Innovation Report on China's Pharmaceutical Digital Marketing Services Industry 2021

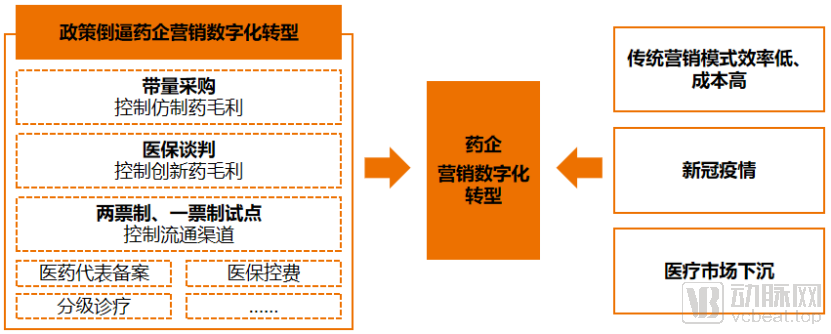

Since 2017, the implementation of policies such as volume-based procurement, national reimbursement drug list (NRDL) negotiations, the “two-invoice” system, pilot programs for the “one-invoice” system, and compliance regulations has gradually steered China’s prescription drug market—particularly the generic drug segment—away from its long-standing high-margin business model. As profit margins have been progressively compressed, the pain points of traditional labor-intensive marketing models, namely high costs and low efficiency, have become increasingly apparent. With the decentralization of healthcare services, the primary care market has become a contested arena for pharmaceutical companies. However, primary healthcare institutions are generally small in scale, widely dispersed, and located in remote areas, making it difficult to effectively reach this market through traditional marketing methods. In contrast, digital marketing offers advantages such as low cost, high efficiency, broad coverage, and traceability, enabling pharmaceutical companies to cover a wider market more efficiently at lower costs while meeting compliance requirements. The COVID-19 pandemic in 2020 severed offline interactions between medical representatives and physicians, significantly accelerating the development of digital marketing.

What value has the digital marketing industry for pharmaceuticals in China delivered? What are the representative business models, and what are their respective advantages and disadvantages? Why have the results of digital marketing fallen short of expectations? What are the future trends?

VCBeat Research Institute provides a comprehensive analysis of the pharmaceutical digital marketing industry from multiple dimensions, including industry background, industrial analysis, issues and challenges, future trends, and typical case studies, with the aim of delivering valuable industry insights to stakeholders.

In the “2021 Report on Innovation in the Digital Pharmaceutical Marketing Services Industry,” we present seven key perspectives on the current development of the digital pharmaceutical marketing sector. Below is a brief interpretation of the full report:

1. Multiple factors, including volume-based procurement policies, corporate demands for cost reduction and efficiency improvement, the pandemic, and the penetration of healthcare markets into lower-tier regions, have driven the industry’s rapid growth in recent years.

2. The domestic pharmaceutical digital marketing services industry is still in a relatively early stage of development. Accumulating data and leveraging digital tools are current needs for pharmaceutical companies, while marketing to existing physician resources remains the mainstream approach.

3. Factors such as pharmaceutical companies’ insufficient understanding of and investment in digitalization, the limited reach and conversion effectiveness of service providers coupled with difficulties in evaluation, and physicians’ lack of motivation to change prescribing habits have resulted in digital marketing outcomes falling short of pharmaceutical companies’ expectations.

4. Offline pharmaceutical sales representatives will continue to exist in large numbers for the long term, and the integration of online and offline marketing is the mainstream trend.

5. Digital marketing service providers with resources from leading pharmaceutical companies will have greater competitive advantages in the future

6. Patient-centric digital marketing will accelerate in the future

7. The Ultimate Form of Future Platform Companies: Large-Scale Comprehensive Medical Service Platforms

Chapter 1: Market and Policy Pressures Drive Digital Transformation in Pharmaceutical Companies

The digital pharmaceutical marketing services industry is still in its early stages of development, transitioning from traffic-driven product promotion to deeper, more precise, and intelligent digital marketing. Policies such as volume-based procurement, national reimbursement drug list negotiations, and the two-invoice system, coupled with the inefficiency, high costs, and compliance risks of traditional marketing models, the impact of the pandemic, and the trend of healthcare market penetration into lower-tier cities compressing pharmaceutical companies’ gross margins, are driving the digital transformation of pharmaceutical marketing.

1

Digital pharmaceutical marketing generally excludes over-the-counter (OTC) drugs and health supplements. This is primarily because OTC drugs and health supplements can be directly advertised to consumers, and secondly, because the market size of prescription drugs far exceeds that of OTC drugs and health supplements. Therefore, the digital pharmaceutical marketing discussed in this article refers specifically to the digital marketing of prescription drugs.

