Emerging Giants in Cancer Early Screening: Rapid Product Iteration and Strategic Approaches in the Data-Driven Era – 2021 Industry Report

Core Viewpoints

From the growth trajectory of malignant tumors, early cancer screening indeed holds promise for altering the course of life.

In an Era Where Strategy Reigns Supreme, Early Cancer Screening Boasts Only Superior Strategies, Not Absolutely Superior Products

Based onThe cost-effectiveness of biomarkers and technological platforms, along with the functionality based on cohort data, defines the strategy.

Multi-omics and Low-Throughput Technologies Shape New Trends in Early Cancer Screening: Data Dominates the Product Landscape

Insufficient Penetration of Centralized Business Models: Direct-to-Consumer (2C) as a Potential Endgame

1Part I Overview and General Introduction

Early Cancer ScreeningEarly cancer screening refers to the screening for early-stage cancers and precancerous lesions in target populations who appear healthy and have not yet exhibited obvious abnormal symptoms. Unlike common genetic testing applications, such as auxiliary diagnosis and companion diagnostics, which aim at clinical evaluation, diagnosis, or grading of tumors, the vast majority of early cancer screening results are negative. In other words, appropriate early cancer screening forms the foundation for early diagnosis and early treatment, helping to alleviate patient suffering, improve prognosis, and even increase cure rates.

Therefore, it is argued that early cancer screening is a truly life-altering intervention.

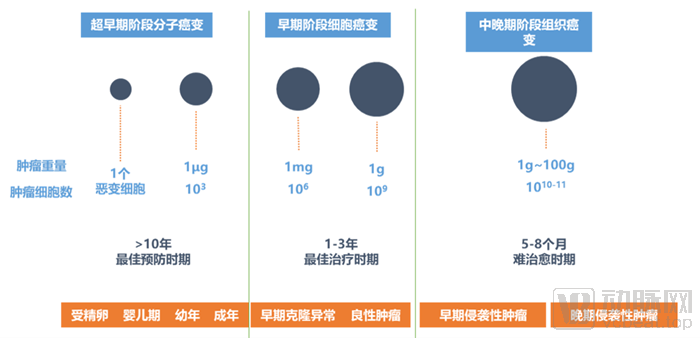

The Prolonged Growth of Malignant Tumors

Typically, the progression of malignant tumors from molecular carcinogenesis in the ultra-early stage to tissue-level carcinogenesis in the middle and late stages spans over a decade. During this period, malignant tumors grow from a single cell into cancerous tissue weighing nearly 100 grams, undergoing three fission stages characterized by accelerated morphological expansion and a progressively compressed timeline. Intervening during the optimal 10-year prevention window and the subsequent 3-year optimal treatment window would undoubtedly significantly enhance the efficiency of diagnosis and treatment throughout the entire course of tumor management.

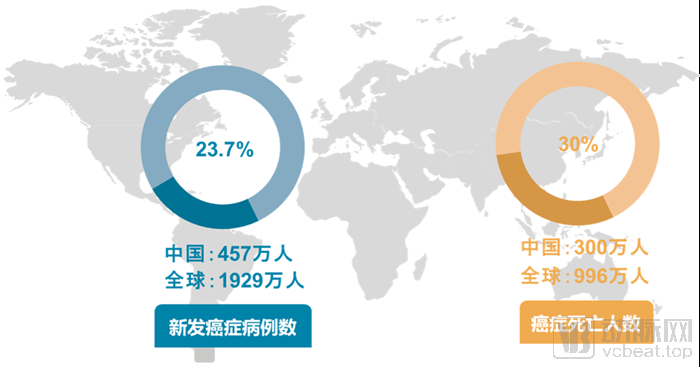

According to the latest 2020 global cancer burden data released by the International Agency for Research on Cancer (IARC) of the World Health Organization, there were 19.29 million new cancer cases worldwide in 2020, including 4.57 million new cases in China, accounting for 23.7% of the global incidence. In 2020, the number of cancer deaths worldwide was 9.96 million, with 3 million cancer deaths in China, representing 30% of the global total. Additionally, according to the latest data published in CA: A Cancer Journal for Clinicians, malignant neoplasms have risen to become the leading cause of death among the Chinese population in 2020.

