Beyond 75% Revenue Growth: Where Is the Next Business Growth Driver for China's Pharmaceutical E-commerce?

In 1998, Shanghai No. 1 Pharmacy launched its own online pharmacy, marking the country’s first “pharmaceutical e-commerce” platform. In the years that followed, Chinese e-commerce platforms represented by Alibaba and JD.com experienced rapid growth, while the development of pharmaceutical e-commerce struggled to gain momentum.

Since the promulgation of the Interim Provisions on the Approval of Online Drug Trading Services in 2005, policies governing pharmaceutical e-commerce have undergone repeated fluctuations, including a temporary suspension of pilot programs for third-party online drug retail. Following the onset of the 13th Five-Year Plan period, the sector experienced multiple rounds of deregulation. In 2017, the review requirements for the “A,” “B,” and “C” certificates were successively abolished, and market entry barriers were lowered. Nevertheless, overall regulatory oversight has not been relaxed; relevant authorities have maintained strict scrutiny over enterprises engaged in online drug trading services.

The outbreak of the COVID-19 pandemic in 2020 dealt a severe blow to offline industries such as tourism and catering, whereas the pharmaceutical e-commerce sector, with its focus on online operations, experienced explosive growth during the pandemic. Under the circumstances, residents were compelled to shift their medication purchasing habits and channels from offline to online platforms. Leading companies in the industry strengthened their overall profitability amid the pandemic’s challenges, while also fostering the development of new business ventures.

VCBeat analyzed the annual reports of Alibaba Health, JD Health, and 111.com to gain insights into the development of pharmaceutical e-commerce over the past year, examining aspects such as financial data and business expansion.

Annual Report Analysis: Rapid Revenue Growth

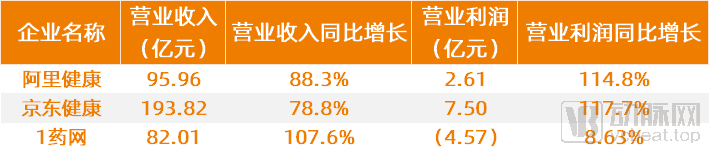

Alibaba Health, JD Health, and 1 Drugstore: 2020 Data (Note: Alibaba Health’s data is for the fiscal year 2020, covering April 2019 to March 2020; parentheses indicate losses)

According to the financial report data, all three companies achieved significant revenue growth. Alibaba Health even managed to turn losses into profits. Although 111.com is still in a loss-making state, the scale of its losses has decreased.

Alibaba Health

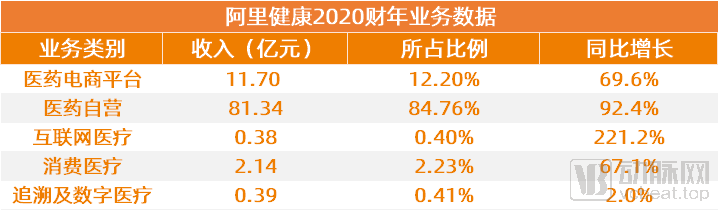

In terms of revenue composition, Alibaba Health’s internet healthcare segment recorded the highest growth rate, although it accounts for a relatively small proportion of total revenue. In fact, the increase in Alibaba Health’s revenue was primarily driven by the rapid growth of its self-operated pharmaceutical business, pharmaceutical e-commerce platform business, and consumer healthcare services.

In terms of revenue share, the self-operated business is undoubtedly a key component of Alibaba Health’s core business segments, generating RMB 8.134 billion in revenue and accounting for over 80% of total revenue.

As Ali Health’s fiscal year runs from April to March of the following year, the annual report data for the latest fiscal year 2021 (April 2020–March 2021) has not yet been released. Currently, data is available only up to September 2020, corresponding to the semi-annual report for the first half of fiscal year 2021. This portion of the data will be analyzed later in the article.

During the pandemic, in response to a surge in user inquiries and medication purchase demands, Alibaba Health, building on its “Worry-Free Medication Purchase” initiative jointly launched with Tmall, further introduced the “Chronic Disease Benefits Program” within its self-operated business. This program provides a suite of chronic disease management services for patients with chronic conditions, including exclusive access to “Cloud Doctors,” factory-direct supply of authentic medications, and personalized medication guidance. Thanks to the self-operated segment’s ability to meet user needs and its rapid organizational responsiveness, its overall performance was less impacted by the pandemic, maintaining a trend of high-speed growth throughout this period.

