Amid Renewed Market Turbulence, Zhiyun Health Builds a Moat in Chronic Disease Management

2020 marked a milestone for the field of chronic disease management, ushering in a highlight moment following the “Hundred Glucose Wars.”

Zhiyun HealthYang Wenlin, CPO and Vice President

Zhiyun HealthYang Wenlin, CPO and Vice President

At the recently concluded “5th Future Healthcare Top 100 Conference,” numerous entrepreneurs and industry professionals convened at the Health Management Forum to conduct a comprehensive and in-depth analysis and discussion on service innovations and market trends in current chronic disease management.Ms. Yang Wenlin, CPO and Vice President of Zhiyun Health, was invited to attend and delivered a special report on “The ‘China Model’ of Internet+ Chronic Disease Management,” sparking heated discussion at the event.

It is evident that the “return” of chronic disease management has garnered widespread market attention and enthusiasm, gradually becoming the next key growth area in the internet healthcare sector. However, all developments follow certain patterns. In the field of chronic disease management, what exactly is driving its “resurgence”? Facing the new market landscape, what kind of solutions should companies deeply entrenched in this sector build to quickly “secure their footing”? VCBeat will address these questions by drawing insights from Ms. Yang Wenlin’s report.

According to statistical data, during the 2015 boom period in mobile health, there were over 2,000 mobile health apps, including more than 700 apps focused on diabetes management, accounting for approximately 30% of the entire mobile health app market.“The Battle of a Hundred Sugars”On the verge of eruption.

But the hype is always temporary. After the tide of trendiness recedes, the landscape of the diabetes market has evolved from its initial “chaotic competition” into“Warring States Period”, including leading apps such as Da Tang Yi, Wei Tang, Zhiyun Health, Tang Yisheng, and Tang Hushi, are accelerating their exploration of business models and adopting a strategy of “building substantial reserves and strengthening barriers” to secure a share of the multi-billion-dollar market.

However, in the field of chronic disease management, harvesting the ripe “fruit” is no easy feat; it requires a considerable wait. Yet this prolonged period is enough to wear down the last reserves of patience among enterprises and capitalists alike. In the aftermath of the initial hype, many have chosen to “exit,” leaving chronic disease management consigned to the “cold palace” and causing it to all but vanish from the public eye.

In 2020, this trend began to reverse. Amid the pandemic, two key factors refocused attention across sectors on mobile chronic disease management: First, older adults, particularly those with chronic conditions, became a high-risk group for COVID-19 due to diminished physiological function and weakened immunity. Second, road closures imposed by the pandemic and the need to prevent nosocomial cross-infection made internet-based chronic disease management essential.

As Ms. Yang Wenlin mentioned in her speech,Chronic disease management suddenly gained significant traction in 2020.

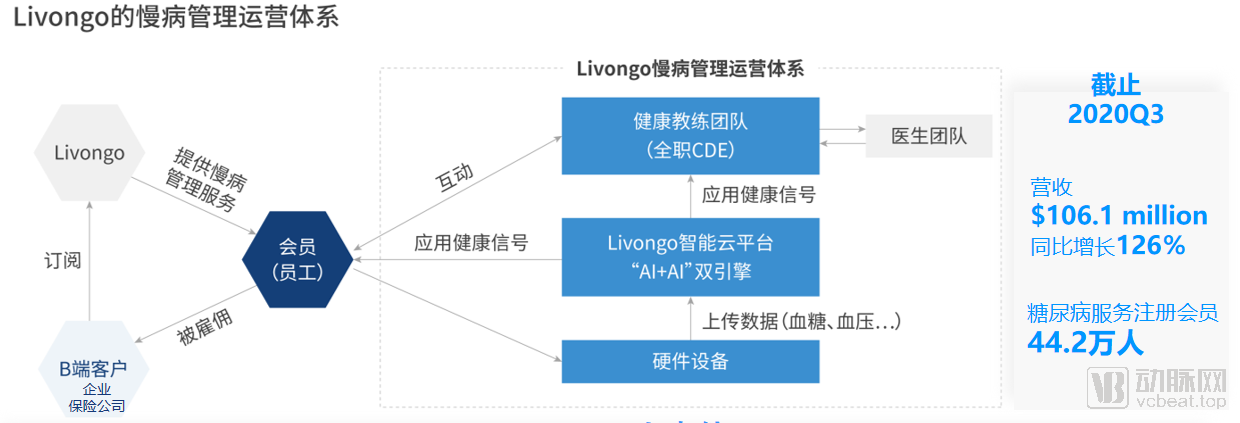

When discussing chronic disease management, it is impossible to overlook Livongo, the U.S.-based intelligent chronic care platform. Recognized as a “milestone” company in the industry, Livongo, founded in 2008, achieved a market capitalization of over $10 billion within just six years and went public on the Nasdaq in July 2019, becoming the first listed company in the chronic disease management sector. One year after its IPO, Livongo was acquired for $18.5 billion by Teladoc Health, a global digital health giant, with the combined entity’s valuation projected to reach $38 billion.

Livongo, in response to the demands of insurance companies and corporate clients, proposedApplying Health Signals(Applied Health Signals) concept, its business model mainly provides integrated health management services for chronic disease patients through an "AI+AI" intelligent system, thereby addressing the difficulty of cost control for U.S. commercial insurance companies, with B-side payments being the primary source of revenue.

Livongo’s business model is clear and straightforward, but in Ms. Yang Wenlin’s view, this “successful model” cannot be directly replicated in China’s chronic disease management sector.