# The Global Cancer Situation Is Severe

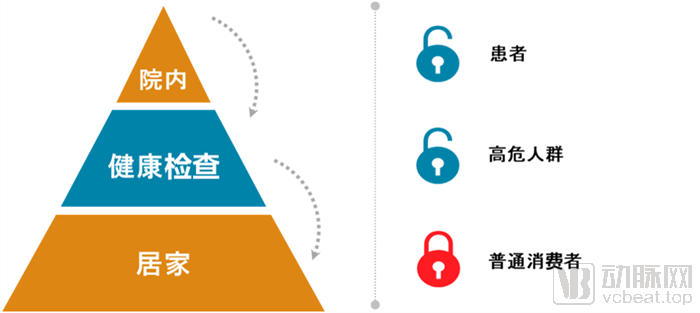

In an ideal scenario, the application scenarios for early cancer screening include in-house testing services conducted by medical institutions and third-party clinical laboratories, direct health screenings for high-risk populations, and convenient at-home testing for general consumers. At present, early cancer screening products are still in the early stages of commercialization, primarily targeting in-hospital patients and high-risk individuals outside of hospital settings.

"Funnel-Style" Volume Surge

From in-hospital settings and health check-ups to home-based care, the population covered by early cancer screening exhibits a pyramid-shaped distribution, with volume gradually increasing from top to bottom. Behind this trend, two key points deserve attention.

First, from the supply side, China’s healthcare system, which is dominated by public medical institutions, struggles to meet the full spectrum of population health needs. Certain medical services characterized by low operational complexity and minimal implementation risk should be systematically diverted to non-public sectors; early cancer screening is one such service.

Second, from the demand side, the regular exclusion of disease risk among the much larger population of apparently healthy individuals represents a significantly greater effective demand compared to those who have already developed symptoms. As awareness of proactive health management continues to grow and under the broader trend of consumption upgrading, the monetization potential of this segment is highly active. Based on an estimated 4.5 million new cases of malignant tumors annually, the population with needs for early cancer screening is ten times that figure.

Generally, the methods employed for early cancer screening primarily fall into two categories: traditional testing and liquid biopsy. Traditional testing modalities mainly include tumor marker assays, medical imaging examinations, and endoscopy. Liquid biopsy, a concept complementary to tissue biopsy, has evolved alongside the emergence of numerous new technologies in the field of precision medicine, offering a more cost-effective solution for early cancer screening. This approach utilizes non-solid biological specimens to analyze tumor-related analytes, such as circulating tumor cells (CTCs) and circulating tumor DNA (ctDNA). In recent years, a key focus of discussion within the precision medicine industry has been how to effectively translate relevant scientific research outcomes into clinical practice to bridge gaps in disease prevention, screening, and treatment.

Traditional Testing vs. Liquid Biopsy

Conventional testing methods have many limitations in the early screening of tumors. Taking colorectal cancer as an example, there are three internationally recognized clinical screening techniques: fecal occult blood test, colonoscopy, and FIT-DNA testing based on molecular detection. Fecal occult blood tests and digital rectal examinations cannot detect early adenomas. The sensitivity of conventional blood-based cancer biomarkers (such as CEA) used in routine health checkups is low, making them unable to detect early signals of colorectal cancer mutations. Requiring all individuals over the age of 50 to undergo colonoscopy is impractical. In the 2018 Urban Cancer Early Diagnosis and Treatment Project, the acceptance rate for colonoscopy was only 15.3%. Compliance among high-risk populations without obvious symptoms remains insufficient. It is necessary to explore screening technologies and strategies suited to China’s specific conditions, so as to improve specificity for high-risk CRC populations and increase the detection rate via colonoscopy.

Among various novel detection methods, liquid biopsy is considered the most promising.

First, liquid biopsy utilizes liquid samples such as blood, urine, or stool, offering simple sampling procedures that significantly reduce costs and minimize patient trauma and risks. Second, unlike medical imaging and endoscopy, which can only examine tumor lesions at specific sites per session, liquid biopsy facilitates simultaneous coverage of multiple tumor types. Third, liquid biopsy is straightforward to perform and yields rapid results, allowing for repeated sample collection to enable high-frequency monitoring.

Furthermore, malignant tumors are heterogeneous diseases. Liquid biopsy can reflect the comprehensive genomic profile of tumors, thereby reducing diagnostic biases caused by tumor heterogeneity while promptly capturing the dynamic changes in tumor progression. In the early stages of cancer (Stage I and Stage II), tumor molecular markers are employed to detect genomic alterations in tumor cells, such as mutations, deletions, rearrangements, methylation, amplifications, and insertions. These findings provide guidance for early diagnosis, prognosis assessment, and selection of therapeutic strategies.

Early Cancer Screening vs. Assisted Diagnosis

However, liquid biopsy-based solutions for early cancer screening also face certain challenges. For instance, their functional positioning is not clearly defined. As most early cancer screening products are still in the nascent stage of industry development, a clear industrial landscape has yet to take shape. Consequently, many industry professionals find it difficult to accurately distinguish between early cancer screening products and tumor auxiliary diagnostic products, often conflating the two.

