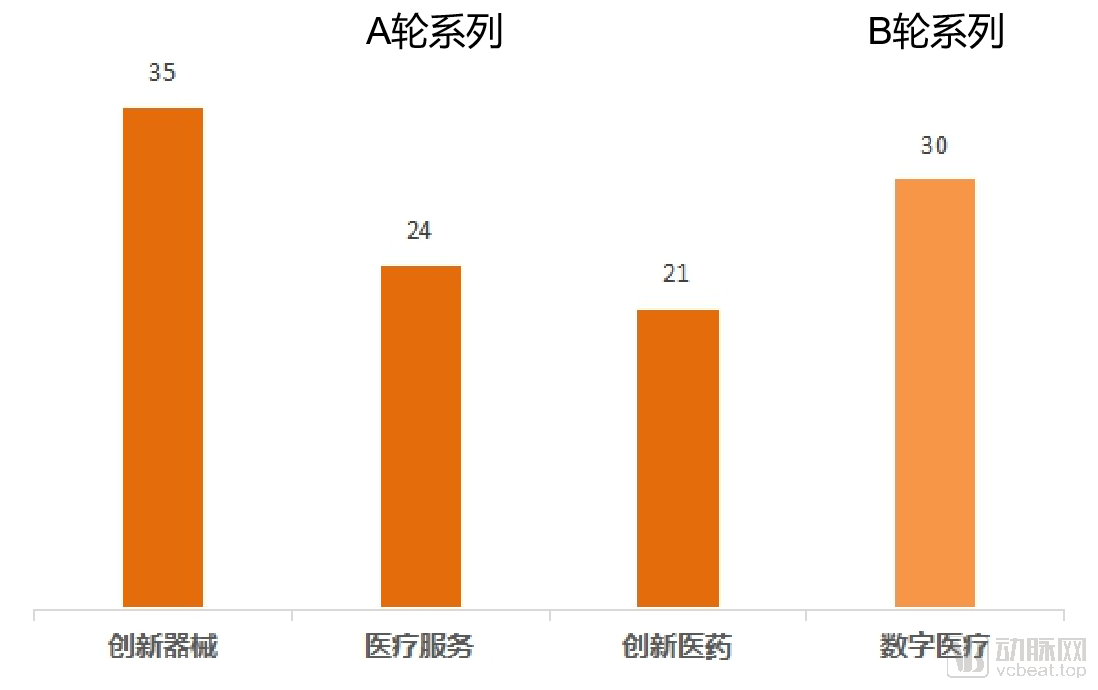

3. Compared with the other three major sectors, digital health companies are more likely to achieve high valuations during their growth stage

Funding rounds are closely tied to a company’s stage of development. Companies that have secured Series A funding typically have just launched their products or services in the market, with their business systems still requiring further refinement, placing them in the growth phase. In contrast, securing Series B and subsequent funding rounds indicates that a company’s business system is relatively mature, its business model has been validated by the market, and it has entered the expansion stage.

An analysis of the highest number of financing rounds among listed companies in the aforementioned four sectors reveals that, although the industry has gradually entered a development phase and capital has become more rational compared to 2019, digital health companies still leverage their market momentum to secure favorable valuations during the growth stage, outperforming the other three major sectors.

It is worth noting that the core competitiveness of most digital health companies on this list is driven by technology, particularly artificial intelligence (AI) applications. As technological barriers continue to rise and are difficult to replicate in the short term, these companies can establish early competitive advantages and design their business systems around core technologies, making their market prospects more predictable. On the other hand, due to the sustained interest in areas such as AI-assisted diagnosis and chronic disease management, capital markets are willing to assign high valuations to these enterprises.

