Opportunities in the Accelerating Integration and Vertical Specialization of China's Aesthetic Medicine Industry: The Rise of Light Aesthetic Chains

Author: Liu Tengfei, Founder & CEO of Fanxing Light Medical Aesthetics

Since the Spring Festival of 2020, the topic of “non-surgical aesthetic medicine” has remained highly popular, and recent discussions about it among media outlets, the investment community, and the medical aesthetics industry have intensified once again.

"Light Medical Aesthetics" is a specialized category of medical aesthetic treatments that bridges the gap between surgical plastic surgery and daily life beauty care. It refers to the use of non-invasive or minimally invasive medical therapies, advanced products, and devices to meet patients' aesthetic demands. Compared with traditional plastic surgery, light medical aesthetics features less invasive procedures, more flexible operational methods, and characteristics such as simplicity, convenience, and safety. Also known as "lunchtime beauty" in Japan and South Korea, it has gradually gained popularity in the Chinese market since 2015.

As an entrepreneur who entered the light medical aesthetics sector several years ago, I have recently sensed considerable curiosity and questions about this emerging niche during conversations with fellow founders and investors. I have taken the time to compile these queries as a means of exchange and sharing with friends who are interested in the light medical aesthetics field.

The explosive or rapid growth of an industry is invariably driven by structural changes across its entire ecosystem. We will analyze the reasons behind the surge in popularity of non-surgical medical aesthetics from four dimensions: consumer demographics, consumer demand, public opinion landscape, and upstream supply.

Dimension 1: Consumer Population

The demographic with the strongest demand for non-surgical medical aesthetics is women aged 20–40, born between 1980 and 2000. According to public data released by iiMedia Research, the number of non-surgical medical aesthetics users in China reached 15.2 million in 2020, continuing to grow at a compound annual growth rate exceeding 50%.

As the post-85, post-90, and post-95 generations—raised with material security and immersed in Korean dramas—have become the main force in the consumer market, medical aesthetic services have shifted from “affordable luxuries” to “fast-moving consumer goods,” with medical aesthetic consumption evolving from a “niche market” to a “mass market.”

Dimension 2: Changes in Demand

In the nearly 3–5 years after 2017, consumer demand for medical aesthetics became more diversified, with the consumer side beginning to distinguish between “plastic surgery” and “medical aesthetics.”

Mild aesthetic medicine demands for improving skin condition, such as anti-aging, whitening and rejuvenation, and subtle adjustments, are now clearly distinguished from plastic surgery procedures aimed at altering facial features, such as double eyelid surgery and rhinoplasty. At present, when consumers refer to “undergoing aesthetic treatments,” they no longer include surgical interventions, but rather refer to the purchase and reception of non-surgical, minimally invasive aesthetic services.

Dimension 3: Public Opinion Environment

Compared with “plastic surgery,” public opinion toward “medical aesthetics” has become increasingly tolerant in recent years, with some variety shows and mainstream celebrities beginning to endorse medical aesthetic products and platforms.

Discussions and perceptions of medical aesthetics on mainstream social media platforms such as Xiaohongshu, Zhihu, and Weibo have become more rational and normalized. For today’s young consumer demographic, undergoing aesthetic medical procedures is a routine consumption behavior that no longer carries stigma.

Dimension 4: Upstream Supply in the Industrial Chain

In the past five years, the number of new mesotherapy products, hyaluronic acid fillers, botulinum toxin injections, and other pharmaceuticals that have received NMPA registration certificates and been launched on the market has exceeded the total from the previous 30 years. This is undoubtedly good news for consumers of non-surgical medical aesthetics; intensifying competition among upstream manufacturers means an expanding array of product choices for consumers and increasingly reasonable pricing.

For downstream light medical aesthetic institutions, the more concentrated the upstream supply chain is, the lower the value of the downstream players; conversely, the more fragmented the upstream is, the greater the value of downstream chains.

