Waterdrop Inc. Goes Public on NYSE Backed by Tencent's Five-Round Investment, Valued at Over $3.8 Billion

After just five years in operation, Waterdrop Inc. successfully went public.

VCBeat has learned that on the evening of May 7 (Beijing time), Waterdrop Inc. officially listed on the New York Stock Exchange, ringing the opening bell under the ticker symbol “WDH.” The company’s initial public offering consisted of 30 million American Depositary Shares (ADSs). The underwriting syndicate included Goldman Sachs, Morgan Stanley, Bank of America Merrill Lynch, as well as Chinese securities firms such as Agricultural Bank of China Securities, China Merchants Securities, and CITIC Securities. The IPO was priced at $12 per share, with an opening trade price of $10.25 and a closing price of $9.70. The company’s market capitalization stood at $3.823 billion, equivalent to over RMB 24.6 billion.

(Image source: East Money)

Since its inception, Waterdrop Inc. has been a “star enterprise,” favored by numerous investors.To date, Shuidi Inc. has completed five rounds of financing, raising a total of over RMB 4 billion. Investors include leading investment firms and tech giants such as Tencent, Boyu Capital, Gaorong Capital, Swiss Re, IDG Capital, Sinovation Ventures, ZhenFund, CICC Capital, BlueRun Ventures, and Meituan’s Strategic Investment Department. Among them, Tencent is a long-term investor in Shuidi, having participated in all five funding rounds. It is currently the largest institutional shareholder, holding a 22.1% stake.

Notably, Shen Peng, the founder of Shuidi Inc., joined Meituan’s startup team after graduating from the Central University of Finance and Economics, rising from an intern to head of Meituan Waimai’s national business team. After leaving Meituan in 2016, the 29-year-old Shen established Shuidi Inc., marking his first venture as the lead entrepreneur.

(The image shows the bell-ringing ceremony)

As China's leading insurance and health services technology platform, Waterdrop Inc. is committed to partnering with collaborators to build a Chinese version of "UnitedHealth Group."The prospectus shows that Waterdrop Inc. currently has two major business segments: insurance protection and health services.The insurance protection segment includes business lines such as Shuidichou and Shuidibao; the health services segment includes business lines such as Shuidi Health and Shuidi Haoyaofu.

In terms of revenue, Waterdrop Inc. has seen continuous growth over the past three years, with revenues of RMB 238 million, RMB 1.511 billion, and RMB 3.028 billion in 2018, 2019, and 2020, respectively. On the other hand, the company’s net losses for the same period amounted to RMB 209.2 million, RMB 321.5 million, and RMB 663.9 million, respectively, indicating an accelerating trend in losses.

In recent years, the insurtech sector has entered an acceleration phase, with companies frequently securing financing.According to a report released by Willis Towers Watson, global insurtech financing reached $7.1 billion in 2020, setting a new historical high and representing a 12% increase from 2019. The number of financing deals also hit an all-time high of 377, a year-on-year increase of 20%. Among these, there were 20 deals valued at over $100 million each (among Chinese companies, Waterdrop ranked fourth globally with $380 million in annual financing). Furthermore, U.S. insurtech giants GoHealth and Oscar Health both went public within the past year.

In a rapidly growing sector, Waterdrop’s initial public offering marks the beginning of its scrutiny by the secondary market. What narrative can Waterdrop truly present? In what direction will its future development evolve? Perhaps we can gain insights into Waterdrop’s future potential by examining the company and its founding team’s track record, financial performance, and business layout.

From the germination of an idea to founding a company and then successfully going public, Shen Peng and his Waterdrop Company took only five years.Behind such rapid development lies Shen Peng’s years of accumulated experience at Meituan.

In 2010, Shen Peng, then about to graduate from the Central University of Finance and Economics, joined Wang Xing’s team as an intern, becoming Meituan’s 10th employee. He embarked on Meituan’s entrepreneurial journey and, over the next six and a half years, witnessed firsthand its evolution from early-stage exploration into a major internet giant.

In this process,Shen Peng has repeatedly participated in Meituan’s internal “zero-to-one” projects.In the early days of Meituan’s group-buying expansion, Shen Peng took 50,000 yuan to Tianjin to launch a directly operated city office, propelling Tianjin’s performance to second place company-wide within the first month, trailing only Beijing. At age 23, owing to his outstanding performance, Shen was promoted to Regional Manager, overseeing a team of 400 employees across Beijing, Tianjin, and Shandong, and participating in the historic “Group-Buying War” that marked a pivotal chapter in the history of mobile internet. At age 26, Shen joined Wang Huiwen, co-founder and Senior Vice President of Meituan, to pilot Meituan Waimai (food delivery) business, leading the team to achieve the industry’s top position within just over a year.