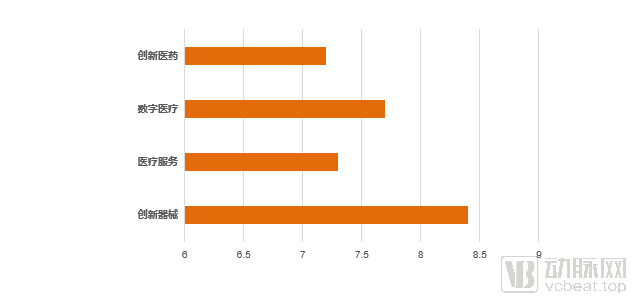

4. Innovative pharmaceutical companies required the shortest time to be listed, while innovative medical device companies required the longest.

From the perspective of establishment date, companies took an average of 7.6 years to be listed on the 2020-2021 Future Healthcare 100 List, which is 0.3 years longer than in 2019. Notably, innovative pharmaceutical companies required the shortest time to make the list, at 7.2 years, compared to 7.6 years for digital health companies and 7.3 years for healthcare service providers.

According to the “2019 Top 100 Future Healthcare Companies: China Innovative Pharmaceuticals List” and the “Digital Healthcare List,” more than 50% of the companies on both lists were founded within the past six years. This indicates that, influenced by the pandemic and related policies in 2020–2021, the pharmaceutical industry surged in popularity beyond digital healthcare, becoming the hottest segment within the healthcare sector and commanding higher valuations.

Innovative medical device companies require the longest time to make it onto the list, with an average of 8.4 years. This is primarily because the companies featured on the innovative medical device list were established relatively early. Furthermore, this characteristic is closely related to the high entry barriers and the extended period required for technological accumulation in the medical device industry.

5. Macroeconomic Trends + Pandemic Impact: Capital Becomes More Rational

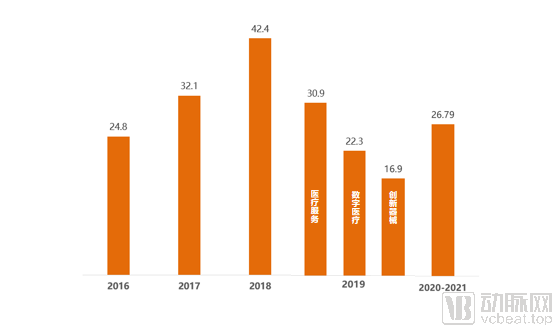

From 2016 to 2018, the average valuation of companies listed on the Future Healthcare 100 Index showed a gradual upward trend, indicating sustained attention from the capital market toward the healthcare industry. The valuations of these companies increased year by year, peaking in 2018. During this three-year period, internet healthcare emerged and developed rapidly, while technologies such as artificial intelligence, big data, cloud computing, and the Internet of Things (IoT) drove innovation and transformation in the healthcare sector, making it highly sought after by investors.

In 2019, the overall macroeconomic growth rate began to decline. The healthcare industry was also affected by the broader macroeconomic environment, with capital markets becoming more cautious and imposing stricter criteria for company selection. This constrained companies’ valuation ranges, leading to a decrease in the average valuation of enterprises listed on the 2019 Future Healthcare Top 100 ranking.

From 2020 to 2021, against the backdrop of the broader economic landscape in 2019, the capital market for the healthcare industry remained cautious. Meanwhile, due to the impact of the pandemic and heightened risk considerations, investors adopted an even more prudent stance.

A unicorn refers to a startup company that has been in operation for less than 10 years and is valued at over $1 billion. Among these, exceptionally high-quality companies with valuations exceeding $10 billion are separately classified as super unicorns. According to the relevant definitions, there are a total of 23 healthcare unicorns across the following four rankings: Top 100 Chinese Medical Services, Top 100 Chinese Innovative Medical Devices, Top 100 Chinese Digital Health, and Top 100 Chinese Innovative Pharmaceuticals.

