25 Overseas Digital Therapeutics Companies: Big Pharma Enters Through M&A, Global Market Size Expected to Exceed $9 Billion by 2025

The rapid advancement of mobile networks and artificial intelligence is increasingly dominating our lives. As these technologies flourish, digital therapeutics are rising to prominence in the healthcare industry, with their remote care advantages becoming particularly pronounced amid the global pandemic outbreak.

According to the official definition by the Digital Therapeutics Alliance, digital therapeutics deliver evidence-based, software-driven interventions to prevent, manage, or treat diseases. Digital therapeutics can be used independently, in combination with medications, or alongside other therapies to improve patient health outcomes.

Looking at the development trajectory of digital therapeutics overseas, initial R&D efforts were primarily concentrated in academia and technology companies.,The inherent compatibility of digital therapeutics with pharmacological treatments has significantly sparked the interest of major pharmaceutical companies. Several prominent publicly listed pharmaceutical firms, such as Takeda Pharmaceutical and Orexo, have actively entered the digital therapeutics sector.

Over the past seven years, investment in digital therapeutics companies in the United States has grown at an average annual rate of 40%, surpassing $1 billion by 2018. Last August, the $18.5 billion merger between digital health giants Teladoc and Livongo further highlighted the immense potential of the digital therapeutics and digital care markets.

THE EVIDENCE FORUM’s white paper on digital therapeutics predicts that the digital therapeutics market will grow tenfold over the next 3–5 years, reaching $9 billion (approximately RMB 50 billion) by 2025.

From the first FDA clearance of Pear Therapeutics’ digital therapeutics product in 2017 to the approval of nearly 30 DTx products by authoritative agencies such as the FDA by 2021, digital therapeutics abroad have flourished under multi-stakeholder drivers.