JD Health

JD Health’s revenue growth was primarily driven by an increase in the number of active users and additional purchases from existing users, the continuous rise in online penetration of pharmaceutical and health product sales, shifts in user behavior, and enhanced brand awareness resulting from the company’s investment in marketing activities. The COVID-19 pandemic in 2020 also contributed to the company’s performance growth.

According to the annual report, JD Health’s total revenue in 2020 reached RMB 19.38 billion, with self-operated business revenue amounting to RMB 16.8 billion, accounting for 86.7% of the total. Revenue from online platforms, digital marketing, and other services increased from RMB 1.4 billion in 2019 to RMB 2.6 billion in 2020, representing a year-on-year growth of 85.4%.

JD Health’s self-operated business primarily centers on “JD Pharmacy,” and it is progressively building a supply chain network that encompasses pharmaceutical companies and health product suppliers. Leveraging its brand recognition and supply chain management capabilities, the self-operated segment has maintained robust growth over the past year.

1Drug.com

Since its U.S. listing in September 2018, 111, Inc. has achieved nearly doubled revenue for three consecutive years, with its 2020 revenue surging by nearly ninefold compared to RMB 950 million in fiscal year 2017. Notably, in addition to maintaining rapid revenue growth, 111, Inc.’s gross profit also further increased. According to financial reports, its gross profit reached RMB 366 million in 2020, representing a year-on-year increase of 121.5%.

Prior to 2018, 1 Drug Network’s primary business was B2C. However, compared with Alibaba Health and JD Health, which benefit from inherent traffic advantages, 1 Drug Network’s consumer-facing business did not achieve rapid growth. After 2018, 1 Drug Network increased its investment in business-to-business (B-end) operations and established the B2D2C model (by building a digital platform for doctor-patient management) and the B2P2C model (by providing SaaS services to pharmacies).

At this stage, 111.com’s ability to achieve stepped growth is largely attributable to its unique S2B2C model, which empowers B-side enterprises through digitalization to jointly serve C-side consumers.

Leveraging the advantages of its S2B2C model, 111.com’s ecosystem achieved rapid expansion in 2020. By the fourth quarter of 2020, the total number of domestic and international pharmaceutical companies with direct ties to 111.com had exceeded 330. In addition to pharmaceutical manufacturers, market participants such as vendors, pharmaceutical distributors, contract sales organizations (CSOs), and commercial insurance companies have also significantly strengthened the existing supply chain platform.

What Has Pharmaceutical E-Commerce Achieved During the Pandemic?

Whether in boosting the high-quality development of the pharmaceutical e-commerce industry or influencing market business categories, the pandemic has impacted market development from various angles. In the face of the sudden COVID-19 outbreak, major pharmaceutical e-commerce platforms have each adopted their own response strategies.

Drug Supply

As the saying goes, “Even the cleverest housewife cannot cook a meal without rice.” For pharmaceutical e-commerce platforms, one of the biggest challenges during the pandemic has been ensuring an adequate supply of medications.

Since February 6, 2020, Alibaba Health has successively launched the “Buy Medicines Without Leaving Home” service on Taobao and Alipay. This internet-based healthcare model, which combines online consultations and e-prescribing with home delivery of medications, enables patients with chronic diseases to safely purchase their required medicines without leaving their homes. It is reported that within less than three days of its launch, the service attracted nearly 3 million cumulative page visitors.

To ensure an adequate supply of medications, Alibaba Health partnered with nearly 50 domestic and international pharmaceutical manufacturers, including Sanofi, HEC Pharm, GlaxoSmithKline, AstraZeneca, CSPC Pharmaceutical Group, Pfizer Upjohn, Novartis, Bayer, Merck & Co., and Bristol Myers Squibb. On February 13, they launched the “Chronic Disease Welfare Program” on Tmall’s “Buy Medicines Without Leaving Home” platform to guarantee the online availability of chronic disease medications during the epidemic, while also providing online chronic disease management services.