Clarifying the Boundaries of Early Cancer Screening

In fact, as can be seen from the above figure, there are significant differences between early cancer screening products and auxiliary diagnostic products; this disparity becomes even more pronounced when compared with disease diagnostic products that have more mature clinical applications.

In summary, for early cancer screening products, clinical guidance significance, definitive diagnosis, and intervention measures are all indispensable.

First, it must have clear clinical guidance significance, and the test results must be recognized by clinicians and experts;

Second, there are straightforward diagnostic methods that can clearly inform patients of the next steps they should take and the potential options available to them;

Third, there are feasible clinical interventions to rapidly provide treatment or relief solutions for patients.

“Good wind lends its strength”

In recent years, the high-potential market for liquid biopsy-based early cancer screening has remained a focal point for research and strategic deployment by genetic testing companies both in China and abroad. Citing data from a Guosen Securities research report, as the application of cancer detection expands and coverage among paying populations accelerates, the global NGS oncology market is projected to grow at a compound annual growth rate (CAGR) of 27%, reaching $75 billion by 2035. Within this market, early cancer screening represents the largest segment, estimated to expand at a CAGR of 75% and reach a covered population of 150 million individuals.

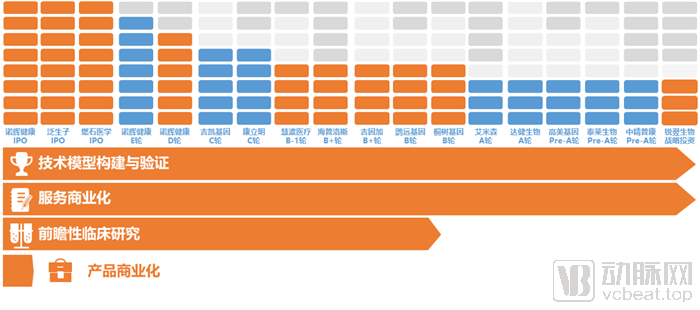

2020–2021 Financing and Industry Progress in Domestic Cancer Early Screening

The figure above provides a brief overview of the capital and product progress of liquid biopsy companies focused on early cancer screening that secured financing in 2020. As of the end of March 2021, all such companies that had completed at least one round of financing in 2020 had finished building and validating their technical models for early cancer screening products and had commercialized their service capabilities. More than half of these enterprises had entered the mid-to-late stages of startup growth (Series B and beyond), with Burning Rock Biotech, Genetron Health, and New Horizon Health listing on stock exchanges in succession. Over half had conducted prospective clinical studies of varying scales, but only New Horizon Health had achieved product commercialization. In other words, while early cancer screening businesses among mainstream domestic manufacturers began generating cash flow, their capacity for scaling remained limited. Throughout this process, external capital played a pivotal role.

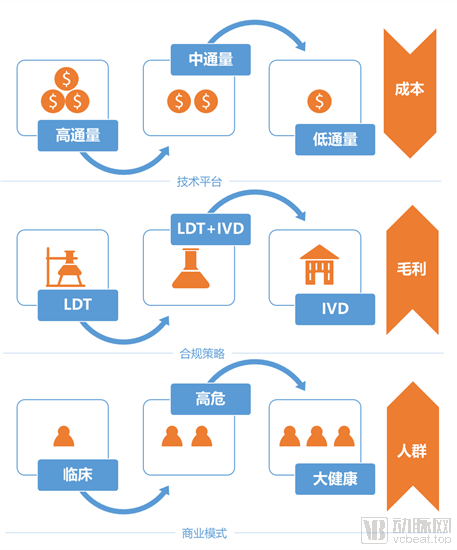

From the past to the future, achieving early cancer screening requires addressing challenges in three areas: technology platforms, compliance strategies, and business models. On one hand, an accurate and stable detection platform is fundamental to ensuring high precision in early cancer screening and diagnosis across various scenarios. On the other hand, the high cost of early screening and diagnostic products can limit their appeal to patients and clinicians in the market.

Evolution of Supply Models in Early Cancer Screening

Overall, early cancer screening is trending from “high-throughput, LDT, clinical” toward “low-throughput, IVD, and broad consumer health.” In this process, changes in technology platform selection will drive down costs, shifts in compliance strategy will improve gross margins, and evolution of business models will significantly expand the target population. At present, “high-throughput + LDT + clinical” remains the developmental stage for most early cancer screening companies; from this perspective, the majority of domestic early cancer screening firms are still in the early start-up phase.