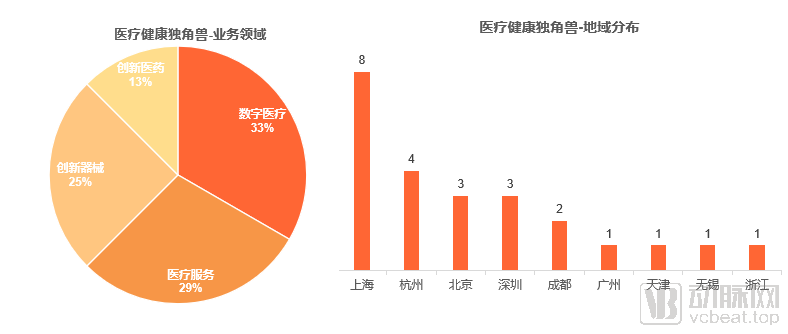

1. Medical services and digital health are evenly matched, with Shanghai as the primary hub for healthcare unicorns

Among these 23 healthcare unicorns, 34.7% (8 companies) are primarily engaged in digital health, 30.4% (7 companies) in healthcare services, while 21.7% (5 companies) and 13% (3 companies) focus on innovative medical devices and innovative pharmaceuticals, respectively.

Compared with the emergence of unicorns in the healthcare services sector in 2019, the digital health sector has demonstrated stronger performance this year. It is worth noting that the rise of unicorns in the healthcare services sector has been primarily driven by three core factors: demographic shifts, economic changes, and evolving disease patterns. In 2020, impacted by the pandemic, offline physical healthcare institutions suffered setbacks in performance, while online healthcare services remained relatively active. Additionally, the remarkable performance of unicorn companies in the veterinary care sector deserves mention. Two such companies appeared on the unicorn list: Ruipai Pet Hospital and New Ruipeng Group, which completed Series C financing and strategic financing, respectively.

Geographically, the concentration of unicorns this year is more dispersed compared to last year. Shanghai demonstrates the strongest incubation capability for healthcare unicorns, while Beijing, Guangdong, and Shanghai collectively account for over 65% (15 companies) of all healthcare unicorns. The top five companies by valuation are, in descending order: Ping An Health Insurance Technology (Shanghai), WeDoctor (Hangzhou), United Imaging Healthcare (Shanghai), New Ruipeng Group (Shenzhen), and MGI Tech (Shenzhen).

2. Over 50% of companies achieve unicorn status at Series C and beyond, with those possessing both core resources and substantial technological accumulation being more favored by capital.

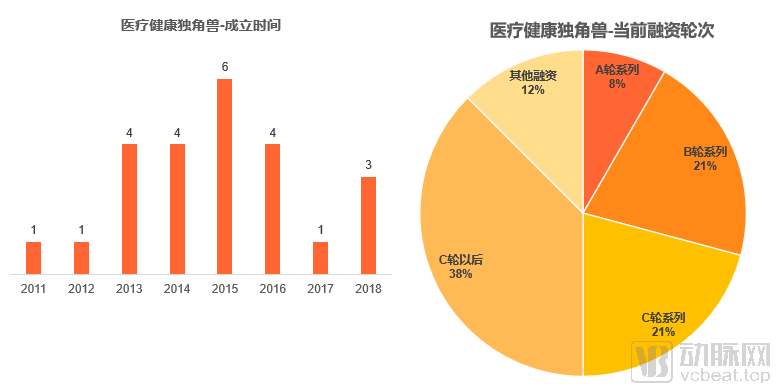

From the perspective of funding rounds, 56% of the companies (13 firms) reached unicorn status at Series C or later, having completed a total of 4–6 funding rounds. In contrast to 2019, when nearly half of the companies made it onto the unicorn list by Series B or earlier, only 26% of this year’s unicorns secured significant financing in the early stages (Series B or earlier). This group includes Ping An Good Doctor Technology, incubated by Ping An Group, and MGI Tech, which leveraged its parent company’s resources.

Unicorns that have reached Series C and beyond have undergone a period of technological, resource, and market accumulation. For instance, Zhiyun Health, a chronic disease and health management service platform, underwent a mid-course transformation and gradually established a profitable business model. Tai Mei Medical independently developed a comprehensive suite of professional software products and built a technology-driven professional service system, progressively expanding its business coverage to include pharmaceutical R&D, pharmacovigilance, medical affairs, market access, and marketing.