1Drug.com has ensured the B2B and B2C supply of face masks, COVID-19 medications, and chronic disease drugs by continuously expanding its distribution channels and leveraging strategic direct-procurement partnerships with more than 100 renowned pharmaceutical companies both in China and abroad.

Pharmaceutical Distribution

Due to the outbreak of the pandemic, consumers were unable to enjoy services such as “next-day delivery” and “24-hour home medication delivery” as they normally would. Many patients have immediate medication needs and cannot tolerate prolonged waits for pharmaceutical deliveries. Therefore, for pharmaceutical e-commerce platforms, the ability to rapidly provide medications to consumers during the pandemic has become a significant competitive advantage.

Leveraging the strengths of JD.com and its collaboration with JD Logistics, JD Health is able to provide customers with an integrated supply chain solution covering the entire process of pharmaceutical warehousing and transportation. As of December 31, 2020, JD Health operated a total of 14 dedicated pharmaceutical warehouses and over 300 non-pharmaceutical warehouses across China. Relying on these dedicated warehouses, its O2O service “JD Medicine Express” has covered more than 300 cities, offering users next-day delivery, same-day delivery, 30-minute delivery, and 24/7 medication delivery services to meet urgent medication needs.

What Changes Have Occurred in Pharmaceutical E-commerce in the Post-Pandemic Era?

Impacted by the “black swan” event of the COVID-19 pandemic, pharmaceutical e-commerce has ushered in an excellent window for growth. However, as epidemic prevention and control measures become normalized, can pharmaceutical e-commerce sustain its existing momentum? What strategic moves have companies undertaken to maintain their favorable development trajectory?

Alibaba Health

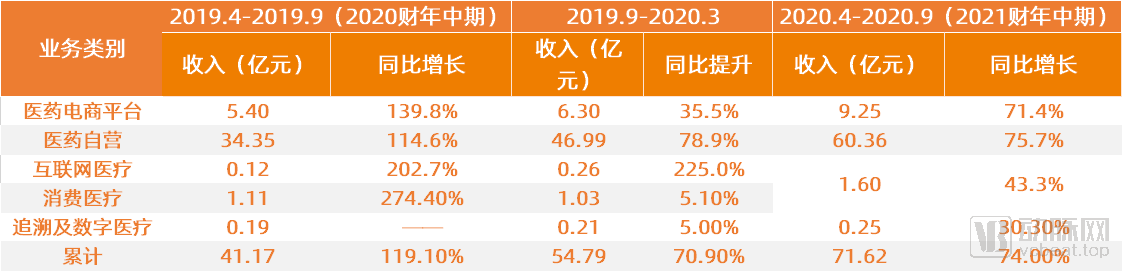

From the perspective of business composition, the pandemic did not alter Alibaba Health’s revenue structure. Self-operated business has remained its core segment both before and during the pandemic, consistently accounting for over 80% of total revenue since 2018.

Changes in Alibaba Health’s Business Segments Before and After the Pandemic

Changes in Alibaba Health’s Business Segments Before and After the Pandemic

(Note: In the interim results for fiscal year 2021, Alibaba Health integrated its internet healthcare and consumer healthcare businesses.)

