Comprehensive Analysis of China's Pharmaceutical and Biotech Industry in 2021: Investment Forecasts and Trend Insights

Excerpted from the 2021 iKang Capital White Paper on China’s Health Industry: Pharmaceuticals and Biotechnology Section, authorized for publication by VCBeat.

This article provides a detailed interpretation of four aspects:

1. What major changes occurred in 2020?

2. Key Investment Themes and Market Outlook for 2021

3. Investment Hotspot Predictions for 2021

4. 20 Companies Worth Watching

Core Viewpoints:

1. After years of development, China’s innovative drug industry has become highly mature in fast-follow strategies, capable of developing me-too or even me-better molecules within a 2–3 year time lag. However, an issue that cannot be overlooked is the intense competition around the same targets; for instance, more than 20 companies are currently conducting R&D on the claudin 18.2 target. Ultimately, drug development must return to its commercial essence: whether a pharmaceutical company can rationally design clinical trials to achieve the optimal approval pathway, rapidly complete clinical studies both domestically and internationally, and possess commercialization experience and pipeline management capabilities. These factors are even more critical than innovation in targets or mechanisms, especially given that China’s capital market has not yet fully opened its doors to first-in-class (FIC) drugs.

2. As volume-based procurement policies compel established pharmaceutical companies to transform and the first wave of biotech firms enters the commercialization stage, collaborative transactions centered on specific products will become more frequent in the future, taking on diverse forms and pathways (such as licensing, M&A, joint ventures, and CSO arrangements). Currently, hot assets attracting partnership interest remain concentrated in late-stage clinical products nearing commercialization. However, Phase III assets are scarce, expensive, and limited in choice; consequently, future collaborations will gradually shift toward earlier stages, potentially extending to partnerships with universities. This trend is underpinned by two factors: the continuous increase in corporate R&D investment driven by industry development, which has raised tolerance for failure rates, and the influx of talent returning from multinational pharmaceutical companies, which has enhanced the industry’s scientific and data-driven understanding of mechanisms and drug translation.

3. Intensifying competition in the innovative drug market has led to a year-on-year decline in returns for pharmaceutical companies under traditional R&D pathways, making the improvement of R&D efficiency an urgent industry-wide challenge. This situation provides an extensive platform for AI to penetrate and reshape the pharmaceutical industry. With the increasing maturity of AI technologies and the substantial accumulation of data on innovative drugs, numerous multinational pharmaceutical companies and internet giants have entered the AI-driven drug discovery sector.

The successive IPOs of Schrödinger and Relay Therapeutics, two AI-driven drug discovery companies, along with the advancement of several AI-developed drug candidates into clinical trials or IND-enabling stages, have drawn unprecedented attention to the field of AI in pharmaceuticals. While innovative drug companies differ in their technologies and application scenarios, they share a common goal: leveraging AI technology to enhance efficiency within the pharmaceutical industry. Although AI may not completely revolutionize the innovative drug R&D process in the short term, any incremental innovation in this trillion-dollar industry, which is crucial to human well-being, will generate substantial economic benefits and social value.

4. Key Sectors Attracting Capital in 2021:

· Gene Therapy

·RNA Therapeutics

· Cellular Immunotherapy

·Small-Molecule Targeted Drug Technology (PROTAC)

· ADC

· AI+ Drug Discovery

According to Frost & Sullivan analysis, China's pharmaceutical market size is projected to reach RMB 1.71 trillion in 2020, representing a year-on-year growth of 5.0%. Among these, the biologics market is experiencing the fastest growth, with a year-on-year increase of 18.5%, and is expected to reach RMB 369.7 billion in 2020. With a five-year compound annual growth rate (CAGR) of 19.1%, the biologics sector significantly outpaces both the chemical drug and traditional Chinese medicine markets.

Meanwhile, according to data from the National Bureau of Statistics, the value-added of industrial enterprises above designated size in China's pharmaceutical manufacturing industry increased by 5.9% year-on-year from January to December 2020, while investment in the pharmaceutical manufacturing sector rose by 28.4% year-on-year, indicating robust market enthusiasm.

From the perspective of patented drugs and generic drugs, the market size of patented drugs in 2020 is expected to reach RMB 963.9 billion, a year-on-year increase of 6.0%, accounting for 54.6% of the entire market; the market size of generic drugs will be RMB 750.8 billion, a year-on-year increase of 3.7%, with a market share of 45.4%.

We believe that the innovative drug market will continue to achieve rapid growth, driven by favorable policies, increased R&D spending by pharmaceutical companies, and heightened investment interest. Furthermore, its share of China’s pharmaceutical market is expected to rise even higher in the future.

Domestic Innovative Drugs Outpace Global R&D Progress, with Multiple Drugs Receiving FDA Approval

Over the past three years, conducting overseas clinical trials for new drugs has gradually become a common practice for Chinese innovative pharmaceutical companies in their global expansion strategies. Many companies have transitioned from following globally popular drug targets to securing First-in-Class or Best-in-Class positions in certain therapeutic areas.

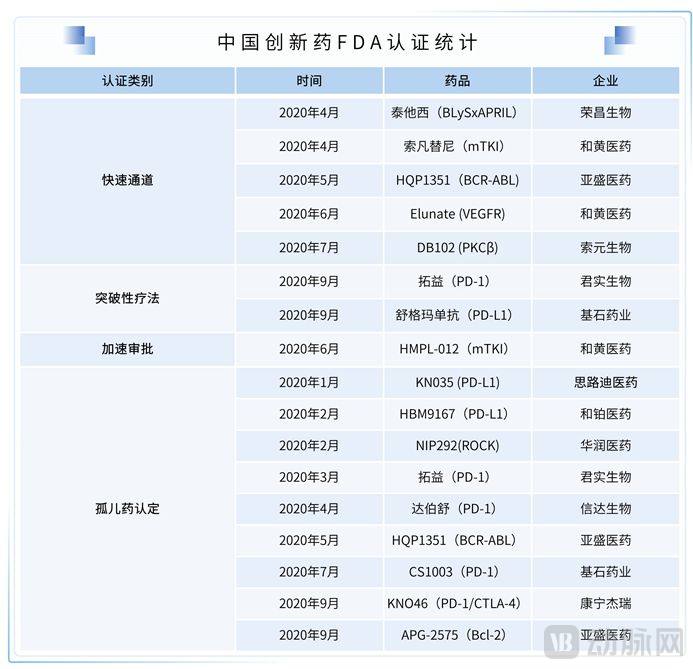

In November 2019, BeiGene’s BTK inhibitor zanubrutinib received FDA approval for the treatment of previously treated adult mantle cell lymphoma. This marked a milestone as the first independently developed Chinese innovative anticancer drug to receive both FDA Breakthrough Therapy Designation and marketing approval in the United States. Currently, following in zanubrutinib’s footsteps, several other domestically developed innovative drugs are in late-stage clinical trials in the U.S., holding promise for expanding the global footprint of China’s innovative pharmaceuticals.

In areas of unmet clinical need, certain domestically developed innovative drugs have also gained recognition from the U.S. Food and Drug Administration (FDA). In 2020, Chinese innovative drugs achieved significant milestones in the FDA approval process, with more than ten products receiving accelerated review, Breakthrough Therapy designation, or Orphan Drug designation. The first wave of Chinese innovative drugs going global has begun to demonstrate international competitiveness.

Both License-In and License-Out Activities Have Surged, with International Collaborations Becoming Increasingly Frequent

The upgrading of China’s domestically developed innovative drugs is also reflected in international collaborations. In the past, Chinese pharmaceutical companies primarily enriched their pipelines by licensing-in products from overseas early- or mid-stage biotech firms. However, as exemplified by the strategic multi-product collaboration between BeiGene and Amgen, Chinese pharmaceutical companies accelerated partnerships with multinational pharmaceutical giants in 2020, both in license-in and license-out transactions, ranking among the top globally in terms of deal value.

In terms of license-in deals, Chinese pharmaceutical companies completed more than 35 license-in product transactions in 2020, with collaboration models ranging from single-product acquisitions to the introduction of technology platforms, making it a landmark year for license-in activities. Noteworthy transactions include:

·Innovent Biologics and Roche Reach $2 Billion Partnership to Develop Universal CAR-T Therapies and TCB Bispecific Antibodies.

· Junshi Biosciences Enters into Collaboration Agreement with Revitope to License Its Proprietary Dual-Antigen-Guided T-Cell Chimeric Activation Technology Platform for the Development of Five CD3 Bispecific Antibodies

· BeiGene has licensed BioAtla’s tumor microenvironment-conditioned antibody technology to address the toxicity issues associated with CTLA-4 antibodies. 3SBio has spent $400 million to introduce GPS, a tumor immunotherapy vaccine targeting WT1, and AVB-500, which modulates the tumor microenvironment by inhibiting GAS6-AXL signaling pathway transmission.

