Aesthetic Medicine Upstream Sector Reaches PE Ratio of 217x: Is Innovation in Materials and Technology the True Growth Driver?

“What is the driving force for the industry’s future development? In the next five to ten years, I believe the driving force will not be demand but rather the upstream sector of the industry; the true drivers of development are materials and technology.”

Recently, at the Aesthetic Medicine Industry Innovation Forum, a sub-forum of the 5th Future Healthcare Top 100 Conference hosted by VCBeat, Jin Xuekun, Founding Partner of Mingfeng Capital and former CEO of Bloomage Biotechnology, delivered a speech titled “Value Distribution in the Aesthetic Medicine Industry Chain.”

According to a research report on the medical aesthetics industry released by Pacific Securities, the domestic medical aesthetics sector has seen rising popularity year by year, with its market and consumer attributes becoming increasingly prominent. In 2019, the market size of China’s medical aesthetics industry reached RMB 176.9 billion, representing a year-on-year growth of 22%. It is projected that the market size will grow to RMB 311.5 billion by 2023.

However, other relevant data indicate that, due to the impact of the COVID-19 pandemic, the market growth rate of China’s medical aesthetics industry will slow significantly to 5.7%, a figure undoubtedly far below the industry’s 22% market growth rate in 2019.

Market Growth Slows, National Regulations Tighten: Is the Medical Aesthetics Industry Facing Severe Challenges Beneath Its “Beautiful” Facade?

The fact is that an examination of the 2020 annual reports of multiple upstream and midstream companies in the medical aesthetics industry reveals that the sector’s development has remained relatively optimistic to date.

According to the 2020 annual report of Imeik, a leading upstream company in the medical aesthetics industry, the company achieved a total revenue of RMB 709 million in 2020, a year-on-year increase of 27.18%, and a net profit attributable to shareholders of the parent company of RMB 439 million, a year-on-year increase of 43.93%. The 2020 financial report of another industry leader, Bloomage Biotechnology, showed that the company’s operating revenue reached RMB 2.63 billion, with a net profit attributable to shareholders of the parent company of RMB 650 million, representing year-on-year increases of 39.6% and 10.3%, respectively, compared to 2019. Furthermore, according to So-Young’s fourth-quarter 2020 financial report, the company’s revenue for the quarter was RMB 425 million, a year-on-year increase of 18.6%, setting a new record for single-quarter revenue since its listing.

However, as the medical aesthetics industry advances amidst ongoing adjustments, its overall market structure is also undergoing subtle changes. What is the current state of development in the medical aesthetics sector? What structural transformations have taken place across the industry? What are the key drivers propelling industry growth, and what are the future trends? Jin Xuekun’s presentation may well provide the answers.

Jin Xuekun, Founding Partner of Mingfeng Capital

“Recently, the structure of the medical aesthetics market has undergone changes.”

First, while the growth rate has indeed slowed, there remains significant room for improvement in penetration rates.

In terms of market size growth rate and penetration rate, the medical aesthetics industry saw a market size growth rate of 33.7% in 2017, which actually slowed down to 11.6% by 2020. Regarding penetration rates, China's medical aesthetics penetration rate was 16.7% in 2019. Although this figure represents an increase from 14.8% in 2018, it remains significantly lower than that of "developed" medical aesthetics countries such as South Korea, the United States, and Brazil, indicating substantial room for future growth.

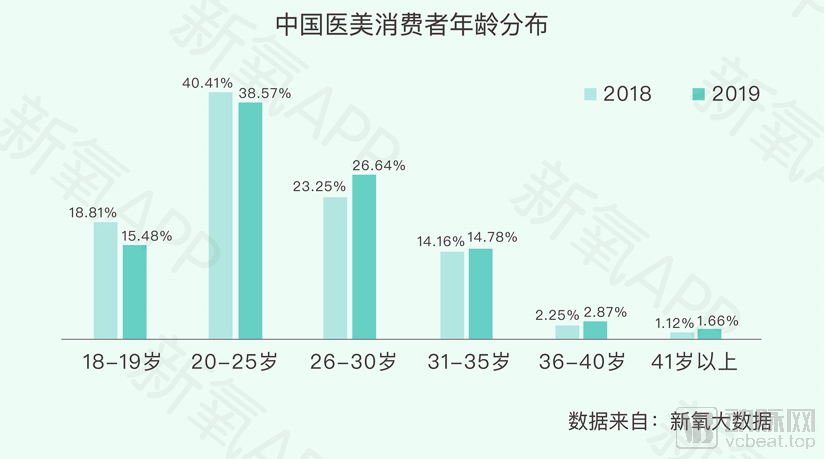

Secondly, the age profile of mainstream consumers is changing.