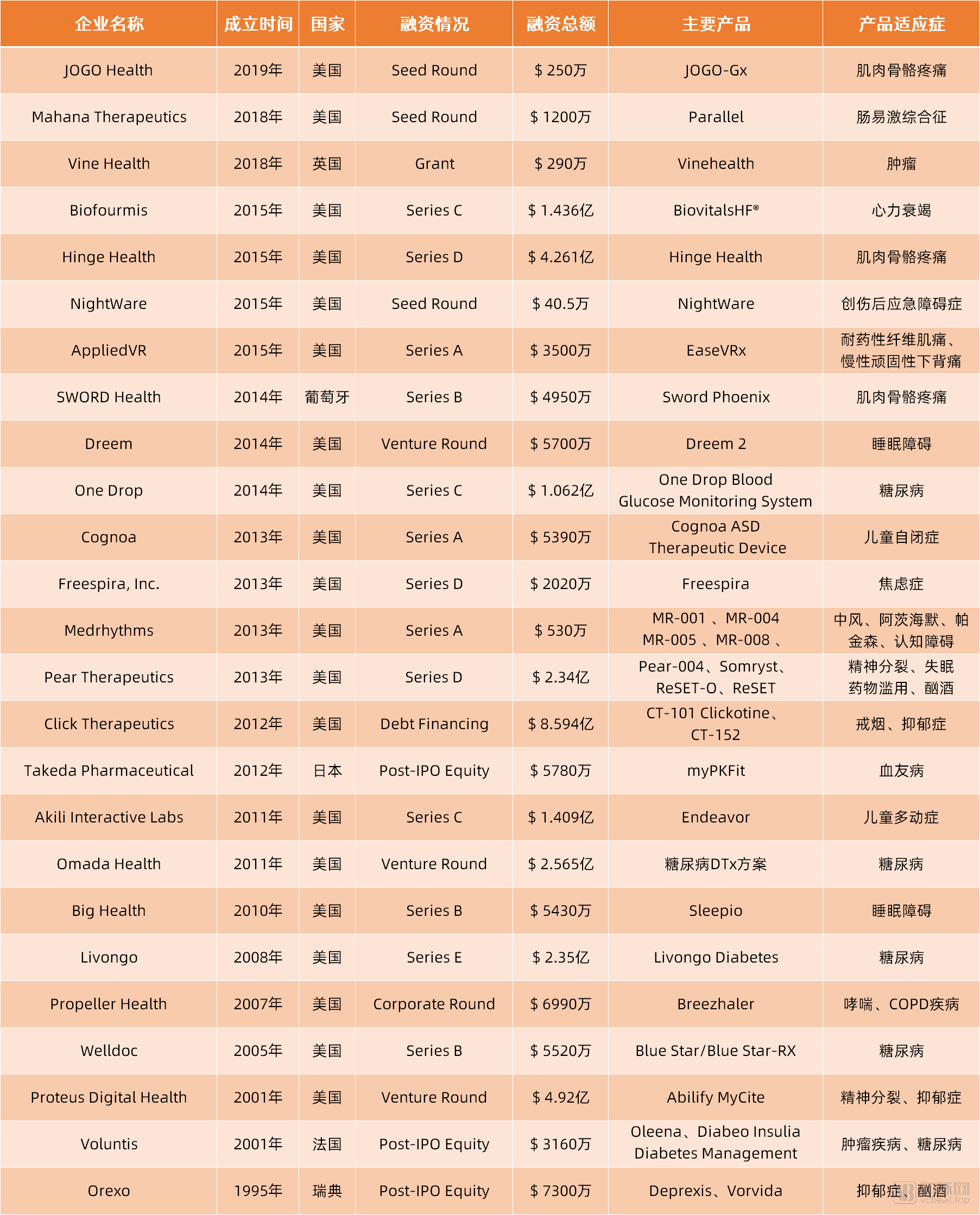

Recently, VCBeat conducted a review of 25 overseas digital therapeutics companies whose products have obtained FDA or CE certification and have a history of financing, compiling the findings into the table below. We aim to characterize these companies from multiple dimensions to identify the underlying logic driving their future development.

Figure 1-25 List of Overseas Digital Therapeutics Companies

Note: 1. Data sources include the VCBeat database and publicly available information; 2. Selection criteria for companies: products incorporate digital therapeutics, have FDA or CE certification, and have secured at least one round of financing.

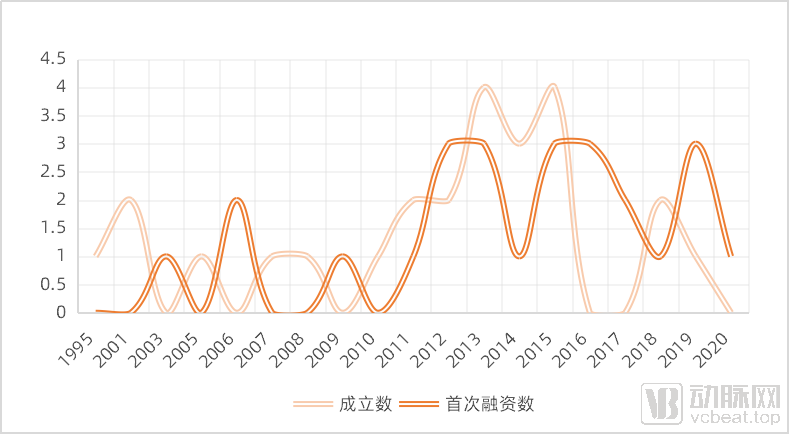

First, we organize the data from the perspective of company establishment and initial financing timelines, as shown in the chart below:

Figure 2 - Founding and Initial Financing Dates of 25 Overseas Digital Therapeutics Companies

It is evident that the establishment of digital therapeutics companies experienced four waves of heightened activity, with a peak in 2013; the trend in initial financing followed suit. In reality, some enterprises that later became industry leaders did not secure their first round of funding shortly after incorporation. For example, Pear Therapeutics, founded in 2013, completed its first financing round two years later; Akili Interactive Labs, established in 2011, did not obtain funding until 2015; and Orexo, founded in 1995, did not successfully raise capital until 2003, an interval of eight years.