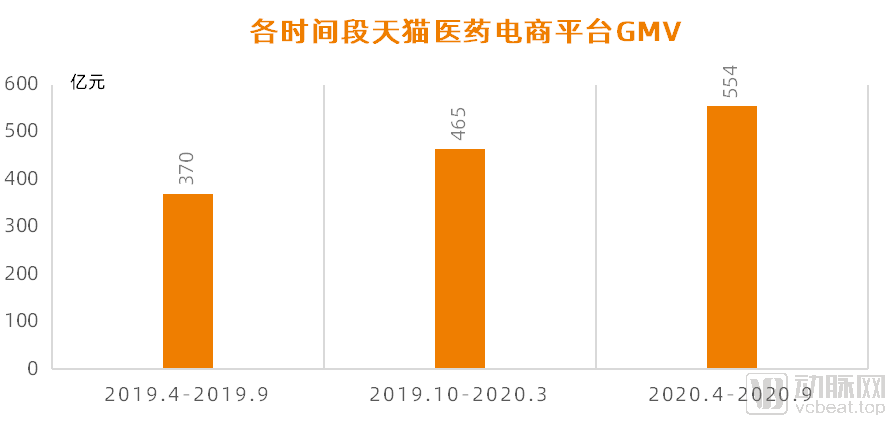

According to the financial results for fiscal year 2020 and the interim results for fiscal year 2021, as of September 30, 2020, the annual active consumers on the Tmall Medicine platform operated by Alibaba Health exceeded 250 million, representing an increase of more than 60 million from six months earlier. In addition, the annual gross merchandise value (GMV) generated by the Tmall Medicine e-commerce platform operated by Alibaba Health has maintained a steady growth trajectory.

Due to the strong localization characteristics of consumer healthcare services, which require consumers to complete services offline, the growth of this business slowed during the pandemic. To further deepen its presence in the internet sector, Alibaba Health integrated its consumer healthcare and internet healthcare businesses into a unified medical and health services segment. In September 2020, it rebranded the Alibaba Health APP as “Yilu” (Medical Deer), aiming to build an integrated online-to-offline internet-based tiered diagnosis and treatment system for local medical and health services, thereby meeting user needs under the new normal of epidemic prevention and control.

Furthermore, Alibaba Health has further enhanced its service capabilities in warehousing, logistics, customer service, and quality control. It has established a distribution network comprising nine warehouses across seven locations, expanding the geographic coverage of its products and enabling next-day delivery services in 60 core cities. Moreover, Alibaba Health has developed direct-to-patient (DTP) cold-chain logistics capabilities, which are now being applied to the distribution of new drugs and oncology medications.

JD Health

Public information reveals that JD Health’s revenue reached RMB 8.8 billion in the first half of 2020, and further climbed to RMB 10.58 billion in the second half, nearly matching its full-year revenue for 2019. Furthermore, as of December 30, 2020, more than 12,000 third-party merchants were operating on JD Health’s online platform, an increase of approximately 3,000 from the over 9,000 recorded six months earlier. This growth underscores JD Health’s substantial commercial potential and market value.

In August 2020, JD Health completed its Series B financing round. Four months later, JD Health officially listed on the Hong Kong Stock Exchange, becoming the first internet healthcare company to go public while already profitable.

In the second half of 2020, JD Health also accelerated the implementation of its strategy. According to incomplete statistics, during the six-month period from June to December 2020, JD Health witnessed more than 20 new product launches and business collaborations, while steadily intensifying its deployment of online medical and healthcare services.

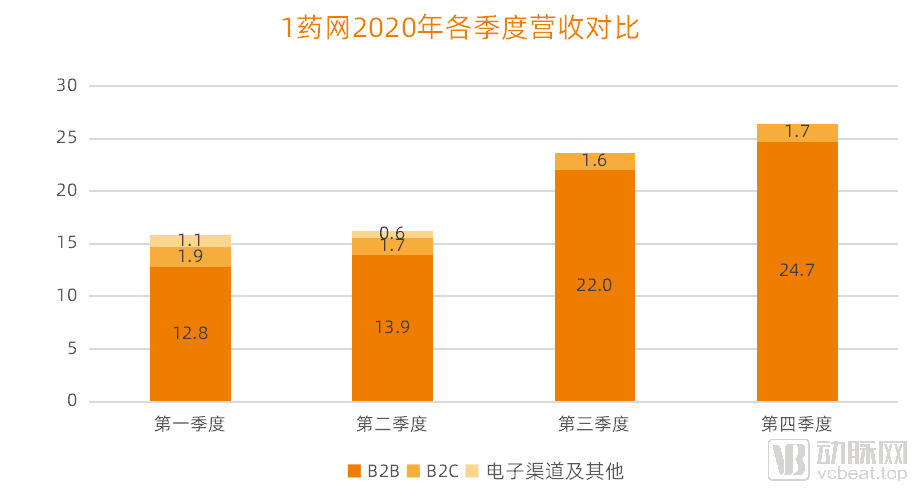

1Drug.com

Data source: 111.com's quarterly financial reports (Note: Revenue from electronic channels has been consolidated into B2B revenue starting from the third quarter)

Overall, 111.com’s revenue has maintained steady growth, with its B2B business experiencing a significant surge in the third quarter. Although pandemic control measures have become routine, 111.com continues to demonstrate robust development. A major driver of this rapid growth is the advantage of its S2B2C model. Additionally, 111.com’s development has been influenced by its subsidiary, Yaofang Technology (Shanghai) Co., Ltd. (“Yaofang Technology”), which operates under the 111.com brand.

