2021 China Healthcare and Wellness Services Industry White Paper: Serious Care, Consumer Medicine, and Digital Health All Present Strong Investment Opportunities

Excerpted from the 2021 iCapital China Health Industry White Paper – Medical and Health Services Section, published with authorization from VCBeat.

Preview of the main content:

1. What significant changes occurred in 2020?

2. Key Investment Themes and Market Outlook for 2021

3. Forecast of Investment Hotspots in 2021

4. 20 Companies Worth Watching

# Core Views:

1. China is facing unprecedented demographic shifts, with population aging and low fertility rates creating substantial demand for and challenges to healthcare resources as well as medical and elderly care services. Over the next decade, the “age-friendly” transformation of China’s healthcare service market will be the most critical theme, unlocking trillion-yuan incremental market opportunities. Today, China’s integrated medical and elderly care industry is still in its early stages, with business models gradually becoming clearer and more refined. In the future, numerous novel service formats and models will emerge, giving rise to new incremental markets and multi-dimensional market segmentation. This evolution will inevitably generate abundant investment opportunities suitable for capital market absorption and large-scale capital entry.

2. To accommodate this demographic shift, state purchasers underpinned by social security payments will inevitably carry through with volume-based procurement (VBP), Diagnosis-Related Groups (DRGs), and Big Data-based Disease Score Payment (DIP). Meanwhile, commercial health insurance, as an effective social supplement to basic medical insurance, will be elevated to a prominent position, thereby alleviating the insufficiency of coverage capacity within the public medical insurance system.

3. The long-standing constraints on the accessibility of high-quality medical services stem from the excessive concentration of premium healthcare resources. The COVID-19 pandemic in 2020 accelerated the development of internet-based healthcare and the tiered diagnosis and treatment system. For the first time, internet healthcare—previously limited to policy encouragement and online registration and consultation—was incorporated into the scope of medical insurance reimbursement. Recent regulations governing the operation of internet hospitals by physical hospitals, specifically the "Guiding Opinions on Actively Promoting Medical Insurance Payment for 'Internet+' Medical Services," will undoubtedly further boost the popularization of internet and mobile healthcare, thereby expanding both the accessibility and utilization efficiency of high-quality medical resources. In the future, healthcare services delivered via the internet and mobile networks will become an indispensable component of the traditional offline healthcare market.

4. China’s healthcare services sector is undergoing profound transformation driven by a technological revolution. The past year has been hailed within the industry as “Year One” of AI in healthcare. With the increasing issuance of Class III medical device certifications, a growing array of new healthcare services based on artificial intelligence, big data, 5G transmission, robotics, wearable smart devices, and intelligent informatics have not only enhanced the efficiency and accuracy of traditional healthcare delivery through technology-driven improvements, but also expanded the conventional boundaries of healthcare services. These innovations have extended service coverage to include healthy and sub-healthy populations, while accelerating the effective penetration of high-quality medical resources, expertise, and best practices into lower-tier markets. We anticipate that “digital healthcare,” which effectively integrates traditional clinical experience with technological innovation, will inevitably become a standard feature of China’s healthcare services market in the future.

5. Key sectors attracting capital focus in 2021 included:

· Specialized Medical Chain Services Group (Neurology Services Group, Dental Chain Services and Digital Enablement, Women’s and Children’s Health and IVF Services, New-Model Pediatrics, Ophthalmology, Medical Aesthetics, Elderly Care)

· Independent Third-Party Medical Center

· Commercial InsurTech

· AI Healthcare and Smart Hospitals

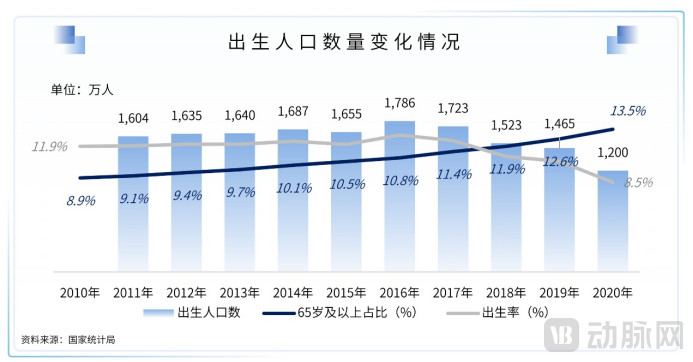

China is currently grappling with the concurrent challenges of a declining birth rate and an aging population, issues that are projected to intensify in the future. This trend is evident from two sets of data:

One indicator is the number of newborns. According to data released by the State Council, China’s annual number of live births has been declining since 2016, dropping from 17.86 million in 2016 to 12 million in 2020. Based on this trend, the number of newborns in 2021 is expected to decline further.