(The image shows a group photo of Shen Peng and Wang Xing.)

(The image shows a group photo of Shen Peng and Wang Xing.)

“Over more than six years at Meituan, the accumulation of experience and learning has given me a deeper understanding and insight into entrepreneurship, as well as the confidence to try it myself,” Shen Peng told VCBeat in a previous exclusive interview. “In early 2016, I noticed that China’s aging population problem was becoming increasingly severe. A report I saw at the time predicted that over the next 10–15 years, the median age of China’s population would rise from 34 to 43, an increase of approximately 10 years—a major demographic trend. Additionally, regarding specific business opportunities, I encountered a situation where a former colleague’s family member fell ill but could not afford treatment. I initiated a fundraising effort among colleagues, but the efficiency was very low. To address these issues, I founded Shuidi Mutual Aid.”

After formally resigning, Shen Peng rented an office in Beijing’s Wangjing SOHO. The company was registered under the name “Beijing Zongqing Xiangqian Technology Co., Ltd.,” a phrase drawn from the closing remark Wang Xing often used in public speeches: “Let go of the past and move forward with passion.” Early team members, including Yang Guang and Jiang Wei, had all followed Shen Peng from Meituan.

Interestingly, thanks to his outstanding performance at Meituan, Shen Peng received millions of RMB in transfers via WeChat and Alipay as soon as he launched his startup, with many of the investments coming from his former Meituan colleagues. When Xu Xiaoping, founder of ZhenFund, learned that Shen Peng had embarked on his entrepreneurial journey, he immediately invited him to dinner together with Wang Qiang. “Shen Peng said he didn’t need money because he already had plenty. So, at the China World Hotel, Wang Qiang and I treated him to quite a few drinks and managed to secure some equity shares,” Xu Xiaoping revealed.

Shortly thereafter, Shuidi Inc. secured investments from multiple renowned investment firms. Shen Peng and his company further demonstrated the project’s robust viability through their actions: within just 100 days of launching Shuidi Mutual Aid, the membership base surpassed one million.

As entrepreneurship deepened, Shen Peng began to lead Waterdrop Inc. in focusing on health insurance and gradually advancing toward becoming a comprehensive health platform company. During this process, Waterdrop Inc. received recognition and support from Tencent. According to the VCBeat database,Since participating in Shuidi’s angel round in 2016, Tencent has taken part in every subsequent funding round of the company. In terms of shareholding, Tencent is Shuidi’s largest institutional shareholder, holding a 22.1% stake prior to its IPO.

A rapidly expanding sector, a strong team background, and the backing of top-tier capital and enterprises have been key factors driving Shuidi Inc.’s rapid rise over the past five years.But setting these aside, what are Waterdrop Inc.’s strategic initiatives and visions at the business level? How is it currently performing? What trends are emerging? These questions may be partially answered by examining its prospectus.

Waterdrop’s revenue is growing rapidly.

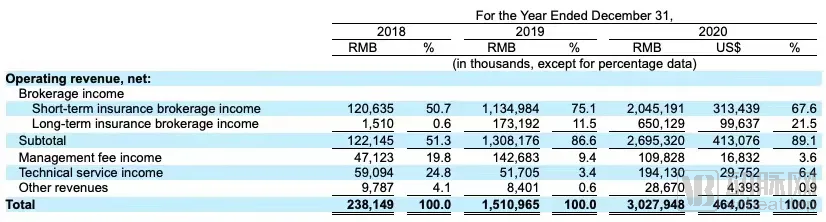

According to the prospectus, Waterdrop’s revenue reached RMB 3.0279 billion in 2020, representing a year-on-year increase of 100.4%. In 2019, the company’s revenue was RMB 1.511 billion, marking a 534.6% increase compared with RMB 238.1 million in 2018. This indicates that Waterdrop’s overall business scale is expanding rapidly.

Among these figures, insurance commissions over the past three years were RMB 122 million, RMB 1.308 billion, and RMB 2.695 billion, accounting for 51.3%, 86.6%, and 89.1% of Waterdrop Inc.’s total revenue, respectively. From this perspective, the insurance business is currently a key growth engine for Waterdrop Inc.’s revenue.