In terms of license-out deals, the number of outbound licensing transactions by Chinese pharmaceutical companies exceeded 15 in 2020, a significant increase from the mere one or two cases seen annually in previous years. Spanning both products and technologies, multiple projects commanded upfront payments exceeding US$100 million, achieving breakthroughs in both quantity and quality. The robust activity in outbound licensing indicates that the R&D capabilities of Chinese pharmaceutical companies have begun to gain recognition in overseas markets. Notable transactions include:

· I-Mab’s CD47 monoclonal antibody, lemzoparlimab, granted AbbVie rights outside the Greater China region for a total consideration of nearly $3 billion, setting a transaction record in 2020.

· In 2020, Eli Lilly secured licenses for three new drugs from China. In addition to expanding its global collaboration with Innovent Biologics on sintilimab, the company obtained overseas development rights for a COVID-19 neutralizing antibody from Junshi Biosciences and acquired overseas rights to a BCL-2 inhibitor from Fosun Pharma.

· Jacobio has out-licensed its two SHP2 inhibitors targeting the hot therapeutic target SHP2.

· Harbour BioMed, WuXi AppTec, and Adagene have also secured multiple out-licensing deals for their biologic antibody and ADC technology platforms.

Looking back on 2020, the COVID-19 pandemic erupted at the beginning of the year, spreading across China in January and February before rapidly expanding worldwide. Under the combined influence of the pandemic and policy factors, China’s pharmaceutical industry as a whole exhibited an initial decline followed by a rebound, while the global biopharmaceutical sector experienced unprecedented fervor.

The pandemic’s positive impact on the pharmaceutical industry has been largely reflected at the capital level. On one hand, the pandemic has drawn greater public attention to and heightened the perceived importance of the pharmaceutical sector, significantly boosting market interest and enthusiasm. On the other hand, the pandemic-induced economic downturn has prompted governments worldwide to adopt counter-cyclical policies and measures, which have favored high-risk assets in the biotechnology sector. In China, monetary policy remains relatively accommodative, and fiscal policy supports the development of biopharmaceuticals as a national strategic emerging industry of major importance. Overall, the pandemic has created a highly favorable capital environment for innovative drug companies from a funding perspective.

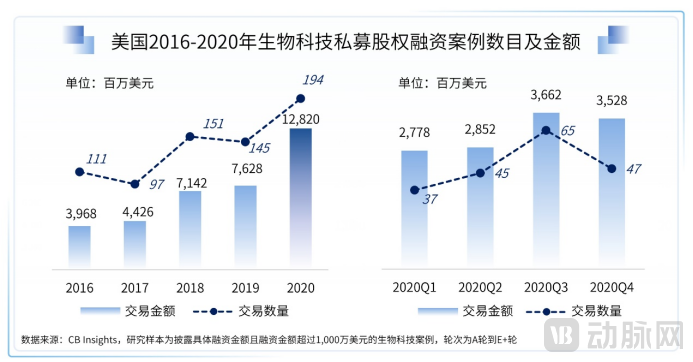

The overseas biotechnology market remains robust. In 2020, the number of primary market financing deals in the U.S. biotech sector rose to nearly 200, with the total funding amount increasing by 68% to reach $12.8 billion. Financing activity accelerated in the second half of the year, with both the number of deals and the total funding amount in the third quarter hitting their highest levels for the year.

Primary market financing in China’s biotechnology sector experienced explosive growth in 2020, with the number of financing deals increasing by over 200% and the total financing volume rising by nearly 300%, reaching approximately USD 4 billion. The primary market remained highly active during the pandemic, with financing in the second quarter alone accounting for 40% of the annual total. The number of financing deals increased steadily through the first three quarters, and although activity slowed in the fourth quarter, the financing amount remained substantial.

Clear Exit Mechanisms on the STAR Market and HKEX; Secondary Market Performance Exceeds Expectations

Since its inception, the number of initial public offerings (IPOs) and the total issuance market value of pharmaceutical and biotechnology companies on the STAR Market have risen rapidly. Although there was a slight decline in the first half of 2020 due to the impact of the pandemic, figures rebounded sharply in the third quarter, with both the number of IPOs and the amount raised reaching record highs.

For R&D-driven enterprises that meet the fifth set of listing criteria of the STAR Market, the issuance market capitalization is mostly concentrated in the range of RMB 10–15 billion. Their therapeutic focus is on oncology, and they all possess innovative drug pipelines. However, these pipelines are generally in the late stages of clinical development, which not only aligns with the concept of innovation but also mitigates the R&D risks that are closely monitored by regulatory authorities.

As another important channel for innovative pharmaceutical companies to go public, the number of initial public offerings (IPOs) by pharmaceutical and biotechnology companies on the Hong Kong Stock Exchange has increased year by year since 2017. In 2020, enthusiasm among pharmaceutical and biotechnology companies for listing in Hong Kong surged, with the total market value of IPOs growing by 65% and the number of IPOs reaching a record high.

Meanwhile, the Hong Kong stock market’s Chapter 18A segment experienced a surge in the second half of 2020, with both the number of initial public offerings (IPOs) and the total issuance value reaching record highs. Among the 16 pharmaceutical and biotechnology companies that went public in 2020, 14 were listed under Chapter 18A, making it commonplace for pre-profit companies to list on the exchange.

Accelerated Review and Approval, Smooth Market Access Channels

On March 30, 2020, the newly revised “Measures for the Administration of Drug Registration” was officially promulgated and came into effect on July 1. In this revised version, the introduction of four expedited pathways—Breakthrough Therapy Designation, Conditional Approval, Priority Review and Approval, and Special Approval—has opened new avenues for the accelerated approval of innovative drugs. Currently, policy guidance has evolved from broadly encouraging innovation to increasingly focusing on clinical value and unmet clinical needs.

This evolution is also in line with international trends. The FDA has been using these tools to accelerate drug development and review for many years. Between 2011 and 2018, 200 (54%) of the 367 new drugs and biologics approved by the FDA utilized at least one expedited development and review pathway, including 44 (12%) that received accelerated approval.

Following the release of the new administrative measures, the CDE website announced the first drug designated as a Breakthrough Therapy in August 2020: Legend Biotech’s LCAR-B38M CAR-T therapy took the lead. New drugs subsequently included in the priority review comprised Hengrui Medicine’s TPO receptor agonist hetrombopag olamine, CStone Pharmaceuticals’ KIT/PDGFRA mutant kinase inhibitor avapritinib, Junshi Biosciences’ PD-1 antibody toripalimab, BeiGene’s PARP inhibitor pamiparib capsules, and Hutchmed’s MET inhibitor savolitinib.

In 2020, the number of Investigational New Drug (IND) applications for Class 1 new drugs accepted by the Center for Drug Evaluation (CDE) grew rapidly, reaching a new high. More than 20 domestically developed innovative drugs submitted marketing authorization applications, and the number of approved domestic new drugs exceeded ten. With the explosive growth in IND applications in recent years, coupled with upgrades to the review and approval pathways, the annual number of approvals for domestic new drugs is expected to maintain continuous growth in the future.

National Reimbursement Drug List (NRDL) Negotiations Become Routine, Product Categories Continue to Expand, and Innovation Remains the Main Theme

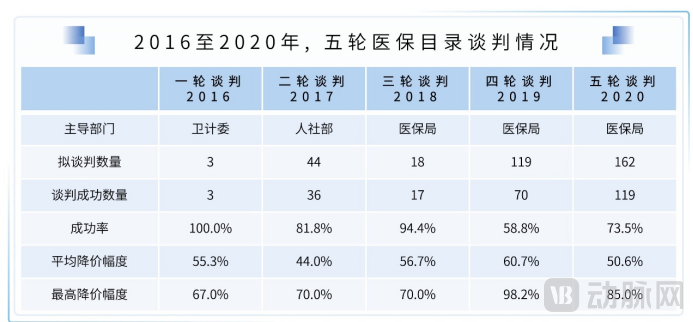

On February 9, 2015, the State Council issued the Guiding Opinions on Improving Centralized Procurement of Drugs in Public Hospitals, proposing for the first time at the top-level design stage a new approach of classified procurement. It required the establishment of an open, transparent, and multi-party drug price negotiation mechanism for certain patented drugs and exclusively manufactured drugs. In October 2015, with the approval of the State Council, 16 ministries and commissions, including the former National Health and Family Planning Commission, established an inter-departmental coordination mechanism to organize and launch the first pilot program for national drug price negotiations.

Since the first round of negotiations for inclusion in the National Reimbursement Drug List (NRDL) in 2016, a total of five rounds of NRDL negotiations have been completed to date. The number of drugs subject to negotiation has increased from three in the first round—tenofovir disoproxil, icotinib, and gefitinib—to 162 in the fifth round. The average price reduction has remained between 40% and 60%, covering major disease areas such as oncology, hepatitis, cardiovascular and cerebrovascular diseases, diabetes, and rheumatic and immune disorders.

In the latest round of national medical insurance negotiations, 66 drug products were added to the National Reimbursement Drug List (NRDL). Among them, 30 are manufactured by domestic companies. In the PD-(L)1 segment, Hengrui Medicine, Junshi Biosciences, and BeiGene all secured inclusion, whereas PD-(L)1 inhibitors from multinational pharmaceutical companies such as Merck & Co., Bristol Myers Squibb (BMS), AstraZeneca, and Roche were not included. It is anticipated that more domestic pharmaceutical companies will leverage these negotiations to exchange price concessions for volume gains, thereby capturing larger market shares.

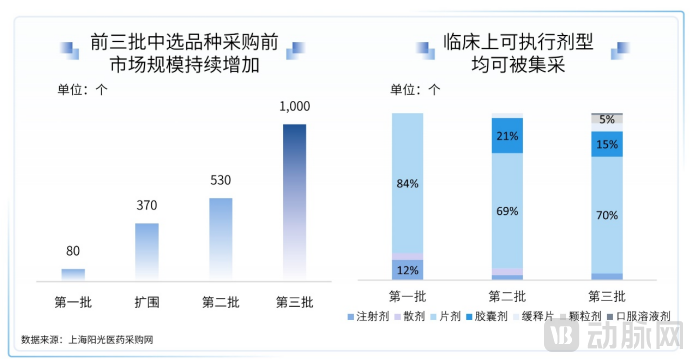

In addition to medical insurance negotiations, volume-based procurement has been conducted three times, with the fourth round imminent. In November 2018, the National Healthcare Security Administration officially released the "Document on Centralized Drug Procurement in 4+7 Cities" on the Shanghai Sunshine Pharmaceutical Procurement Network. The first batch included a total of 31 categories, with pilot programs implemented in 11 cities: Beijing, Tianjin, Shanghai, Chongqing, Shenyang, Dalian, Xiamen, Guangzhou, Shenzhen, Chengdu, and Xi’an. A total of 25 drug varieties were selected, among which only three were originator drugs, accounting for just 12%, demonstrating a significant substitution effect by domestically produced alternatives.

Subsequently, the rules for volume-based procurement were further refined to allow multiple enterprises to win bids and permit certain price variations among different manufacturers for the same drug, thereby gradually establishing a normalized, standardized, and nationwide long-term mechanism. Currently, volume-based procurement has been expanded across China, with the number of covered products rising to 90. The pre-procurement market size has continued to grow, and the range of dosage forms has been constantly expanding.

In 2020, significant healthcare insurance funds were allocated to pandemic response. Post-pandemic, cost-containment measures under the healthcare insurance system are likely to intensify, exerting further pressure on the payment side. As healthcare insurance negotiations and volume-based procurement policies become normalized, more pharmaceutical companies will be compelled by payment pressures to transition from generic drug production to innovation. From a long-term perspective, innovation will remain the consistent overarching theme.

DRGs Year One Combined with DIP: Deeply Optimizing Health Insurance Payment Methods

China's previous health insurance payment system was primarily based on fee-for-service (FFS) and global budgeting.

Fee-for-service payment refers to retrospective reimbursement based on the specific items and quantities provided during the diagnosis and treatment process. Since performing more procedures generates higher revenue, this model tends to lead to over-treatment. Global budget prepayment refers to the current health insurance global budget system, which primarily allocates regional funds to individual hospitals. Adjustments are made based on historical levels without considering changes in hospital service volume, which has, to some extent, led to hospitals refusing to admit critically ill or difficult-to-treat cases.

Since the 1980s, Europe, the United States, and Japan have begun exploring the Diagnosis-Related Groups (DRGs) payment model. DRGs classify patients with similar clinical characteristics into groups based on factors such as age, gender, length of stay, primary diagnosis, conditions, surgical procedures, disease severity, comorbidities, and complications. A bundled Medicare payment standard is determined for each group, and local health insurance agencies use this standard to make prospective payments to healthcare institutions. When hospitals admit patients covered by health insurance, the insurance agencies reimburse the hospitals according to the prospective payment standard for the specific condition.

In 2019, the National Healthcare Security Administration, the Ministry of Finance, the National Health Commission, and the National Administration of Traditional Chinese Medicine jointly issued the Notice on the List of National Pilot Cities for Diagnosis-Related Groups (DRG) Payment, designating 30 cities, including Beijing, Tianjin, and Handan in Hebei Province, as national pilot cities for DRG payment. After three years of preparatory work, the pilot cities conducted simulated operations in the second half of 2020 and initiated actual payments in 2021, marking the inaugural year of DRG implementation in China.

Half a year after the pilot implementation of Diagnosis-Related Groups (DRGs), China simultaneously introduced the Big Data Diagnosis-Intervention Packet (DIP) points-based payment system, with 71 pilot cities announced in November 2020. Under the DIP model, overall budget caps for healthcare institutions are no longer broken down into detailed control targets. Instead, payment units such as medical items, disease types, and per-diem rates are converted into a specific number of points. At the end of each year, the actual monetary value per point is determined based on the total points accumulated by all healthcare institutions and the regional medical insurance fund expenditure budget, and payments are made to healthcare institutions according to their actual points earned. Under the DIP system, if healthcare institutions wish to secure a larger share of the allocated budget, they need to accumulate more points, thereby incentivizing hospitals to provide more efficient and cost-effective medical services.

Whether it is DRG-based bundled payment or DIP point-based payment, both are classification systems for inpatients, with the fundamental aim of curbing unreasonable growth in medical expenses. Following the implementation of DRGs/DIP, healthcare security authorities can better control the total amount of insurance payments, while hospitals must control the cost per hospitalization. This compels hospitals to improve efficiency and reduce service costs, curb excessive examinations and overtreatment, and simultaneously enhance the quality of diagnosis and treatment to secure higher point values.

Of course, the introduction of any new system is accompanied by potential issues, such as exaggerating patient conditions to apply critical care fee standards, reducing necessary diagnostic and treatment items to save costs, and tilting resources toward tertiary medical institutions. Whether DRGs and DIP will be mutually exclusive or coexist in the future remains undetermined, and their actual effects still need to be verified and refined. However, the general direction of diversified cost control in China is very clear, and the pressure on pharmaceutical companies and hospitals to reduce prices and control costs will persist in the long term.

Commercial Insurance Is Emerging, and Individual Payment Capacity Continues to Rise

If public health insurance represents the equitable distribution of basic medical resources, then commercial health insurance constitutes differentiated, individualized purchasing. Currently, the development environment for commercial insurance is relatively robust. The government supports the establishment and operation of private hospitals while simultaneously introducing preferential individual income tax policies, thereby directly or indirectly stimulating and encouraging the growth of commercial health insurance.

Compared with the mature commercial insurance system in the United States, China’s commercial health insurance sector is still in its early stages of development. Urgent issues such as uneven regional development, limited product formats, and non-standardized coverage terms need to be addressed. However, with rising health awareness and disposable income among residents, it has become increasingly common for individuals and enterprises to purchase commercial insurance. In recent years, China’s health insurance industry has experienced rapid overall growth, with premium income maintaining an upward trend. The number of private hospitals has reached tens of thousands, and they are expected to become another major pillar of healthcare financing alongside the basic medical insurance fund in the future.

mRNA Technology Leads COVID-19 Vaccine Development, Reshaping the Vaccine Industry Landscape

Traditional vaccines typically require eight years or more to move from the laboratory to the market, a process that includes design, development, preclinical testing, clinical trials, and regulatory review. Leveraging the technical advantages of rapid design and fast production, mRNA vaccines quickly emerged as the strongest contenders to be among the first COVID-19 vaccines approved for market entry at the outset of the global vaccine development race.

Indeed, the first COVID-19 vaccine approved for widespread global use was the mRNA vaccine developed by BioNTech in collaboration with Pfizer. It not only demonstrated a favorable safety profile, but Phase III clinical trial data also showed an efficacy of 90%. Another mRNA vaccine from Moderna achieved an efficacy of 94%, demonstrating outstanding performance.

According to statistics, mRNA vaccines are currently the most widely administered COVID-19 vaccines globally, with their protective efficacy and safety supported by real-world data. These findings suggest that mRNA technology holds promise for combating future infectious disease outbreaks. Consequently, developing vaccines using mRNA technology is no longer purely a scientific challenge but rather an engineering problem.

It is reasonable to believe that the overall landscape of the vaccine industry will be reshaped by the application of mRNA technology. Meanwhile, given the technical mechanisms and modes of action of mRNA vaccines, there is high expectation for their potential in combating tumors.

AI + Drug Discovery Emerges as a New Pathway for Novel Drug Development

Generally, the research, development, and market launch of innovative drugs require decades and cost billions of dollars, with a failure rate exceeding 90%.

In 2020, the FDA approved a total of 53 new drugs for market launch, among which 35 were small-molecule drugs. Most of these drugs were designed based on known molecular targets, and it was extremely rare to discover new molecules capable of acting on novel targets with broad therapeutic indications. However, with the rapid accumulation of drug R&D data, digital transformation, and the accelerated development of artificial intelligence (AI) technologies, the application of AI in new drug discovery has been increasingly prevalent.

In principle, compared with traditional methods, AI can enable faster, lower-cost, and superior decision-making, particularly when supported by appropriate data or simulations. The integration of AI into the entire drug research and development (R&D) process is advancing through exploration, spanning from drug target discovery, virtual screening, drug synthesis, prediction of ADME-T (absorption, distribution, metabolism, excretion, and toxicity) properties and physicochemical properties (such as crystal forms), and drug repurposing, to the management of clinical trials and patient recruitment, as well as pharmacovigilance applications and the generation of real-world evidence.

New Players in Various Roles Focus on Chinese Innovation, Reshaping the Pharmaceutical Industry

Amid the continuous development and transformation of China’s innovative drug industry, an increasing number of new players are entering this arena.

On one hand, traditional pharmaceutical companies are increasingly prioritizing and expanding their innovative drug businesses, while the rising industry enthusiasm has attracted numerous scientists to launch startups and join the sector. On the other hand, as domestic industrial giants make strategic moves in pharmaceutical investments, overseas pharmaceutical companies are also establishing investment footholds in China. With US dollar-denominated funds becoming increasingly active in the Chinese market, Chinese innovation has come into the spotlight of global players.

In addition to successful examples of domestic traditional pharmaceutical companies transforming into innovative drug enterprises, such as Hengrui Medicine and Sino Biopharmaceutical, there are still thousands of traditional pharmaceutical companies in China. These companies are currently engaging in self-innovation and business iteration, emerging as new players in the innovative drug industry. Notably, many of these companies are publicly listed, and some are already seeking to spin off their innovative drug business segments to accelerate the development of their innovative drug pipelines.

As China’s innovative drug industry continues to develop, an increasing number of new players are entering the biopharmaceutical investment and financing market:

· Real estate giant Country Garden established Country Garden Ventures in 2019 and has completed multiple investments in the healthcare sector, including Mabspace Biologics.

· AstraZeneca and CICC Capital’s Joint Global Healthcare Industry Fund Completes $1 Billion Fundraising. This fund is the first healthcare industry fund raised by AstraZeneca globally and, to date, its largest such fund. It also marks AstraZeneca’s inaugural practice in China of integrating industrial operations with financial capital.

·Multiple US dollar-denominated funds participated in financing rounds for Chinese biopharmaceutical companies in 2020. Institutions such as RA Capital, Janchor Partners, and Cormorant Asset Management appeared among the investors of several companies, including Conatus Pharmaceuticals (Kangnaide), Everest Medicines, RemeGen, InnoCare Pharma (Yifang Bio), and CanSino Biologics (Beihai Kangcheng).

Amid a landscape of flourishing enterprises and diverse players, China’s biopharmaceutical industry will see continuous improvement in its investment and financing systems, including pipeline assessment and valuation.

In the Post-Pandemic Era, Value Returns: Only Enterprises with Sustained Innovation Capabilities Can Achieve Long-Term Recognition

Entering 2021, against the backdrop of widespread vaccine adoption and the normalization of epidemic prevention measures, the impact of the pandemic is expected to gradually fade. The industry is likely to place greater emphasis on the evolution of mid-to-long-term fundamentals. Key dimensions that truly reflect product value—such as the innovativeness of pipeline products, clinical data, and team execution capabilities—are anticipated to become the primary criteria for market pricing, thereby imposing new requirements on industry participants.

In 2020, the supply of biomedical companies listing on the STAR Market increased, while regulatory scrutiny tightened slightly. Zesheng Technology and Yiteng Jingang terminated their IPOs, and two of the seven companies listed under the fifth set of listing criteria saw their stock prices fall below the offering price, signaling a clear valuation correction. The implicit requirements in the determination of STAR Market attributes and the clarification of delisting rules also reflect the ongoing tightening of regulatory review.

Specifically, the requirements for scientific and technological innovation attributes include having more than five invention patents that generate core business revenue, with R&D investment accounting for more than 5% of operating income over the past three years, or cumulative R&D investment exceeding RMB 60 million over the same period. Therefore, companies operating under a pure license-in model should approach listing on the STAR Market with caution.

The delisting rules stipulate that under the fifth set of listing criteria, if a listed company reports both negative net profit and operating revenue below RMB 100 million in its fourth fiscal year, a delisting warning will be issued. Given that it typically takes 3–5 years for innovative drugs to progress from Phase III clinical trials to market launch, it can be inferred that companies planning to list under the fifth set of criteria must have at least one drug candidate in Phase III clinical trials or registration-enabling clinical studies.

In 2020, the Hong Kong stock market experienced severe polarization, with only solid fundamentals able to support higher valuations. Harbour BioMed, Simcere Pharmaceutical, and JW Therapeutics all broke their IPO issue prices shortly after listing; Yongtai Biologics broke its issue price on the 20th day post-IPO. In total, seven pharmaceutical companies listed in Hong Kong have traded below their IPO prices.

In summary, companies with disappointing stock performance are primarily concentrated in overcrowded sectors, where the clinical value of their products is called into question regarding market size and future R&D potential; in contrast, pharmaceutical and biotechnology companies with outstanding performance possess three key success factors: market prospects, innovative R&D capabilities, and strategic pipeline layout.

Whether the future pipeline is robust, balanced, and well-stratified; whether in-house developed products possess First-in-Class or Best-in-Class potential; whether License-in products are supported by commensurate clinical development capabilities; and whether the therapeutic areas focus on large markets such as oncology and autoimmune diseases or high-potential specialty fields will all drive valuation differentials.

Furthermore, in an environment of surging enthusiasm in the capital markets, the risks associated with drug development may be obscured by transient prosperity; however, the successive announcements by multiple listed pharmaceutical companies terminating clinical trials have still sounded an alarm for investors. In the near future, stock price volatility for innovative pharmaceutical companies is likely to remain significantly elevated. For example:

· On February 8, Bio-Thera Solutions announced that its independently developed HER2-ADC, BAT8001, failed to meet the pre-specified superiority endpoint versus the control group (lapatinib plus capecitabine) in its Phase III clinical trial. The R&D expenditure of RMB 226 million may be written off, and the company’s stock price plummeted by 18.73% in response. BAT8001 has become the first product among STAR Market-listed companies to have its clinical development terminated.

·Immunovant, a partner of Harbour BioMed, terminated the overseas clinical trials of MVT-1401 due to safety concerns, causing Harbour BioMed’s stock price to plummet by 11.49% on the day the news was announced.

·Kintor Pharmaceutical’s core product, proxalutamide, saw its stock price plummet by nearly half after failing to meet the first primary endpoint in Phase III clinical trials; however, the stock later recovered its losses following a major breakthrough in the use of proxalutamide for treating COVID-19.

The successive waves of IPOs and subsequent trading-below-offer-price debuts in the biopharmaceutical sector are less indicative of a bubble forming and bursting, but rather reflect the restructuring of the industry’s supply chain and development logic following more than a decade of sustained investment in capital and talent. China’s biopharmaceutical industry is now getting back on track, gradually entering a phase characterized by technological accumulation and R&D breakthroughs.

The risks inherent in drug development persist. In the future, value will increasingly center on independent R&D capabilities, business development (BD) and clinical execution prowess, and local commercialization capacity, while capital market investments will trend toward greater rationality.

Compared to the increasingly fierce competition in oncology, ophthalmology remains a blue-ocean market.

In recent years, driven by factors such as population aging, lifestyle changes, increased work intensity, greater exposure to allergens, and improper eye use, the prevalence of various ocular conditions—including eye infections, keratoconjunctivitis, dry eye disease, corneal injury, retinopathy, cataracts, and glaucoma—has risen year by year, leading to rapid growth in the ophthalmology market. Statistics show that China has 75 million patients with dry eye disease, 51 million with age-related macular degeneration (AMD), and 6 million with glaucoma, representing a substantial patient base.

Layouts in the ophthalmology sector have been progressively initiated over the past one to two years. Anti-VEGF therapy currently represents the most fundamental direction for ophthalmic drug R&D in China, with companies such as Ocumension Therapeutics, Qilu Pharmaceutical, and Zhuhai Essex Bio-Technology all establishing their presence in this area. In the segment with the highest patient prevalence, namely myopia and presbyopia, Zoclean Eye Care, a subsidiary of Lee’s Pharmaceutical, announced a product licensing agreement with Nevakar to secure exclusive commercialization rights for low-concentration atropine. Additionally, Aura Biosciences (Jimu Shengwu) licensed MicroPine, which utilizes the Optejet micro-dose drug delivery platform, from Eyenovia. In the field of dry eye disease, Hengrui Medicine licensed two drugs from Novaliq, aiming to target the dry eye disease segment where treatment options remain limited.

China has a large population of ophthalmic patients, yet public awareness of eye diseases remains significantly lower than in Europe and the United States. Research and development in areas such as uveitis and retinopathy remain largely unexplored. In contrast, ophthalmic treatment in the U.S. has moved beyond anti-VEGF therapies, with emerging modalities such as gene therapy, cell therapy, and complement therapy achieving promising clinical progress. As the next major frontier, the field of ophthalmology still holds numerous opportunities to be uncovered, both in depth and breadth.

Compared with chemotherapy, small-molecule targeted drugs have well-defined mechanisms of action and fewer side effects. Compared with large-molecule drugs, small-molecule drugs can be administered orally, leading to better patient adherence and lower production costs. In recent years, as immunotherapy has become increasingly prevalent, large-molecule drugs have dominated the spotlight. However, with the clinical validation of KRAS, a target once considered undruggable, small-molecule drugs are expected to regain momentum in research and development.

Three Major Advances in the Small Molecule Field in 2020

First, Amgen has submitted a New Drug Application (NDA) for sotorasib targeting KRAS, and the drug has received FDA Breakthrough Therapy Designation; Mirati’s KRAS G12C inhibitor, adagrasib, demonstrated a disease control rate (DCR) of up to 96% in patients with non-small cell lung cancer (NSCLC) harboring specific mutations during Phase 1/2 clinical trials; additionally, drugs targeting related pathway components such as SOS1 and SHP2 are progressively entering clinical development.

Secondly, small-molecule drugs are entering the autoimmune disease sector, which has long been dominated by biologics. AbbVie’s upadacitinib met its clinical endpoints in Phase 3 trials for atopic dermatitis; Hengrui Medicine’s independently developed highly selective JAK1 inhibitor, SHR0302, also met its clinical endpoints in Phase 2 trials for atopic dermatitis.

Finally, PROTAC technology achieved a major breakthrough. Arvinas released positive efficacy data for ARV-110 and ARV-471 in patients with prostate cancer and breast cancer, respectively, leading to a 95% surge in its stock price on the day and a market capitalization of $2.367 billion. Nurix Therapeutics subsequently completed multiple transactions, including a global strategic collaboration with Gilead Sciences valued at up to $2.345 billion and a strategic partnership with Sanofi worth up to $2.5 billion.

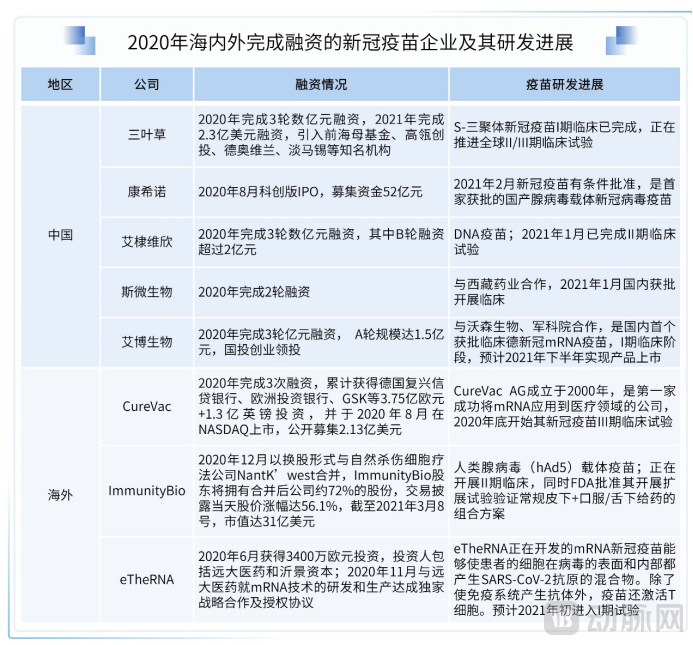

In 2020, the hottest investment theme in the healthcare sector, spurred by the COVID-19 pandemic, was undoubtedly COVID-19 vaccines.

Based on a variety of different vaccination approaches, more than 200 COVID-19 candidate vaccines are under development worldwide. In this race to develop COVID-19 vaccines, mRNA technology has once again taken center stage.

On December 2 last year, the mRNA COVID-19 vaccine produced by BioNTech in collaboration with Pfizer, one of the “big three” mRNA companies internationally, was granted a “Temporary Authorization for Emergency Use” by the UK’s Medicines and Healthcare products Regulatory Agency (MHRA), becoming the first COVID-19 vaccine approved for widespread use globally. This approval, based on Phase III clinical trial results, is of significant importance. Shortly thereafter, on December 18, Moderna’s mRNA COVID-19 vaccine also received Emergency Use Authorization (EUA) in the United States, as well as authorization in the United Kingdom and Canada.

Leveraging the momentum gained during the pandemic, mRNA technology has evolved from being “largely ignored” three decades ago to becoming “highly sought-after” today, emerging as a new favorite in the biopharmaceutical sector and a key strategic focus for major pharmaceutical companies.

In 2020, “AI-Driven Molecular Discovery” was included in the list of “10 Breakthrough Technologies” released by MIT Technology Review. It is conceivable that when artificial intelligence and the pharmaceutical industry—two trillion-dollar sectors—converge, they are poised to unleash enormous potential.

The capital market has also shown strong favor toward this sector. In 2020, a total of 17 companies focused on AI-driven drug development completed more than 20 financing rounds, each exceeding $10 million, with the total amount raised reaching approximately $3 billion.

As the first publicly listed company in this field, Schrödinger went public on the Nasdaq in February 2020 and currently has a market capitalization of $5.66 billion. Schrödinger’s development trajectory offers a reference model for other companies in the industry. The company’s core technology platform is its physics-based computing platform, which provides integrated, differentiated solutions for predictive modeling, data analysis, and collaborations in the new drug discovery process.

According to the company’s latest annual report, in 2020, all of the top 20 pharmaceutical companies adopted Schrödinger’s solutions, contributing approximately $32 million in revenue, which accounted for 34% of total software revenue. The number of customers with an Annual Contract Value (ACV) exceeding $100,000 continued to grow, rising from 122 in 2018 to 153 last year. Meanwhile, as of 2020, the retention rate for customers with an ACV over $100,000 reached 99%, setting a new historical high. These figures demonstrate that Schrödinger’s solutions are gaining increasing recognition among customers.

Furthermore, the company is deeply engaged in collaborative R&D with pharmaceutical enterprises. Last year, it partnered with pharmaceutical companies to advance the development of over 25 new drug projects. These projects are expected to generate upfront payments, research funding, and milestone payments for Schrödinger, as well as potential additional milestone payments, option fees, and royalties.

In November 2020, the Company entered into an exclusive global collaboration and license agreement with Bristol Myers Squibb (BMS) to discover, research, and develop targeted therapies in the fields of oncology, neurology, and immunology. Under the terms of the agreement, the Company received a $55 million upfront payment from BMS and is eligible to receive potential future payments totaling up to $2.7 billion.

This collaboration not only enables the early generation of revenue at a certain scale but also accumulates a broader dataset and secures brand endorsement from top multinational corporations (MNCs), which is highly beneficial to the company’s business development. In addition to sales and external collaborations, Schrödinger launched internal R&D projects in mid-2018 aimed at discovering first-in-class (FIC) or best-in-class (BIC) drugs. The company expects to submit three Investigational New Drug (IND) applications in 2022 and anticipates obtaining clinical data from its first IND-enabled project by mid-2022.

Relay Therapeutics, another company that went public in 2020, has a relatively focused business strategy. Leveraging its Dynamo platform—which integrates novel experimental techniques (such as room-temperature crystallography and cryo-electron microscopy) with computational technologies (including molecular dynamics and machine learning)—and utilizing the custom-built Anton 3 supercomputer, Relay is dedicated to developing targeted therapies with higher specificity and potency against protein targets.

Dynamo’s AI can search through millions of potential compounds to identify those offering maximal potency, selectivity, and bioavailability, thereby accelerating the development of drug candidates in clinical and pre-commercialization stages. The company’s current pipeline includes two Phase I clinical candidates—RLY-1971 (an SHP2 inhibitor) and RLY-4008 (an FGFR2 inhibitor)—as well as one pre-IND candidate, RLY-PI3K1047 (a PI3Kα inhibitor).

The successful listings of overseas AI companies have provided a reference model for the development of domestic enterprises. Although the AI-driven drug R&D segment in China has been relatively quiet in recent years, it has begun to accelerate significantly since multiple companies, including XtalPi, completed financing rounds last year. With the rapid advancement of businesses across various categories of AI-driven drug R&D firms, and the emergence and growth of more such companies fueled by capital, AI is becoming an unstoppable new driving force in new drug development, poised to become the next-generation infrastructure for pharmaceutical R&D.

Of course, significant challenges remain in this process, such as data interfacing, standardization, and integration with existing R&D systems. These challenges present opportunities for all industry players, including domestic AI-driven drug discovery companies.

The 2020 Nobel Prize in Chemistry was awarded to Dr. Emmanuelle Charpentier, a French microbiologist, and Dr. Jennifer A. Doudna, a member of the U.S. National Academy of Sciences, for their outstanding contributions to gene editing, a development that has greatly energized the field of gene editing and the broader realm of gene therapy.

The first gene therapy product in Western countries was Glybera, a gene therapy drug from UniQure, approved by the European Medicines Agency (EMA) in 2012. Although the drug was not commercially successful after its official launch in 2014 and was withdrawn from the market in 2017, its approval thoroughly opened the door to gene therapy.

In the following years, multiple gene therapies and related technical products entered the market successively: in 2016, GlaxoSmithKline’s Strimvelis was approved for marketing in Europe; in 2017, Novartis and Gilead Sciences respectively received U.S. approval for their CAR-T therapies Kymriah and Yescarta, and Spark Therapeutics’ AAV vector-based gene therapy drug Luxturna, among others.

In overseas capital markets, gene therapy companies experienced an IPO boom in 2020, with seven companies going public and raising a total of $1.2 billion. In China, in addition to Gendicine, the first approved gene therapy product, and Oncorine, the second one to reach the market, more than 20 clinical trials are currently underway in the field of gene therapy. These trials target indications including hemophilia A and B, beta-thalassemia, metastatic non-small cell lung cancer, esophageal cancer, Leber’s hereditary optic neuropathy (LHON), autoimmune deficiency diseases, and various solid tumors.

Mirroring the vigorous advancement of gene therapy clinical trials, investment enthusiasm in China’s gene therapy sector was also exceptionally high in 2020. According to incomplete statistics, multiple companies in the domestic gene therapy field completed financing rounds last year, with many securing two or more rounds of funding.

Entering the third decade of the 21st century, CXO/pharmaceutical outsourcing organizations have become integrated into the entire lifecycle of pharmaceutical products. As a vital segment of the pharmaceutical industry, the prosperity of the pharmaceutical outsourcing sector is closely tied to the development of the broader pharmaceutical industry.

Over the past decade, driven by the rapid growth of the pharmaceutical industry, China’s pharmaceutical outsourcing sector has also experienced explosive development, giving rise to several leading platform-based enterprises such as WuXi AppTec and Pharmaron. Meanwhile, companies like WuXi Biologics, Tigermed, and Asymchem have deepened their industrial development within niche segments while expanding their business horizontally.

The market size of the CXO industry is primarily driven by downstream R&D investment and penetration rates. With intensifying competition in new drug development, sustained growth in R&D spending, and increasingly stringent requirements from pharmaceutical companies for efficiency and quality, coupled with favorable policies such as incentives for innovation and the Marketing Authorization Holder (MAH) system, the penetration rate of CXO services is expected to rise continuously in the long term. Leading companies in each niche segment are steadily strengthening their scale and supply chain advantages through continuous accumulation, thereby establishing a sustainable long-term growth trajectory.

Financing in China’s CXO sector was also extremely robust in 2020. Notably, Tigermed’s listing on the Hong Kong Stock Exchange raised over HK$10.7 billion, further enhancing its industry influence and ushering the CRO industry into an era dominated by two major players. It is evident that in a market environment characterized by strong investor enthusiasm for healthcare, companies with clear technological or scale advantages in niche segments have gained significant recognition and favor from investors.

The CXO sector continues to maintain its momentum. Although only three months have passed in 2021, Auscan Biologics, a well-known enterprise in the CDMO field, has completed a new round of Series C financing amounting to nearly RMB 500 million in early March this year, following two consecutive rounds of funding last year. This demonstrates that investors remain optimistic about the growth prospects of leading companies in this niche segment.

Adeno-Associated Virus (AAV) Delivery Technology

Since the 1970s, the invention of genetic engineering has driven the development of key technologies closely related to gene therapy, such as gene delivery, acquisition, and editing. Important genetic engineering techniques—including gene vector technology, gene cloning, and gene editing—have profoundly influenced modern gene therapy.

Currently, the most prominent technologies in the gene therapy field are arguably adeno-associated virus (AAV) vector delivery technology, CRISPR gene editing technology, single/dual base editing technology, and oncolytic virus genetic engineering technology.

Adeno-associated virus (AAV) was first discovered in the mid-1960s in laboratory adenovirus (AdV) preparations and was subsequently identified in human tissues. Characterized by its non-pathogenicity, efficient long-term gene expression, ease of genetic manipulation, and low or absent immunogenicity, AAV has become a pivotal tool for gene delivery. Given that different AAV serotypes exhibit distinct tissue tropism, researchers are also exploring the use of AAV vectors to achieve targeted therapy.

To date, three gene therapy drugs using recombinant adeno-associated virus (AAV) as a vector have been approved for marketing worldwide, and additional AAV-based gene therapies have submitted marketing applications. This demonstrates the immense potential of AAV gene therapy. In addition to AAV, other viral vectors currently used in clinical practice include adenovirus (AdV), lentivirus (LV), and retrovirus (RV).

CRISPR Gene Editing Technology and Single/Double Base Editing Technology

As a gene-editing tool, CRISPR has become the most prominent technology in the field of biomedicine. Currently, CRISPR technology is highly mature; it was awarded the Nobel Prize in Chemistry in 2020 and holds promise for providing new therapeutic avenues for patients with various hereditary genetic disorders.

While CRISPR technology is widely applied in the field of gene therapy, techniques such as RNA editing based on the CRISPR-Cas13 family—which enable RNA editing, knockout, detection, tracking, and imaging—deserve attention from the industry.

Another noteworthy advancement is single- and dual-base editing technology. Since many genomic mutations occur at the single-base level, there is a heightened demand for greater precision in gene editing. In response, CRISPR-based single-base editing technologies have emerged. However, single-base editing systems suffer from significant off-target effects and can induce extensive unintended mutations. They also have limitations such as a narrow editing window and low editing efficiency. To address these issues, Prime Editor (PE), a gene editor capable of searching and replacing bases, has been developed. PE can effectively achieve all 12 types of base conversions and enable precise multi-base insertions without relying on double-strand breaks (DSBs) or donor DNA.

Oncolytic Virus Genetic Engineering Technology

Oncolytic Virus (OV) is a class of viruses that can selectively infect and kill tumor cells, possessing the ability to replicate specifically and stimulate the body to produce an anti-tumor immune response. Special oncolytic viruses are created by genetically modifying some naturally occurring viruses with weak pathogenicity. These modified viruses exploit the inactivation or defects of tumor suppressor genes in target cells to selectively infect tumor cells, replicate extensively within them, and ultimately destroy the tumor cells.

As recombinant viral genome engineering technologies mature, oncolytic virus therapy has been widely adopted in clinical practice. In recent years, genetic engineering of oncolytic viruses has re-emerged into the spotlight, becoming a promising spark in the field of gene therapy research and development both in China and abroad, warranting high expectations.

RNA therapeutics, referring to RNA-based drugs or vaccines, are primarily categorized into three types: oligonucleotides, mRNA, and RNA-related small molecules. In 2020, the rapid and efficient development and regulatory approval of mRNA-based COVID-19 vaccines drew greater attention to RNA therapeutics.

With the market launch of Evrysdi (risdiplam), the first approved small-molecule RNA-targeting therapy, in August last year, its cumulative sales reached $8.9 million in the third quarter. Additionally, the mRNA vaccines from BioNTech and Moderna were successively approved in December of last year. There is reason to believe that the momentum behind RNA therapies will continue to intensify in 2021 and for many years to come.

Currently, the leading players in the RNA therapeutics sector are predominantly small and mid-sized biotechnology companies, while large multinational pharmaceutical firms primarily engage through deep collaborations with a select few top RNA biotech enterprises. According to the review article “RNA therapeutics on the rise” published in Nature Reviews Drug Discovery in 2020, more than 400 RNA-targeted drug development programs, including mRNA vaccines, were in various stages of clinical research, suggesting that multiple RNA therapies are expected to gain regulatory approval and reach the market in the near future.

