Digital Chronic Disease Management, Digital Marketing, and RWS: Which Holds the Greatest Potential in Pharmaceutical Digital Innovation?

Among the various industry stakeholders in the healthcare sector, the pharmaceutical industry, as a provider of therapeutic solutions, is advancing its digital transformation from an initial stage toward greater depth. Based on preliminary research, we have identified that, starting from the actual digital transformation needs of pharmaceutical companies, initiatives can primarily be implemented across five key scenarios.

As digital technologies permeate the pharmaceutical industry, they enable pharmaceutical companies to achieve agile operations across the entire value chain, from research and development and manufacturing to distribution and sales.

The five major scenarios represent the core pain points and demands of pharmaceutical enterprises seeking to accelerate growth and enhance efficiency through digitalization. But how should they undergo digital transformation? Traditional pharmaceutical companies, despite their profound understanding of disease mechanisms and clinical pain points, often find themselves ill-equipped for this challenge. In contrast, digital-native firms with expertise in applying digital technologies offer appropriate solutions to these market pain points.

To further support connectors within the industry, the 2020–2021 Pharmaceutical Company Digital Solution Innovation Competition was successfully launched. The event was hosted by Microsoft China and Zhangjiang Group, with strategic partnerships from AstraZeneca, Johnson & Johnson, Sanofi, Merck, Novartis, and Roche, and supported by the CEIBS Alumni Healthcare Industry Association, Zhangjiang Sci-Tech Investment, Microsoft Accelerator, Microsoft AI and IoT Lab, Wuxi International Life Science Innovation Park, Legend Capital, and Probes Capital. Operated by VCBeat, the competition ultimately selected ten winning companies from over one hundred applicant innovative enterprises, based on six evaluation criteria: team strength, relevance to pain points, solution innovation, case implementation, technical feasibility, and market potential.

Here, to uncover the hidden trends in medical digitalization behind the data, VCBeat has compiled and analyzed the relevant data of all participating enterprises in this competition, aiming to identify where the new forces driving the digitalization of the pharmaceutical industry truly stand.

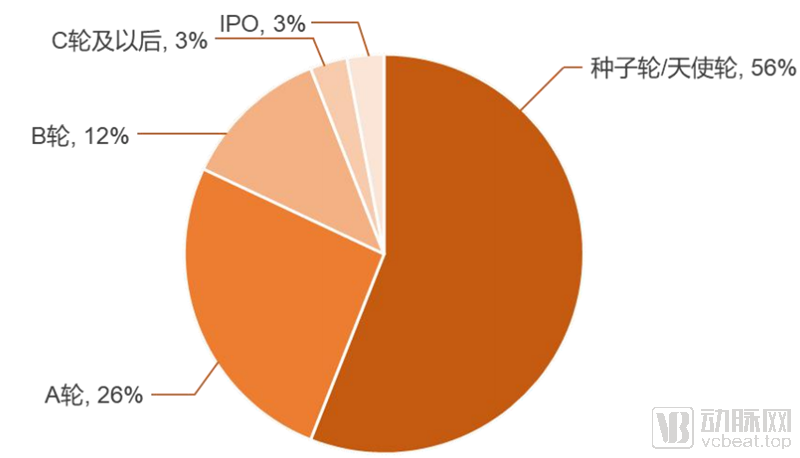

As shown in the chart, the majority of companies participating in this IPS Innovation Competition are at funding stages ranging from Seed to Series A, accounting for over 80% of all participants. In contrast, companies at Series C and later stages represent a relatively small proportion, less than 20%. Looking at each funding stage individually, companies at the Seed stage or with no prior financing constitute the largest share at 36%. Companies at the Angel and Series A stages account for 26% and 20%, respectively, showing a modest difference. The proportion of companies at Series B drops noticeably to 12%. Companies at Series C and beyond, including listed companies, have the lowest participation rate, at just 3%.