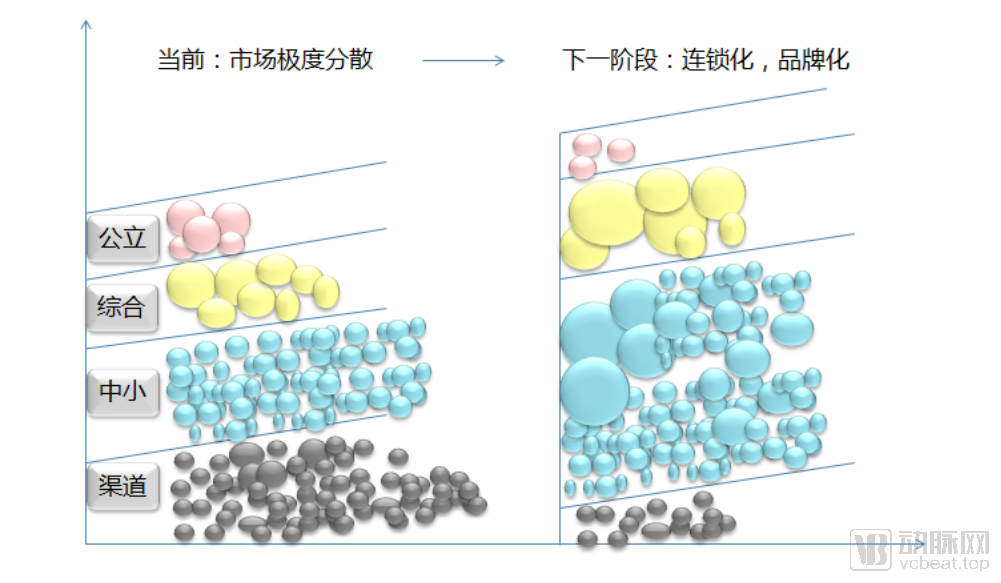

After nearly three decades of unregulated growth in China, the medical aesthetics industry currently faces a series of challenges, including low levels of chain consolidation, insufficient supply of high-quality services, a significant market share held by illegal clinics, and uneven professional competence among practitioners.

How Low Is the Chain Affiliation Rate in Medical Aesthetics? Here’s a Set of Data for Your Reference: As of 2020, there were approximately 15,000 legally operating and licensed medical aesthetic institutions in China. How many of them could truly be considered chain organizations? No more than 300, accounting for less than 2%.

On one hand, this indicates that there is still a long way to go in achieving standardized and chain-based operations; on the other hand, it highlights that the downstream medical aesthetics institutions will have substantial room and opportunities for further consolidation over the next 5–10 years.

The medical aesthetic institutions currently on the market are broadly composed of the following categories:

Public Hospital Departments of Medical Aesthetics and Plastic Surgery (represented by Shanghai Ninth People’s Hospital, Beijing Ba Da Chu Plastic Surgery Hospital, and Xijing Hospital of the Fourth Military Medical University)

Comprehensive plastic surgery hospitals generally have a floor area of over 5,000 square meters (representative brands include Mylike, Yestar, Milan Baiyu, and Huahan).

Small to Medium-Sized Medical Aesthetic Clinics (500–2,000 sqm)

Channel-based medical aesthetics (primarily relying on high rebates to target the B2B market for beauty salons; not covered in this article)

Forecast of the Future Market Structure of Medical Aesthetics

The primary battleground for consumer healthcare has never been within public hospitals. As the aesthetic medicine market continues to heat up, the plastic surgery and dermatology departments of public hospitals will gradually withdraw from competition in the consumer (C-end) market, instead assuming roles that support industry development, such as providing technical empowerment and training. In recent years, a large number of skilled plastic surgeons have left the public system to launch their own practices, further distancing public hospitals from consumers.

Comprehensive plastic surgery hospitals with a floor area of over 5,000 square meters will undergo accelerated consolidation against the backdrop of continuous growth in the medical aesthetics market. In the future, the market can support the coexistence of 8–10 large- and medium-sized chain brands, with leading chain brands demonstrating an accelerating trend of consolidation.

Among them, the most numerous small and medium-sized institutions will become the main battleground for transformation in the medical aesthetics industry. The following three types of positioned institutions will be the ultimate beneficiaries of this round of transformation.