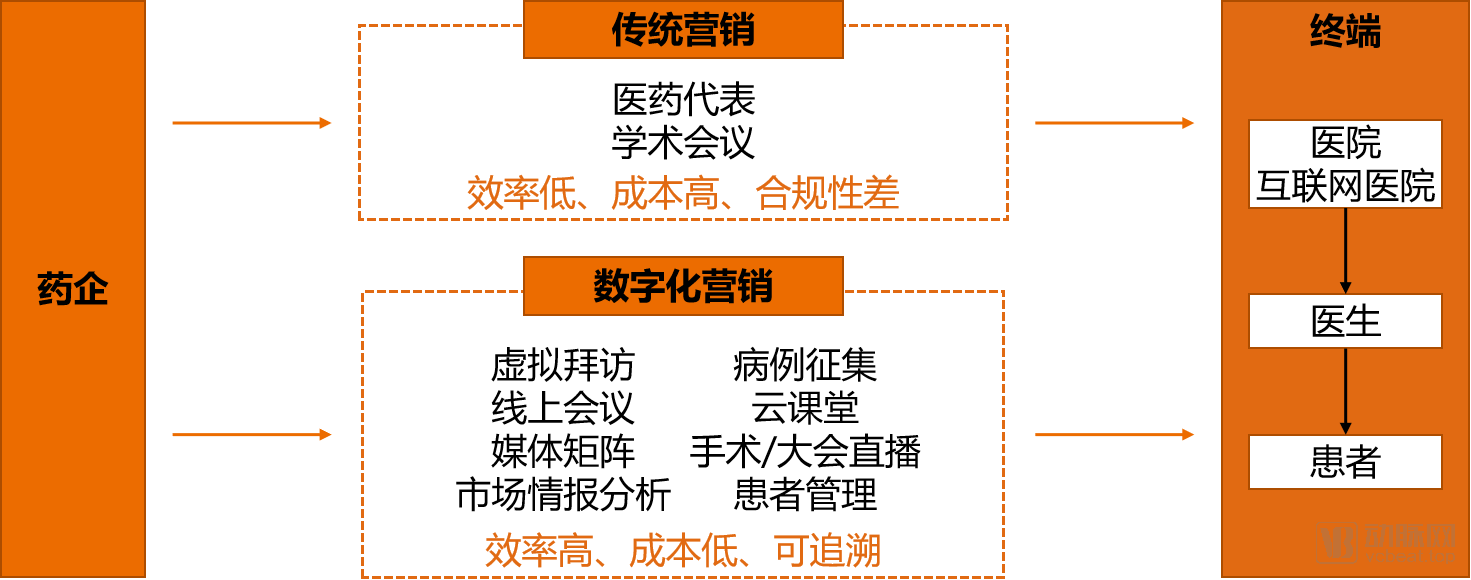

Digital Marketing in the Pharmaceutical IndustryDigital marketing in the pharmaceutical industry primarily refers to the online promotion of prescription drugs by pharmaceutical companies through digital systems, including virtual physician visits, online academic conferences, and analyses of the latest academic advancements, with the aim of boosting sales. Most pharmaceutical companies leverage third-party service providers to facilitate the growth of these related businesses. The primary target audience for digital pharmaceutical marketing is physicians. The objective is to enhance physicians’ awareness and understanding of specific medications through the dissemination of medical knowledge about related products, thereby influencing their prescribing decisions and ultimately driving prescription drug sales.

2

Due to policy impacts, pain points in traditional marketing models, the pandemic, and market penetration into lower-tier cities, the era of high gross margins for pharmaceutical companies has come to an end. Digital marketing offers high efficiency, low costs, and traceability (meeting pharmaceutical companies’ needs for compliance and effective marketing). To reduce marketing costs, improve efficiency, and ultimately boost sales and profits, pharmaceutical companies are embarking on a digital transformation of their marketing strategies.

Four Key Factors Driving the Digital Transformation of Pharmaceutical Marketing

Comparison Between Traditional Marketing and Digital Marketing

Source: VCBeat

3

The pharmaceutical digital marketing services industry is still in a relatively early stage of development, transitioning from traffic-driven product promotion to deeper, more precise, and smarter digital marketing. Digitalization in the pharmaceutical sector lags behind other industries, presenting significant future market potential, with some companies already beginning to emerge as notable players.

In China, MediWellness, a leading provider in the medical industry and health management services specializing in chronic disease care, was established in 2000. Around 2005, three pharmaceutical digital marketing technology companies were founded. As this period coincided with the boom in CRM system development, some of these enterprises focused on providing CRM solutions to pharmaceutical companies.

On March 17, 2009, the Central Committee of the Communist Party of China and the State Council released the “Opinions on Deepening the Reform of the Medical and Healthcare System,” marking the launch of the new healthcare reform. The reform aimed to basically achieve universal health insurance coverage, establish a standardized procurement mechanism for essential medicines, create a new operational model for primary healthcare institutions, restore their public-welfare nature, improve the compensation mechanism, and eliminate the practice of “subsidizing healthcare with drug profits.” With the initiation of the new healthcare reform, professional physician platforms such as DXY, Medlive, and Apricot Forest, as well as online consultation platforms like Chunyu Doctor, were successively established between 2010 and 2013. By around 2015, the maturation of cloud computing and digital technologies prompted technology-driven digital marketing companies to transition from providing CRM systems to offering SaaS services, thereby sparking a second wave of entrepreneurship among tech-based digital marketing enterprises.

Since late 2017, four rounds of national medical insurance negotiations have been conducted consecutively. The number of successfully negotiated drugs has continued to increase, rising from 36 to 119, while the average price reduction has remained at a high level of 40.0%–60.7%. The volume-based procurement policy, implemented in early 2019, brought an end to the era of high gross margins for domestic generic drugs. Since 2017, digital pharmaceutical marketing has developed rapidly; over the past three years, the market size of China’s digital pharmaceutical marketing sector has surged at an annual growth rate of approximately 20%, marking a period of rapid market expansion.

In 2020, the onset of the pandemic rapidly completed market education, further accelerating the digital transformation of pharmaceutical marketing. During the pandemic, coverage by digital platforms increased by 30%, and internet healthcare experienced an explosive growth period, with nearly 80% of doctors using online platforms to access medical information.