Early Cancer Screening Industry Analysis Model

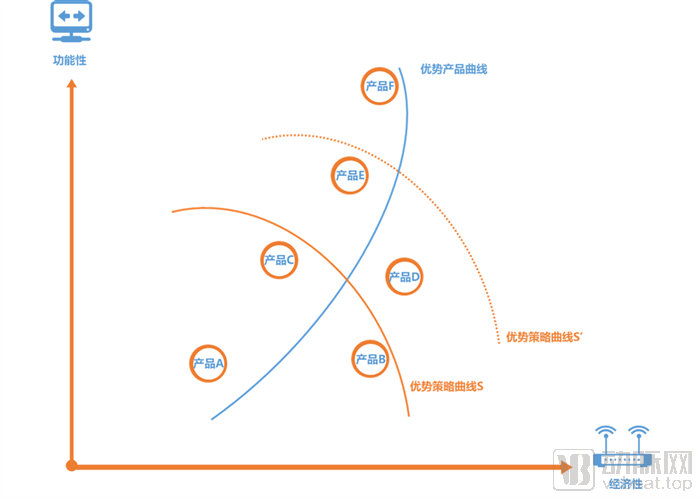

Overall, there is a trade-off between the functional performance and cost-effectiveness of early cancer screening. Under specific technological conditions, the substitution effect between functionality and cost-effectiveness exhibits a diminishing trend, with certain possibility boundaries, thereby forming a corresponding frontier of superior products, as illustrated by the “Superior Strategy Curve S.” Within the scope defined by Superior Strategy Curve S, Product B and Product C hold greater strategic advantages relative to Product A. Prior to iterations in inherent technological capabilities, no product exists that consistently outperforms both Product B and Product C. However, once internal and external technological capabilities improve, the Superior Strategy Curve shifts from S to S’ along the product frontier, ushering in significant enhancements in both functionality and cost-effectiveness across the industry. Consequently, the performance combinations represented by Product D and Product E will become mainstream.

It is evident that comprehensively enhancing technical capabilities requires a prolonged process of breakthroughs and validation, which is even more pronounced in the field of clinical technology. Furthermore, domestic companies engaged in early cancer screening are inherently driven by a service-oriented mindset rather than an engineering one. Consequently, for the foreseeable future, strategy will remain paramount in China’s early cancer screening industry; under current technological constraints, there are no superior products, only superior strategies.

Only enterprises that adopt dominant strategies can secure first-mover advantages and establish market barriers in the fiercely competitive early cancer screening market. If a company insists on focusing solely on its flagship products, it may be constrained by R&D progress and lose critical market share.

Drawing on practices within China’s early cancer screening industry, we can also observe that companies capable of establishing advantages in specific dimensions have all adopted corresponding strategic approaches.

2Part II: Technical Pathways for Early Cancer Screening

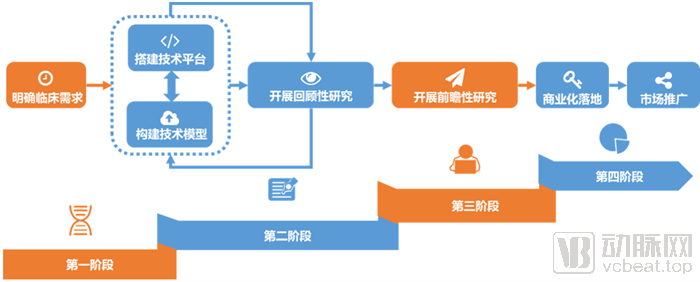

Typically, the clinical translation of various gene sequencing technologies undergoes four stages. This is also true for liquid biopsy-based early cancer screening technologies.

Phase 1: Building the underlying technology platform, which is the most fundamental yet core requirement for gene sequencing companies; Phase 2: Developing models and conducting retrospective studies, i.e., validating the model’s algorithms using known data, thereby laying the preliminary foundation for clinical application; Phase 3: Conducting prospective clinical trials to validate the model from the previous phase in real-world settings, where a larger patient enrollment yields more authentic clinical outcomes; Phase 4: Industrialization and commercial deployment of the product.

Four Stages of Early Cancer Screening Product Development

Although many unresolved questions remain when understanding early cancer screening from the perspective of robust supply and demand and their alignment, approaching the issue from a technological standpoint significantly simplifies the analysis. By accurately describing the biomarkers, technological platform, and medical statistics of an early cancer screening product, one can essentially provide a comprehensive characterization of its functional and economic attributes.

Generally, the three major descriptive dimensions of early cancer screening products are interconnected. The strengthening or weakening of this interconnection affects the balance between the functional performance and cost-effectiveness of these products. A greater variety and quantity of biomarkers, along with higher detection complexity, impose stricter requirements on the technical platform, leading to better performance in medical statistical indicators—that is, stronger functional efficacy but weaker economic efficiency; and vice versa.