Digital therapeutics companies established after 2014 often completed their financing rounds within a year. This indirectly reflects that the pioneers in the digital therapeutics sector underwent a gradual process of technological accumulation and market acceptance, thereby providing valuable insights and methodologies for later entrants.

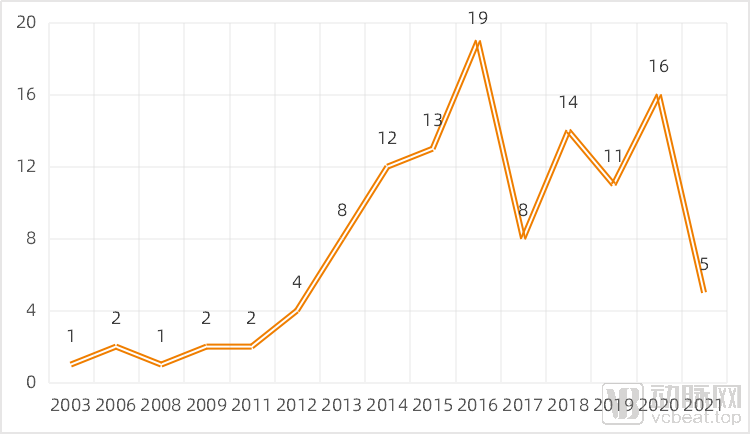

Figure 3 - Statistics on Financing Events of 25 Overseas Digital Therapeutics Companies

In fact, the number of digital therapeutics financing events among these 25 companies increased almost every year, peaking in 2016, followed by a slight decline, before surging again in 2020.

This also reflects the continued positive trend in the digital therapeutics investment market. Digital therapeutics, driven by evidence-based medicine and high-quality software programs, demonstrated significant advantages during the 2020 COVID-19 outbreak. With both “substance and style,” they have captured the interest of investment firms. In 2021, even before the year was halfway through, there had already been five financing rounds among 25 companies, indicating undiminished momentum. VCBeat will continue to closely monitor developments in this blue-ocean market of digital therapeutics.

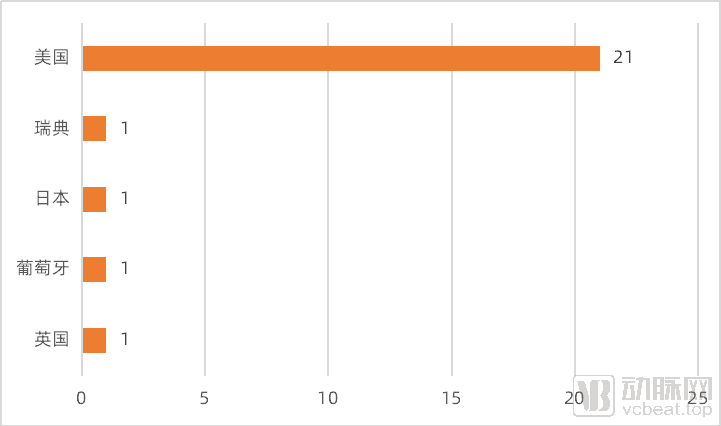

Figure 4-25 Geographic Distribution of 25 Digital Therapeutics Companies

Geographically, all companies included in this inventory are located in developed countries, with U.S.-based digital therapeutics firms holding an overwhelming majority. This dominance is driven by two key factors: first, developed nations boast significantly higher internet penetration rates, alongside rapid growth in digital technology adoption and increasing demand for healthcare cost containment; second, the United States possesses the world’s most mature financial market system, providing domestic innovative enterprises with distinct competitive advantages.

