2021 Hemodialysis Industry Research Report: Surging Demand and the Rise of Domestic Brands

I. Hemodialysis is the primary treatment modality for patients with uremia, characterized by inelastic demand and high frequency.

Considering various factors such as clinical application, therapeutic efficacy, and treatment costs across different blood purification technologies, hemodialysis remains the primary treatment modality for uremia due to its superior efficacy, broad applicability to patients at all stages of renal disease, and higher reimbursement rates. Other blood purification techniques serve as complementary options, differing in therapeutic outcomes, indications, and economic feasibility. For patients with uremia, hemodialysis is an essential and high-frequency treatment: patients typically undergo dialysis three times per week, with each session lasting approximately four hours, resulting in annual expenses of around 80,000 to 100,000 RMB.

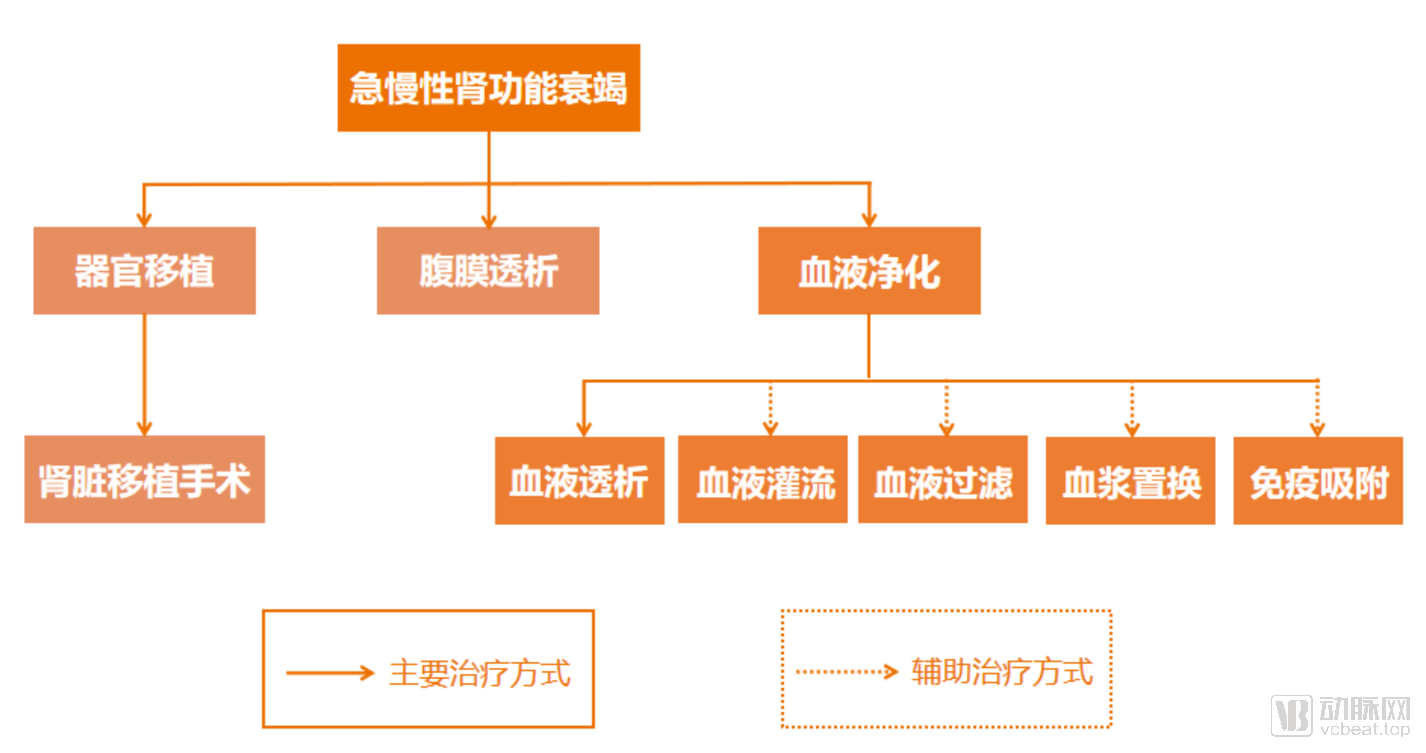

Overview of Treatment Modalities for Acute and Chronic Renal Failure

During hemodialysis, the main equipment, consumables, and medications involved are as follows:

Classification | Project |

Equipment | Dialysis Machine |

CRRT | |

Consumables | Dialyzer |

Dialysis Tubing | |

Puncture Needle | |

Dialysate | |

Drug | Anti-anemia Drugs |

Anticoagulant |

Product Definition and Classification

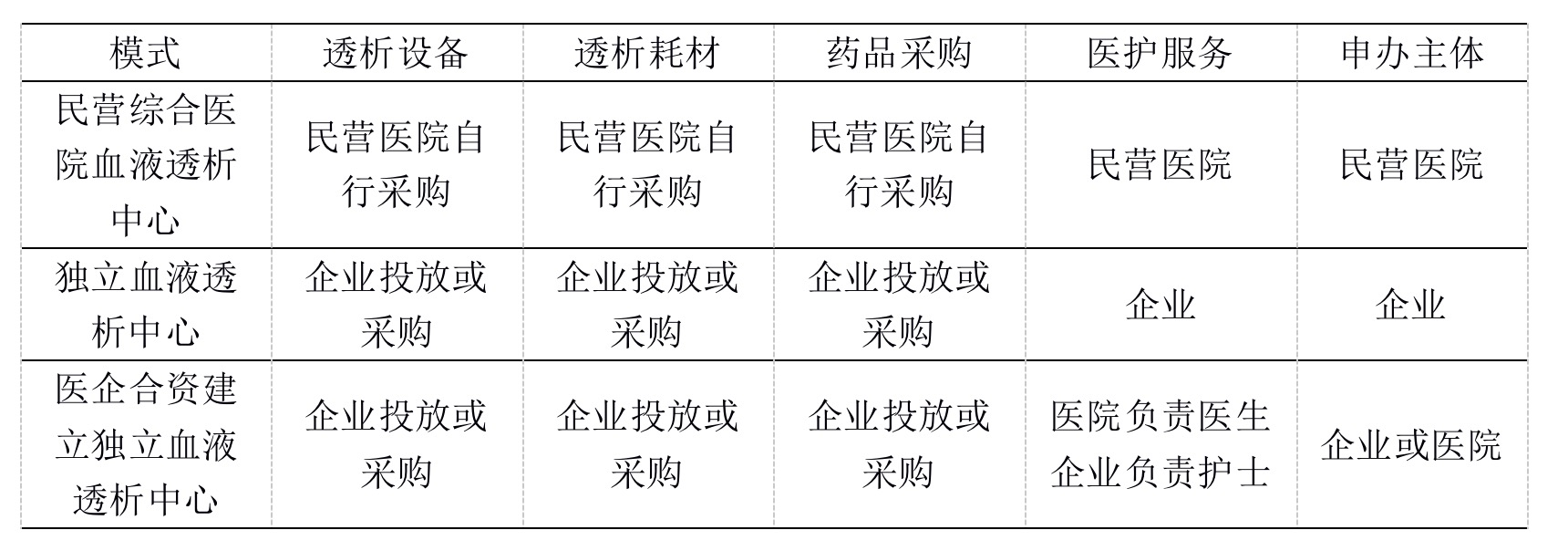

Currently, providers of hemodialysis services in China can be categorized into two major groups: public hospitals and private institutions.

Classification of Operational Models for Private Hemodialysis Centers

II. Sustained Huge Demand Continues to Drive the Development of China’s Hemodialysis Industry, with a Trillion-Yuan Market Gradually Emerging

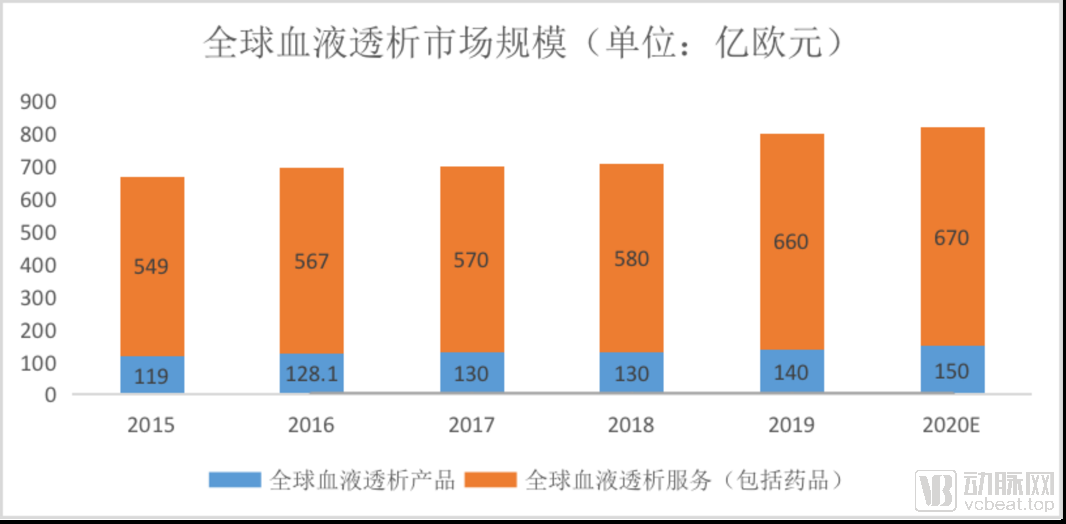

Globally, hemodialysis has remained and will continue to be the primary treatment modality for patients with chronic kidney disease. According to forecasts and statistics disclosed in Fresenius’s annual report, the global dialysis market size has steadily increased from €66.8 billion in 2015 to €82.0 billion in 2020, representing a compound annual growth rate of approximately 4%. By 2021, the dialysis market is expected to further expand to around €83–85 billion. Among this, the market share of dialysis services (including pharmaceuticals) accounts for more than 80%.

Global Hemodialysis Market Size

Source: Fresenius Annual Reports (2015–2020), compiled by VCBeat.

Accelerated Expansion of Private Hemodialysis Centers: Since 2014, the Chinese government has gradually lowered the requirements for establishing independent hemodialysis centers and encouraged social capital to enter the field. This has promoted the development of hemodialysis centers towards chain and group operations, providing a favorable policy opportunity for private capital in China to enter the hemodialysis sector.Gradual Improvement of Critical Illness Insurance Further Unleashes Patient Demand: Overall, the inclusion of uremia in critical illness insurance coverage and the continuous increase in reimbursement ratios have significantly alleviated patients' financial burden. This has encouraged more patients to choose hemodialysis treatment, thereby driving overall market growth.Support for Innovative Development of Domestic Medical Devices Enhances the Vitality of Chinese Enterprises: Since 2011, national policies have encouraged and supported the development of hemodialysis equipment and consumables. Recently, provinces such as Sichuan, Guangdong, and Zhejiang have published "lists of imported products" to strengthen the management of government procurement of imported goods. As hemodialysis machines are not included in these procurement lists, this creates opportunities for manufacturers of domestically produced hemodialysis machines.

According to data from the China National Renal Data System (CNRDS), the number of patients undergoing hemodialysis treatment was 447,000 in 2016 and reached 633,000 by the end of 2019, representing a compound annual growth rate (CAGR) of 12%. Meanwhile, the number of new patients with end-stage renal disease (ESRD) in China has also been growing rapidly; from 2016 to the end of 2019, the CAGR for new cases was approximately 21%, which is one of the key drivers fueling the future growth of China’s blood purification industry.

Moreover, the treatment rate for patients in China is less than 20%, significantly lagging behind the global average of 37% and the 75% observed in European and North American countries. As per capita income rises and health insurance coverage expands, the proportion of patients with end-stage renal disease (ESRD) receiving treatment will continue to increase, thereby further driving growth in the blood purification industry.

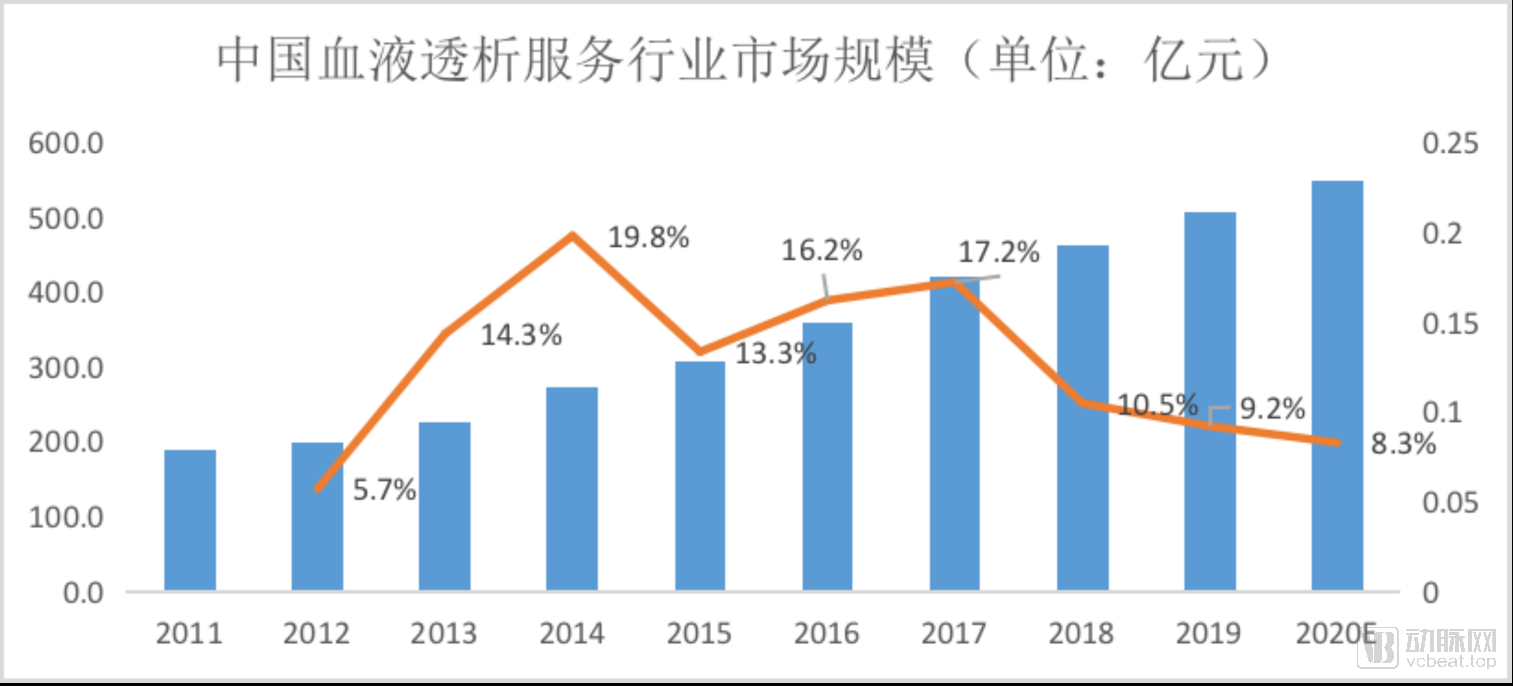

Since 2014, driven by policy support, the market size of hemodialysis services has maintained double-digit growth for consecutive years. We estimate that the total market size of hemodialysis services reached approximately RMB 54.8 billion in 2020. In the future, with the further improvement of healthcare policies such as the expansion of medical insurance coverage, increased reimbursement ratios for critical illness insurance, and tiered diagnosis and treatment, along with the innovative development and clinical application of new technologies and dialysis models, the multi-level and personalized needs of patients with end-stage renal disease (ESRD) will be effectively met. Consequently, the market size of the hemodialysis service industry will continue to grow, reaching nearly RMB 70 billion by 2025.

Market Size of China's Hemodialysis Services Industry

Source: VCBeat

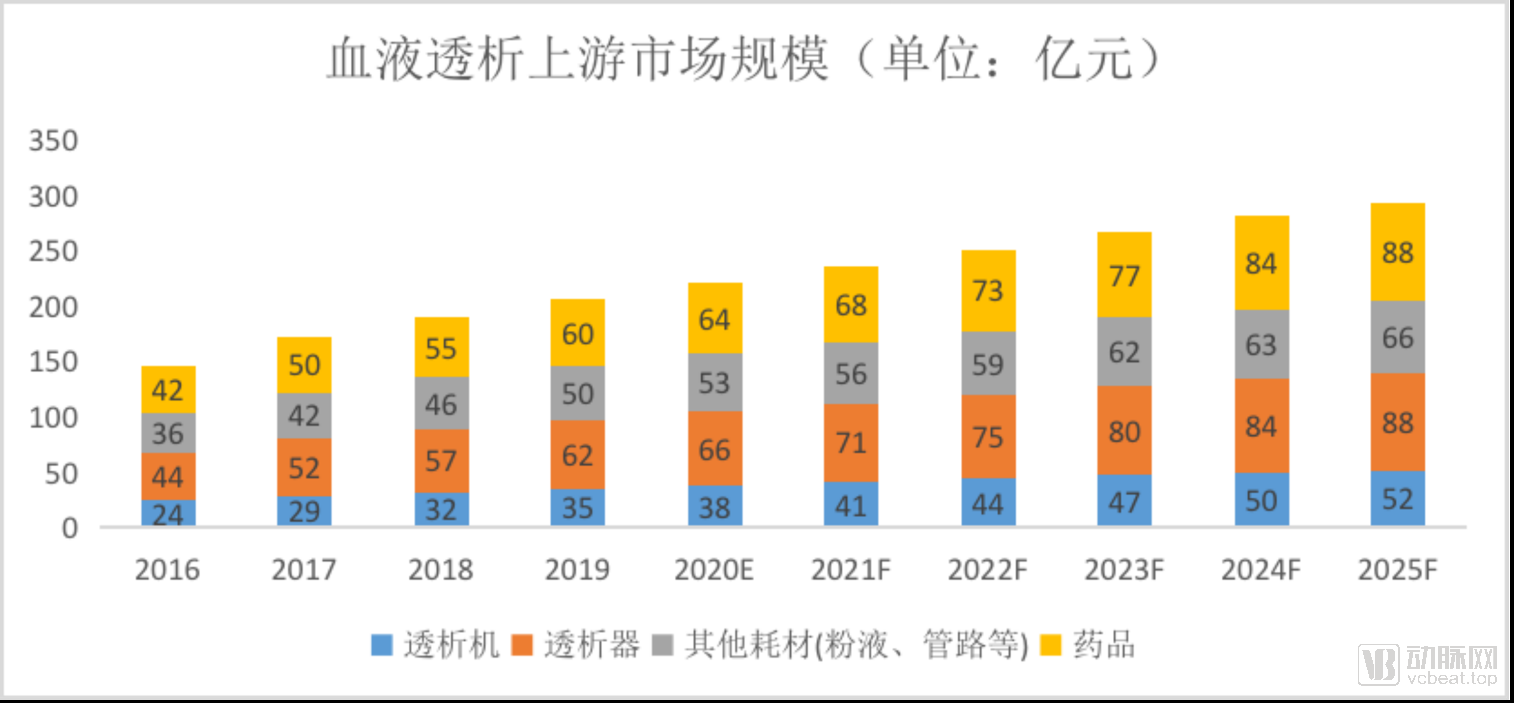

The growth of hemodialysis centers is simultaneously driving the expansion of the entire hemodialysis industry chain. According to our estimates, in 2020, the market sizes for dialysis machines, dialyzers, and pharmaceuticals were approximately RMB 3.8 billion, RMB 6.6 billion, and RMB 6.4 billion, respectively. As the market scale of hemodialysis centers expands, demand for dialysis equipment and consumables will continue to rise. We project that by 2025, the combined market size of the upstream industry chain—including dialysis equipment, pharmaceuticals, and consumables—will approach RMB 30 billion.

Market Size of the Upstream Hemodialysis Industry

Source: VCBeat

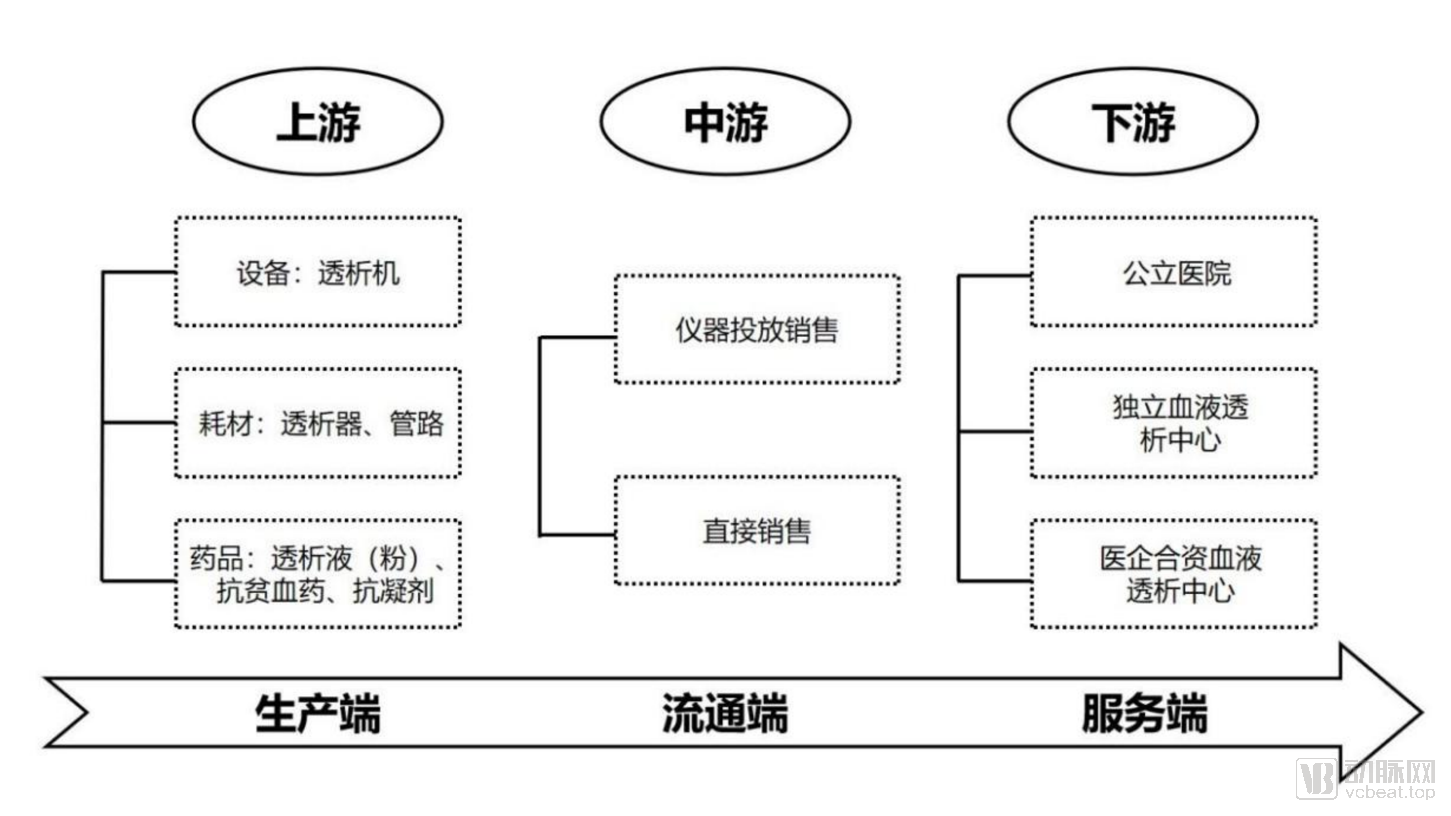

III. The industrial chain structure of the hemodialysis industry is clearly defined, encompassing upstream products, midstream distribution, and downstream services

Hemodialysis Industry Chain Structure

Upstream high-end products face significant technical barriers, and the level of domestic production remains to be improved; no leading enterprises have yet emerged in the midstream distribution sector, while upstream industry leaders show a trend toward integration; there is a substantial gap in downstream services, indicating considerable room for growth.

IV. Significant Differentiation in Competitive Landscapes Across Sub-sectors, with Domestic Brands Gradually Rising

From a global perspective, the hemodialysis market is highly concentrated. The market share is primarily held by companies such as Fresenius, Baxter (USA), B. Braun (Germany), Nikkiso (Japan), Nipro (Japan), and Toray (Japan).

14.2.1 Achieving full industry chain coverage has become the development goal of leading domestic and foreign-funded enterprises

Corporate Distribution Landscape

Data source: VCBeat

24.2.2 Overview of the Competitive Landscape in Sub-Sectors

ChinaHemodialysis MachineThe market is highly concentrated, with imported products dominating overall.

Hemodialysis Machine | Imports (80%-90%): Fresenius, Baxter (Sweden Gambro), B. Braun (Germany), Nipro (Japan), Toray (Japan), Bellco |

Domestic (10%-20%): Shandong Weigao, Chongqing Sunwisen, Guangzhou Jihua, Biolight, Chongqing Aokailong |

List of Partial Manufacturers Participating in Hemodialysis Machines

Source: VCBeat.

Bedside Hemofiltration Machine (CRRT)Continuous Renal Replacement Therapy (CRRT) is a novel blood purification technology developed on the basis of hemodialysis machines. Also known as continuous renal replacement therapy, it employs continuous extracorporeal blood purification for 24 hours or nearly 24 hours per day to replace impaired renal function. The application of CRRT has significantly improved the treatment efficiency and survival rates of critically ill patients.

Bedside Hemofiltration Machine (CRRT) | Imports: Baxter, Fresenius, B. Braun, Asahi Kasei, Nikkiso, Kawasumi |

Domestic: Chongqing Sunwowa, Jafron Biomedical |

Summary of CRRT Manufacturers

Source: Compiled by VCBeat

HemodialyzerThe market is highly concentrated, and similar to hemodialysis machines, it remains dominated by imported products.

Hemodialyzer | Imports (70%-80%): Nipro (Japan), Toray (Japan), Baxter (USA) [Gambro (Sweden)], MINNTECH, Medivators, Fresenius (Germany), B. Braun (Germany), Bellco (Italy), Hydrona (Egypt), Satas (Malaysia), etc. |

Domestic (20%-30%): Shandong Weigao, Chongqing Sunwatt, Shanxi Huading Jinquan, Shanghai Peini, Chengdu Ousai, Guangzhou Bain, Beijing Runkun Jiahua, Hangzhou Asahi Kasei, Changzhou Langsheng, Guangzhou Jihua, etc. |

List of Partial Manufacturers Participating in the Hemodialyzer Market

Source: Blue Book of China's Medical Devices 2019, compiled by VCBeat.

Hemodialysis Blood TubingThis sector is dominated primarily by domestic brands.

Hemodialysis Bloodline Tubing | Imports (50%): Fresenius (Germany), Baxter (USA) [Gambro (Sweden)], Nipro (Japan), Vita Medical, etc. |

Domestic (50%): Shandong Weigao, Chongqing Shanwaishan, Sichuan Nangeer, Shanghai Dahua, Jiangxi Sanxin, Guangzhou Bain, Zhuhai Dasheng, Ningbo Tianyi, Shenguang Medical Products, Zhangjiagang Shagong, Gambro Shanghai, etc. |

List of Manufacturers Involved in Hemodialysis Tubing Systems

Source: Blue Book of Chinese Medical Devices 2019, compiled by VCBeat.

Hemodialysis Powder and Solutionfield, basically achieving domestic substitution.

Hemodialysis Powder and Solution | Imports (10%): Fresenius (Germany), Baxter (Gambro, Sweden), Nipro (Japan), etc. |

Domestic (90%): Shandong Weigao, Biolight, Chongqing Sunwowa, Tianjin Hainuode, Jafron Biomedical, Jiangxi Sanxin, Guangzhou Jihua, Hebei Ziweishan, Taiskang, Fanmei Medical Materials, Guangzhou Kangsheng, Baiyunshan, Changzhou Huayue Microinvasive, Huanghua Sichuang, Nanjing Haibo, etc. |

List of Manufacturers Participating in the Hemodialysis Powder and Solution Segment

Source: China Medical Device Blue Book 2019, compiled by VCBeat.

Hemodialysis CenterIn terms of strategic layout, only a small number of companies have currently established hemodialysis centers. Domestic enterprises with such deployments include 3SBio, Weigao Group, Shinva Medical, and Deheng Medical.

Hemodialysis Center | Imports: Fresenius (Germany), B. Braun (Germany), DaVita, etc. |

Domestic: Chongqing Shanwaishan, Shandong Weigao, 3SBio, Xinhua Medical, Dakang Medical, Sanxin Medical, Biolight, etc. |

Summary of Vendors Participating in Hemodialysis Services

Source: Blue Book of Chinese Medical Devices 2019, compiled by VCBeat.

34.2.3 Introduction to Key Domestic Enterprises

Weigao Group was established in 1998 and is headquartered in Weihai, Shandong Province. Its subsidiary, Weigao Blood Purification Industry Group, was founded in 2004. Specializing in the field of blood purification, it was the first enterprise to achieve full industry chain coverage for products and services related to blood purification therapy. Its main products include hemodialysis machines, high-flux and low-flux polysulfone membrane dialyzers, hemofilters, dialysis tubing sets, arteriovenous fistula needles, dialysate (powder), plasma separators, and protein A immunoadsorption columns. Weigao Blood Purification Group partnered with Nikkiso Co., Ltd. to establish Weigao Nikkiso (Weihai) Dialysis Machine Co., Ltd., through which it introduced Nikkiso’s proprietary technologies and management systems. This collaboration enabled the production of world-leading hemodialysis devices such as the DBB-27C and DBB-06S, as well as other dialysis products including the DBB-07 single-patient hemodiafiltration device, the DBB-06S hemodialysis device, and the DBG-03 single-patient hemodiafiltration device. The production system has been certified under both ISO 9001 and ISO 13485 quality management standards. Currently, Weigao holds a dominant market share in China for its two major consumable product lines: dialyzers and dialysis tubing sets.

Chongqing Sunwatt Blood Purification Technology Co., Ltd. was established in 2001 and has been dedicated to the field of blood purification for over two decades. It is a company with a complete industrial chain, integrating blood purification equipment, consumables, intelligent management systems, and a chain of hemodialysis centers. The company’s main business activities are divided into three major segments: research, development, production, and sales of blood purification equipment; distribution of hemodialysis consumables; and construction of hemodialysis centers. Its products are exported to nearly 100 countries and regions, making it a leading Chinese manufacturer of hemodialysis equipment for export. In terms of innovation and R&D capabilities, the company possesses national-level technological innovation platforms, including a National Enterprise Technology Center and a National Engineering Research Center. It has successfully developed an online hemodiafiltration machine with internationally advanced standards and China’s first bedside continuous blood purification system. Regarding sales channel coverage, the company’s equipment is used in major medical institutions across China, including PLA General Hospital (301 Hospital), Qilu Hospital of Shandong University, The Second Xiangya Hospital, General Hospital of the Eastern Theater Command, General Hospital of the Central Theater Command, Xinqiao Hospital Affiliated to Army Medical University, and The First Affiliated Hospital of Chongqing Medical University. In terms of patents, the company has applied for 8 international patents and 181 national patents (including 79 invention patents), with 122 patents granted. It has also drafted 2 national standards and 5 industry standards. Meanwhile, Sunwatt will continue to strengthen product R&D and technological improvements, actively respond to national policies, develop more domestically produced hemodialysis equipment with independent intellectual property rights, and accelerate the process of import substitution.In 2020, Shanwaishan Group was designated as a key national producer of epidemic prevention supplies by the National Development and Reform Commission (NDRC), the National Health Commission (NHC), and the Ministry of Industry and Information Technology (MIIT), in recognition of the critical role its continuous renal replacement therapy (CRRT) systems played in saving critically ill COVID-19 patients during the pandemic.

Baolaite is a modern high-tech enterprise integrating the research and development, production, and sales of medical devices. Over the past three years, its sales revenue has grown at a rate of over 40%, with an increasing number of Grade A tertiary hospitals adopting Baolaite’s products and services. As the only company among A-share listed enterprises to hold a medical device registration certificate for hemodialysis machines and boasting the most complete hemodialysis industry chain, Baolaite has completed its nationwide layout in the hemodialysis sector. Currently, it has established five major industrial bases in Guangdong, Jiangxi, Liaoning, Chongqing, and Tianjin across China, marking Baolaite as a leading domestic provider of comprehensive blood purification solutions. In 2020, Baolaite’s hemodialysis-related products generated RMB 611 million in revenue, representing a year-on-year increase of 3.72% from RMB 589 million in 2019.

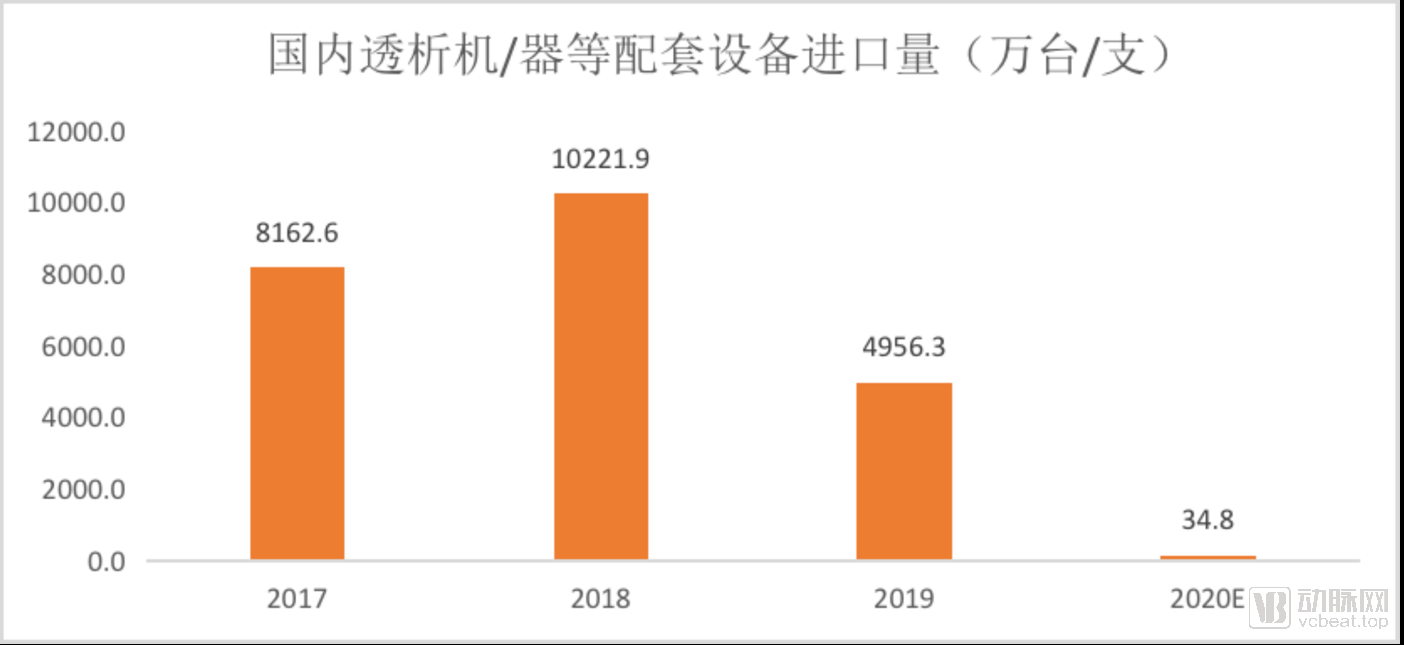

Prior to 2003, China’s dialysis equipment relied almost entirely on imports. It was not until 2003 that this exclusive dependence on imported products was broken. Recent trends have witnessed the rise of domestic brands, and we believe that the pace of import substitution will inevitably accelerate in the future.

Customs data indicate that the import volume of related equipment and consumables, primarily hemodialysis machines and dialyzers, has been on a downward trend since 2018. Notably, in 2020, imports declined significantly due to the impact of the pandemic. Furthermore, in terms of the number of enterprises, data released by the National Medical Products Administration show that, as of the report’s disclosure date, there were eight manufacturers each with registration certificates for hemodialyzers and hemodialysis machines, representing an increase from 2016 levels for both categories.

Domestic Imports of Dialysis Machines and Associated Equipment

Data Source: General Administration of Customs

V. Enhancing product technology and achieving full industry chain coverage are the major development trends for players in China’s hemodialysis industry

Advances in hemodialysis modalities offer hope for improving clinical outcomes in blood purification and uremia treatment. The incremental hemodialysis model has regained attention, enabling patients undergoing long-term conventional hemodialysis—who are at risk of accelerated decline in residual kidney function (RKF)—to mitigate these potential health risks and avoid unnecessary healthcare expenditures.

The evolution of products in the hemodialysis industry relies on continuous innovation in dialysis membranes. Traditional dialysis machines purify blood based on polymer membranes; however, conventional high-molecular-weight hemodialysis (HD) membranes have limited clearance capacity for medium- and large-molecular-weight substances, resulting in limitations such as high overall costs and poor patient prognosis. To overcome these inherent limitations, innovation in dialysis membranes is essential. In recent years, graphene oxide membranes, mixed matrix membranes, and medium cut-off (MCO) dialysis membranes have emerged as potential next-generation membrane materials.

Simplifying hemodialysis treatment processes and enhancing device portability are also key directions for innovation in hemodialysis products. Improving the portability of hemodialysis devices enables patients to undergo treatment in various settings, including hospitals, dialysis centers, homes, and communities, thereby facilitating care and improving their quality of life. With continuous innovation in hemodialysis technology, home-based dialysis devices are gradually being deployed and adopted, while wearable and implantable artificial kidneys are on the horizon.

Insufficient Supply of Hemodialysis Services in China Drives Strong Demand for Third-Party Independent Providers. Fueled by the growing treatment needs of hemodialysis patients, there is a severe shortage of hemodialysis services across China. Given the high dependence of these services on hemodialysis equipment, manufacturers possess a natural advantage in entering the service market. Consequently, domestic companies such as Shandong Weigao, Chongqing Shanwaishan, and Zhuhai Biolight have proactively established their presence in the hemodialysis service sector. Upstream hemodialysis equipment manufacturers hold developmental advantages, and it is likely that more upstream enterprises will expand into the downstream hemodialysis service industry in the future.

The above is an excerpt from the “2021 Hemodialysis Industry Report: Surging Demand and the Rise of Domestic Brands.” Scan the mini-program code below to access the full report.

If you wish to connect with companies featured by VCBeat, please complete the form, and our staff will assist you as soon as possible.

Note: All corporate data cited in this article were provided and verified by the interviewees to the analysts. If you have resources to share or wish to connect regarding reported projects, please click the link to submit your basic information, and we will contact you as soon as possible.