One group comprises the population aged 65 and above. Since China entered an aging society in 2000, the degree of population aging has continued to deepen. According to data from the Seventh National Population Census, the population aged 65 and above currently accounts for approximately 13.5% of the total population, a proportion that is expected to reach 14% shortly.

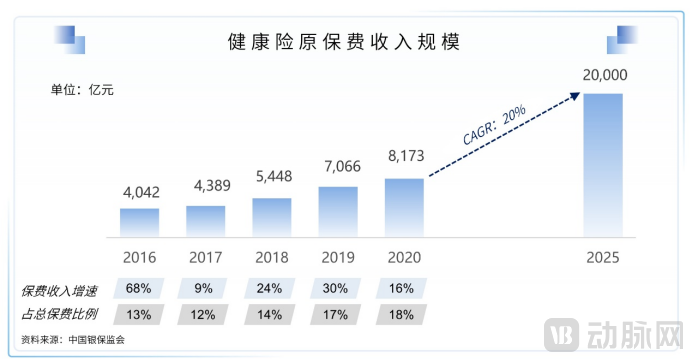

The health insurance market continues to expand in scale and is expected to surpass auto insurance in 2021 to become China’s second-largest insurance category. In 2020, health insurance premium income reached RMB 817.3 billion, accounting for 18% of total premium income, slightly below that of auto insurance, which recorded RMB 824.5 billion in premium income in 2020. However, the five-year historical compound annual growth rate (CAGR) for health insurance was as high as 19%, whereas the year-on-year growth rate for auto insurance in 2020 compared to 2019 was only 0.69%.

As a vital supplement to basic medical insurance, innovative commercial health insurance products are continually diversifying. Products such as specialty drug insurance and city-specific supplemental medical insurance (Huimin Bao) are facilitating the broader adoption of commercial health insurance. With the expanding market scale, commercial insurance is poised to become a key payer for enterprises in innovative pharmaceuticals and medical devices, mid-to-high-end medical services, digital therapeutics, and internet healthcare, thereby fostering a new ecosystem for China’s healthcare industry.

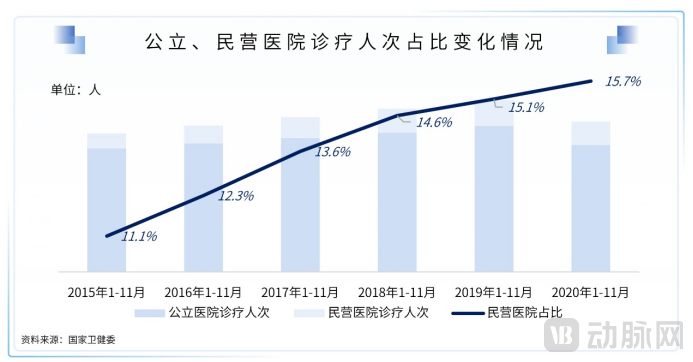

Post-pandemic, the public healthcare system has been addressing its shortcomings, while the private healthcare sector has been expanding, with its share of both the number of institutions and hospital beds continuing to rise.

Post-pandemic, the construction of the public healthcare system will be further strengthened, including the establishment of new public tertiary hospitals and specialized infectious disease hospitals, as well as the enhancement of primary healthcare service capabilities.

Meanwhile, private medical institutions have been developing at a faster pace, with the proportion of outpatient and emergency visits in private hospitals increasing from 15.1% during January–November 2019 to 15.7% during the same period in 2020. The number of non-public medical institutions rose from 439,862 in 2015 to 470,842 in 2019, while the number of public medical institutions declined from 543,666 in 2015 to 536,737 in 2019.

Meanwhile, the number of hospital beds in private medical and health institutions increased from 1.0753 million in 2015 to 1.9462 million in 2019, with a compound annual growth rate (CAGR) of 15.99%, whereas the CAGR for public medical and health institutions during the same period was only 3.67%; the proportion of hospital beds in private medical institutions relative to the total number of beds in all medical and health institutions has exceeded 22%.