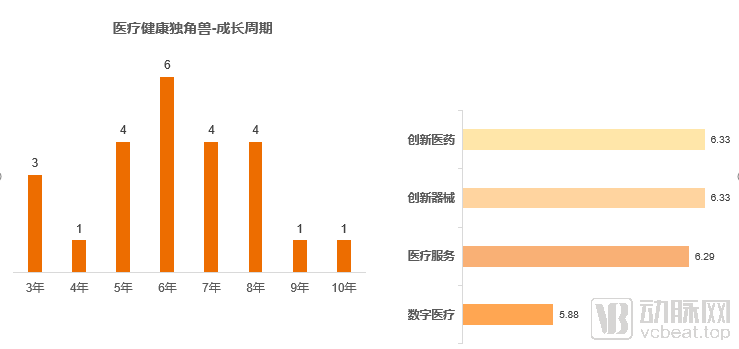

3. Growth cycles are concentrated within 5–8 years, with the shortest cycle being 3 years.

From their establishment (commencement of formal operations) to 2021, the growth cycles of these 24 healthcare unicorns mostly ranged between 5 and 8 years, accounting for 73.91%. Among them, companies in the innovative medical devices segment had the longest average growth cycle at 6.4 years, which was very close to that of companies in the innovative pharmaceuticals and healthcare services sectors. In contrast, companies in the digital health sector had the shortest growth cycle.

Although some high-quality enterprises have attracted significant capital interest and achieved unicorn status within three years of establishment, the time required for such companies to become unicorns has not shortened compared to 2019.

The above is an excerpt from the “2020–2021 Top 100 Future Healthcare Companies Growth Report: Data Report Interpretation—The Calculus of Life.” The report is structured as follows:

I. List Description

II. List Release

1. 2020-2021 Future Healthcare 100 · China Medical Services List TOP 100

2. 2020-2021 Future Healthcare 100 · China’s Top 100 Innovative Medical Devices

3. 2020-2021 Future Healthcare 100 · China Digital Healthcare List TOP 100

4. 2020-2021 Future Healthcare 100 · China Innovative Medicine List TOP 100

III. Overall Analysis of the Rankings

1. Medical services topped the list in total valuation, with innovative pharmaceuticals a close second

2. Incubator Hubs in Jiangsu and Guangdong See Resurgent Interest, Leading the Development of the Pharmaceutical and Medical Device Industries

3. Compared with the other three major sectors, digital health companies are more likely to achieve high valuations during their growth stage

4. Innovative pharmaceutical companies took the shortest time to make the list, while innovative medical device companies took the longest.

5. Macroeconomic Trends + Pandemic Impact: Capital Becomes More Rational

IV. Analysis of Healthcare Unicorns

1. Healthcare Services and Digital Health Share Equal Prominence, with Shanghai as the Primary Hub for Healthcare Unicorns

2. Over 50% of companies achieve unicorn status at Series C and beyond, with those possessing both core resources and accumulated technological expertise being more favored by capital.

3. Growth cycles are concentrated within 5–8 years, with the shortest cycle being 3 years.

V. Data Analysis of the Four Major Leaderboards

1. China Healthcare Services Ranking

2. China's Innovative Medical Device List

3. China Digital Healthcare Rankings

4. China Innovative Medicine List

VI. Analysis of the Growth Trajectories of Top 100 Enterprises

1. Miao Health: Building a Digital Precision Health Management Platform

2. XinYi International: China’s Professional Intelligent Medical Cloud Service Provider

3. Kangbojia: Provider of IT Infrastructure Solutions for High-End Medical Institutions

4. Magnesium Health: An Innovative Provider of Medical Payment Management Services

5. InsurGeek: A Professional Employee Insurance Platform for Enterprises

6. Zhiyun Health: One-Stop Chronic Disease Management and Smart Healthcare Platform

The above is an excerpt from the “2020–2021 Top 100 Future Healthcare Companies Growth Report: A Data-Driven Perspective on Growth Trajectories.” For the full report, please scan the mini-program QR code below.