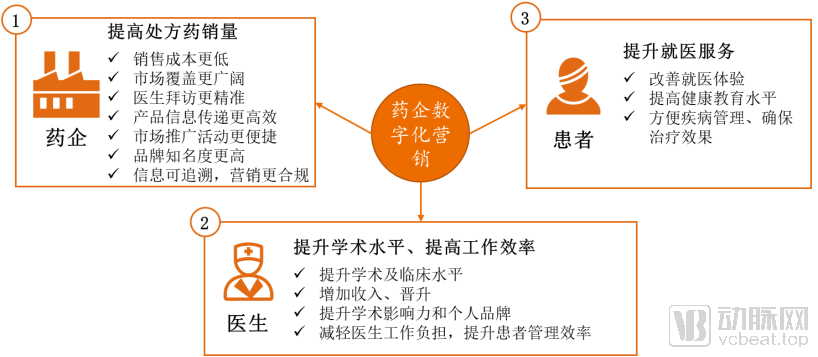

From the Perspective of Pharmaceutical Companies

Digital marketing in the pharmaceutical industry involves comprehensively, precisely, and timely delivering customized information from pharmaceutical companies to physicians, while accurately and objectively feeding back physicians’ opinions to the companies. This completes a digital closed loop of information exchange, ultimately enabling the adjustment of subsequent marketing strategies and boosting sales of prescription drugs for pharmaceutical enterprises.

From the Physician's Perspective

Digital marketing strategies can aggregate academic resources to enhance physicians’ academic and clinical competencies, thereby meeting their needs for career advancement and income growth. They can also facilitate convenient scientific exchange and professional networking, boosting physicians’ academic influence and personal branding. Furthermore, by leveraging productivity tools and patient management solutions, these strategies help standardize clinical practices, alleviate physicians’ workload, and improve the efficiency of patient management.

From the Patient's Perspective

Digital marketing strategies can enhance the patient healthcare experience, improve health education, facilitate disease management, and ensure treatment efficacy.

Digital MarketingMeeting the needs of pharmaceutical companies, physicians, and patients

Data Source: VCBeat

Chapter 2: Introduction to the Digital Pharmaceutical Marketing Industry

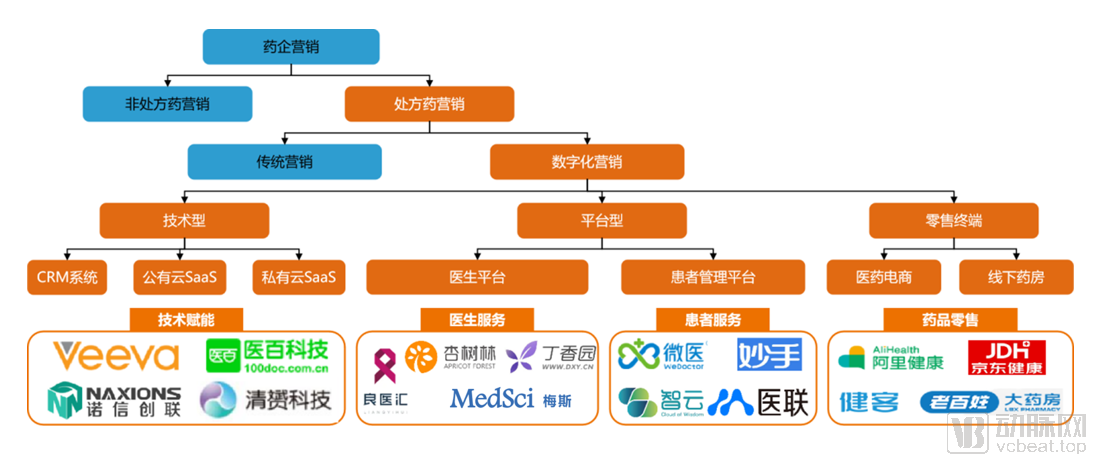

Over the past few years, digital marketing in the pharmaceutical industry has evolved to give rise to a cohort of companies with distinct business models: technology-driven firms, platform-based enterprises, and terminal-focused entities. The crux of digital marketing for pharmaceutical companies lies in meeting and influencing physicians’ needs to drive prescription behaviors, thereby achieving their digital marketing objectives. While different types of companies employ varying business models, pathways, and marketing strategies to implement digital marketing, they all ultimately aim to help pharmaceutical companies empower existing channels, expand incremental channels, or establish an integrated physician-patient ecosystem.

Based on differences in service offerings and business models, pharmaceutical digital marketing enterprises are categorized into three major types: technology-driven, platform-based, and retail terminal-oriented.

CRM System:

Technology companies typically provide tools for enterprise digital marketing services, helping pharmaceutical companies shift their offline marketing scenarios to online platforms, thereby revitalizing their own private domain traffic.

Enterprises provide pharmaceutical companies with basic CRM marketing management platforms, which may be lightly customized to meet the specific needs of the pharmaceutical industry or may be general-purpose CRM systems widely used across various industries.

Public Cloud SaaS Platform:

The company provides pharmaceutical enterprises with a public cloud-based digital marketing SaaS platform, integrating features required for the digital marketing process in the pharmaceutical industry, such as online visits, academic conferences, and case submissions. All users utilize the same digital marketing system and store their information on the same public cloud server.

Private Cloud SaaS Platform:

The company provides pharmaceutical enterprises with a private cloud-based digital marketing SaaS platform, which is further customized according to the specific needs of pharmaceutical companies on the basis of public cloud SaaS platforms, and uses private cloud servers to store related information.