Amid the continuous decline in the number of public medical institutions and constraints on bed capacity expansion, private medical institutions are expected to play an increasingly important role on the supply side of healthcare services in the future.

The pandemic has accelerated the development of internet hospitals, third-party laboratory testing, and pharmaceutical e-commerce.

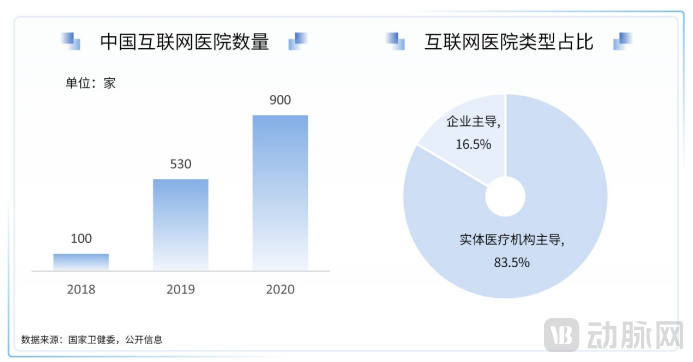

In 2020, driven by the impact of the pandemic, efforts to develop internet hospitals were significantly intensified. In 2018, there were only 100 internet hospitals in China; by the end of 2020, this number had exceeded 900. Notably, an increasing number of brick-and-mortar hospitals have chosen to establish an online presence, leveraging internet hospital platforms to serve a broader patient base. Currently, among existing internet hospitals, those led by physical medical institutions account for more than 80%.

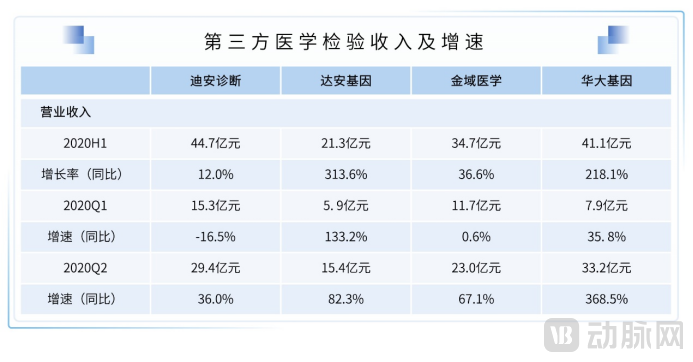

In 2020, the pandemic also spurred rapid growth in third-party clinical laboratory testing. Data show that by September 2020, nucleic acid tests conducted by independent clinical laboratories (ICLs) across China accounted for approximately 40% of the national total, representing a substantial share of nationwide testing capacity. Driven by the patient volume generated during the pandemic and the ongoing demand to strengthen grassroots testing capabilities, the market penetration rate of ICLs in China is expected to accelerate.

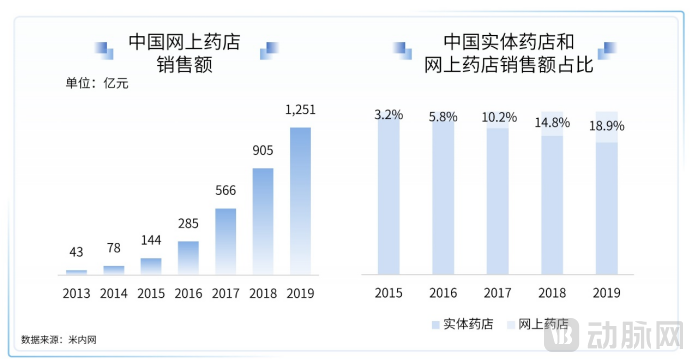

China’s online pharmacy sales grew from RMB 14.4 billion in 2015 to RMB 125.1 billion in 2019, representing a compound annual growth rate (CAGR) of 72%. Meanwhile, the share of online pharmacy sales rose to 18.9% in 2019. Online pharmacies have played a significant role in pharmaceutical retail. The pandemic has further cultivated consumers’ habit of purchasing medications online, and the importance of pharmaceutical e-commerce platforms and numerous internet hospitals as drug distribution channels is expected to strengthen in the future.

Consumer-driven healthcare services continue to grow at a rapid pace. Beyond the prominence of medical aesthetics, dentistry, ophthalmology, and mental health have become sustained hotspots in the industry.

In recent years, driven by national policy support encouraging private healthcare provision, as well as China’s large population base and growing consumer spending power and health awareness, consumer-oriented specialized medical services have experienced robust growth, gradually becoming a vital component of China’s healthcare resources.

