China's First Biopharma Industrial Park REIT Successfully Issued, Marking a New Growth Engine for the Sector

On May 18, with Suzhou Industrial Park Bio-Industry Development Co., Ltd. (hereinafter referred to as the “Bio-Company”) as the original equity holder,“Zhonglian Yuanlian–Qianhai Open Source–Suzhou Biomedical Industrial Park Asset-Backed Special Program”Officially launched, it will further deepen and advance the development of Suzhou BioBAY’s biopharmaceutical industry.

It is understood that the products issued this timeWith a total size of RMB 2.65 billion, including RMB 1.855 billion in senior tranches and RMB 795 million in subordinated tranches, the facility has a tenor of five years. The senior tranche was rated AAAsf by China Chengxin International Credit Rating Co., Ltd., with a fixed coupon rate of 4.28%. This marks the first biopharmaceutical industrial park quasi-REITs issuance completed in China.

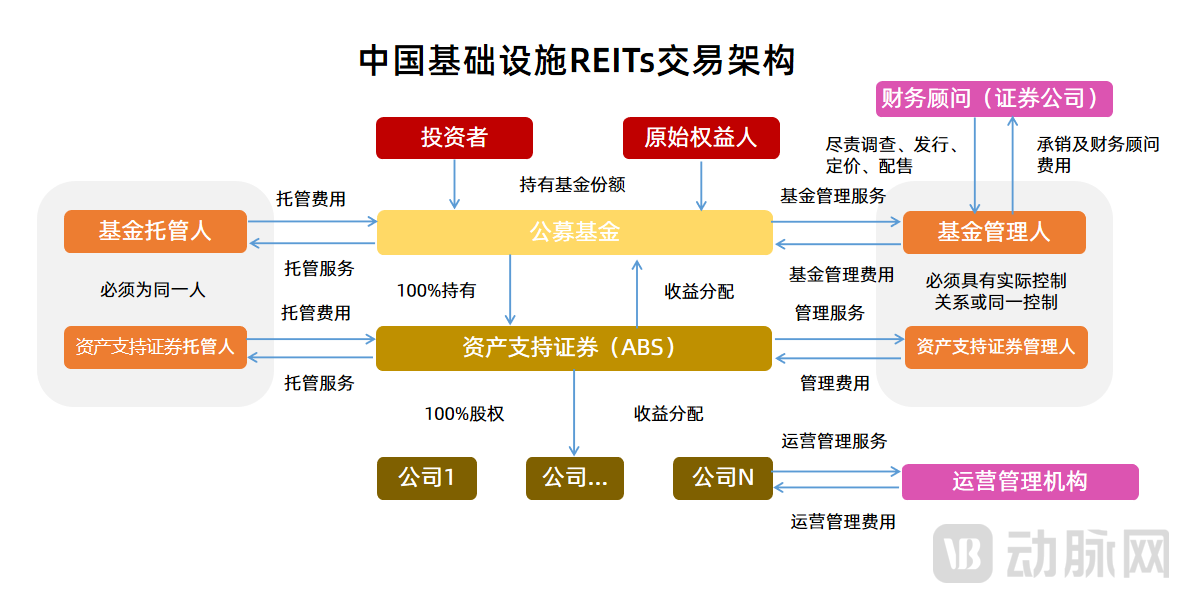

The full English name of REITs is Real Estate Investment Trusts, i.e.Real Estate Investment Trusts (REITs), refers to standardized financial products that are publicly traded on stock exchanges and convert real estate assets or interests with continuous and stable income into highly liquid listed securities through securitization. Its essence is real estate securitization, which can be colloquially understood as asset management institutions using a series of product designs to "slice" illiquid properties into multiple securitized products for trading, thereby providing an allocation channel for both suppliers and demanders of capital.

REITs originated in the United States in the 1960s. During their early development, they garnered little market attention due to limited effectiveness. It was not until the enactment of the U.S. Tax Reform Act and the boom in the American real estate industry that the advantage of REITs in enhancing capital turnover became increasingly apparent. The U.S. REITs market subsequently experienced substantial growth and gradually exported its successful model overseas.

To date, numerous countries around the world have established REITs markets, predominantly in developed economies across Europe and North America. China’s REITs market started relatively late, with its origins traceable to the early 21st century. However, it was not until 2014, when quasi-REITs products represented by the “CITIC Qihang Special Asset Management Plan” were introduced, that China officially embarked on its exploration of REITs. (“Quasi-REITs” refer to products whose institutional design is less mature than that of true REITs and which exhibit certain differences in product structure.)

In recent years, with the maturation of China’s legal framework, regulatory environment, and market conditions, as well as the practical experience gained from early quasi-REITs, China’s REITs market has entered a phase of rapid development.

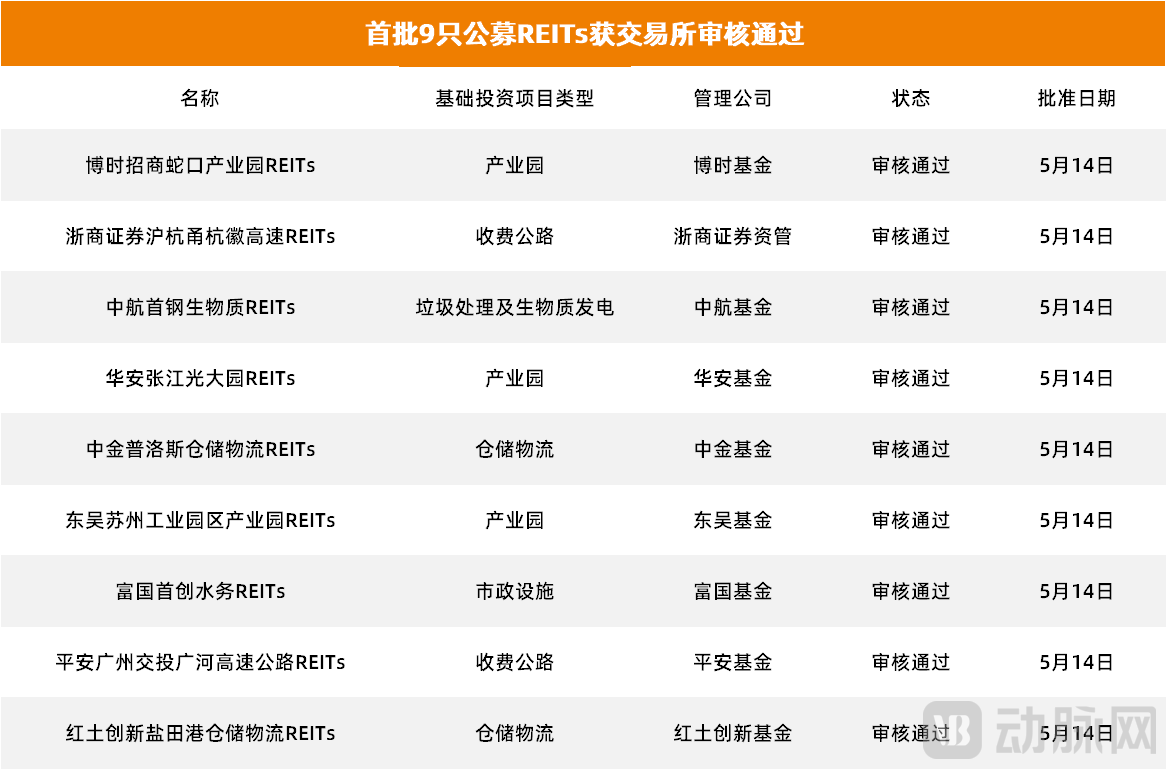

On May 14, the China Securities Regulatory Commission (CSRC) granted registration approval for the first batch of infrastructure public REITs projects on the Shanghai and Shenzhen stock exchanges. Among them, five projects were listed on the Shanghai Stock Exchange and four on the Shenzhen Stock Exchange. The projects cover mainstream infrastructure types such as toll roads, industrial parks, warehousing and logistics, sewage treatment, waste treatment, and biomass power generation. This marks a significant step forward in the pilot program for the first batch of infrastructure public REITs products, which will now enter the phase of public fund offering.

Among the nine infrastructure public REITs projects approved in this review, the Soochow Suzhou Industrial Park Closed-End Infrastructure Securities Investment Fund is China’s first biopharmaceutical industry-focused REITs project, holding significant importance for the future development of the biopharmaceutical sector.

It is understood that the underlying assets of this project are Phase I of the Suzhou BioBAY, with cash flows derived from leasing, property management, and other ancillary income generated by tenant enterprises within the bio-pharmaceutical industrial park. Zhonglian Fund serves as the general coordinator and financial advisor for the project, while Yuanlian Fund and Qianhai Open Source Asset Management act as the fund manager and special plan manager, respectively. Suzhou Industrial Park Baicheng Asset Management Co., Ltd., a wholly-owned subsidiary of the Bio-Company, serves as the asset operator, continuing to provide services to tenants of Phase I of the Bio-Industrial Park.

The originator will invest the proceeds raised from this issuance into the construction of the industrial park, fully leveraging the functions and strength of the capital market. By creating standardized financial products that are replicable and scalable, it aims to boost the economic development of the entire park and effectively expand funding for carrier infrastructure construction.Establish a virtuous development cycle of “development–incubation–maturity–REITs–redevelopment” to facilitate the rapid and healthy growth of the park’s “primary industry” and inject vitality into China’s biopharmaceutical sector.

In recent years, the Suzhou Municipal Government has attached great importance to the development of the biopharmaceutical industry. It has successively formulated and issued a series of important documents, including the Guiding Opinions on Accelerating the Clustered Development of Suzhou’s Biopharmaceutical Industry, Several Measures on Accelerating the High-Quality Development of Suzhou’s Biopharmaceutical Industry, and the Implementation Plan for Fully Building Suzhou into a Landmark for the Biopharmaceutical and Health Industries (2020–2030). These documents explicitly propose benchmarking against and drawing lessons from the “Boston Model” in the United States, comprehensively constructing a biopharmaceutical industrial ecosystem with distinct Suzhou characteristics, striving to establish Suzhou as the most competitive and influential biopharmaceutical industry landmark in China within ten years, and enhancing its international reputation.

Driven by concentrated policy support, Suzhou’s biopharmaceutical industry has ushered in unprecedented development opportunities, with BioBAY in the Suzhou Industrial Park serving as the most representative example. Compared with other biopharmaceutical industrial parks in China, BioBAY started relatively late but began at a high level, gained momentum rapidly, and achieved swift growth. In just over ten years, it has emerged as a significant and dynamic force in China’s biopharmaceutical sector that cannot be overlooked.

As of now, the number of listed companies within the Bio-Industrial Park, both domestically and internationally, has reached 17 (with two companies dual-listed). Biopharmaceutical enterprises in the park attract approximately RMB 10 billion in social capital investment annually, with cumulative financing exceeding RMB 50 billion. According to the “2020 Evaluation and Analysis Report on the Competitiveness of China’s Biopharmaceutical Industrial Parks” released by the Biotechnology Development Center of the Ministry of Science and Technology, Suzhou Industrial Park has retained its top position for industrial competitiveness—the most significant indicator—among biopharmaceutical parks across China, while ranking among the leaders in other key metrics.

The successful issuance of this special program aligns with Suzhou’s strategic goal of developing its “No. 1 Industry,” driven internally by the revitalization of assets. It responds to long-term market trends, enhances the capital market’s capacity to serve the real economy, and provides strong support for the comprehensive layout of the biopharmaceutical industry in the Yangtze River Delta region, thereby offering new possibilities and exploratory directions for biopharmaceutical industrial park-type REITs. Furthermore, it delivers solutions and innovative impetus for revitalizing existing state-owned assets to ensure their preservation and appreciation, as well as for innovating and upgrading corporate operational models and improving the quality and efficiency of park assets.

The pilot program for REITs at the Suzhou BioBAY is merely the beginning of this exploration; in the future, such initiatives will be continuously rolled out and implemented across more medical industry clusters.

Currently, with increasing support in terms of policies and funding, China’s healthcare industry is further exhibiting a trend toward clustered development. As a result, both the national government and local authorities are actively strategizing and supporting the growth of the healthcare sector.

At the national level, regions with strong industrial foundations, robust innovation capabilities, favorable business environments, and high levels of openness are continuously selected to support the establishment of medical health industrial parks. At the local level, governments across various regions integrate regional resources, strengthen top-level design, prioritize planning, and guide industrial clustering by formulating industry plans and policies, thereby fostering the development of distinctive medical health industrial parks in different areas.

However, it is essential to recognize that, compared with the mature industrial clusters abroad, China’s biopharmaceutical industry is still in its early stages and requires continuous improvement and optimization across all aspects. In particular, regarding the critical area of industrial investment funds, how to attract more capital inflows and maximize the value of existing capital constitutes a significant and highly urgent challenge for China’s biopharmaceutical sector.

However, the emergence of REITs may prevent this issue from remaining a core factor hindering industrial development.

From a corporate perspective, launching a pilot program for public REITs can help revitalize existing infrastructure assets, raise equity capital from the public to fund investments in addressing corporate weaknesses and new projects, cultivate new high-quality infrastructure assets, and inject them into REITs when conditions are ripe, thereby forming a virtuous cycle of infrastructure investment;From an Investor's Perspective, bringing mature infrastructure assets into the capital market helps provide financial products that offer both long-term allocation value and stable dividends;From the perspective of industry development, which is conducive to deepening supply-side structural reform in the financial sector, further enhancing the core capacity of capital markets to serve industrial development, thereby increasing the proportion of equity financing and broadening investment channels through which capital empowers industrial development.

Lin Caiyi, Deputy Dean of the Research Institute of China Chief Economists Forum, believes that China’s stock of infrastructure assets may exceed RMB 100 trillion. Based on an asset securitization rate of 1%, the potential market size for infrastructure REITs would surpass RMB 1 trillion. With the first batch of public infrastructure REITs projects approved by the Shanghai and Shenzhen Stock Exchanges, this new trillion-yuan-scale investment and financing market will gradually be activated in the future, holding significant importance for the development of China’s capital markets and for guiding industrial growth.

REITs: Perhaps the New Growth Engine for the Future of the Biopharmaceutical Industry