Professional Physician Platform:

This marketing approach relies on an extensive network of physicians, primarily attracting them by offering professional expertise as its key value proposition. Physician platforms have accumulated a large base of medical professionals through provider-facing services such as case portfolios, online training, and academic forums. Additionally, traditional pharmaceutical sales representative functions can be performed by the platform’s virtual representatives.

Patient Education Platform:

A variety of patient education activities and screening management programs can be implemented, including online video-based disease education, mini-programs for disease risk assessment, and a health media matrix, to provide educational and management services for patients with chronic diseases.

As compliance efforts for online prescriptions advance, the prescription drug distribution model combining online sales with offline delivery by pharmaceutical e-commerce platforms has gradually gained recognition. This sales model has also established a unique advantage for pharmaceutical e-commerce in chronic disease management. Pharmaceutical companies are collaborating with these e-commerce platforms to provide whole-course disease management for patients with chronic conditions through online diagnosis and treatment.

Offline Pharmacies:

Offline pharmacies have absorbed a substantial volume of prescription drug demand shifting from hospitals due to the outflow of prescriptions. Similar to pharmaceutical e-commerce platforms, pharmaceutical companies are collaborating with offline pharmacies to help them establish digital chronic disease management systems, thereby enhancing the pharmacies’ capacity to serve patients with chronic conditions.

Key Positioning and Participants in the Pharmaceutical Digital Marketing Services Industry

Data source: VCBeat

From a goal-oriented perspective, pharmaceutical companies’ collaborations with different types of digital firms can be categorized into three approaches: 1. Empowering existing channels (building private-domain traffic); 2. Expanding incremental channels (acquiring public-domain traffic); 3. Connecting to patient endpoints (integrated physician-patient ecosystem).

Empowering Existing Channels:

To better manage and maintain the customer resources they have accumulated over the years, pharmaceutical companies need a comprehensive digital solution to improve their efficiency in resource maintenance. Existing channel empowerment is mostly provided by technology companies in the form of SaaS services, usually on a project basis, offering services such as consulting, implementation, training, and launch to help pharmaceutical companies build private domain traffic and revitalize existing doctor and hospital resources.

Incremental Channel Expansion:

As the size of pharmaceutical sales teams shrinks, the number of physicians each representative must cover is rapidly expanding. The traditional labor-intensive sales model is no longer sustainable, making it an urgent priority for pharmaceutical companies to identify effective channels for reaching physicians. Consequently, internet healthcare platforms and physician communities with extensive doctor resources have become the primary arenas for pharmaceutical companies to expand their reach. In the era of digital marketing, rather than focusing solely on product promotion to the tens of thousands of physicians on these platforms, sales strategies are shifting toward addressing physicians’ needs, such as providing diagnostic and treatment tools, patient management solutions, and continuing medical education.

When pharmaceutical companies choose to collaborate with physician platform-type companies, although most collaborations are conducted on a project basis, their primary objective is to gain greater access to the physician resources available on these platforms.

Integrated Doctor-Patient Care Layout:

As the share of hospitals in pharmaceutical distribution declines, retail pharmacies have absorbed a significant volume of terminal sales shifting away from hospitals, positioning themselves to potentially become the largest patient traffic gateway in the future. Consequently, physical and online pharmacies, as the medication dispensing points closest to patients, have become key intermediaries for pharmaceutical companies to reach patients. Chronic disease medications represent a critical component of pharmaceutical sales. The long-term, stable medication adherence among chronic disease patients ensures that this segment remains the largest market within the pharmaceutical industry. Therefore, collaboration between pharmaceutical companies and pharmacies is particularly vital in the chronic disease sector.

The ultimate goal of digital marketing is to reduce costs and increase efficiency.

Currently, there are two marketing closed loops: (1) physician reach, physician nurturing, trial use, efficacy feedback, and routine use; and (2) patient reach, patient education, and repurchase. Given that physicians have the authority to prescribe medications and prescription drugs account for the majority of pharmaceutical companies’ sales volume, healthcare professionals (HCPs) are currently the focal point of digital marketing in the pharmaceutical industry.

A Complete HCP Closed-Loop Marketing Cycle Is as Follows

(1) Outreach: Pharmaceutical companies reach their target physician audience through WeChat official accounts, academic live streams, and premium columns, while facilitating basic interactions.

(2) Nurturing: At this stage, some physicians establish initial contact with virtual representatives by downloading apps or using enterprise WeChat, and complete identity verification through registration. Consequently, basic tags for these physicians, such as hospital, department, and region, are generated within the data system. Pharmaceutical companies then leverage these basic tags to conduct preliminary marketing activities, such as online launch events and online training sessions.

(3) Pilot Implementation: Establish closer ties with physicians through live-streamed drug promotions, surgical broadcasts, online product launches, and virtual conferences, thereby encouraging prescription issuance.

(4) Feedback: Methods such as online case collection and case sharing can provide timely feedback on drug efficacy. Online case collection enables the rapid accumulation of a large volume of cases, effectively avoiding issues associated with manual data entry, such as poor accuracy and duplicate entries.

(5) Routine Use: Physicians and experts have become regular prescribers of the drug and serve as “key opinion leaders” (KOLs). At this stage, further influence over potential customers is exerted through expert lectures, academic live streams, and other channels, thereby achieving a closed-loop marketing cycle.

Digital Marketing Execution Closed-Loop Diagram

Data source: VCBeat

Additionally, on the patient side, pharmaceutical companies primarily reach, educate, and drive prescription sales to patients by establishing chronic disease management platforms in collaboration with patient management platforms.