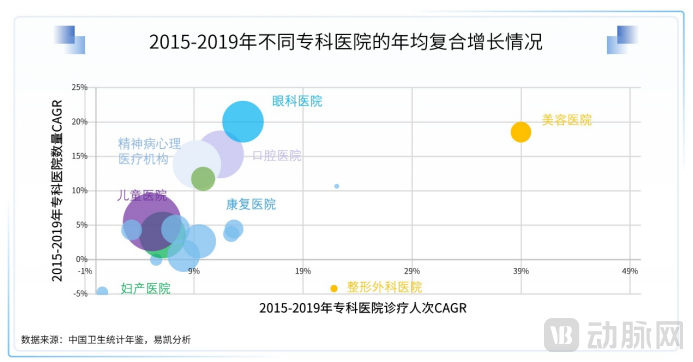

The number of specialized hospitals in China increased from 6,023 in 2015 to 8,531 in 2019, representing a compound annual growth rate (CAGR) of 9.09%; meanwhile, the number of patient visits to specialized hospitals grew from 277 million in 2015 to 386 million in 2019, with a CAGR of 8.65%.

Both in terms of the number of hospitals and patient visits, specialized hospitals have grown at a rate exceeding the overall average for all hospitals, ranking first among all hospital subcategories.

Based on the five-year historical growth rates across different specialty hospitals, medical aesthetic services have led the overall growth of specialty medical services. Both the number of medical aesthetic institutions and the volume of patient visits have maintained rapid growth, making it the most dynamic specialty field over the past five years.

However, in the field of plastic surgery, the number of patient visits has grown rapidly, with a growth rate exceeding 19%; yet the number of hospitals has seen negative growth, and the total number of institutions has declined. This is primarily due to heightened compliance requirements for medical aesthetic institutions. A significant volume of demand has shifted toward leading compliant providers, while non-compliant institutions have faced closures amid stricter regulatory oversight.

Furthermore, ophthalmology, stomatology, rehabilitation, and psychiatry/psychology have all been specialty areas with rapid growth in recent years. We have observed that the number of hospitals in these fields has maintained a rapid growth rate, exceeding 10%; meanwhile, the growth in the number of hospitals has outpaced the growth in patient visits, indicating that the expansion of medical service supply has been faster than the growth in demand.

The Epidemic Poses Short-Term Challenges to Offline Medical Service Providers, While Benefiting Leading Companies Across Various Sectors in the Long Run

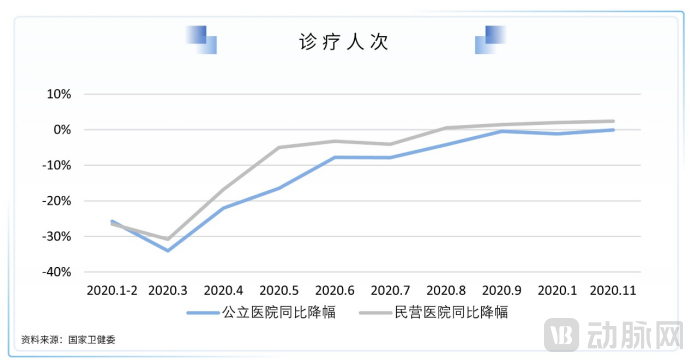

In early 2020, the COVID-19 pandemic significantly impacted offline healthcare service providers. Data released by the National Bureau of Statistics showed that outpatient and inpatient visits at public and private hospitals decreased by nearly 30% year-on-year in the first quarter, gradually recovered thereafter, and returned to growth by the end of the year.

According to the financial reports of healthcare groups listed on the Hong Kong Stock Exchange and China’s A-share market, the pandemic had the most severe impact in the first quarter. Factors such as delayed openings, restrictions or reductions in patient admissions, and constraints on surgical services adversely affected performance. As a result, Aier Eye Hospital and Topchoice Medical reported year-on-year revenue declines of 27% and 51%, respectively, in the first quarter. Conditions gradually improved starting in the second quarter, with business revenue achieving year-on-year growth by the third quarter.

Meanwhile, we found that large-scale chain institutions with a wide geographic distribution were relatively less affected; in contrast, smaller medical groups with concentrated institutional footprints suffered greater impacts from the pandemic.