Compared with the global pipeline, domestic companies have been slower to follow up in the RNA field, mainly consisting of small biotechnology companies and CROs, with fewer large pharmaceutical companies involved. Moreover, existing projects are primarily focused on siRNA and mRNA technology areas, which are still in early stages and not yet highly competitive. It is recommended that investors pay attention to innovative biomedical enterprises that possess advanced technologies in nucleic acid modification and delivery systems, as well as those with pipelines across different disease areas.

In 2017, the FDA successively approved Novartis’s Kymriah (for lymphoma) and Gilead’s Yescarta (for leukemia), two CAR-T cell immunotherapies, for market launch. This spurred a surge of companies, backed by capital, into the immune cell therapy sector in recent years. Particularly in the already niche field of hematologic malignancies, dozens of enterprises have crowded in, creating a competitive landscape strikingly similar to that of the PD-1/PD-L1 space.

We believe that only CAR-T companies capable of demonstrating commercial viability in the field of hematologic malignancies—encompassing regulatory approval, scaled manufacturing, and sales infrastructure—possess investment value. For other enterprises still in the pre-commercialization phase, they must prove themselves with robust products characterized by superior efficacy, enhanced safety profiles, and lower costs.

Relatively speaking, emerging technologies such as TILs, U-CART, CAR-NK, and TCR-T, as well as CAR-T therapies potentially applicable to solid tumors, may present greater investment opportunities. However, these technologies face a common challenge: the absence of successfully marketed products to serve as reference cases, which poses a significant hurdle for investors.

TIL Immunotherapy

TIL therapy utilizes immune cells derived from tumor-infiltrating lymphocytes. It typically involves identifying specific mutations in the patient, using this mutational information to isolate T cells capable of effectively targeting these mutations, and then extracting these T cells. These T cells can precisely recognize cancer cells; after undergoing ex vivo expansion and other processing steps, they are reinfused into the patient to exert anti-tumor effects. TIL immunotherapy is currently still in the clinical trial phase.

As a highly differentiated, customized, and targeted immunotherapy, TIL therapy still has certain limitations in terms of efficacy, safety, and accessibility: for example, the difficulty in isolating specific T cells from tumor-infiltrating tissues, the lack of unified standards, and the suppression of T cells by the tumor microenvironment.

Universal CAR-T (U-CAR-T) Therapy

Universal CAR-T, as a next-generation immunotherapy product, offers unparalleled advantages, including scalable industrial manufacturing, consistent quality, lower costs, broader patient applicability, and shorter production cycles.

However, the FDA has remained highly vigilant regarding the safety of allogeneic therapies entering clinical trials. In particular, several U-CART-related clinical studies have been halted in recent years. This is primarily because the T-cell receptor (TCR) on allogeneic T cells may recognize alloantigens in the recipient’s body, thereby triggering graft-versus-host disease (GVHD).

Furthermore, HLA expression on allogeneic T cells can rapidly trigger rejection by host immune cells. Therefore, minimizing or avoiding safety issues is key to the success of this technology.

CAR-NK Therapy

Natural killer (NK) cells are a unique group of anti-tumor effector cells that play a pivotal role in both innate and adaptive immune responses, owing to their MHC-unrestricted cytotoxicity, cytokine production, and immunological memory capabilities. Compared with CAR-T cells, CAR-NK cells offer distinct advantages, including an improved safety profile, reduced systemic toxicity, and good tolerance to allogeneic NK cells. In addition to recognizing tumor surface antigens via single-chain antibodies to suppress cancer cells, NK cells can also inhibit tumor growth by recognizing various ligands through multiple receptors. Furthermore, NK cells are readily available from abundant sources and can be easily expanded under appropriate culture conditions, facilitating their broad clinical application.

Currently, several clinical trials of CAR-NK cell therapy for hematologic malignancies and solid tumors are underway.

TCR-T Therapy

TCR-T therapy involves introducing a gene encoding an artificial T-cell receptor (TCR) into T cells. This engineered TCR contains a specific sequence capable of recognizing the patient’s tumor, thereby replacing the natural TCR to mediate target cell recognition. TCR-T therapy can target any “non-self” protein, offering broader patient applicability. Its mechanism more closely mimics the natural TCR-dependent function of T cells, resulting in relatively lower toxicity and side effects.

Proteolysis-Targeting Chimeras (PROTACs) differ from traditional small-molecule inhibitors by employing an event-driven pharmacological mechanism—namely, target protein degradation—as opposed to the conventional occupancy-driven mode, which inactivates target proteins through binding.

Current PROTAC molecules predominantly utilize small-molecule E3 ligase binders and consist of three components: one end targets the protein of interest, the other binds to an E3 ubiquitin ligase, and the two are connected by a linker. PROTACs bring the target protein into proximity with the E3 ligase, thereby promoting ubiquitination of the target protein and directing it to the ubiquitin–proteasome degradation pathway, ultimately achieving degradation of the target protein.

Currently, only 10% of proteins can be modulated by small molecules, and another 10%, located extracellularly, can be regulated by macromolecules; the remaining 80% are considered undruggable. In contrast, while traditional targeted therapies require strong binding to target proteins, PROTACs only need weak binding to specifically tag them for degradation. Therefore, PROTACs can target proteins currently deemed undruggable.

To date, the degradation of proteins such as KRAS, BRD4, RIPK2, ERRα, BRD9, TBK1, Sirt2, CDK9, p38α, Pirin, c-Met, EGFR, FAK, and FLT3 has been reported using PROTAC technology.

In addition to their broad target spectrum, PROTACs exhibit higher selectivity due to their direct catalytic role in degrading target proteins. They can circumvent drug resistance arising from mutations and achieve high degradation efficiency at low compound concentrations, thereby potentially reducing drug toxicity.

Currently, Arvinas is the company making the most rapid progress in the PROTAC field. Its androgen receptor (AR) degrader, ARV-110, for the treatment of prostate cancer, has entered Phase I clinical trials, with subsequent candidates targeting the estrogen receptor (ER) and tau protein in development. Kymera Therapeutics’ protein degrader targeting IRAK4 was expected to initiate clinical trials in 2021. Other players in the industry include C4 Therapeutics, Captor Therapeutics, Nutrix, Cellida, Vividion, and Cullgen.

PROTACs remain in the early stages of development, with numerous challenges yet to be overcome, such as high molecular weight, poor druggability of the ternary complex, limited availability of E3 ubiquitin ligases, and off-target toxicity. Current exploration in the PROTAC field still focuses primarily on well-validated targets, such as AR and KRAS. Future products capable of degrading previously “undruggable” targets hold greater promise for becoming the next blockbuster drugs.

Antibody-drug conjugates (ADCs) are a class of targeted biologics composed of an antibody, a linker, and a cytotoxic drug. Upon binding of the antibody moiety to antigens on the surface of tumor cells, the ADC is internalized by the tumor cells and degraded in lysosomes, releasing active toxins that disrupt DNA or inhibit tumor cell division, thereby exerting a tumoricidal effect.

ADCs combine the specificity of antibodies with the potency of small molecules. Compared to traditional antibodies, ADCs theoretically offer superior efficacy by releasing highly potent cytotoxins within tumor tissues. Additionally, they exhibit fewer systemic side effects than chemotherapy and provide a wider therapeutic window.

Currently, there are 10 antibody-drug conjugates (ADCs) approved for marketing worldwide. Among them, the anti-CD30 ADC Adcetris and the anti-HER2 ADC Kadcyla have been approved in China. In 2020, Adcetris achieved global sales revenue of USD 1.06 billion, while Kadcyla reported sales revenue of CHF 1.745 billion. According to publicly available data, there are currently 119 ADC products in clinical development globally, with major targets including HER2, EGFR, TROP-2, PSMA, and CD19.

In the development of antibody-drug conjugates (ADCs), the selection of all three components is critical. Target selection and antibody quality determine the ADC’s affinity for tumor cells, the linker type dictates drug stability, and the choice of toxin determines both cytotoxic potency and side effects. ADC technology has now evolved to its third generation.

The first-generation drugs, represented by Mylotarg, utilized an unstable hydrazone linker, which led to excessive dissociation of the drug in serum, resulting in off-target effects and reduced efficacy.

Second-generation ADCs such as Adcetris and Kadcyla have undergone optimization in their antibody, linker, and toxin components. For instance, Kadcyla has previously demonstrated superiority over trastuzumab in head-to-head trials. Nevertheless, second-generation ADCs still rely on chemical conjugation, resulting in poor homogeneity of the drug-to-antibody ratio (DAR), which adversely affects pharmacokinetics and increases the risk of toxic side effects.

Third-generation ADCs benefit from advances in site-specific conjugation technologies, including ThioMab technology, ThioBridge technology, the incorporation of non-natural amino acids, and enzyme-catalyzed methods. These innovations confer greater homogeneity and enhanced in vivo stability to ADCs, thereby widening the therapeutic window.

Current novel conjugation technologies have opened up broader opportunities for antibody-drug conjugates (ADCs), while new types of payloads, such as PBD and SN-38, are increasingly being utilized in drug development, indicating that the ADC field is gaining strong momentum. In the future, broad-spectrum ADCs leveraging diverse target proteins or potent cytotoxic agents are also highly anticipated.

Gut microbiota has been a research hotspot in recent years, but no definitive results have been yielded over the past decade.

The success of three clinical trials of microbiome-based drugs in 2020 has reignited interest in treating diseases by modulating the gut microbiota.

Phase II trial data released by Finch Therapeutics in June demonstrated that its product delivers statistically significant clinical benefits: in the Phase II PRISM3 trial involving 206 patients, 74.5% of those with recurrent CDI who received a single dose of CP101 achieved sustained clinical cure by Week 8, representing a statistically significant improvement compared to 61.5% in the control group (p<0.05). Seres Therapeutics reported last August that SER-109, a purified bacterial spore formulation derived from fecal microbiota, met its primary endpoint in a Phase III clinical trial. Compared with placebo, treatment with SER-109 reduced the incidence of Clostridioides difficile-associated diarrhea by more than 30%, and Seres Therapeutics will submit a Biologics License Application (BLA) based on these results.

The aforementioned clinical trials successfully ignited enthusiasm in the capital markets. Finch Therapeutics announced the completion of a $90 million Series D financing round just three months after releasing its Phase II trial data. Meanwhile, on the day Seres Therapeutics disclosed its clinical trial results, its stock price surged by 389.22%.

In addition to leveraging gut microbiota for the treatment of conditions such as recurrent Clostridioides difficile infection, ulcerative colitis, and inflammatory bowel disease, numerous other indications are in early-stage clinical development, including asthma, rheumatoid arthritis, neurodegenerative diseases, and non-alcoholic steatohepatitis (NASH). Furthermore, research has revealed that certain microbes can induce, rather than stabilize, immune responses—a characteristic that may help enhance the efficacy of immuno-oncology (IO) therapeutics. In light of this, Bristol-Myers Squibb (BMS) has invested in the microbiome company Vedanta Biosciences and initiated Phase I trials evaluating combinations of microbiome therapies with its drug Opdivo. Merck & Co. has also partnered with 4D Pharma and Evelo Biosciences to assess whether selected microbial species can augment the effectiveness of its drug Keytruda.

In particular, the gut microbiota represents a vast reservoir of microbial species replete with diverse potential pharmacological mechanisms; regulatory approval and market launch of any product in this field would signal the opening of a massive market.

Ascendis Pharma

Viseon Therapeutics was established in 2018, with a commitment to becoming an expert in the field of endocrine-related treatments. The company aims to introduce globally leading therapies and pharmaceutical products into China, hoping to enable more Chinese patients to benefit earlier from advanced and reliable global treatment solutions. Viseon has obtained exclusive licensing rights for Ascendis’ endocrine therapy portfolio and will develop and promote this treatment regimen across Greater China (including mainland China, Hong Kong, Macau, and Taiwan).

Jiayin Bio

Founded in 2019, Jiayin Biologics is a pharmaceutical company with extensive GMP-compliant large-scale manufacturing capabilities in the field of gene therapy. Since its establishment, the company has achieved rapid growth, assembling a core team with comprehensive practical experience across R&D, process development, and manufacturing—a rarity among Chinese gene therapy firms. With deep technological reserves, Jiayin Biologics is poised to become an internationally recognized gene therapy company known for its innovation and influence. The company’s vision is to conquer intractable diseases by providing groundbreaking, one-time curative, safe, effective, and affordable gene therapies.

SM Biotech

Founded in Zhangjiang, Shanghai in 2016, Stemirna is a leading enterprise in China for mRNA therapeutics and advanced nano-formulation platforms. The company possesses proprietary innovative platforms for mRNA synthesis and LPP (Lipid-Polymer-Particle) nano-delivery, with its COVID-19 vaccine expected to be launched within 2021.

Linko Pharmaceuticals

Linka Therapeutics, established in 2017, is dedicated to the discovery and development of novel therapeutics for cancer, immune-mediated, and inflammatory diseases. The company was co-founded by seasoned drug R&D experts and executives from Pfizer, Merck, and Johnson & Johnson, who collectively bring over 70 years of extensive experience in drug discovery. Linka Therapeutics has successfully developed multiple first-in-class new drugs through independent R&D; in 2020, it completed regulatory filings for three clinical trials and successfully obtained clinical trial approvals in both China and the United States.

Keyue Pharma

Keyue Pharma, founded in 2017, is dedicated to developing complement-targeted therapies for the treatment of immune-mediated diseases. The company has developed a drug discovery platform, LOGIC, featuring unique humanized complement gene mouse models. This platform enables lead optimization using preclinical disease models to identify optimal targets, thereby overcoming various challenges in complement drug discovery. By employing rigorous and innovative approaches to modulate the complement system, Keyue Pharma aims to fundamentally improve the lives of patients with complement-mediated diseases.

InnoCare Pharma

Yinli Pharmaceuticals is an innovative drug company focused on the research and development of treatments for hematologic malignancies, solid tumors, and kidney diseases. Backed by a senior management team with international perspective and resources, and leveraging deep expertise in medicinal chemistry design and translational medicine, the company has developed highly original and mature first-in-class (FIC) and best-in-class (BIC) small-molecule drugs. Yinli Pharmaceuticals currently has three drug candidates in clinical stages, with multiple additional candidates expected to enter clinical trials within the next one to two years. Among these, its PI3Kδ inhibitor demonstrates superior efficacy and safety compared to other agents targeting the same pathway, and has received multiple certifications from both the U.S. Food and Drug Administration (FDA) and the National Medical Products Administration (NMPA). This product has entered into a collaboration with Hengrui Medicine in China, which also made a $20 million equity investment in Yinli Pharmaceuticals.

Bailisikang

Founded in Hangzhou, Zhejiang Province, in December 2017, Biologics is a clinical-stage biopharmaceutical R&D enterprise with independent intellectual property rights, co-established by multiple Ph.D. holders who returned to China after studying in the United States. The company focuses on the research, development, and industrialization of innovative biologics for oncology. Its core team boasts extensive experience in the successful development and commercialization of multiple products in this field, along with diverse technological platforms. Upholding its core value proposition of “Harnessing Collective Expertise to Safeguard Public Health,” Biologics collaborates closely with domestic and international biopharmaceutical companies to advance first-in-class (FIC) and best-in-class (BIC) innovative biologics with global competitiveness.

Icono

Aicon Biopharma is an innovative pharmaceutical company focused on developing first-in-class (FIC) or best-in-class (BIC) drugs. The company’s research centers on the “cell death–inflammation” axis, with a key focus on elucidating the mechanisms of regulated cell death in disease and assessing the druggability of associated targets. Aicon Biopharma has established a robust pipeline of independently developed products and has secured multiple patents in both China and the United States.

Baoyuan Pharma

Baoyuan Pharma, established in 2018, is an international, clinical-stage biopharmaceutical company focused on oncology, with operations in both China and the United States. Currently, Baoyuan Pharma is developing three oncology drug candidates in clinical stages. Among them, Taletrectinib (ROS1/NTRK), the most advanced candidate, is currently conducting Phase II single-arm registrational clinical trials in China and globally.

GenFleet Therapeutics

GenFleet Therapeutics was founded in 2017 by seasoned overseas-returnee drug development experts. Guided by unmet clinical needs and centered on disease biology and translational medicine, the company conducts in-depth research into the latest biological mechanisms in areas such as tumor signaling pathways, the tumor immune microenvironment, and immunomodulation, with a commitment to developing original, first-in-class global novel therapeutics.

Extreme Vision Biopharma

Jimu Bio is committed to becoming China’s leading ophthalmic enterprise, focusing on the development of breakthrough novel ophthalmic drugs with high commercial value. By strategically positioning itself in high-tech fields such as gene therapy and rare diseases, the company aims to address unmet clinical needs in ophthalmic care and lead the Chinese ophthalmic treatment market.

Changfeng Pharmaceutical

Changfeng Pharmaceutical is a high-tech, innovative pharmaceutical company integrating R&D, manufacturing, and sales, with a focus on the development of inhalation drug delivery technologies. Its R&D portfolio covers multiple therapeutic areas with significant clinical demand, including asthma, chronic obstructive pulmonary disease (COPD), and allergic rhinitis.

Aosikang

Ausco Biopharma is a global biopharmaceutical R&D, manufacturing, and service enterprise specializing in cell culture media and contract development and manufacturing organization (CDMO) services. Led by Dr. Luo Shun, its international team brings over two decades of hands-on experience from multinational pharmaceutical companies and has served more than 100 clients both domestically and internationally.

Shufang Pharmaceuticals