It is well known that companies in later funding rounds tend to be more mature in terms of capital raising and the establishment of talent and technical systems. At this stage, their need for collaboration with large pharmaceutical companies and digital technology firms is relatively lower. In contrast, early-stage startups, which more commonly face incomplete technical platform development and relative capital shortages, demonstrate a stronger need to leverage external resources for building technical platforms and attracting talent.

Participating companies have tailored their strategies to leverage their respective team capabilities and technical expertise, focusing on different aspects of the five key application scenarios for implementing digital technologies in the pharmaceutical industry. It is evident that nearly 60% of these companies have heavily invested in “empowering patients and the general public,” adopting a patient-centric approach to better address clinical needs and helping pharmaceutical companies extend their role beyond mere drug suppliers to become part of a broader patient empowerment ecosystem.

Next is leveraging digital technologies to accelerate medical R&D innovation (43%) and optimize practitioner experience (41%). On one hand, this provides foundational data support to help pharmaceutical companies achieve full lifecycle management of their products; on the other hand, it enables comprehensive digital adoption in the management and organizational structure of the pharmaceutical industry, helping employees improve work experience and efficiency while enhancing corporate profitability.

Establishing Agile Operational Processes (35%) is the next strategic priority for enterprises: leveraging digital tools to help pharmaceutical companies achieve agile operations across the entire value chain—from R&D and manufacturing to distribution and sales—thereby maximizing operational value through the most efficient pathways.

Compared with the deployment in the other four major application scenarios, startups are somewhat lacking in safeguarding medical information security, accounting for only slightly more than one-quarter of the total (29%). Nevertheless, the importance of protecting medical information security is self-evident, as it will, to a certain extent, influence the digital transformation of the entire healthcare industry. With the maturation of cloud technologies and the continuous enhancement of data security levels, migrating data to the cloud has become an inevitable trend in the development of the pharmaceutical industry.

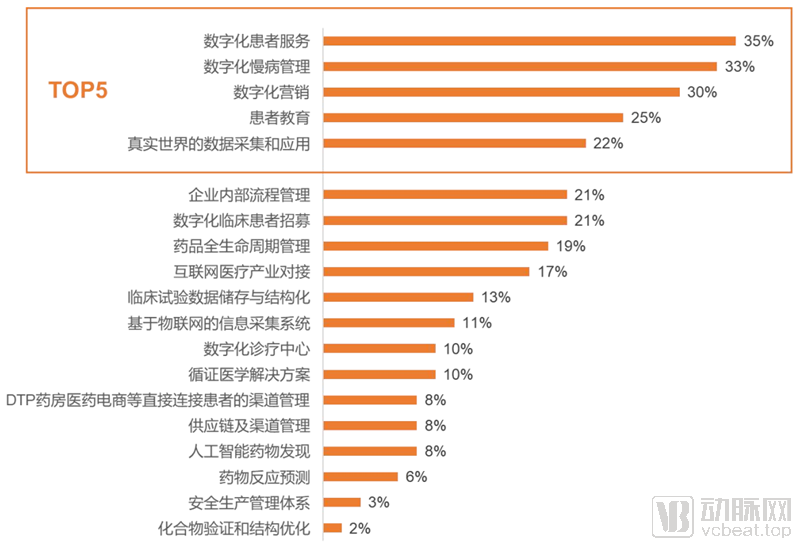

Given that each of the five major scenarios encompasses various sub-scenarios, VCBeat has compiled statistics on the distribution across 19 sub-scenarios within these five major categories to help readers gain a clearer understanding of how digital health companies are positioning themselves. Additionally, we provide brief introductions to the five sub-scenarios with the highest number of company engagements.

As shown in the figure, among the 19 specific scenarios where digital technologies have been implemented, the five most widely adopted by enterprises are: Digital Patient Services (35%), Digital Chronic Disease Management (33%), Digital Marketing (30%), Patient Education (25%), and Collection and Application of Real-World Data (22%).