According to data from the “2019 Aesthetic Medicine Industry White Paper” released by So-Young, the age distribution of consumers is undergoing structural changes. As is well known, ten years ago or earlier, consumers of aesthetic medicine in China were predominantly affluent individuals aged 40 and above. However, data from the So-Young White Paper indicate that by 2019, the primary consumer base had shifted to the 20–30 age group. The consumption awareness and preferences of this demographic are not only dominant at present but will continue to hold sway over the next decade, directly reshaping and iterating a new landscape for aesthetic medicine consumption in China.

Source: So-Young “2019 White Paper on the Medical Aesthetics Industry”

Third, new first-tier cities have become the most critical battleground for the medical aesthetics industry.

“The structure of the market is shifting. Previously, first-tier cities dominated, but now the most significant changes are occurring in new first-tier cities,” stated Jin Xuekun. According to data released by Fastdata Jishu, the proportion of medical aesthetics consumers in first-tier cities gradually declined from 37.5% in 2017 to 24.7% in 2020, whereas in new first-tier cities, it rose steadily from 35.5% in 2017 to 42.7% in 2020. “These figures may not be entirely precise; we are discussing a trend.”

Jin Xuekun believes that the structural changes in the medical aesthetics industry are reflected in various aspects, such as urban distribution, age distribution, and consumer product categories. “As suppliers or service providers, we should recognize these subtle structural shifts and actively ‘cater to’ and lead these changes.”

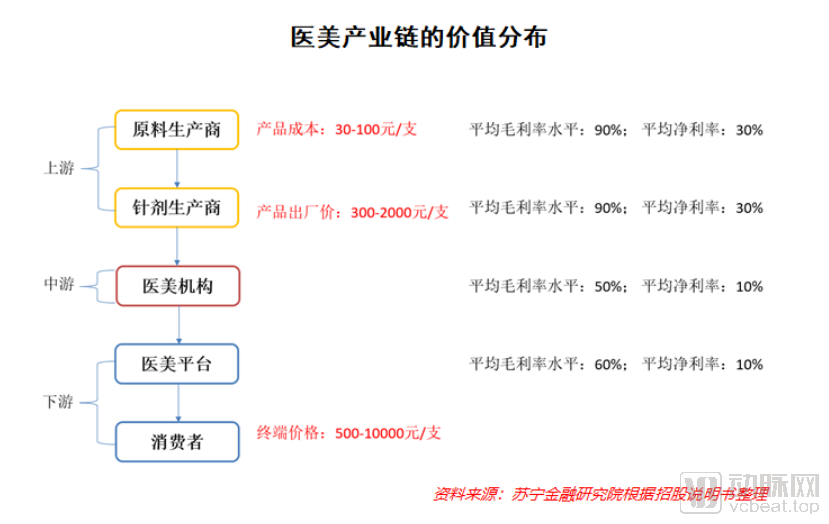

Uneven value distribution across the industry chain is another characteristic of the current medical aesthetics sector. At present, upstream enterprises in the medical aesthetics industry chain demonstrate strong profitability, while midstream and downstream players show relatively weak earnings performance, with an intensifying head effect.

According to Jin Xuekun, in the medical aesthetics industry chain, upstream companies—such as raw material manufacturers and injectable product manufacturers—have an average gross profit margin of 90% and an average net profit margin of 30%. In contrast, mid- and downstream entities, including medical aesthetics institutions and platforms, report average gross profit margins of 70%–80% and 60%, respectively, with average net profit margins of only 10%–15% and 10%, all of which are lower than those of upstream enterprises.