Generally, the carriers of tumor early screening biomarkers used for liquid biopsy include four types: circulating tumor cells (CTCs), circulating tumor DNA (ctDNA), exosomes, and microRNA (miRNA).

When used for early cancer screening, each of the four biomarker carriers has its own advantages and disadvantages. Circulating tumor cells (CTCs) have a short half-life and offer strong real-time reflectivity, but their low abundance results in very few being captured. Cell-free DNA (cfDNA)/circulating tumor DNA (ctDNA) is highly representative of different tumor tissues and helps clarify tumor genotyping; however, standardized detection protocols are lacking, and their abundance in the blood of patients with early-stage tumors often falls below the limit of detection. Exosomes are abundant and stable, but technical limitations restrict the sensitivity of their isolation and analysis. MicroRNAs (miRNAs) have demonstrated good predictive value in high-risk populations for lung cancer, but further research is needed to strengthen the evidence of their correlation.

Overall, research on circulating tumor cells (CTCs) and circulating tumor DNA (ctDNA) is relatively mature, with ctDNA demonstrating greater advantages. The primary challenges in CTC detection lie in the difficulties of capture and identification. In the circulatory system of patients with metastatic cancer, there is only one CTC per 1×10⁹ normal blood cells. In contrast, ctDNA offers relatively higher sensitivity for early-stage cancer detection and is currently the most widely used type of biomarker carrier in the market.

In terms of genetic alterations, tumor biomarkers at the DNA level typically manifest primarily as three types: methylation, point mutations, and copy number variations.

In terms of technical platforms, methylation detection technologies are continuously being updated and iterated. Currently, based on differences in sample DNA pretreatment methods, ctDNA methylation detection approaches can be categorized into three main types: (1) pretreatment based on restriction enzymes; (2) pretreatment based on affinity enrichment; and (3) pretreatment based on bisulfite conversion. Among these, bisulfite-based pretreatment for ctDNA methylation detection and analysis is the most mature technology and represents the current mainstream approach. Nevertheless, innovations in pretreatment methods have also emerged. For instance, Genetron Health has adopted a methylation conversion strategy that is milder than bisulfite conversion, enabling the detection of genomic variants while maintaining high-precision methylation detection.

Based on bisulfite treatment, various analytical methods for assessing ctDNA methylation have been developed, such as methylation-specific PCR, real-time fluorescence PCR, and next-generation sequencing (NGS).

In addition, nucleic acid mass spectrometry platforms and rapid FISH platforms are also used for early cancer screening.

Typically, the performance of a cancer early screening test is evaluated using medical statistical metrics such as sensitivity, specificity, diagnostic accuracy, positive predictive value, and negative predictive value.

A higher NPV indicates that individuals can have greater confidence in a negative test result. Taking colorectal cancer screening as an example, if the NPV of an early-screening product is low, it implies an excessively high rate of false negatives, which may lead to delayed treatment for many colorectal cancer patients due to missed diagnoses. For instance, data show that Colotect® achieves a Negative Predictive Value (NPV) of 99.6%, thereby maximizing the avoidance of missed diagnoses. Clinically, screening and health check-ups share similar objectives; their core function is to help examinees rule out health risks, ensure the highest possible reliability of negative test results, and encourage those with positive results to seek medical attention at hospitals.

Interrelationships Among Medical Statistical Indicators in Early Cancer Screening

PPV/NPV are related to sensitivity, specificity, and prevalence. The higher the prevalence, the higher the positive predictive value, indicating that testing is more effective in high-risk populations, with a lower rate of false positives, thereby avoiding overdiagnosis and overtreatment. The lower the prevalence, the higher the negative predictive value, indicating that testing is more effective in average-risk populations, with a lower rate of false negatives, thereby avoiding missed detections and diagnoses.

PPV is also significantly influenced by specificity; when prevalence remains constant, increasing specificity contributes more to improving PPV than increasing sensitivity.

PPV, NPV, sensitivity, and specificity are closely interrelated and influenced by numerous factors. When designing early cancer screening tests, it is essential to balance these metrics to identify the optimal equilibrium, rather than pursuing any single indicator in isolation. Regulatory authorities and the market do not evaluate product performance based on a single metric either; instead, they conduct a comprehensive assessment of all three indicators, taking into account the specific characteristics of the cancer type and the experimental conditions, to determine the product’s value.

In product design, developers must first identify biomarkers, select targets, determine binding sites, and choose the appropriate technology platform. Extensive research has demonstrated that disease onset and progression are associated with multiple factors; complex diseases such as malignant tumors involve pathological processes across multiple levels and dimensions, including the genome, transcriptome, proteome, microbiome, and metabolome.