The first category comprises physician-founded startups.Such medical aesthetic institutions are characterized by high customer loyalty and healthy profit margins. However, they rely excessively on physicians’ reputations, making it difficult for physician-founders to achieve scalability due to constraints in both time allocation and management experience.

The second category is vertically positioned chain institutions,For instance, chains specializing in fat-related procedures, chains focusing on blepharoplasty for under-eye bags, and so forth;

The third category is maintenance-oriented light medical aesthetics chains,The advantages include a highly standardized service process, low reliance on physicians’ technical skills, high frequency and high price points, strong replicability, and substantial benefits from economies of scale. However, the drawbacks are also relatively apparent: products are prone to homogenization, necessitating greater innovation in product offerings and service experiences; the chain-business model demands a large pool of managerial talent, requiring significant time and financial investment in the early stages to establish a talent development system, among other things.

The future market can support 5–8 light medical aesthetics chain brands with over 100 outlets each, while the number of leading chain brands is expected to exceed 300.

Based on the above analysis, we can conclude that chain-operated light medical aesthetics is a business format that is growing and expanding in line with industry trends. This prompts us to delve deeper into what kind of light medical aesthetics business model is more efficient and competitive.

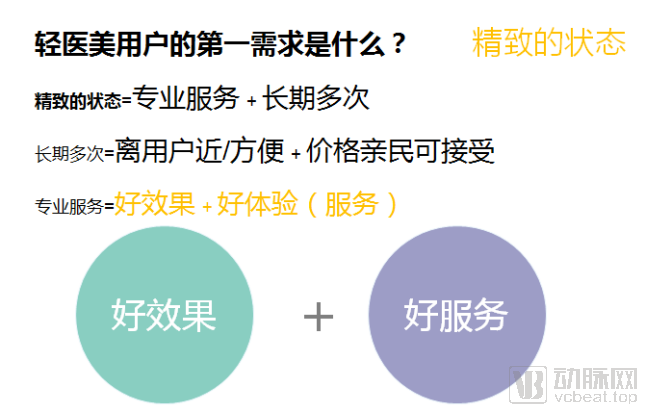

First,Put yourself in the consumer's shoes:What Is the Primary Need of Light Medical Aesthetics Consumers?

I believe it is a “refined state,” where one achieves a more polished appearance and a more youthful look through minimally invasive aesthetic medicine products and procedures. If we further break down this “refined state,” it equates to “professional services” plus “long-term, repeated treatments.”

“Professional Services” = Good Outcomes + Quality Service

“Long-term, frequent use” = Proximity/convenience + High cost-effectiveness

Based on such an analysis of user needs, the business model for single-location non-surgical aesthetic clinics has gradually become clear. It is defined by several key attributes: proximity to target customers, high cost-effectiveness, guaranteed results, and a highly comfortable service experience.

Consumer healthcare is inherently suited to a “small and beautiful” model, as users’ personalized demands require more rapid responses, and they are more willing to pay a premium for superior service experiences.

Therefore, the optimal size for minimally invasive aesthetic clinics is 300–500 square meters, with each location spaced 3–5 kilometers apart to achieve high-density coverage. This ensures that users can always find the nearest clinic within 30 minutes, while maintaining a unified pricing system and standardized service processes and experiences.

Primary Needs of Light Medical Aesthetics Users

The above content represents a reverse-engineering approach to determining the optimal store model, derived from the perspective of user needs.

Second, how should the most efficient organizational structure for a chain business model be established?

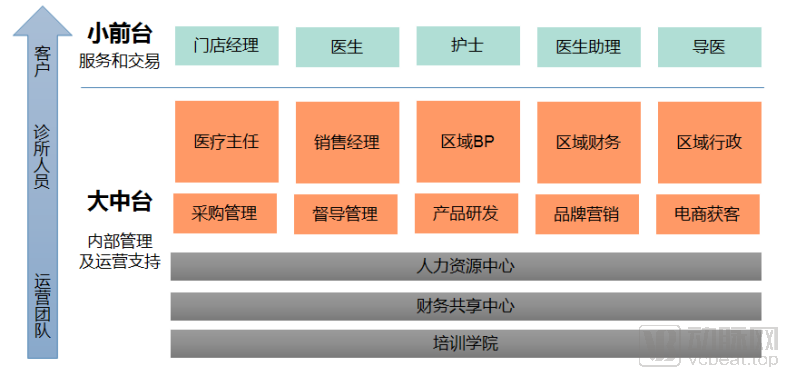

Unlike traditional medical aesthetics institutions, small yet refined light medical aesthetics clinics are well-suited for the "large middle platform, small front-end" model.