Source: Suning Finance Research Institute, “Real Data Reveals the Exorbitant Profit Margins in the Medical Aesthetics Industry”

What are the underlying reasons? The fragmentation of midstream service providers and high customer acquisition and marketing costs are the primary factors compressing profit margins for medical aesthetics institutions. According to the aforementioned report by Guoyuan Securities, traditional medical aesthetics institutions incur customer acquisition and marketing costs of 30%–50%, labor costs (primarily physician compensation) of 15%–25%, and consulting service costs of 3%–7%. When combined with operational and management expenses, these factors result in somewhat “weak” profitability for midstream service providers in the medical aesthetics industry.

However, in contrast, core enterprises at the upstream of the industry benefit from stringent regulatory policies specific to the pharmaceutical sector, high entry barriers for upstream players, and the difficulty in securing raw materials and technologies required for medical aesthetics product manufacturing. These factors ensure robust profitability and provide substantial security for upstream enterprises.

Therefore, materials and technologies are crucial for upstream enterprises to maintain high revenue-generating capabilities over the long term. Jin Xuekun believes that this may also serve as a strong guarantee for the sustained forward development of the entire industry.

“Over the next 5 to 10 years, the driving force behind industry development will not be demand but the upstream sector. The core drivers remain materials and technology, particularly materials.”

How Have Upstream Enterprises Become the Driving Force for Industry Development? Why Do Materials and Technology Remain the Core Drivers?

Jin Xuekun’s rationale is that materials and technology can transform latent demand into reality, with the majority of such materials and technologies controlled by upstream enterprises. “Much like the iPhone in its early days, people did not initially realize they had such a need; it was only after the iPhone emerged that they recognized its necessity. Materials and technology can drive transformative change within an industry.”

Currently, Jin Xuekun believes that the approval of non-hyaluronic acid Class III materials such as PCL and PLLA, along with technological iterations like EBD, will stimulate more diverse demand in the future, thereby driving the entire industry toward new directions.

As Jin Xuekun pointed out, leading upstream companies have indeed been actively expanding their product pipelines in recent times.

On February 21 this year, Haohai Biological Technology issued an announcement stating that it would inject RMB 70 million into Ouhua Meike and subscribe to RMB 52.03 million of its newly increased registered capital, thereby acquiring a 63.64% equity stake in Ouhua Meike for RMB 205 million. According to VCBeat, a key asset in Haohai Biological Technology’s acquisition of Ouhua Meike is Endymed Medical, an Israeli medical device company. Endymed’s professional medical equipment portfolio covers various dermatological treatment modalities, including radiofrequency, ultrasound, and UV light. Meanwhile, its consumer-grade high-tech device, Newa, is set to become the first FDA-cleared over-the-counter (OTC) home-use instrument for skin tightening, anti-aging, and facial contouring. This acquisition undoubtedly significantly strengthens Haohai Biological Technology’s capabilities in the energy-based devices (EBD) sector.

In April this year, Huadong Medicine made new strides in enriching its product pipeline with the approval of its PCL-based dermal filler (commonly known as “Girl’s Needle”). This approval marks the first time a non-hyaluronic acid filler has received official national recognition in China, thereby expanding the range of medical aesthetic products and meeting consumers’ diverse needs. Jin Xuekun commented, “This is a epoch-making milestone for the medical aesthetics industry this year. The approval of non-hyaluronic acid fillers has injected fresh blood and momentum into the industry’s development.” It is understood that Huadong Medicine’s newly approved “Girl’s Needle” product is composed of 30% polycaprolactone (PCL) and 70% carboxymethyl cellulose (CMC). Both materials are fully biodegradable, enhancing the product’s safety profile, while its primary functions are filling and tissue restoration. The launch of the first batch of this product signals the imminent opening of a new track in the injectable filler segment of the medical aesthetics market.

On April 22, the first polylactic acid (PLLA) facial filler (“Youth Rejuvenation Injection”) applied for by Changchun Shengboma Biomaterials Co., Ltd. was officially approved.

Meanwhile, the traditional hyaluronic acid sector has also witnessed new developments this year. Early this year, the National Health Commission officially approved Bloomage Biotech’s application to use hyaluronic acid as a novel food ingredient. Although the cosmetic efficacy of oral hyaluronic acid remains subject to considerable skepticism, this market segment has now formally entered its growth phase.