(Image source: Shuidi Inc. prospectus)

(Image source: Shuidi Inc. prospectus)

However, on the other hand, Waterdrop Inc.’s losses have been widening. In 2018, 2019, and 2020, Waterdrop’s net losses amounted to RMB 209 million, RMB 322 million, and RMB 664 million, respectively. The adjusted EBITDA losses (Non-GAAP) for 2018, 2019, and 2020 were RMB 140 million, RMB 159 million, and RMB 247 million, respectively, with EBITDA loss margins of 58.93%, 10.52%, and 8.17% over the three-year period.

With Revenue Expanding on One Side and Losses Deepening on the Other, Is Waterdrop’s Business Model Viable?

Let’s examine the positioning of Shuidi Inc. According to Shen Peng’s remarks at the recent Healthy China Forum,Shuidi Inc. is committed to building an extensive network of insurance protection and health services through medical fundraising, an insurance platform, and a health service platform.

At the operational level, this is reflected in the insurance protection segment’s Shuidi Bao and Shuidi Chou business lines, as well as the medical health segment’s Shuidi Health and Shuidi Haoyaofu business lines.

First, observe the business performance of the insurance coverage segment.

Shuidi Mutual Aid has been terminated following an upgrade implemented over a month ago. As a free online platform for personal fundraising for critical illnesses, Shuidi Chou itself does not generate revenue; rather, it primarily serves to drive user traffic and provide insurance education. As of December 31, 2020, more than 340 million people had donated a total of over RMB 37 billion to more than 1.7 million patients through the Shuidi Chou platform. In terms of fundraising volume in 2020, Shuidi Chou ranked first among numerous critical illness fundraising platforms in China.

Waterdrop Insurance, positioned as an internet insurance platform, serves as the primary revenue source. According to Waterdrop’s prospectus, the cumulative number of paying insurance customers reached approximately 1.7 million, 8.8 million, and 19.2 million as of December 31, 2018, December 31, 2019, and December 31, 2020, respectively. The cumulative number of paid insurance policies amounted to 30.7 million as of December 31, 2020.

As can be seen from the above, in the insurance protection segment, Waterdrop Company leverages Shuidichou and Shuidi Huzhu for user education and social fission to reach users. By raising awareness of the financial gaps associated with diseases and medical care, it converts this protection consciousness into insurance purchases, thereby completing the closed loop of its business model.

Let’s examine the business performance of the health services segment.

Since last year, Waterdrop Inc. has expanded into the health services sector, launching initiatives such as “Waterdrop Good Medicine Pay” and “Waterdrop Health.” Taking “Waterdrop Good Medicine Pay” as an example, within less than a year of its launch, the service has partnered with more than ten renowned domestic and international pharmaceutical companies and over 1,400 DTP (Direct-to-Patient) pharmacies. It has cumulatively served more than 100,000 patients, helping them save up to RMB 20 million in medical expenses.

Therefore, it is not difficult to find that,From a business architecture perspective, Waterdrop’s various business lines are strongly interconnected. For instance, Waterdrop Crowdfunding focuses on user acquisition and market education, while Waterdrop Insurance is responsible for monetization—a key driver behind Waterdrop’s robust revenue generation. Furthermore, the payer role established through these insurance coverage businesses provides strategic support for the future development of Waterdrop’s health services segment.

If the business logic holds up, then where are Shuidi Inc.’s losses?

As can be seen from the prospectus,Waterdrop’s primary expenditure is on marketing and customer acquisition.. From 2018 to 2020, Shuidi Inc.’s sales and marketing expenses were RMB 185 million, RMB 1.056 billion, and RMB 2.131 billion, respectively. In other words, Shuidi Inc. has been continuously expanding its revenue scale by acquiring customers through marketing efforts.

Does this indicate that Shuidi Inc. is relying on "cash burn" to drive growth? This requires assessment from two perspectives: first, whether losses remain controllable; and second, what mid- to long-term objectives are to be achieved.

Regarding Controllability. Based on Waterdrop Inc.’s cost structure, marketing and customer acquisition costs accounted for 69.92% and 70.36% of total revenue over the past two years, respectively, indicating that the effectiveness of marketing and customer acquisition has not been negatively impacted by the growth in revenue scale.

Regarding Mid-to-Long-Term Goals. With its inherent internet DNA, Waterdrop naturally enjoys lower customer acquisition costs, enabling rapid market expansion and the pursuit of economies of scale, which in turn drive further cost efficiencies. Currently, Waterdrop’s per-customer acquisition cost is below the industry average, giving it a significant cost advantage. Calculations show that in 2020, Waterdrop Insurance’s customer acquisition cost per paying user was approximately RMB 168, whereas public reports indicate that traditional insurers face acquisition costs as high as several thousand yuan. This provides Waterdrop with ample confidence to increase marketing and customer acquisition spending to capture a larger market share.