In 2020, Yaofang Technology completed two rounds of financing in August and December, respectively. The fundraising accelerated 111.com’s investment in digital technology and business expansion. Currently, 111.com is preparing for Yaofang Technology’s initial public offering on the STAR Market.

"Moving forward, 1 Yao Wang will continue to strengthen all aspects of its S2B2C model, enhance its existing AI technologies and data processing capabilities, empower doctors and pharmacies, and advance its business expansion plans."

Business Analysis: Intensifying Efforts in Healthcare Services

For Alibaba Health and JD Health, revenue from the pharmaceutical e-commerce segment undoubtedly serves as a cash cow. However, these companies are clearly not content with the status quo; instead, they are choosing to step out of their comfort zone in pharmaceutical distribution and gradually ramp up their efforts in medical services.

In the logic of pharmaceutical e-commerce, users have a more proactive demand for medicines, purchasing them independently based on their own needs. In contrast, this is not the case with medical and health services; most users do not have a strong proactive demand for such services, thus requiring more operational efforts and promotion.

According to JD Health’s 2020 annual report, the company’s selling and marketing expenses increased from RMB 746 million in 2019 to RMB 1.435 billion in 2020, representing a year-on-year increase of 92.3%. This growth was primarily driven by higher promotional and advertising expenditures, as well as intensified marketing efforts for JD Health’s retail pharmacy business, online medical and health services, and other innovative businesses.

As early as 2014, JD Health operated as an independent business segment within JD.com. When internet companies began making significant inroads into the healthcare industry, JD chose to enter the market through retail. In 2019, JD Health was spun off from JD.com to operate independently, adopting a strategy centered on health management and comprehensively expanding its medical and healthcare services. In 2020, in addition to launching a series of anti-epidemic and pandemic prevention and control services, JD Health released its standalone apps, “JD Health” and “JD Family Doctor.” On the digital healthcare front, specialized centers—including the Heart Center, Mental Health and Psychology Center, Traditional Chinese Medicine Hospital, Respiratory Center, and Otolaryngology Center—were successively established, fully addressing users’ personalized needs and further deepening its “Internet + Healthcare” services.

Moving forward, JD Health will strengthen its internet hospital services and deepen the development of specialized centers by connecting with more top-tier experts and establishing additional specialty centers to cover a broader range of therapeutic areas. Meanwhile, it will further drive cross-growth of products and services through its retail pharmacy business, integrating existing retail pharmacies, medical service operations, and offline physician resources to create a closed-loop ecosystem for online healthcare services.

In its efforts to strengthen healthcare services, Alibaba Health has opted for a comprehensive upgrade of its internet healthcare business positioning, integrating internet healthcare with consumer healthcare services. It also rebranded the Alibaba Health APP as “Yilu,” focusing on services such as medical content search, online consultation and inquiry, appointment registration, vaccine scheduling, and rapid medication delivery. Meanwhile, leveraging AI technology, it aims to make medical consultations more accessible and intelligent.

In addition to accessing online diagnosis and treatment services through the “Yilu” app, users can also obtain medication guidance, follow-up consultations, prescription renewals, and medical consultation services via platforms such as Alipay, Taobao, and Tmall, thereby offering more diverse ways to access these services.

Going forward, Alibaba Health will continue to increase its investment in internet healthcare services, continuously accumulating and enriching high-quality content. By leveraging technological and business model innovations, and integrating diversified, multi-dimensional medical tools and service capabilities, the company aims to meet the public’s demand for health services.

Objectively speaking, the onset of the COVID-19 pandemic has highlighted the unique advantages of pharmaceutical e-commerce and presented significant growth opportunities for the industry. In the post-pandemic era, to better meet consumer service demands, some pharmaceutical e-commerce platforms have intensified their investments in online healthcare services. While entering the internet healthcare sector from pharmaceutical sales is not a novel approach within the industry, it offers substantial growth potential for large enterprises such as Ali Health and JD Health.