Specifically, there are fundamental differences between the healthcare security systems of China and the United States, with the most pronounced disparity lying in the payment structure. The United States has a highly developed commercial insurance market, where commercial insurance coverage reaches 80%. In the past two years, annual commercial insurance expenditures have accounted for 10% of the U.S. GDP. Among these commercial health insurance plans, 90% are employer-sponsored. At the point of payment, employers typically cover 80% of the premium costs, while employees are responsible for the remaining 20%.

In contrast to other countries, China’s payment landscape is still dominated by basic medical insurance and critical illness pooling, with out-of-pocket payments and commercial insurance serving only as supplements. Therefore, it is not aligned with the current reality for domestic chronic disease management companies to target commercial insurers as their primary clients.

Beyond having a clear payer, the most significant factor contributing to Livongo’s success lies in its accurate grasp of market demand. For insurance companies, minimizing medical expenditures for corporate employees is naturally a priority. Compared with healthy employees, those with chronic diseases account for the bulk of insurers’ payouts. Consequently, enterprises urgently need to introduce viable solutions for employee health management to reduce subsequent medical costs. So, what are the pain points in the field of chronic disease management in China?

First, inefficiency leads to inadequate assurance of medical services.

Secondly, there is insufficient patient compliance.Due to patients’ lack of self-management awareness, it is difficult for hospitals to assume the role of continuous care managers. In traditional chronic disease management models, reliance is placed predominantly on pharmacological interventions, reflecting a reactive “treat-when-ill” mindset rather than implementing systematic prevention and control strategies. Consequently, there is a lack of seamless continuity across the pre-diagnosis, treatment, and post-treatment phases. Particularly, the “silo effect” in monitoring chronic disease indicators hinders both physicians’ ability to provide effective management and patients’ engagement in their own care.

Finally, there is inadequate health insurance coverage.A robust and transparent payment system has always been a key factor supporting the development of the healthcare sector. However, in the field of chronic disease management, the current payment framework remains inadequate. Taking out-of-pocket payments as an example, basic medical insurance and commercial insurance cover 54.7% of costs, while patients bear 45.3% out of pocket. There is an urgent need for a more effective and cost-efficient payment solution for chronic disease patients.

To address these challenges, “digitalization” may well be the optimal solution. As Ms. Yang Wenlin has pointed out, chronic disease management in China is a sector in urgent need of digital transformation, characterized by its large patient population, extended management cycles, and strong demand for personalized care. By leveraging digital technologies, it is possible to extensively intervene across multiple stages—including early-stage monitoring, follow-up management, and personalized chronic disease management services—thereby providing patients with convenient access to care at various service touchpoints.

The pandemic has injected new vitality into chronic disease management. However, to avoid settling for fleeting prosperity and instead achieve sustainable growth, it is imperative to overcome the various obstacles hindering long-term development. This is key to maintaining competitive market strength and serves as the crucial lifeline that enables companies to successfully “reach shore” after the turbulent waves subside.

As a “benchmark enterprise” in chronic disease management in China, Zhiyun Health has become an industry-leading unicorn and has gradually pioneered a Chinese model for chronic disease management.

Specifically, in terms of sub-sectors, as China's largest one-stop platform for chronic disease management and smart healthcare, Zhiyun Health has specially developed solutions targeting the needs of hospitals.“Zhiyun Yihui,” the chronic disease management SaaS platform with the highest coverage rate among mainstream hospitals in China, and “Zhiyun Internet Hospital,” the largest online communication service platform for chronic disease patients, doctors, and hospitals in China. The former focuses on building platforms for hospitals to enhance their overall operational efficiency, while the latter emphasizes providing services to patients, optimizing treatment outcomes by strengthening communication between doctors and patients.

In terms of medications with long-term demand among patients with chronic diseases, Zhiyun Health has meticulously crafted the most cost-effective solutions in China, based on the actual needs of patients and pharmacies.“Zhiyun Wenzhen” SaaS Platform for Pharmacy Prescription Services. This is Zhiyun Health’s third core product, designed to enhance the operational efficiency and profitability of pharmacies by providing professional and compliant pharmaceutical and medical services to offline pharmacies, while establishing and delivering 24/7 health management services across the pharmacy ecosystem, thereby enabling residents to more conveniently and affordably return to a healthy lifestyle.

Meanwhile, Zhiyun Health is also actively expanding its consumer-facing business and integrating partners across multiple industries—including healthcare and elderly care, media, retail, and community services—to create a full-industry-chain service platform, thereby pioneering an innovative “Internet Plus” model for chronic disease management. For instance, in collaboration with A-Living Services, it has establishedSmart Community Health Kiosk, in addition, Zhiyun Health also possesses China's largestSweet Home: A Vertical Community for Chronic Disease Management, the forum has over 10 million users, with more than 300,000 daily active users.

Overall, by leveraging its independently developed Hospital SaaS system, Pharmacy SaaS system, Internet Hospital platform, and Zhiyun Health App, Zhiyun Health has connected diverse scenarios across healthcare providers, pharmaceuticals, insurance, and community settings. It empowers various collaborators along the industry chain with digital capabilities, creating a robust network ecosystem effect through innovative and scalable solutions, ultimately enhancing the overall efficiency and service capacity of chronic disease management.

Currently, there are nearly 500 million people in China with chronic diseases or at risk of developing them, indicating that the chronic disease management market in China still has substantial unmet demand. On the other hand, as cutting-edge technologies such as AI, 5G, and cloud computing continue to permeate the healthcare sector, digital chronic disease management is poised to become an even larger market segment in the future.

Based on this, for chronic disease management companies, how to better integrate Internet technology into the service system, quickly address the existing problems facing the industry, and demonstrate greater value to the healthcare sector will be the primary direction of our joint exploration.