Based on different stages of the distribution lifecycle, pharmaceuticals can be broadly categorized into the market launch phase, national reimbursement drug list (NRDL) inclusion phase, and volume-based procurement (VBP) phase. Additionally, from the perspective of utilization patterns, drugs can be classified as general medicines, specialty drugs, and orphan drugs. Digital marketing strategies vary accordingly across these distinct lifecycle stages and drug categories.

Newly Launched Drugs

Whether for specialty drugs, oncology medications, or other categories, newly launched pharmaceuticals are a key focus of digital marketing. As these are new products, offline medical representatives still play a crucial role in building trust with expert physicians at leading tertiary hospitals in first-tier cities, with digital tools serving only as supplementary aids. In second- and third-tier cities, a hybrid approach combining virtual representatives with offline representatives can help new drugs rapidly penetrate from core to secondary markets, enabling swift education and broad coverage. Currently, the launch strategy for innovative and other newly introduced drugs primarily relies on an integrated online-offline model.

National Reimbursement List (NRL) Essential Medicines

The core requirements for this class of drugs are rapid market access expansion and differentiation from competitors. At this stage, it is essential to leverage virtual representatives to rapidly cover hospitals in second- and third-tier cities, as well as primary care institutions, thereby reaching areas previously inaccessible due to limitations in offline human resources. This strategy enables broad coverage and a swift increase in sales volume.

Centralized Procurement Drugs

Digital marketing efforts may be more targeted toward drugs that failed to win bids in the Volume-Based Procurement (VBP). For VBP-winning drugs, digital marketing has limited effectiveness due to restrictions on sales expenses and significant product homogenization. In contrast, for drugs that did not win VBP bids, pharmaceutical companies can mitigate the decline in sales volume and achieve partial volume retention by directing traffic to out-of-hospital pharmacies and encouraging physicians to prescribe medications for purchase outside hospitals.

China's pharmaceutical digital marketing industry is still in a very early stage.

The entire industry is still in a phase of data accumulation and existing customer base maintenance. Therefore, marketing to the existing customer base is currently the focal point of digital marketing for most domestic pharmaceutical companies.

Development Stages, Advantages, and Disadvantages Vary Among Companies of Different Types in the Industry

Technology-driven companies:

Technology-driven companies have experienced robust growth in recent years. Centered on serving pharmaceutical enterprises, they maintain the closest ties with these clients. However, their B2B commercial DNA dictates a project-oriented approach, where competitiveness hinges on the quality and standards of project delivery, resulting in significant reliance on key account relationships and product development. The advantages include: (1) Close engagement with enterprises enables them to secure corresponding projects and returns in line with clients’ annual budgets. (2) They empower offline medical representatives, meet clients’ customized needs, and provide one-stop solutions ranging from content to technology. The disadvantages are: (1) Higher investments in sales and R&D expenses adversely affect long-term profitability. (2) As enterprises deepen their digital transformation, technology-driven firms often struggle to meet pharmaceutical companies’ demands for acquiring incremental customers. (3) The effectiveness of digital marketing by pharmaceutical companies largely depends on operational capabilities for content assets, which increases operational difficulties for most technology- or content-focused companies and makes it challenging to evaluate the outcomes of digital marketing efforts.

Platform-Based Companies:

Platform-based companies are more mature than technology-driven ones. These companies focus on consumer-side (C-end) operations, with traffic volume serving as their core competitive advantage. The mindset and inherent characteristics of the internet industry determine both the advantages and disadvantages of this model. The advantages include: (1) greater suitability for incremental marketing and traffic acquisition; (2) easier evaluation of key metrics such as physician conversion rates and download rates; and (3) numerous innovative collaboration models with pharmaceutical companies, such as chronic disease management and case data collection, which provide new perspectives on digital empowerment. Meanwhile, similar to many traffic-oriented companies, the disadvantages include: (1) weak connections with payers; and (2) limited truly effective traffic for pharmaceutical companies, often resulting in a gap between traffic monetization and sales conversion. Additionally, pharmaceutical companies are generally reluctant to store their data assets on third-party platforms.

Terminal-type companies:

Terminal-focused companies predominantly operate under B2C e-commerce or O2O models. These models are relatively mature and stable, boasting substantial patient traffic on their platforms that can be readily converted into actual sales data. As such, they serve as a powerful complement to traditional digital marketing transformation strategies. Currently, leading pharmaceutical companies, such as Hengrui Medicine, have chosen to collaborate with terminal-focused companies. However, the domestic prescription drug market remains primarily driven by physician-prescribed orders. For most pharmaceutical companies, the current stage of industry development is still too early, and their focus remains largely on how to influence physicians.

Chapter 3: Analysis of Reasons Why Digital Marketing Performance Falls Short of Pharmaceutical Companies’ Expectations

Insufficient Resource Investment

Although pharmaceutical companies have invested in building internal systems such as CRM and ERP, and spent even more on external online marketing campaigns, some enterprises still lack sufficient funding for digital marketing, resulting in limited efforts toward digital transformation.

Organizations and interest systems have not adapted to new digital marketing methods.

Some pharmaceutical companies have failed to adapt their organizational structures and interest systems to new digital marketing models, and they often lack professionals who possess expertise in both pharmaceutical marketing and internet marketing. In China, digital marketing initiatives within pharmaceutical firms are typically led by the marketing department; however, digital marketing is a strategic imperative for the CEO, extending beyond the sole responsibility of the marketing department or medical representatives.