Analyzing only single-omics data imposes significant limitations on target screening. Achieving precision medicine for complex diseases relies on the accumulation of multi-dimensional data. Once multi-dimensional patient data become sufficiently abundant, comprehensive multi-level and multi-dimensional analysis of multi-omics data will help researchers gain a more thorough and systematic understanding of disease initiation and progression, thereby providing more actionable and effective information for early disease screening, clinical diagnosis, and subsequent drug development and precision medicine.

Building on this foundation, domestic teams in China have integrated multi-omics data—including microbiomics, metabolomics, and genomics—to comprehensively account for genetic and environmental factors. Through meta-analysis, they have identified disease-associated gut microbial communities with relative stability for common intestinal disorders, further considering different microbial kingdoms (bacteria, fungi, archaea, and viruses) and their interactions. For instance, the colorectal adenoma early screening product developed by Rendong Medicine incorporates both bacterial and fungal microbial kingdoms. Furthermore, to achieve higher sensitivity and specificity, advanced bioinformatic denoising algorithms have become a key technological frontier that companies are striving to master.

Furthermore, multi-omics is advancing more deeply toward a “multi-omics+” paradigm, continuously expanding in both depth and breadth. Big data and deep learning algorithms are increasingly being applied to early cancer screening, enabling non-invasive intelligent detection. For instance, QiYunNuoDe has launched a suite of products, including a multi-omics intelligent system, an AI-driven precision health management system, a visualized report management system, and an all-in-one data management appliance. These solutions are expected to achieve specificity and sensitivity exceeding 95% for colorectal cancer detection.

3Part III: Compliance Strategies for Early Cancer Screening

For the development of early cancer screening products, large and stable clinical sample cohorts are just as critical as robust and reliable technology. Hundreds of potential hypermethylation sites must undergo clinical validation to ensure their accuracy and reliability. In other words, regulatory registration of early cancer screening products requires rigorous retrospective and prospective studies.

Among these, retrospective studies refer to technical validation conducted in samples or populations with known disease status, aimed at evaluating the detection sensitivity by stage and cancer type in diagnosed individuals, as well as specificity in cancer-free populations, thereby laying the groundwork for prospective interventional studies.

There is a multitude of tumor targets. Selecting stable and reliable biomarkers as criteria for distinguishing tumor cells from normal cells requires extensive research based on clinical trial data. As previously mentioned, the complexity of tumors makes it highly unlikely to rely on a single molecular marker for early screening. Screening for multiple categories of molecular markers is also challenging; it not only requires identifying suitable markers from a vast array of candidates but also establishing various reliable low-frequency detection technologies. This necessitates forming specialized scientific research and enterprise management teams, establishing collaborative partnerships with multiple leading domestic hospitals, accumulating clinical patient samples, creating a biomarker correlation library, determining molecular markers and detection methods for early diagnosis and screening, and advancing the establishment of Class 100,000 cleanroom laboratories.

Undoubtedly, the development of scientific early cancer screening products must be built upon relatively certain and robust technological foundations. The establishment of a preliminary technical framework is crucial for the implementation of large-scale prospective cohorts, facilitating more in-depth analysis of clinical data in later stages.

In China, early cancer screening companies are racing to establish large-scale prospective clinical trials. Among these, the PreCar trial conducted by Genetron Health and the Clear-C trial conducted by New Horizon Health are the most representative, exemplifying the typical characteristics of large-scale prospective clinical trials using follow-up as the endpoint and gold-standard confirmation as the endpoint, respectively.

Despite the rush of companies to enter the field, large-cohort prospective clinical trials remain high-investment, high-risk endeavors.

First, select scenarios that align with clinical needs. As prospective clinical studies primarily provide evidence for the subsequent clinical application of early cancer screening products, accurate mapping between clinical trials and real-world clinical practice is critical to the success of both the prospective trials and the product itself. However, given the high complexity of real-world clinical settings, constructing comparable virtual scenarios may present unexpected challenges. During this process, developers must employ various strategies to effectively address these difficulties.

Second, precisely define the inclusion criteria for the study population. Fundamentally, prospective clinical studies are outcome-oriented; only when real-world data align with clinical trial protocols can the trial endpoints be achieved. In other words, if the potential study population has only a minimal likelihood of yielding data that meet the required standards, the risk associated with the prospective clinical study will be significantly elevated. Taking positive predictive value (PPV) as an example, if the incidence of the specific malignancy is extremely low in the population selected for the prospective clinical study, it will be exceedingly difficult to reach the corresponding clinical trial endpoints.