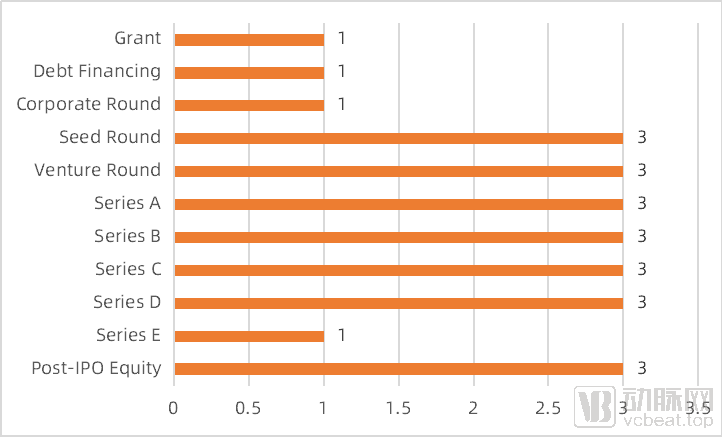

Figure 5-25 Distribution of Current Financing Rounds for 25 Overseas Digital Therapeutics Companies

In terms of financing, the distribution of digital therapeutics companies across various funding rounds is relatively even, with many well-known institutional investors participating. For instance, Temasek led the Series C financing round for Akili Interactive Labs; SoftBank led the latest funding rounds for both Pear Therapeutics and Biofourmis; and Johnson & Johnson Innovation and Samsung Ventures each co-led two separate Series B financing rounds for Welldoc.

Furthermore, after gaining market recognition, some digital therapeutics companies may be acquired by industry giants to facilitate further growth. For example, in December 2018, medical device manufacturer ResMed acquired the digital therapeutics startup Propeller Health for $225 million; digital health giants Teladoc and Livongo merged in August 2020; during the same period, Proteus Digital Health was also acquired by Otsuka Pharmaceutical Co., Ltd. (Otsuka).

Furthermore, well-capitalized pharmaceutical companies have frequently invested in digital therapeutics firms. For instance, the Swiss pharmaceutical giant Novartis participated in every funding round of Pear Therapeutics in 2018, with a total investment of $70 million.

These transactions were all conducted among large enterprises in the healthcare sector, not only providing digital therapeutics companies with financial support to expand their product portfolios, but also creating a competitive landscape that attracts more healthcare companies to enter the market.

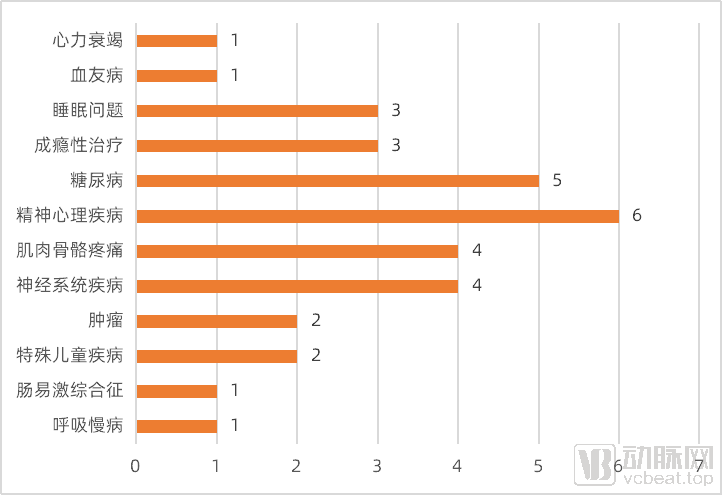

Figure 6. Indications of Products from 25 Overseas Digital Therapeutics Companies

In recent years, digital therapeutics products, based on applications or artificial intelligence platforms, have increasingly been integrated with wearable devices or medical devices to prevent, detect, manage, or treat various conditions, including mental health disorders, cognitive impairments, obesity, diabetes, and respiratory diseases.

The digital therapeutics companies reviewed in this analysis have primarily built their product portfolios around chronic disease management, focusing on areas such as diabetes and mental health disorders. Among them, 24 companies have obtained relevant FDA clearance or approval for their products, three have secured European CE marking, and one has received certification from the National Medical Products Administration (NMPA).

In the United States, over 130 million people suffer from at least one chronic disease, while chronic disease management often encounters issues such as poor patient adherence and difficulties in long-term follow-up. The emergence of digital therapeutics has provided crucial solutions to these problems, helping patients manage their conditions appropriately and integrating with existing health insurance plans to offer supplementary clinical treatment support.