Information lacks appeal; data utilization is insufficient.

Many enterprises deliver messages in repetitive formats with monotonous content, leading physicians to ignore them entirely; some even unfollow accounts or uninstall apps upon receiving such posts. The vast amounts of data generated through digital marketing remain largely underutilized, primarily due to issues concerning data quality, authenticity, and analytical capability. Currently, the industry is still in the phase of data accumulation, far from reaching the stage of true big data application, thus failing to provide effective guidance for business operations.

Low Number of Active Users and Low Engagement Response Rate

Whether in physician communities or doctor-patient platforms, the number of active users is often insufficient. In the past, a large number of companies engaged in data fabrication, inflating figures, or adopted strategies involving massive subsidies and aggressive offline promotional campaigns to artificially boost the reported number of registered physicians. Sustained outreach to target physicians, whether online or offline, remains challenging. Regardless of the total number of registrations, each outreach effort can only reach a small fraction of physicians. Moreover, across all channels, even with a large physician base, campaign response rates typically do not exceed 8%.

Without a robust sales and operations team, it is difficult to help enterprises achieve incremental growth.

The process of converting physician engagement into prescriptions is complex; it cannot be achieved through mere occasional interactions, but rather requires high-frequency engagement that addresses physicians’ professional interests. Without a robust sales and operations team, a platform with only a base of physician users will struggle to help pharmaceutical companies drive incremental growth.

The Difficulty in Evaluating the Effectiveness of Digital Marketing

Whether it is for converting direct sales volumes or enhancing internal efficiency, current digital marketing solutions struggle to provide quantifiable or intuitive evaluation metrics. Furthermore, the complexity and professionalism inherent in pharmaceutical marketing dictate that while digital marketing can make significant inroads in reaching physicians, human involvement remains essential for actual sales conversion. Consequently, many services and products offered by vendors are perceived merely as tools by pharmaceutical companies, which indirectly hampers the pace of industry development.

Doctors’ demands for information quality and the experience of medical practice and care are continuously increasing.

Physicians often work at a fast pace with tight schedules, leaving them little time to absorb product information. As the channels for accessing digital information become increasingly diverse, doctors have growing expectations regarding information accessibility, service quality, and their overall clinical and patient-care experience. They often seek a single platform that can meet all their needs, which places high demands on the content quality of medical information platforms.

Digital marketing methods lack sufficient driving force compared to traditional marketing approaches.

The knowledge and convenience physicians gain through digital marketing cannot be directly linked to any specific prescription drug, and the benefits derived from digital marketing are not direct financial gains but rather an indirect enhancement of self-worth. Lacking tangible incentives, the marketing of prescription drugs has become increasingly challenging. Although kickbacks are becoming harder to offer and are steadily declining, such incentive-driven practices remain highly tempting to certain segments of the medical community.

Chapter 4: Analysis of Future Trends in the Digital Pharmaceutical Marketing Industry

Unlike other industries, pharmaceutical marketing is a highly specialized and high-frequency endeavor. Influencing physicians is not an instantaneous achievement but rather a continuous process of engagement and conversion. Therefore, offline professional medical representatives continue to play a vital role in facilitating in-depth communication. This is particularly true for newly launched innovative drugs, which require medical representatives to conduct face-to-face visits with key opinion leaders in core cities. This necessity stems from the fact that, over the course of industry development, many outstanding medical representatives have already established trust-based relationships with top-tier target customers.

On the other hand, the practice of kickback-driven sales remains difficult to eradicate; more stringent penalties are the solution to this problem.

From the perspective of pharmaceutical companies, most currently have a weak grasp of digital marketing concepts.

The entire industry is currently still in the data accumulation stage, let alone leveraging and analyzing big data mining. However, we have also observed that many leading enterprises have embarked on the path of digital transformation. Here, digital transformation refers to the comprehensive digitalization of the entire process, including R&D, production, and sales. With a data middle platform as the foundation and big data-driven decision-making at the core, these companies aim to establish a closed-loop data ecosystem, in which digital marketing constitutes just one component.

This places higher demands on companies providing digital marketing services.

On one hand, it is essential to understand the digital marketing landscape itself; on the other, it is crucial to provide technological empowerment through marketing and data middle platforms. Simultaneously, companies must keep pace with pharmaceutical enterprises’ own transformation in digital mindset and philosophy. In the future, companies that offer robust data-driven solutions and adopt data as a core strategic asset will undoubtedly be more favored by leading pharmaceutical clients.

"Internet+" Chronic Disease Management Still Holds Immense Development Potential

"Internet Plus" chronic disease management has become a valuable supplement to out-of-hospital treatment for patients, and this market still holds significant potential for development. On one hand, the trend of utilizing out-of-hospital pharmacies and seeking outpatient care outside hospitals is gradually taking shape; on the other hand, patients' habits of online consultations and medication purchases are being actively cultivated by various internet giants and specialized third-party online doctor-patient platforms.

Leading pharmaceutical companies also regard patient management as a key component of their digital marketing strategies.

From the perspective of pharmaceutical companies, leading firms such as Pfizer, AstraZeneca, and Hengrui Medicine have adopted patient management as a key component of their digital marketing strategies. It is foreseeable that patient-centric digital marketing will accelerate in growth over the next few years, with an increasing number of pharmaceutical companies choosing this approach to complement traditional marketing methods.