Digital patient services typically refer to internet hospitals or digital health enterprises leveraging online platforms to connect physicians, nurses, and patients. These services facilitate communication and care delivery between healthcare providers and patients through information and data sharing. Digital patient services encompass a wide range of offerings, including AI-driven self-service and AI-assisted physician services, providing patients with appointment scheduling, medical consultations, interpretation of various pathology reports, prescription issuance, pharmaceutical care, and guidance on care pathways. The comprehensiveness of these services varies depending on the development and capabilities of each platform.

Online medical records and offline test results provided by patients can help physicians gain a more accurate understanding of patient conditions during real-time consultations, enabling precise patient profiling. Many digital patient service platforms complement hospital internal systems, serving to channel patients to offline hospitals and strengthen patient loyalty to these institutions.

For pharmaceutical companies, analyzing and organizing patient feedback data from online platforms enables in-depth exploration of patients’ clinical needs and clear identification of their clinical pain points. This provides valuable guidance for selecting new drug development directions and improving drug formulation designs. Some pharmaceutical companies have also strengthened patient engagement and communication by embedding process-oriented services into internet platforms, thereby enhancing patient loyalty to branded medications.

Traditional chronic disease management models primarily follow the workflow of “diagnosis, treatment, rehabilitation, and follow-up.” Healthcare professionals in hospitals and community settings serve as the main implementers, undertaking multiple responsibilities including prevention, health maintenance, medical care, rehabilitation, and health education. In traditional chronic disease management, the key to effective management still relies heavily on “human resources.” However, in the face of a continuously growing population of patients with chronic diseases, human resources alone are clearly insufficient to meet the substantial management demands.

Most patients with chronic diseases generally receive adequate treatment during hospitalization; however, given the vast number of such patients, healthcare providers are often unable to provide sustained care once they are discharged. This significantly undermines the effectiveness of management by existing medical institutions and constitutes a primary reason for the substantial burden posed by chronic diseases.

Currently, China has up to 300 million patients with chronic diseases, and these conditions cause annual losses exceeding RMB 5 trillion to the country. A report from Qianzhan Industry Research Institute shows that more than 60% of patients do not take their medications as prescribed after discharge; poor medication adherence is a key factor leading to suboptimal therapeutic outcomes and complications, and it is also a major reason why medical costs remain difficult to control.

Digital chronic disease management has, to a certain extent, effectively addressed this issue: digital technologies can be integrated into various stages of hospital-based care, including early-stage patient monitoring, follow-up management, and personalized chronic disease management services, thereby enhancing the efficiency of healthcare institutions in managing chronic diseases.

Digital management platforms, in conjunction with complementary smart in vitro monitoring devices provided by enterprises, enable real-time monitoring of patients’ physiological conditions and transmission of this data to physicians. Some digital management platforms also offer AI-powered report analysis and graphical trend management. This not only allows physicians to assess disease progression in real time and maintain patient records, but also facilitates the flexible formulation of treatment plans and provides remote guidance for patients’ self-management of their conditions. As a result, patient medication adherence is improved, and pharmaceutical companies, as direct suppliers of medications, also benefit indirectly.

Furthermore, by organizing and analyzing patient medical data accumulated on online platforms, pharmaceutical companies can gain a more precise understanding of patients’ needs and outcomes during actual medication use.

Digital Pharmaceutical Marketing primarily refers to the online promotion of prescription drug products under pharmaceutical companies, utilizing digital tools or digital-based application scenarios. It represents the current trend of close collaboration between pharmaceutical companies and internet platforms.

Digital marketing in the pharmaceutical industry helps pharmaceutical companies move the visits of medical representatives, which originally took place offline, online. This not only reduces corporate sales costs and expands sales channels but also improves the efficiency of utilizing doctors' idle time, earning welcome from hospitals.

Furthermore, compared with offline promotion, digital marketing enables more effective recording and accumulation of physician visit data. Through online marketing, platforms can faithfully document the entire communication process between pharmaceutical representatives and physicians, thereby converting it into proprietary data assets for pharmaceutical companies.