This model has been most efficiently embodied by Xueersi, China’s most valuable education giant.

Xueersi implements decentralized and refined management of its chain campuses through a “large middle-office + small front-office” model, standardizing headquarters’ oversight of enrollment, recruitment, training, teaching research, monitoring, and technology across all campuses nationwide. As branch campuses rely heavily on headquarters’ support, this has given rise to a strong centralized management system.

Indeed, it was after 2007 that Xueersi established its teaching and research department, strengthened its middle-office infrastructure, and ultimately overtook New Oriental on the curve, emerging as the education chain giant with the highest market capitalization.

In light medical aesthetics chains, the centralized middle platform assumes functions such as regional customer acquisition, marketing, centralized procurement, training academy, human resources center, and finance center. It empowers front-end stores across multiple dimensions, while these stores, through more agile organizational structures, lower operating costs, and standardized processes, reduce reliance on physicians’ technical skills and the difficulty of standardized management.

"Large Middle Platform, Small Front-End Model"

Light medical aesthetics without the support of a robust central platform is like a carrier-based aircraft without an aircraft carrier: it can still fly, but not far.

Certainly, the downside of this model is that the initial investment required to build a middle platform is inevitably very high. Only a few small chains in the light medical aesthetics sector will face the most significant challenges, as they lack the flexibility and low-cost advantages of single stores while not yet achieving the substantial efficiency gains brought by larger-scale chain operations. They need to leverage capital to overcome the "middle-income trap." Once a chain expands to over a dozen outlets, its overall operational efficiency will significantly improve.

Third, the most pressing issue: how can light medical aesthetics chains achieve “cost reduction and efficiency enhancement”?

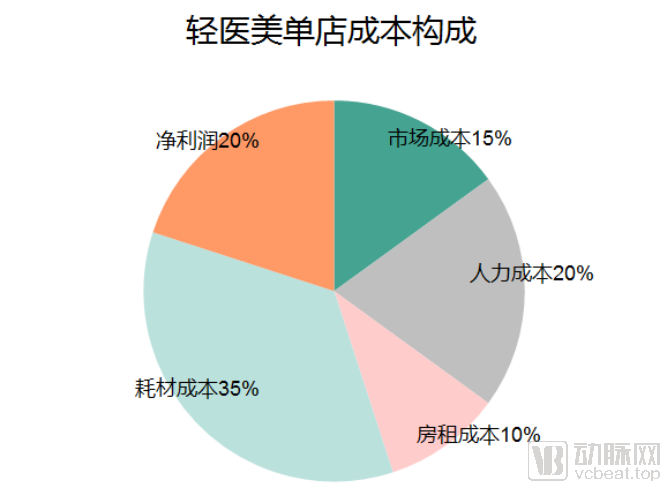

In my view, the reason why most chain medical aesthetics clinics in China exhibit the phenomenon of “being chained but not locked” is that they have ultimately failed to address the imperative of “cost reduction and efficiency improvement.”

Labor costs and marketing expenses constitute the bulk of a medical aesthetics institution’s cost structure; any chain model that fails to significantly optimize these two cost components cannot be considered a sound one.

First, consider labor costs. The most basic optimization is to share middle-office personnel. Marketing and product teams can be based in first-tier cities, while customer service centers, training centers, human resources centers, and finance centers can be located in second- and third-tier markets with lower labor costs. Meanwhile, as the number of chain stores increases, the marginal cost of middle-office labor will be continuously amortized.

Next is the training system. A robust training framework, coupled with strong middle-platform support, can significantly reduce reliance on individual capabilities and lower employee turnover. A well-developed talent pipeline and promotion incentive system ensure the efficient operation of the organization.