Tech-Driven Digital Marketing Service Providers Focus on Top-Tier Clients

We assess that technology-driven digital marketing service providers will remain sales-oriented in the short term, with a primary focus on top-tier clients. Currently, profits within China’s pharmaceutical industry are increasingly concentrating among leading enterprises. On one hand, these leading pharmaceutical companies have monopolized a significant pool of talent specializing in innovative drugs; on the other hand, the continued advancement of volume-based procurement has substantially compressed profit margins for generic drugs. According to previous research and estimates by VCBeat, the future market size of the pharmaceutical digital marketing industry is projected to reach RMB 8–10 billion. The majority of this revenue is expected to come from top-tier pharmaceutical company clients, as they possess greater profit margins to allocate budgets and view digital investment as an ongoing process. This provides digital marketing service providers that secure resources from leading enterprises with a stable revenue stream, thereby reducing their need for extensive marketing expenditures in the broader market.

Key Accounts Drive Technological Advancements in Digital Marketing Service Providers

In addition, the high expectations and demand for innovation in digital marketing from key clients will drive technological advancements among digital marketing service providers, creating a virtuous cycle that further solidifies their competitive advantages.

The ultimate end-state of platform-based service providers is a comprehensive service platform.

We anticipate that the ultimate landscape for platform-based service providers will be dominated by a few comprehensive platform companies. The future industry trend indicates that comprehensive medical platforms (such as DXY, Miaoshou Doctor, and Medlive) will delve deeper into vertical sectors to enhance their professional and service value in specific niches, thereby addressing increasing competition from specialized platforms. Meanwhile, currently specialized medical platforms (such as Good Doctor Hui and MediWeiKang) will gradually expand horizontally on the foundation of solidifying their services within their respective domains, aiming to boost their overall competitiveness. The evolutionary paths of both comprehensive and specialized platforms are driving them toward becoming more extensive and deeply integrated comprehensive service platforms.

Criteria for Judgment

Comprehensive service platforms of the future hold advantages over vertical platforms in both external service efficiency and internal organizational efficiency, representing a more efficient organizational model for the entire industry.

The efficiency of external services determines the breadth and sustainability of revenue streams:

Currently, the profitability models of platform-based companies are more concentrated on the pharmaceutical enterprise side and the patient side. For pharmaceutical companies, product development often involves multiple pipelines. During the promotion phase, the initial cost of achieving a breakthrough for any single product is similar; however, comprehensive platforms offer lower customer reuse costs and facilitate the accumulation of user resources on a single platform. From the patient’s perspective, vertical apps or other carriers struggle to establish strong mindshare. Patients tend to access various service platforms for purposes such as seeking medical consultations, health management, and chronic disease management, rather than downloading specific apps solely for the treatment of a particular disease. Therefore, comprehensive platforms have an advantage over niche vertical platforms in accumulating consumer (C-end) traffic from patients, which helps further expand monetization channels. The efficiency of external services determines the breadth and sustainability of revenue streams.

Internal organizational efficiency determines cost and execution:

Once comprehensive platforms achieve stable profitability in several niche segments, they can temporarily sacrifice profits to compete against vertical-specific platforms when seeking to capture greater market share in a particular vertical. Therefore, even vertical platforms that perform exceptionally well in their niche segments must consider horizontal expansion to gain larger scale advantages. Furthermore, when expanding into service areas for certain rare diseases, comprehensive platforms can launch new businesses at lower costs because their core service systems and external resources are already established, requiring no significant organizational restructuring.

Chapter 5: Case Studies

1

(1) Introduction to Basic Company Information:

Founded in 2016, Yibai Technology launched its core product—the Medical Marketing SaaS Cloud Platform—in 2018. Within just a few years, the company has rapidly grown into China’s leading provider of digital transformation services for pharmaceutical marketing. Leveraging its independently developed, all-scenario, one-stop pharmaceutical marketing SaaS cloud platform, Yibai Technology delivers comprehensive digital solutions to pharmaceutical companies, medical device manufacturers, academic societies, and associations. Covering more than 30 traditional offline marketing scenarios, the platform empowers pharmaceutical enterprises to enter a new era of digital marketing characterized by compliance, exclusivity, efficiency, and enablement.

Core Advantages

Rapid response capability, robust delivery capacity, continuous reinforcement of technical advantages, and establishment of a technological moat.

(2) Corporate Financing Status:

Series A+; tens of millions of USD

(3) Core Products:

One-stop SaaS cloud platform integrating multiple digital marketing tools.

Yibai Technology Digital Marketing Product Portfolio

Data Source: Medibang Technology

(4) Business Model:

Centered on a SaaS cloud platform, we tailor digital tools to meet the differentiated needs of pharmaceutical enterprise clients, delivering an integrated digital marketing platform that spans from front-end consulting and strategy to back-end operations and maintenance.

(5) Case:

Client Name:A Pharmaceutical.

Issues to be addressed:Expand brand influence and enhance product awareness and reputation among the target physician community.

Cooperation Model:Yibai Technology empowered Pharmaceutical Company A to build an academic exchange platform for physicians and scholars. By leveraging multi-location interactive live streaming, the company facilitated online case competition evaluations among experts and speakers. Through case sharing by the speakers, this initiative reinforced brand credibility and demonstrated product efficacy, thereby providing strong endorsement for the brand.