By analyzing big data from medical representative visits, pharmaceutical companies can not only create physician profiles to enhance their understanding of clients but, more importantly, gain insights into the performance of medical representatives. This enables representatives to identify areas for improvement in their work, thereby boosting efficiency and fostering mutual growth between employees and the company.

VCBeat industry data show that the scale of China’s pharmaceutical digital marketing market has been growing year by year, reaching RMB 1.57 billion in 2019. The outbreak of the COVID-19 pandemic at the end of 2019 severed the offline connections between pharmaceutical sales representatives and physicians due to physical distancing measures, severely disrupting traditional marketing channels and rendering them nearly inoperable. As a result, pharmaceutical digital marketing has further advanced.

From the patient’s perspective, online platforms provide rich and systematic disease education by offering expert explanatory videos and disseminating science-based information related to patients’ conditions. This helps patients acquire disease-related knowledge, enhance their understanding of their condition and treatment options, and receive personalized, targeted guidance and education.

From the perspective of pharmaceutical companies, while patients utilize online platforms for disease management and to learn about related conditions, this also presents an opportunity for companies to engage directly with patients.

Patients active on digital pharmaceutical platforms are predominantly those requiring long-term disease management. Such management entails a continuous, long-term demand for medications. By aggregating physician resources on online platforms, pharmaceutical companies provide corresponding disease management services to patients. This approach not only helps patients recognize and understand their conditions but also enhances awareness and understanding of the companies’ pharmaceutical products, thereby successfully achieving pharmaceutical promotion.

Real-world data (RWD) collection encompasses various aspects of patients’ lives, including medication use, medical visits and treatments, and adverse reactions; these data are generated through real-world studies (RWS). Real-world studies refer to research in which data are derived from real-life healthcare settings, reflecting actual clinical practices and patients’ health status under real-world conditions. The purpose of such studies is to understand the impact of a given medical product on the health of the study population. By leveraging large volumes of real-world healthcare data, these studies identify and quantify the benefits, risks, and outcomes of various intervention strategies, evaluate the safety and effectiveness of medical products, uncover unmet needs, and generate insights using robust and scientific methodologies to support product value positioning.

Since its introduction to China in 2010, Real-World Study (RWS) has garnered significant attention, particularly in the fields of clinical medicine and regulation. On January 7, 2020, the National Medical Products Administration (NMPA) issued its first policy document of the year dedicated to real-world studies. On July 1, the newly revised Measures for the Administration of Drug Registration came into effect, requiring drug marketing authorization holders to proactively conduct post-marketing studies for new products. On August 3, the Guidelines for Real-World Data to Generate Real-World Evidence (Draft for Comment) were released. This policy emphasis has propelled the development of real-world studies in China onto a “fast track.”

During the pandemic, China launched “new infrastructure” initiatives, represented by big data and artificial intelligence. In early April 2020, the State Council issued the “Opinions on Building a More Complete System and Mechanism for Market-Based Allocation of Production Factors,” clearly establishing data as a new type of production factor and ushering medical big data into its “second half.”

Value output is a key characteristic as healthcare big data enters its next phase. Crude data collection methods and poor data quality will be phased out, replaced by high-quality data integration, analysis, mining, and more comprehensive utilization. The value of data is evolving from merely summarizing medical practices to supporting clinical decision-making and providing comprehensive AI-assisted diagnostic support.

Digital technology-based real-world studies can mine valuable biomarkers from big data, helping pharmaceuticals further identify effective target populations, thereby improving the efficacy of drug treatments.

The chart shows that the use of big data and artificial intelligence (AI) technologies is widespread among enterprises: 81% of companies have adopted big data solutions, while the adoption rate for AI technologies stands at approximately 68%. AI and big data have long evolved from pioneering attempts in select sectors to foundational technologies applied across a broad range of fields.

In the healthcare industry, artificial intelligence and big data are widely applied in drug development, clinical research, patient services, marketing, and internal enterprise management.