In summary, Waterdrop Inc. currently demonstrates strong growth momentum and is continuously driving revenue expansion through customer acquisition strategies such as marketing. Underpinning this performance is the ecological synergy advantage derived from Waterdrop’s clear business closed-loop. Nevertheless, it remains crucial to note that the company faces significant challenges in sustaining cost reduction and efficiency improvements, while actively expanding amidst evolving industry regulatory environments.

China’s health insurance industry is entering a phase of rapid development.

In 2020, China’s gross written premiums for health insurance exceeded RMB 800 billion. According to projections by VBInsight, the scale of health insurance premiums will surpass RMB 1 trillion for the first time in 2022, and is expected to reach RMB 2.021 trillion by 2025, indicating substantial market growth potential.

At the policy level, health insurance, as a key component of innovation in healthcare payment, has been frequently referenced in policy documents. On March 5, 2020, the “Opinions on Deepening the Reform of the Healthcare Security System” issued by the Central Committee of the Communist Party of China and the State Council included the statement: “Establish a multi-tiered healthcare security system with basic medical insurance as the mainstay, medical assistance as the safety net, and complementary development of supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid.” This provides top-level design for China’s healthcare payment system.

Riding the trend, a large number of enterprises and capital have poured into the health insurance sector in recent years.Major financing events over the past year include Insurance Geek securing $25 million in Series C funding, Nanyan Insurance Technology raising RMB 250 million in Series C funding, and Nuanwa Technology obtaining RMB 100 million in Series A funding. Moreover, Chinese health insurance technology companies have demonstrated remarkable frequency in fundraising. For instance, Yuanxin Huibao completed three rounds of financing within two years, Medxint Health secured five rounds in three years, Miao Health closed four rounds in four years, and Insurance Geek finalized seven rounds in five years.

The overall fundraising pace reveals a growing number of health insurance technology companies reaching Series C and D rounds, indicating that China’s health insurance enterprises are on the verge of going public. However, the industry still faces significant challenges in closing the loop between “health management and health insurance.” Persistent obstacles such as information asymmetry, low levels of specialization, high claims ratios, and weak profitability continue to hinder the development of the health insurance sector.

In contrast, the U.S. health insurance market has already given rise to industry giants such as UnitedHealth Group.As a component of the U.S. S&P 500 Index, UnitedHealth Group has seen its stock price increase more than 15-fold over the past decade, with current annual revenue exceeding $240 billion.Notably, when UnitedHealth went public in 1984, it positioned itself as a technology platform within the healthcare industry and has continuously pursued technological innovation.

(The image shows the UnitedHealth Group building)

(The image shows the UnitedHealth Group building)

At this juncture, domestic enterprises have also begun to prioritize technology and actively strategize their layouts. In its prospectus, Waterdrop Inc. highlighted that the company’s unique advantage lies in “advanced technology and differentiated data insights.” Specifically, through five years of accumulation, Waterdrop has gradually formed a technological strategy of “AI + Blockchain + Data = Construction,” empowering the insurance and healthcare industries with technology to achieve online integration, streamlined processes, data-driven operations, and intelligent solutions.

According to the introduction, Shuidi Inc. establishes its big data foundation by accessing third-party data and collecting online and offline data related to Shuidichou (Shuidi Crowdfunding) and Shuidibao (Shuidi Insurance). This involves extracting, de-identifying, cleaning, and integrating the accessed data. Empowered by Shuidi’s AI capabilities—including Natural Language Processing (NLP), Optical Character Recognition (OCR), recommendation algorithms, and identity verification and authentication—the company ultimately delivers solutions for intelligent insurance, intelligent customer service, intelligent healthcare, risk control, and marketing strategies.

Of course, beyond technology, the pathway built by UnitedHealth primarily consists of two components: insurance coverage and health services. Although Waterdrop Inc. follows a similar model, it currently holds a leading position only in insurance coverage, while its health services segment is still in its early stages. It is important to recognize that medical and health services represent the true “deep-water zone” of the broader healthcare industry.

From this perspective, the IPO is not the end goal for Waterdrop Inc., but rather the starting point for its deep dive into the complex waters of the broader health and wellness sector. What does the future hold? Only time will tell.