Third, allocate sufficient clinical trial management capabilities. Typically, the prospective clinical studies for early cancer screening projects involve a much larger enrolled population compared to traditional clinical trials. If an efficient end-to-end management system cannot be established for such large-scale populations, the likelihood of success for these prospective clinical studies will be extremely low.

4Part IV: Business Models for Early Cancer Screening

Although easily overlooked, for domestic early cancer screening products, product and market have never been disconnected. As early as 2016, New Horizon Health attempted to create a closed-loop service for early cancer screening that integrated online and offline components.

In February 2016, New Horizon Health entered into cross-industry collaborations with multiple industry giants and renowned hospitals, including Baidu Doctor, Taikang Online, ZhongAn Insurance, iKang Guobin, WeDoctor, and Peking Union Medical College Hospital. By integrating the internet with insurance, mobile healthcare, and hospital-based health examination services, the company aimed to construct a comprehensive landscape for early cancer diagnosis and prevention.

Since then, the landscape of early tumor screening has remained unchanged: samples are collected at terminal application scenarios and delivered to medical laboratories via commercial networks.

The only change is that end-use scenarios have become more diversified, with an increasing number of early cancer screening products entering hospitals, and some even originating from within hospital settings. The commercial network has grown richer, with pharmaceutical companies and retail pharmacies joining the ecosystem. Sample types have also become more diverse; as technical platforms continue to be optimized, all existing medical testing platforms can now be utilized for early cancer screening.

Nevertheless, even to this day, the “last mile” of early cancer screening has never been truly bridged. For most potential users, there is an insufficient variety of early cancer screening options available, and a larger pool of potential users remains untapped.

Currently, in the commercialization process of early cancer screening services or products, the B2B2C model has been predominantly adopted. Between manufacturers and end users lies a complex B-side network comprising medical institutions, health checkup centers, insurance companies, and community organizations. The entire system operates as an ecosystem with pronounced centralization characteristics.

Among these, health examination institutions constitute the B2B network for early cancer screening where market competition is relatively mature at present. Currently, most commercialized early cancer screening products are sold by being embedded as specialized test items within premium health checkup packages offered by these institutions. National chain private health examination providers, such as iKang Healthcare Group and Meinian Onehealth, represent the primary settings for this model. For instance, New Horizon Health and Genetron Health have established stable partnerships with iKang Healthcare Group, while Burning Rock Dx’s early bladder cancer screening program has recently been introduced there. Meinian Onehealth, meanwhile, carries out early colorectal cancer screening projects through its equity stake in MyGene. In addition, health management centers within certain public medical institutions also serve as commercialization channels for early cancer screening products. For example, HuiRui Gene’s Lesining was primarily implemented in hospital-based examination centers during the initial phase of the PreCar project.

As the market for limited physical examination institutions becomes increasingly crowded, some manufacturers are attempting to tap into the market for public welfare health initiatives. For instance, companies such as Genetron Health and Burning Rock Biotech have prioritized collaborations with local public welfare programs as a key commercialization pathway. Although public welfare projects operate under distinct business logics and the incidence of different cancer types varies by region, these initiatives remain a significant potential avenue for scaling up early cancer screening. Local governments typically allocate funds for the prevention and control of major diseases within their fiscal budgets. In recent years, driven by the “Healthy China” initiative’s emphasis on encouraging the clinical application of new technologies, local health commissions and disease control departments have shown an increasing tendency to pilot newer technologies that offer superior performance, albeit at relatively higher costs.

Out-of-Hospital: Early Cancer Screening Linked to Insurance 2.0

Compared with the vision from years ago, driven by technology, the linkage between early cancer screening and commercial insurance has become more diversified.

Currently, the role of commercial health insurance has evolved from basic medical expense reimbursement to comprehensive health management that integrates prevention, treatment, and rehabilitation. Due to the nature of cancer, patients often present at advanced stages when symptoms become prominent enough to prompt medical consultation; even with insurance coverage, the likelihood of recovery remains low. By integrating services such as professional early cancer screening, insurance is shifting from passive, back-end compensation to proactive, front-end prevention, thereby moving upstream and extending its reach within the health management continuum.

Out-of-Hospital: Internet+ Early Cancer Screening

Explore "Internet + Healthcare" services in the oncology field, focusing on online follow-up consultations for chronic diseases, follow-up management, patient-provider education, and the research and development of related products. Together, we aim to build a chronic disease management service system for the Oncology Cloud Clinic, leveraging internet healthcare operations, specialized chronic disease management frameworks, and integrated online-offline medical resources, while combining capabilities in tumor genetic testing products, data services, and scientific research support.