The pandemic has also accelerated industry consolidation, with small, standalone private medical institutions exiting the market due to their weak risk resilience. Leading institutions have not only recovered rapidly from the pandemic but are also poised to capture demand released by competitors’ exit, thereby further expanding their scale and strength.

The pandemic hindered in-person medical visits, leading to a surge in demand for internet healthcare and further gaining recognition from all sectors.

The pandemic hindered personnel mobility and offline medical visits, leading to a surge in demand for online consultations and medication purchases, which drove rapid business growth for various internet healthcare companies. During the peak of the pandemic, the Ping An Good Doctor app recorded over 1.11 billion visits, with new registered users reaching ten times the pre-pandemic level and the average daily number of consultations by new users rising to nine times the pre-pandemic figure. In the first half of 2020, JD Health’s annual active users and gross merchandise volume (GMV) increased by 35.5% and 71.2%, respectively, year on year.

Internet-based healthcare is gaining wider acceptance among doctors and patients, and the government has introduced policies to support its development. In the future, further deregulation will continue to drive rapid industry growth.

Sudden Events Strain Medical Resources, Highlighting the Role of Third-Party Medical Services

In the early stages of the outbreak, in response to the shortage of testing capabilities, various in vitro diagnostic (IVD) companies rapidly developed detection products for the novel coronavirus, thereby providing the instruments and materials necessary for subsequent large-scale screening.

Amid sporadic resurgences of the epidemic and the emergence of asymptomatic cases, large-scale screening has been carried out across various regions. The short-term, concentrated influx of a large volume of samples has tested local testing capacities, in which third-party medical laboratories have played a significant role and continue to provide nucleic acid testing services to the public.

According to the financial reports of listed companies, third-party medical testing firms experienced a decline in performance during the first quarter, followed by rapid growth in the remaining quarters. The Chinese government has repeatedly issued documents emphasizing the integration of third-party medical testing capabilities, explicitly stating that “provinces may procure services through cooperation with qualified third-party testing institutions.” Furthermore, in the revised recommendations for the Classification and Codes of Health Institutions (Organizations) released by the Statistical Information Center of the National Health Commission, categories and codes for medical testing laboratories and pathology diagnosis centers were added, thereby providing further institutional support for the development of third-party medical service providers.

Successive Approvals of Class III Medical Device Certificates for AI-Based Medical Imaging Products Mark 2020 as the Inaugural Year of Commercialization for Medical Artificial Intelligence

In January 2020, Keya Medical’s software for calculating coronary fractional flow reserve (FFR) was approved by the National Medical Products Administration (NMPA) as a Class III medical device, marking the first Class III certification granted to an AI-based medical product.

In June, Ande Medical Intelligence’s brain MRI intracranial tumor product received the first Class III medical device certification for AI-assisted diagnosis. Subsequently, Class III certifications for AI products targeting multiple anatomical sites—including orthopedics, ophthalmology, and pulmonary nodules—from various companies were approved in succession. This policy breakthrough also ignited a surge in the capital market, with leading companies securing substantial financing and launching commercialization efforts.

Healthcare Insurance Reform and Cost Control Proceed in Tandem, with Commercial Insurance and Diversified Payment Models Taking Center Stage

In 2020, various national ministries and commissions introduced a series of policies to promote cost containment in medical insurance and establish a diversified payment model integrating basic medical insurance with commercial health insurance.

The “Opinions on Deepening the Reform of the Medical Security System” issued in March 2020 serves as the top-level design for medical insurance reform. Under the overall “1+4+2” framework, it aims to enhance the operational efficiency of medical insurance funds and meet the public’s basic needs for healthcare security through measures such as expanding revenue sources, controlling expenditures, and implementing refined management. Meanwhile, it establishes commercial health insurance as an important supplement to basic medical insurance. Subsequent policies have also encouraged the development of long-term care insurance.

Healthcare insurance reforms are also underway, exploring more refined, composite, and diversified payment methods under the existing global budget prepayment system. These primarily include Diagnosis-Related Group (DRG)-based payment, regional point-based global budgeting, and Disease Intervention Packet (DIP)-based payment.