Because artificial intelligence (AI) requires learning from historical data and algorithmic training to acquire “intelligence” and achieve upgrades and improvements, large volumes of high-quality medical data form the foundation for AI’s decision-making capabilities. To a certain extent, AI and big data are two sides of the same coin. AI without data is akin to cooking without rice, a phenomenon that is particularly evident in the healthcare industry. On the other hand, without AI intervention to refine, clean, and analyze big data, it is difficult to fully unlock the value embedded in medical big data through manual methods alone.

Other digital technologies, such as blockchain, the Internet of Things (IoT), containers, and VR/AR/mixed reality, are more focused on specific business operations. For instance, the transmission of patient physiological data via wearable devices leans more toward IoT applications, while remote teaching using medical instruments or virtual simulations for surgical procedure training is more aligned with VR/AR/mixed reality technologies.

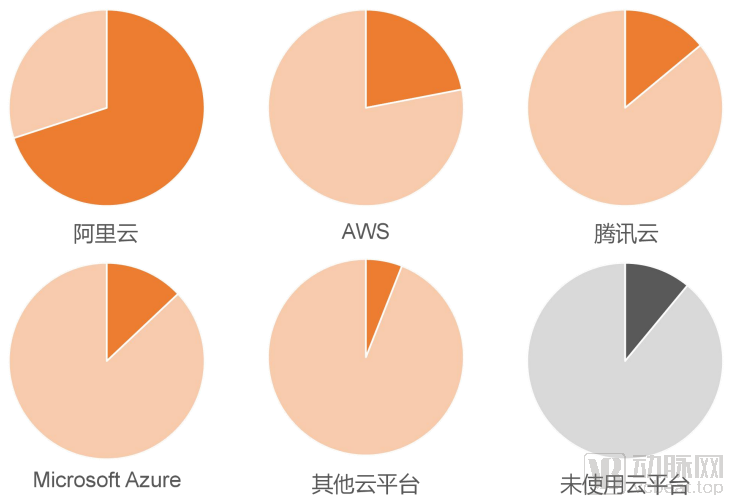

In terms of the popularity of single-cloud platform adoption among enterprises, Alibaba Cloud ranks first, chosen by 70% of companies. AWS follows as the second most popular option, selected by nearly 22% of enterprises. The adoption rates for Tencent Cloud and Microsoft Azure are comparable, at 14% and 13%, respectively. Additionally, a small number of enterprises opt for other cloud platforms, such as Huawei Cloud, Ping An Cloud, and Government Cloud.

Based on the actual practices of enterprises using cloud computing platforms, the vast majority have adopted multiple (1–3) cloud platforms simultaneously. This indicates that, in current practical development, hybrid clouds composed of platforms from different providers have become a standard choice for enterprises delivering cloud-based solutions.

It is worth noting that among all participating enterprises, 11% still do not use cloud platforms. In fact, surveys of these companies revealed that only two reported having neither adopted cloud services nor any need to do so. Meanwhile, most enterprises that have already deployed on cloud platforms indicated that they still have additional cloud adoption needs at their current stage of development.

This indicates that the cloud migration of pharmaceutical solutions is still ongoing. Although most solutions have already been deployed on the cloud, there remains substantial untapped demand for further cloud adoption.

The cloud platform serves as the foundation for solutions. As pharmaceutical industry-specific solutions accumulate on the cloud platform, a comprehensive cloud-based solution ecosystem can be established. This ecosystem comprises three key stakeholders: cloud service providers, pharmaceutical companies, and solution providers. Cloud service providers deliver underlying cloud platform infrastructure; solution providers leverage cloud computing and storage resources to offer tailored services to pharmaceutical companies; and pharmaceutical companies, as the paying clients, embrace digital technologies to reengineer their operational workflows.

Building an ecosystem requires the joint efforts of three parties; any unilateral attempt will stall the digital transformation of the pharmaceutical industry. In fact, this holds true for the digital transformation of the entire healthcare industry as well. All industry participants should maintain an open mindset and embrace this wave of industrial transformation.

Scan the mini-program QR code below to access the full report: “Healthcare Digital Innovation Quarterly: Identifying High-Potential Players in Pharmaceutical Digital Transformation”