From a technical perspective, Jin Xuekun believes that technology is also one of the core drivers of industry development. “Currently, technologies are broadly categorized into four types: energy-based devices (EBD), topical application, transdermal delivery, and injection—these are inescapable fundamental approaches. Although regulations classify products into Class I, II, and III, these categories are still predominantly driven by the aforementioned technological modalities.”

Meanwhile, Jin Xuekun added that companies have considerable flexibility in choosing technical approaches, opting for micromachining or microfluidics, or alternatively developing microspheres, microcapsules, and gels.

Jin Xuekun believes that, from the demand side, the trend in the medical aesthetics industry is shifting from contour beauty to overall aesthetic state.

“In the earliest days of medical aesthetics, consumers sought to spend a thousand or ten thousand yuan to instantly enhance features such as the nose and eyes. Thus, early-stage, basic medical aesthetic procedures focused on rapidly addressing facial contouring. However, this represents the most rudimentary level of beauty; in the next stage, consumers pursue ‘wellness beauty’—a more advanced form of aesthetic enhancement.”

Jin Xuekun’s view is supported by relevant data.

According to data released by the China Fragrance and Flavor Cosmetics Industry Association, anti-aging treatments currently account for a mention rate of 72.2% among all medical aesthetic maintenance procedures, making them the most concerning and popular service category for Chinese women. The age at which Chinese women begin to focus on anti-aging has dropped from 25 to 23, and even as low as 20 years old. These figures indicate that female consumers are increasingly pursuing a natural and optimal state of beauty when selecting medical aesthetic treatments.

Regarding development trends on the supply side, Jin Xuekun identifies three key aspects: First, combination therapy regimens. “Future treatment protocols will inevitably be combination-based; for instance, topical therapies can be combined with injectable treatments.” Second, whole-course management. Third, strengthened interdisciplinary application.

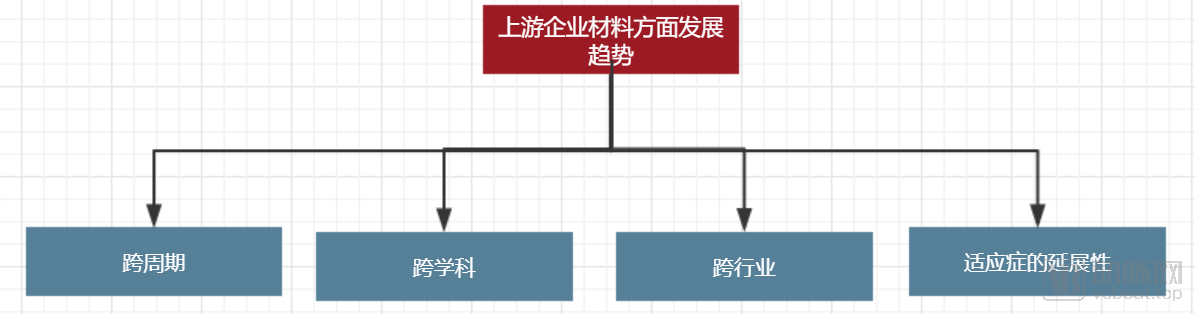

In addition, Jin Xuekun believes that upstream companies in the medical aesthetics industry will focus on four key areas in materials development in the future:

VCBeat Graphic

First, the material must have cross-lifecycle appeal, meaning it is not merely a short-lived trend but remains popular for a decade or even longer. Second, the material should be interdisciplinary; hyaluronic acid, perhaps the most well-known example, is such an interdisciplinary material. Third, the material must span multiple industries. “A major category of materials must cross industry boundaries; otherwise, it cannot become a mainstream material and may fall out of favor after a brief period of popularity.” Fourth, the material should offer expandable indications. For instance, botulinum toxin can be used both for wrinkle reduction and for treating hemifacial spasm.

“Only by focusing on these four key points can this industry be truly developed and scaled up,” said Jin Xuekun. “In the next decade of medical aesthetics, materials aligned with this logic will inevitably be dominated by ‘regenerative’ collagen.”