Marketing Effectiveness:A series of multi-session competitions has provided online educational opportunities for more physicians, earning support and recognition from experts and clinicians. Total number of case competitions: 10+; Duration per session: 130+ minutes; Cumulative number of expert commentators: 50+; Cumulative number of target physicians educated: 20,000+

(1) Basic Company Information:

Founded in 2017, Qingyun Technology provides pharmaceutical brands with one-stop, real-time, intelligent, and platform-based digital representative services, leveraging its independently developed systems including the Zhiyun SCRM (Smart Cloud Social Customer Relationship Management) system for online physician behavior management, remote visit decision-making and quality inspection system, and physician persona data analysis engine. To date, Qingyun Technology has covered more than 38,000 primary care hospitals and accumulated 10 million records of online behavioral data from primary care physicians. In core hospitals, the company has collaborated with over 30 brands from 18 pharmaceutical enterprises, covering therapeutic areas such as cardiovascular diseases, diabetes, respiratory conditions, vaccines, urology, anti-infectives, and oncology.

Core Advantages:

The professional promotional capabilities of virtual representatives, combined with the collaborative execution capabilities of pharmaceutical companies’ teams, enable online pharmacy platforms to extend their prescription services.

(2) Financing Status:

Series B

(3) Core Products:

Digital Marketing Services

Digital marketing services with marketing outcomes as deliverables, including promotional activities such as product market access, clinical academic services, and terminal sales drive.

Digital Market Services

Online marketing campaigns with deliverables focused on market activities, including online academic conferences, online traffic generation, and online academic services.

Digital R&D Services

R&D services delivering online behavior analytics, including development capabilities such as physician profiling, AI recommendation engines, and data analysis systems.

(4) Business Model:

Qingyun Technology has established an online “expressway” connecting primary care physicians in China through a digital marketing model centered on virtual representatives. Leveraging artificial intelligence and big data analytics, the company delivers personalized online medical services to effectively engage and retain Chinese primary care physicians. Qingyun Technology is poised to command the largest private-domain traffic pool of primary care physicians in China, while providing the most efficient and convenient online platform for pharmaceutical marketing and other health services.

(5) Case Study:

Case Name:Marketing of Diabetes Products in the Primary Care CHC Market

Issues to be addressed: There are numerous primary-level CHC institutions with low potential, and traditional marketing models are unprofitable.

Cooperation Model:Through the virtual representative digital marketing services provided by Qingyun Technology, five virtual representatives were deployed to cover 1,500 consumer healthcare companies (CHCs) and over 3,000 prescribing physicians, with service fees paid based on sales performance.

Marketing Effectiveness:The project has lasted for three years, with a compound annual growth rate (CAGR) of over 50% and sales revenue exceeding RMB 200 million. The digital marketing process is fully transparent and compliant, with marketing service fees accounting for less than 5% of sales revenue.

(1) Basic Company Information:

Founded in 2008, MedSci has leveraged its robust medical academic expertise and professional digital platform. After years of accumulation and strategic layout, it began expanding into mobile healthcare services and Multi-Channel Marketing (MCM) services in 2015. Currently, MedSci has established a mature digital marketing system targeting physicians and patients, providing pharmaceutical companies with integrated Academic Promotion Outreach (APO) solutions.

Core Advantages

Proprietary physician platform with extensive high-quality doctor resources, academic authority and professional expertise within the medical community, and comprehensive digital communication solutions.

(2) Latest Financing Status:

Series B; RMB 150 million

(3) Core Products:

APO Academic Marketing Model

Precise coverage of target physicians, with accurate delivery of professional content and academic communication.

MCM Multichannel Marketing

Leveraging MedSci membership, we provide pharmaceutical companies with product insights through technologies such as precise data matching and member profiling.

Real-World Study Solutions

Based on MedSci iClinicalStation, enhance evidence generation efficiency, reduce costs, and improve research quality.

(4) Business Model:

Focusing on pharmaceutical enterprise clients, we leverage the MedSci Doctor Platform and the iProfiler physician profiling system, along with the YiXunDa™ tool, to deliver an integrated doctor-patient management system and digital academic dissemination solutions. This enables precise coverage and dissemination while quantifying communication effectiveness.

(5) Case:

Case Name:Xi'an Janssen Snairui Project

Customer Name:Xi'an Janssen

Issues to be addressed: Enhance Customer Brand Influence and Boost Product Awareness

Solutions and Outcomes:MedSci has established eight physician communities, covering a total of 1,300 physicians, and has promoted and disseminated a substantial volume of high-quality content spanning clinical practice, diagnosis and treatment, scientific research, training, case studies, presentation skills, and PPT design. Key content includes 60 literature interpretations and case shares in Himalaya FM audiobook format, 30 videos from the “21 Lectures on Multidrug-Resistance” series, 20 domestic and international medical live streams, 216 newsletters and quizzes, and two nationwide research training lecture tours. In total, more than 170 medical needs, over 60 product-related requests, and more than 30 inquiries regarding reimbursement policies were collected, and market access and medication adoption were completed for 17 cases.

Disclaimer:

The information contained in this report is derived from publicly available sources and interviews. VCBeat Research Institute makes no representations or warranties regarding the accuracy, completeness, or reliability of such information. The data, opinions, and projections presented herein reflect only the judgments of VCBeat Research Institute as of the date of publication, and past performance should not be regarded as an indicator of future results. At different times, VCBeat Research Institute may issue reports with information, opinions, or projections that are inconsistent with those contained in this report. VCBeat Research Institute does not guarantee that the information herein will remain current. Furthermore, VCBeat Research Institute reserves the right to modify the information contained in this report without prior notice, and investors should independently monitor any relevant updates or modifications.

Copyright Notice:

This document is copyrighted by VCBeat. Unauthorized use without permission will result in legal action.

The above is an excerpt from the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free: