Domestic Innovators Surge in Disposable Endoscopy: Can China Accelerate Import Substitution and Compete with Global Giants?

Endoscope: a diagnostic instrument capable of directly accessing the body’s natural lumens, providing physicians with comprehensive diagnostic information for disease treatment.

However, traditional endoscopes have complex structures that are difficult to clean and sterilize thoroughly. The reuse of the same endoscope across different patients can easily lead to cross-infection, causing severe health damage or even death to those infected.

In December 2018, Olympus was fined nearly $600 million due to infection issues associated with its duodenoscopes. Reports indicated that amid frequent infection incidents, Olympus failed to ensure adequate cleaning protocols for the endoscopes, resulting in incomplete cleaning and disinfection by healthcare facilities. Between 2012 and 2015, this led to bacterial infections in more than 190 patients.

According to relevant studies, endoscopes rank first in the risk of cross-infection among medical devices. More than 70% of endoscopes are not thoroughly cleaned, and nearly three-quarters of commonly used endoscopes are contaminated with bacteria. Consequently, the safety of endoscope use has become an unavoidable issue.

After years of exploration by endoscopy companies, single-use endoscopes have taken center stage. Their emergence has effectively addressed the issue of cross-infection, and since they are disposable, there is no wear and tear on the equipment, ensuring that each endoscope is in optimal condition upon unpacking, thereby improving surgical efficiency to some extent. Furthermore, single-use endoscopes enable hospitals to better control costs associated with endoscopic procedures, facilitating the wider adoption of endoscopic surgery in primary care hospitals.

However, whether single-use endoscopes can shine on the stage of medical devices is influenced by multiple factors, including technology and cost.

In this article, we review 11 domestic companies in the single-use endoscopy sector, detailing their product development stages and application scenarios. Additionally, we introduce several foreign enterprises to provide insight into the development landscape of single-use endoscopes.

Technological Updates Trigger Dramatic Cost Shifts, Enabling One-Time Replacement Across Multiple Fields

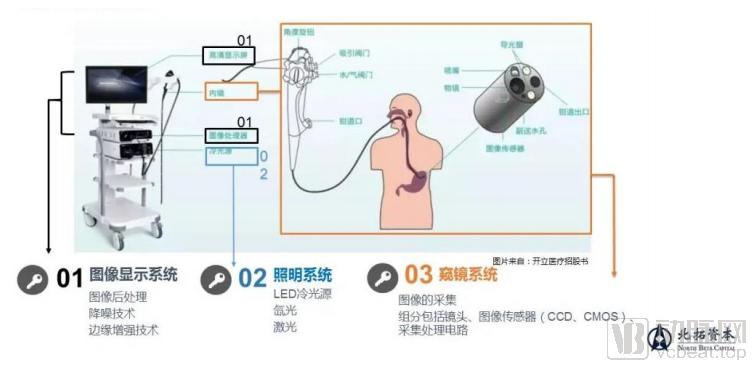

Before formally introducing single-use endoscopes, let us briefly review the structure of an endoscope. A traditional endoscope consists of three systems: an image display system, an illumination system, and an endoscopic viewing system.

Figure 1. Composition of Traditional Endoscopes

Source: Beituo Capital

Among these, the core of the endoscope system lies in image acquisition, with key components including the imaging lens, image sensor, and acquisition and processing circuitry.The transition to single-use endoscopes is closely tied to advancements in image sensor technology.

The Rise of CMOS Brings Opportunities for Single-Use Endoscopes

In the market, image sensors can be divided into two major categories: charge-coupled devices (CCD) and complementary metal-oxide-semiconductor (CMOS) sensors. In the early stages of electronic endoscope development, CCDs were widely used. However, due to the high manufacturing difficulty of CCDs and restrictions on core technologies and exports by foreign giants, CCD prices remained high. With the rise of CMOS technology, endoscope manufacturers are gradually transitioning from CCD to CMOS.

Compared with CCD, CMOS offers the advantages of lower power consumption and reduced noise. Although its image quality is slightly inferior, it is steadily closing the gap with CCD. More importantly, the CMOS market is fragmented with relatively low technical barriers, enabling domestic manufacturers to independently achieve industrialization.Currently, the declining price trend of CMOS sensors presents opportunities for single-use endoscopes.

Furthermore, endoscopes possess the dual attributes of both medical devices and consumables.The main unit is durable and not easily damaged, but the lifespan of the endoscope insertion tube varies from six months to ten years. When single-use becomes the norm and reusability is no longer pursued for endoscopes, the design and materials of the insertion tube will trend toward simplification, and cost control will be further optimized.

Applicable Across Multiple Fields, the Single-Use Endoscope Market Is Substantial

The possibility of large-scale, low-cost production brought about by technological advancements has qualified disposable endoscopes for market entry. So, where is the market? This is another critical question for disposable endoscopes to complete their “performance,” and also an important consideration for companies entering the field.

Considering factors such as the acquisition cost, service life, turnover frequency, difficulty of disinfection, and maintenance costs of endoscopes,Disposable endoscopes are more cost-effective than traditional reusable endoscopes in multiple fields.

For hospitals, costs are more controllable.Taking flexible ureteroscopic surgery as an example, from the perspective of equipment procurement costs for hospitals, purchasing two imported flexible ureteroscopes and one main unit costs approximately RMB 2 million. In contrast, procuring multiple Chinese-made disposable flexible ureteroscopes along with one main unit can keep the cost under RMB 100,000. On a per-procedure basis, the cost of traditional reusable endoscopes (including reprocessing, maintenance, etc.) exceeds RMB 12,000, whereas the hospital procurement price for disposable flexible ureteroscopes is generally below RMB 10,000.

For patients,Compared with traditional endoscopes, single-use endoscopes currently incur higher costs. However, they offer a safer examination experience by preventing cross-infection. Nevertheless, as consumption levels rise in China and the trend toward treating endoscopes as disposable consumables strengthens, the competitiveness of single-use endoscopes will gradually increase.

According to statistics, the endoscope types most suitable for single-use applications mainly include cholangiopancreatoscopes, gastrointestinal endoscopes, cystoscopes, bronchoscopes, nasopharyngolaryngoscopes, and hysteroscopes, covering multiple clinical departments such as gastroenterology, urology, pulmonology, and gynecology. These endoscope types correspond to a potential diagnostic and therapeutic volume of nearly 70 million cases in China.This is a vast blue ocean market.