Light medical aesthetics chains with high-density regional coverage can first significantly enhance efficiency through the shared utilization of cross-regional member services, high-value equipment, and physician teams.

Concurrently, as regional density and exposure increase, customer trust and marketing return on investment (ROI) will further improve. (Under equal conditions, customers will definitely prioritize the provider closest to them or the one with the largest number of chain locations.)

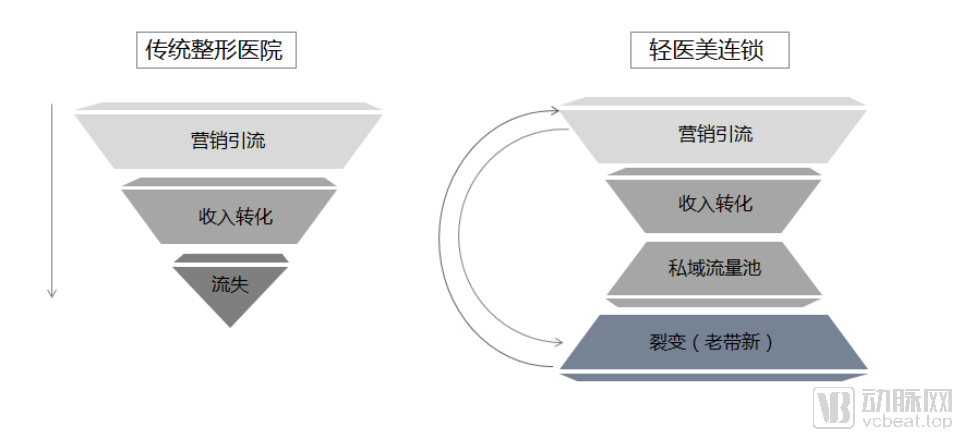

Most importantly, the non-surgical aesthetic medicine sector boasts a naturally high repurchase rate. Once a robust trust mechanism is established, strategic private-domain operations can make referrals from existing clients a core source of traffic. These referrals come with high levels of trust and conversion rates, while incurring minimal costs, thereby further balancing and reducing overall customer acquisition expenses.

Starlight Light Medical Aesthetics Private Domain Customer Cycle

Fourth, how can the model be rapidly replicated after it has been refined and matured on a small scale?

Integration of Existing Markets + Partnership Model

To achieve rapid replication and expansion, merely opening new stores one by one is certainly insufficient, even with capital support. Some insights may be drawn from Aier Eye Hospital, the leading player in the medical services industry.

As previously mentioned, the medical aesthetics industry is a highly fragmented market. A large number of small, independent clinics lack operational teams, resulting in low overall operational efficiency. These entities often struggle at the subsistence level and face the risk of bankruptcy at the slightest disturbance. After accumulating a certain scale and reputation, leveraging capital and team equity investments to consolidate the existing market, partnering with outstanding non-surgical medical aesthetics physicians, and relying on a physician-partner model can serve as an effective strategy for rapid nationwide expansion during the second phase of building a non-surgical medical aesthetics chain.

Meinian Onehealth and Aier Eye Hospital continue to maintain high-profit growth by establishing M&A funds to acquire high-quality targets nationwide, incubating them off-balance-sheet, and consolidating them into the listed companies’ financial statements once their financial performance matures.

Each model has its rationale for existence within a specific historical context. What we are discussing is, against the backdrop of growing awareness and demand for non-surgical medical aesthetics and rapid market expansion, which type of non-surgical medical aesthetics model is better suited for rapid growth.

It is evident that the penetration rate of China’s medical aesthetics market remains significantly lower than that of leading markets such as Japan, South Korea, Europe, and the United States. With per capita GDP still lagging behind that of developed nations, consumer demand for high-quality medical aesthetic services continues to grow, indicating substantial room for further expansion.

We firmly believe that the next generation of medical aesthetics brands will surely emerge in the Chinese market in the coming years.

Even the largest player in the non-surgical medical aesthetics sector currently operates only 15 clinics. The medical services industry is a marathon; the starting gun has just fired, and competitors have merely gained a few hundred meters of an early lead. Everything is just beginning.