In-Hospital: Integrated End-to-End Solutions

With the growing base of cancer patients, increasing penetration of targeted and immunotherapies, and expanding application of next-generation sequencing (NGS) testing, hospitals—particularly specialized oncology hospitals and large tertiary Grade A hospitals—are experiencing rising demand for conducting in-house tumor NGS testing. Some early-stage cancer screening vendors are attempting to deploy all-in-one automated NGS analysis and interpretation systems that connect directly to sequencers, read raw sequencing data, accurately analyze and interpret the clinical significance of variants, and generate user-friendly interpretation reports fully automatically in offline mode, thereby achieving one-click bioinformatics analysis, interpretation, and personalized report generation.

In-hospital: Enter Clinical Guidelines

If integrated end-to-end solutions correspond to the penetration capability of the Laboratory Developed Tests (LDT) model in cutting-edge testing services, then inclusion in clinical guidelines represents the primary strategy adopted after the corresponding diagnostic technologies have obtained product registration certificates. This has been repeatedly validated in diagnostic technologies based on next-generation sequencing (NGS) platforms, and even earlier molecular testing platforms. To some extent, a portion of the demand for early cancer screening will inevitably need to be met by repeating this process.

On-site: Partner Pharmaceutical Companies

Large pharmaceutical companies often have extensive sales networks, either in-house or outsourced. The medical resources connected through these terminals hold certain reusable value for early cancer screening manufacturers striving to penetrate the hospital market. Depending on differences in cooperation duration, target markets, exclusivity, and other factors, early cancer screening manufacturers may establish either close or loose partnerships with large pharmaceutical companies.

As indicated by the preceding analysis, for early cancer screening products to achieve sufficient market penetration, it is crucial to possess the capability to directly serve individual consumers. By shifting the primary application scenarios from medical institutions and check-up centers—which have relatively limited growth ceilings—to health management services with greater potential for rapid scaling, the B2C model can gradually evolve from a subsidiary of the B2B2C model into one of the mainstream models operating on par with it. This represents our current hypothesis regarding the ultimate landscape of the early cancer screening industry.

Indeed, as a health screening product transitions from out-of-hospital settings to in-hospital environments and then expands back out of hospitals, its essential characteristics inevitably change. Overall, high detection accuracy, ease of use, and strong stability constitute the core viability of early cancer screening products.

Currently, end-users exhibit low willingness to actively switch due to established operational habits and the lack of unified testing standards. Consequently, early-screening products that enter the market first will gain a significant first-mover advantage. In other words, the window of opportunity for cancer early-screening manufacturers is narrow. Therefore, at this stage, cancer early-screening companies must pursue a dual strategy: on one hand, they should select scientific biomarkers and technical platforms, accelerate prospective clinical trials, and continuously advance product development toward large-scale commercialization; on the other hand, they must comprehensively identify high-density scenarios with potential users and rapidly extend their service capabilities into these settings.

In reality, whether competing in medical institutions and health checkup centers or integrating insurers, communities, and the internet into the business model through innovative approaches, early cancer screening manufacturers are all aiming to anchor the most high-density user scenarios and strive to establish brand exclusivity.

In an era where strategy reigns supreme, it is imperative to further optimize product strategies, secure strategic positions against competitors, and build competitive barriers.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free.

Part I: Overview and General Introduction

I. Changing Trajectories: Early Cancer Screening Holds a Multi-Billion Dollar Market

II. Innovating and Renewing: Early Cancer Screening Harnesses Innovative Vitality

III. Strategy is King: Early Cancer Screening Targets Healthcare

Part II: Technical Pathways for Early Cancer Screening

I. Biomarkers and Technology Platforms Anchor the Cost-Effectiveness of Early Cancer Screening

II. Multi-omics and Low-throughput Approaches Emerge as New Trends in Early Cancer Screening Technologies

III. Data-Driven Success: Colorectal and Liver Cancer Early Screening See the Fastest Progress

Part III: Compliance Strategies for Early Cancer Screening

I. Retrospective and Prospective Clinical Studies to Define the Role of Functional Tumor Early Screening

II. Proactive Positioning: Advancing Large-Scale Prospective Trials Is the Mainstream Strategy

III. High Investment, High Risk: Three Key Points of Prospective Clinical Research

Part IV: Business Models for Early Cancer Screening

I. From Laboratory to End User: The Last Mile Gap in Early Cancer Screening

II. Leveraging B-side Networks, the Centralized Model Shows Insufficient Penetration

III. The Endgame Hypothesis for Early Cancer Screening: Directly Serving the Consumer Market

Part V: Typical Cases of Early Cancer Screening