Five Companies Approved by NMPA, with Application Scenarios Focused on Urology

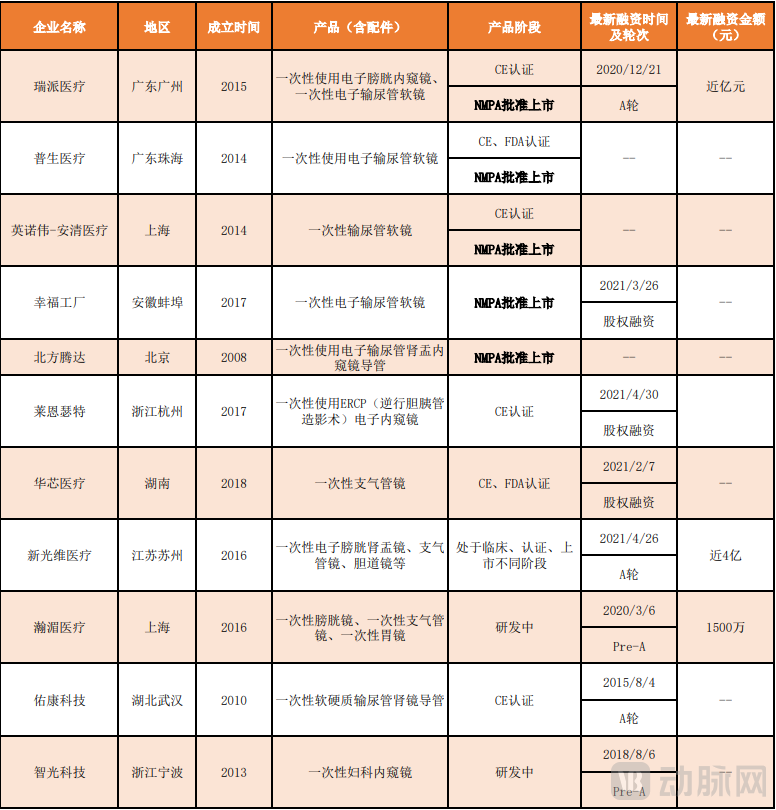

Several companies have already set sail in this blue ocean. According to incomplete statistics, this article has compiled a list of 11 domestic enterprises engaged in the research, development, and manufacturing of single-use endoscopes, as shown in the figure below:

Figure 2-11 List of Domestic Disposable Endoscope Companies

Source: Compiled from public data

From the perspective of the R&D phase of disposable endoscope products, most companies have already launched their first products to the market, but overall, they are still in the early stages of market development.

To date, five companies in China have obtained six registration certificates from the National Medical Products Administration (NMPA), namely Ruipai Medical, Pusheng Medical, InnovaMed (subsidiary: Anqing Medical), Xingfu Factory, and Beifang Tengda. Among them, Ruipai Medical has received two approvals for its single-use electronic cystoscope and single-use flexible electronic ureteroscope.

Furthermore, 6 out of the 11 companies have obtained CE or FDA certification. More than half of the products have gained regulatory approval for market release, demonstrating that the research and development of disposable endoscopes has achieved initial success.

However, products that have obtained approval and certification are limited to a single type of endoscope. Taking disposable endoscopes that have received NMPA registration certificates as an example, six of them are concentrated in urology, with five belonging to disposable flexible ureteroscopes. Additionally, their approval dates are clustered around 2020, and the market performance has not yet been fully reflected. Therefore, overall, disposable endoscopes are just emerging and remain in the early stages of development.

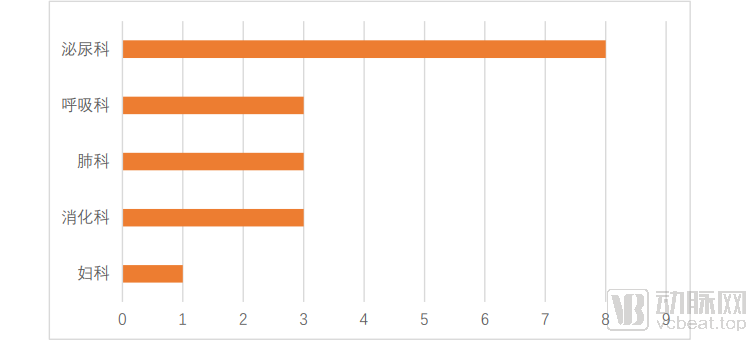

From the perspective of usage scenarios for disposable endoscopes, there is a clear bias.Among them, urology had the highest number, followed by respiratory medicine, gastroenterology, and pulmonology.See the figure below for details.

Figure 3 - Distribution of Usage Scenarios for Disposable Endoscope Products from 11 Domestic Companies

Among the aforementioned 11 companies, eight have focused their research and development efforts on disposable endoscopes for urology, including disposable flexible electronic ureteroscopes, disposable electronic cystoscopes, and disposable electronic ureteropyeloscopes. All products approved by the National Medical Products Administration (NMPA) also fall within the urology segment. Why does urology account for such a dominant market share?

According to Chen Xingwang, CEO of Hanmei Medical, on the one hand, the urinary system is a sterile environment, and the costs associated with cleaning, disinfection, and sterilization of equipment required to maintain sterility for urological instruments are extremely high. On the other hand, under China’s current medical insurance reimbursement system, flexible electronic cystoscopy commands relatively high fees, thereby providing greater pricing flexibility for single-use endoscope products entering the market.

Overall, differences in the technical feasibility and future market potential of single-use endoscopes across various clinical departments have led to significant variations in product distribution.For example, gastroscopy in the Department of Gastroenterology.

In terms of performance, gastroscopes place certain demands on the imaging quality and flexibility of the equipment. Cost control is relatively favorable, with lower maintenance and disinfection expenses; additionally, reimbursement rates under medical insurance are not high. Therefore, while complete one-time replacement in the short term is challenging, partial substitution holds considerable promise. On one hand, there is substantial demand for gastroscopy, and its technological pathway is relatively mature; on the other hand, the risk of cross-infection during surgical diagnosis and treatment is significant.

Furthermore, surgical procedures tend to cause wear and tear on endoscopes. Since the diagnostic system of the endoscope is in close proximity to the therapeutic devices, vibrations generated during treatment inevitably result in a certain degree of natural wear. If the operating distance is too close, the likelihood of lens damage increases significantly. Repeated reprocessing and disinfection after surgeries also lead to a decline in endoscope performance. These factors collectively increase hospital maintenance costs, making the gastroenterology department a key market for disposable endoscope products.

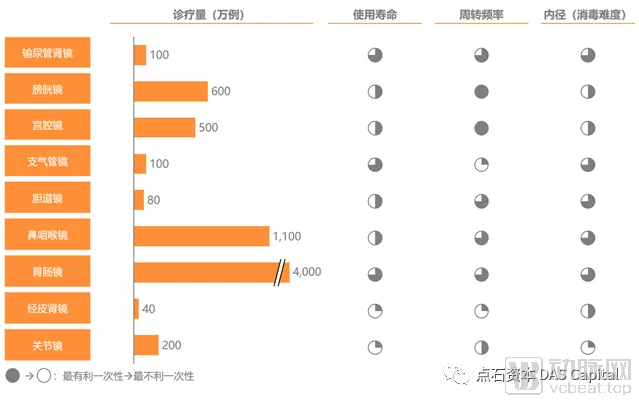

Due to the impact of the COVID-19 pandemic, the Department of Respiratory Medicine is currently driving significant market demand for disposable bronchoscopes. Market forecasts for other types of disposable endoscopes are shown in the figure below.

Figure 4 - Market Opportunity Estimation for Disposable Endoscopes

Source: DAS Capital

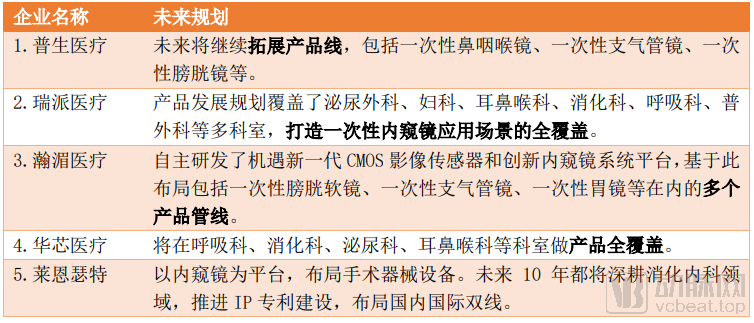

Although disposable endoscope products in China are currently mainly concentrated in ureteroscopes and cystoscopes.ButFrom the perspective of future corporate strategy, most companies are not limited to a single product or specific use case; instead, they are pursuing diversified layouts that span across multiple clinical departments.The future strategic layout of certain companies is shown in the figure below.

Figure 5. Future Development Directions of Some Domestic Disposable Endoscope Companies

Companies such as Pusheng Medical, Ruipai Medical, and Huaxin Medical aim to achieve comprehensive coverage of the single-use endoscope product portfolio in the future. It is foreseeable that once their first product’s business model proves viable in the market, a sweeping “single-use revolution” in endoscopy will swiftly follow.

However, in addition to diversified layouts, some companies choose to focus on a specific field. For instance, Lainsert will dedicate itself to gastroenterology over the next decade. Lainsert states that the ultimate goal of single-use endoscopes is not merely to reduce costs and prevent cross-infection, but to leverage the functional value of the products to address the pain points and challenges faced by clinicians. Currently, the company is developing its second- and third-generation products, aiming to create multiple surgical solutions for gastroenterology centered around its endoscopy platform.

Concentrated in the Eastern Region, Financing Just Kicks Off

We continue to focus on enterprises, examining their characteristics through the lenses of founding date, geographic distribution, and financing rounds.

First, in terms of establishment time and geographic distribution, the 11 companies were founded between 2008 and 2018, with the majority concentrated in the eastern region.The establishment of companies was relatively concentrated over the four-year period from 2014 to 2017, with a total of seven companies founded: Pusheng Medical, Innovawe-Anqing Medical, Ruipai Medical, Xinguangwei Medical, Hanmei Medical, and Lancesert.

Regional Distribution Characteristics: Given the imbalance in the distribution of medical resources across different regions in China, the eastern region holds greater advantages in the research, development, and application of new technologies such as single-use endoscopes.

Secondly, in terms of financing rounds, most enterprises have completed their initial funding but remain in the stage of capital evaluation.。Of the 11 companies, eight are known to have completed relevant financing rounds: two have closed Series A financing, three have completed Pre-A financing, and three have secured equity financing.

The current state of corporate financing, which is largely in its early stages, roughly corresponds to the development trajectory of single-use endoscopes: while products have been launched and are undergoing market fit assessment, the extent to which they meet specific market demands and their product value still require further validation.

Among them, New Guangwei Medical completed a Series A financing round of nearly RMB 400 million in April this year. This is one of the largest funding projects in the domestic endoscopy field in recent years, jointly led by Hillhouse Ventures and Lilly Asia Ventures.

Xinguangwei Medical is a company focused on the research and development of image processing and innovation in endoscopic technology. Its products hold unique advantages in cutting-edge endoscopic technologies and productization directions, such as ultra-high-definition imaging, 3D imaging, and the disposabilization of endoscopic consumables (single-use technology). It is reported that multiple single-use electronic endoscope products under Xinguangwei Medical have entered clinical use, registration, or sales stages in China, the United States, Europe, and other countries and regions, demonstrating certain international competitiveness.

In December 2020, Ruipai Medical completed a Series A financing round of nearly RMB 100 million to strengthen and expand its product R&D pipeline, accelerate the deployment of automated production lines, and increase investment in brand marketing. In July and August 2020, Ruipai Medical obtained Class III medical device registration certificates for two products, becoming the manufacturer with the largest number of domestic Class III registration certificates for single-use endoscopes. Its independently developed single-use electronic cystoscope is also competitive on a global scale.

Foreign Endoscopy Giants Enter the Market with Mature Products

As the trend of treating endoscopes as disposable consumables has become increasingly apparent in recent years, many international companies have begun to strategically position themselves in the single-use endoscope market. According to Boston Scientific’s projections, the global market size for single-use endoscopes will reach $2 billion in 2024.

While major Chinese endoscope manufacturers have been slow to deploy in the disposable endoscope market, several international giants—such as Olympus, Pentax, and Boston Scientific—have already entered the field and developed mature products.

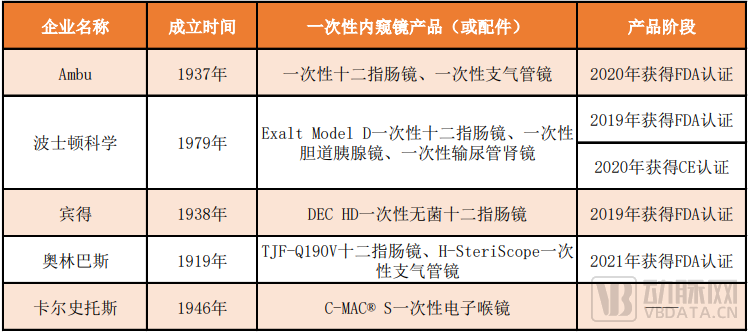

This article briefly lists some foreign disposable endoscope products and companies.As shown in the figure below.

Figure 6. Some Overseas Manufacturers of Disposable Endoscopes

Source: Compiled from public information

In terms of application scenarios, the products are concentrated in gastroenterology, pulmonology, and urology, which is broadly consistent with the distribution focus of domestic single-use endoscopes. However, there are differences upon closer examination: overseas markets place greater emphasis on gastroenterology, while the domestic market leans more heavily toward urology.

These companies have decades of experience in the research, development, and manufacturing of endoscopes. Currently, most single-use endoscopes are designed and manufactured based on the architecture of traditional reusable endoscopes. Therefore, the maturity of conventional endoscope technology significantly facilitates the development of single-use endoscopes.

Notably, Boston Scientific entered the endoscopy field as early as 1981. Its strategy for disposable endoscopes began with urological and gastrointestinal endoscopy, the areas most closely aligned with its core business, culminating in the launch of LithoVue, the world’s first single-use ureteroscope. Currently, its product portfolio has expanded to include duodenoscopes, bronchoscopes, gastrosopes, and cholangioscopes.

Ambu’s sales of single-use endoscopes have surpassed one million units. Since 2001, the company has gradually shifted its production lines to Malaysia and China, while placing greater emphasis on the development of single-use devices. In 2009, Ambu launched aScope, the world’s first single-use bronchoscope. Starting with bronchoscopes, Ambu is progressively establishing a comprehensive portfolio of single-use endoscopic products, with plans to introduce additional offerings such as single-use colonoscopes and single-use gastroscopes in the future.

Poised for Action: The Grand Drama of “Consumable-ization” Is About to Begin

China's Endoscopy Sector: A "Lowland" for Domestic Substitution, China’s endoscopy market, valued at over RMB 25 billion, is dominated by Japanese companies (Olympus, Fujifilm, and Pentax) and European and American firms (Karl Storz, Stryker, and Wolf). Leveraging their technological advantages, these players have rapidly established patent barriers and industry standards, leaving domestic companies struggling to catch up. Chinese-made endoscope brands hold a low market share and primarily serve the mid-to-low-end segments; achieving import substitution remains a long and arduous journey.

China has introduced a series of policies to encourage innovation in medical devices and support and promote the substitution of domestically produced products. In the field of single-use endoscopes, Beifang Tengda’s single-use electronic ureterorenoscope catheter passed the special review for innovative medical devices in 2017, entered the green approval channel, and has obtained NMPA registration certification this year.

According to industry analysis, the trend toward disposable endoscopic consumables may accelerate the domestic substitution of endoscopes.Currently, domestic companies have secured a foothold in the field of single-use endoscopes and possess considerable international competitiveness.

However, the development of single-use endoscopes has not been smooth sailing. To enhance product competitiveness, it is essential to effectively address the challenges of cost control and product performance.

First, while it is undeniable that single-use endoscopes will impact the cost control of traditional reusable endoscopes, their current costs remain relatively high and mass production levels are low, resulting in no significant price advantage. However, with further technological advancements and material upgrades in single-use endoscopes, low-cost mass production can be achieved.

Second, in terms of performance, single-use endoscopes are slightly inferior to reusable endoscopes and still need to catch up. Therefore, the competitiveness of single-use endoscopes remains to be strengthened.

As the saying goes, “one minute on stage takes ten years of practice off stage.” Amid the opportunity presented by the “disposable-ization” of endoscopes, single-use endoscopes are gathering momentum, poised for a spectacular showcase.

References:

[1] Zheng Yexin. Industry Research: A Glimpse into the Development Trends of China’s Endoscopy Industry. Beituo Capital. 2020-11-03.

[2] Dun Yuting. Disposable Endoscopes Poised for Takeoff: Hanmei Medical Secures RMB 15 Million in Pre-A Financing. 36Kr. 2020-03-06.

[3] Jie Fan She. The trend of “consumable-ization” in medical endoscopes has emerged, with domestic manufacturers overtaking on the bend. DAS Capital. 2021-01-15.

[4] Endoscopes: Forging Ahead Amid the Wave of Domestic Substitution. Guoyuan Securities. 2020-12-15.