The COVID-19 pandemic once triggered a crisis in public mental and psychological health. Therefore, digital therapeutics companies seeking to attract payers, investors, and partners should expand their presence in relevant medical fields.

Although the digital therapeutics products from companies included in this review have all obtained authoritative certifications, digital therapeutics have, in fact, posed significant challenges to regulatory agencies. The FDA’s regulatory review of digital therapeutics currently continues to follow traditional pathways for medical device design, which are slow and inefficient, and thus ill-suited for the rapid development and validation of Software as a Medical Device (SaMD) products.

To streamline the review process for digital therapeutics products, the FDA developed the Digital Health Innovation Action Plan, which introduced the FDA Pre-Cert Program for Software as a Medical Device.

Under this program, companies can apply to the FDA for a pre-certification assessment. Once approved, minor updates or adjustments to the product after market launch will not require further review. In April last year, the FDA also relaxed approval regulations for digital therapeutics in mental health to accelerate their time to market.

Given that the regulatory framework for digital therapeutics in China is not yet mature, no dominant players have emerged, and significant uncertainty remains for digital therapeutic products in the future, we have decided to analyze the products of three leading overseas companies that have not been acquired at the end of this article, aiming to identify what makes them attractive to top-tier capital.

Hinge Health

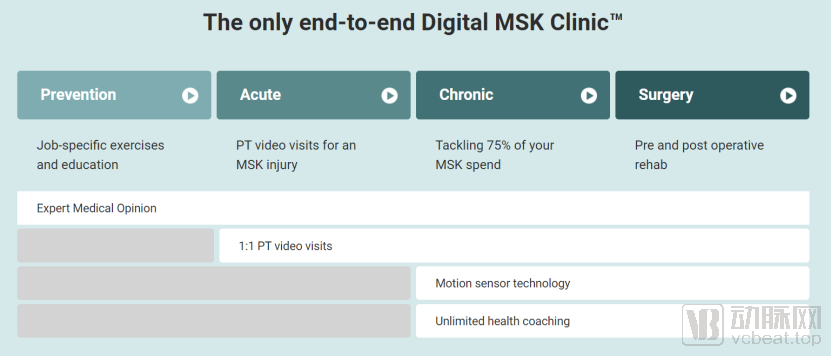

Hinge Health specializes in digital musculoskeletal treatment solutions, leveraging sensor technology combined with one-on-one coaching to enable patients to easily access care from home. Its evidence-based technology has been proven to alleviate pain and avoid surgery.

Hinge Health operates the world’s first and most comprehensive digital musculoskeletal (MSK) clinic, with products and services that include expert medical opinions, one-on-one video coaching, motion sensor technology, and ongoing health guidance.

Stanford University (Stanford & Vanderbilt) found in a study of 10,264 Hinge Health users that Hinge Health reduced pain by 69% and saved $5,012.52 per user.

Compared with opioids, Hinge Health’s digital therapeutics deliver fourfold greater pain relief, improve patients’ mental health, and achieve the industry’s highest patient adherence rate of 75%.

Hinge Health’s Product Model | Source: Hinge Health Official Website

Hinge Health has completed its Series D financing, topping the list of non-M&A companies in total funds raised with $426.1 million. The company maintains offices in San Francisco, Portland, Minneapolis, and Chicago, employs over 500 staff members—primarily clinical experts, data specialists, and engineers—and has established partnerships with more than 300 enterprises, including Philips and Boeing.

Omada Health

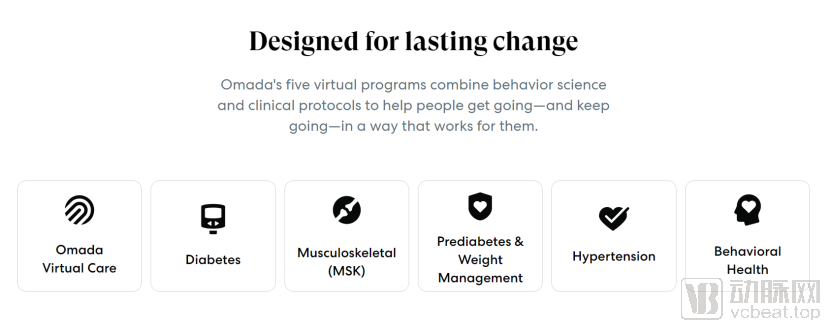

Omada Health is a technology company that guides and helps people change their lifestyle behaviors to prevent chronic diseases and reduce disease incidence, serving as a leading representative in the field of digital therapeutics.

By identifying the link between chronic diseases and user engagement, Omada Health has developed five programs targeting diabetes, musculoskeletal (MSK) pain, weight management, hypertension, and behavioral health, delivering a highly comprehensive virtual care solution.

Omada Health’s Five-Step Program. Image source: Omada Health official website

Omada Health is the first company to apply social networking principles to legitimate clinical treatment. It has recently completed a new round of venture capital financing after its Series D, raising $256.5 million—second only to Hinge Health. Lead investors include Wellington Management and Cigna Group. The company has partnered with more than 1,500 enterprises, including American Eagle Outfitters and 3M, and its online user base has exceeded 450,000.

Pear Therapeutics

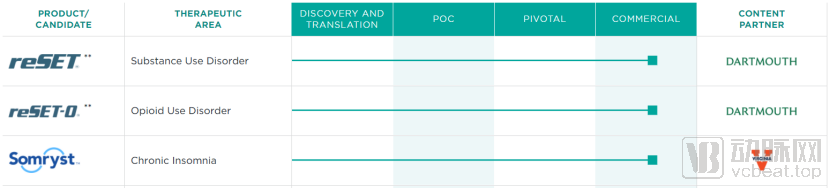

Pear Therapeutics is a software-based digital therapeutics provider and one of the first nine companies in the FDA’s digital therapeutics pilot program. It has launched three FDA-authorized prescription digital therapeutics (PDTs) for psychiatric indications: reSET for substance use disorder, reSET-O for opioid use disorder, and Somryst for insomnia and its associated depression.

Pear Therapeutics’ Product Pipeline. Image source: Pear Therapeutics official website

Pear Therapeutics is the first company to receive FDA approval for a prescription digital therapeutic. It has completed its Series D financing, raising a total of $234 million, with Temasek Holdings and SoftBank both serving as lead investors.

It is evident that the competitive advantages of certain companies in the digital therapeutics sector are gradually emerging.

Current overseas digital therapeutics companies are gradually exhibiting two distinct characteristics. On one hand, although they are not yet mature in the capital market, their financing pace is accelerating, with the time spent on early-stage rounds shortened to less than one year. On the other hand, there is now a relatively clear strategy for integrating online and offline services in chronic disease management within the digital therapeutics sector.

Among the 25 overseas digital therapeutics companies reviewed, we found that enterprises like Omada Health, which offer integrated product solutions and engage employers, health plans, and healthcare institutions, as well as companies like Pear Therapeutics with diversified product pipelines, are more likely to gain a competitive advantage.

Furthermore, digital therapeutics hold significant promise in improving patients’ medication adherence, likely emerging as a new growth driver for pharmaceutical companies to build their ecosystems and facilitating the integration of diagnosis and treatment. Conversely, the strategic advantages offered by large pharmaceutical companies will enhance the efficiency of developing and promoting digital therapeutics. In the near future, mergers and acquisitions among digital therapeutics companies are expected to increase, with greater participation from pharmaceutical firms.

However, digital therapeutics remains an innovative field globally. Key challenges that must be addressed include market education, pursuing differentiated competition, resolving reimbursement issues, improving regulatory approval and oversight, and safeguarding patient privacy and data security.

Yet these challenges cannot halt the surging momentum of the digital therapeutics industry; this market is just getting started, with promising prospects ahead.