Policy Trends: Regulatory Measures for Online Sales of Prescription Drugs

Over the more than 20 years since the inception of China’s first pharmaceutical e-commerce platform, the state has repeatedly adjusted its regulatory policies for “pharmaceutical e-commerce,” with the permissibility of online sales of prescription drugs remaining a hotly debated topic within the industry.

To strengthen the supervision and administration of online food and drug operations and to ensure food and drug safety, in 2014, the China Food and Drug Administration (CFDA) publicly solicited comments on the “Measures for the Supervision and Administration of Online Food and Drug Operations (Draft for Comments).” Article 8 thereof stipulates that online drug distributors shall sell prescription drugs based on prescriptions, in accordance with the requirements for classified drug management; the standards, format, validity period, and other aspects of such prescriptions shall comply with the relevant regulations on prescription management.

On November 12, 2020, the General Office of the National Medical Products Administration (NMPA) publicly solicited comments on the “Administrative Measures for the Supervision and Regulation of Online Drug Sales (Draft for Comments),” formally providing direction for the online sale of prescription drugs by permitting their online sale and the display of prescription drug information. Since then, the new regulatory framework for online drug sales has finally been implemented.

According to the interim financial results for fiscal year 2021 released by Alibaba Health, the company has established a “1+N” brand collaboration mechanism in the prescription drug sector. It has set up ten major disease centers focusing on conditions such as heart disease, diabetes, and liver disease. By integrating a service matrix that combines user traffic, medical content, physicians, and post-dispensing medication reminders, Alibaba Health is able to provide patients with more accessible and higher-quality services.

Beyond the online sale of prescription drugs, inclusion in the national medical insurance system is another critical factor influencing the development of the pharmaceutical e-commerce industry. Spurred by the pandemic, internet healthcare has rapidly expanded and been incorporated into the scope of medical insurance reimbursement, enabling physicians to issue online prescriptions with immediate insurance settlement. Consequently, calls from the industry for the integration of pharmaceutical e-commerce into the medical insurance system have grown increasingly loud.

However, constrained by various technological and regulatory factors, the model integrating pharmaceutical e-commerce with medical insurance has not yet been realized. According to the "2021 Research Report on Global and China Pharmaceutical E-commerce Market and Development Trends" released by iiMedia Research, more than half of the users cited the inability to use medical insurance for payment as their primary dissatisfaction with pharmaceutical e-commerce platforms.

At this stage, some pharmaceutical e-commerce platforms have integrated with medical insurance through the “online order, store delivery” model. Simply put, consumers place orders via online platforms and purchase medications using medical insurance at affiliated physical pharmacies, with last-mile delivery handled by the platform’s couriers. For consumers, the entire process—from ordering to medical insurance payment—can be completed online. However, this model relies on offline brick-and-mortar pharmacies that are already equipped for medical insurance settlement; standalone online e-commerce platforms alone cannot achieve this.

Final Remarks

Compiling annual report data, policy trends, and industry trends, VCBeat has summarized its viewpoints as follows:

1. The benefits that the pandemic brought to pharmaceutical e-commerce will not disappear with the containment of the outbreak. As patients’ awareness and acceptance of online channels continue to grow, the pharmaceutical e-commerce sector as a whole remains in a state of healthy development;

2. A single pharmaceutical distribution service cannot meet consumer demands; B2C-focused e-pharmacies need to enhance medical services to create a closed-loop “medical care + pharmaceuticals” ecosystem;

3. Online sales of prescription drugs may become another growth driver for the retail business of pharmaceutical e-commerce;

4. Integration with medical insurance payment systems is one of the key drivers promoting the development of pharmaceutical e-commerce;

Overall, policy remains a key focus for pharmaceutical e-commerce. Whether it involves the online sale of prescription drugs or integration with medical insurance, industry development is inextricably linked to government regulation and oversight. Furthermore, exploring post-pandemic market demands to formulate future corporate development strategies remains the most critical step for pharmaceutical e-commerce companies at this stage.