On June 18, the issuance of the "Notice from the Office of the National Healthcare Security Administration on Printing and Distributing the Sub-grouping Scheme for China Healthcare Security Diagnosis-Related Groups (CHS-DRG) (Version 1.0)" signaled that the pilot program for DRG-based payment was about to officially enter the implementation phase. Meanwhile, in 2020, the pilot program for Big Data Diagnosis-Intervention Packet (DIP) payment was launched, running parallel to the DRG payment pilots. The promotion of both DRG and DIP has imposed requirements and presented challenges regarding hospitals’ refined management, the improvement of medical record quality, and the enhancement of information technology infrastructure. At the same time, it has created market opportunities for the further expansion of commercial health insurance.

Centralized Drug Procurement to Become the New Normal

In 2020, China launched the second and third rounds of national centralized drug procurement, with 32 drugs selected in the second round and 55 in the third. The average price reduction for drugs in the third round was 53%, with a maximum reduction of 97%. Currently, the fourth round of centralized drug procurement has also begun, covering 45 varieties, signaling that centralized drug procurement has become normalized.

The three rounds of national centralized drug procurement covered a total of 112 pharmaceutical products, generating annual savings of approximately RMB 53.9 billion based on the agreed purchase volumes. The implementation of centralized drug procurement has created fiscal space to enhance the coverage capacity of medical insurance and to increase the service-based income of healthcare professionals. Meanwhile, it has accelerated the innovative transformation of pharmaceutical companies and the restructuring of the pharmaceutical distribution supply chain.

Establish Standards for Integrated Medical and Elderly Care Services to Proactively Address Deep Population Aging

On December 31, 2019, the National Health Commission of China released the Guidelines for Services in Integrated Medical and Elderly Care Institutions (Trial), establishing official standards for integrated medical and elderly care services. The Guidelines were formulated by the National Health Commission, the Ministry of Civil Affairs, and the National Administration of Traditional Chinese Medicine, requiring local integrated medical and elderly care institutions to refer to the Guidelines to standardize service delivery and effectively improve the quality of integrated medical and elderly care services.

On December 27, 2019, the State Administration for Market Regulation and the Standardization Administration of China officially released the mandatory national standard Basic Specifications for Service Safety in Elderly Care Institutions (hereinafter referred to as the “Specifications for Elderly Care Institutions”), which will come into effect on January 1, 2022. This is the first mandatory national standard in China’s elderly care service sector, and it will help prevent safety hazards in the services provided by elderly care institutions, maximize the protection of the personal health and life safety of older adults, and continuously standardize and improve the quality of services in these institutions.

On December 19, 2020, the National Health Commission released the *Guidelines for Contractual Cooperation between Medical and Health Institutions and Elderly Care Service Institutions (Trial)*, proposing that elderly care service institutions may select prospective medical and health partners based on principles such as “proximity and convenience” and “matching services to needs.” The specific content of medical and health service cooperation and associated funding shall be determined through mutual consultation and agreement. Elderly care service institutions are encouraged to prioritize contractual cooperation with nearby primary medical and health institutions, as well as with continuing care facilities providing rehabilitation, nursing, and palliative care services. On December 31, the General Office of the State Council issued the *Opinions on Promoting the Healthy Development of Elderly and Childcare Services*, further calling for the improvement of the basic elderly care service system and the expansion of service capacity and outreach of township nursing homes. The introduction of these policies helps promote standardized operations of elderly care service institutions and enhance their service capabilities.

Frontier technologies such as artificial intelligence, big data, and 5G are deeply empowering medical services, making smart healthcare the new favorite.

During the COVID-19 pandemic, various cutting-edge technologies were integrated with healthcare services across diverse scenarios to support epidemic control efforts, allowing the public to experience the convenience brought by smart healthcare. Examples include telemedicine and online consultations based on the “Internet+” model; health codes powered by big data; and AI-based applications such as intelligent interpretation of medical images and computer-aided diagnosis.

Frontier technologies represented by artificial intelligence, big data, and 5G are gradually transforming traditional healthcare service models, with smart healthcare emerging as a new favorite.

“Class III Certification” Debut Boosts Imaging AI Development, Pressing the Fast-Forward Button on Commercialization

In January 2020, the long-awaited first Class III medical device certificate for a medical AI product in China was issued. In the following months, products such as coronary flow reserve fraction calculation software, ECG analysis software, MR imaging-assisted diagnostic software for intracranial tumors, fundus image-assisted diagnostic software for diabetic retinopathy, coronary CT angiography image-assisted triage software for vascular stenosis, CT imaging-assisted detection software for pulmonary nodules, and intelligent CT fracture analysis systems successively obtained Class III registration certificates from the NMPA. The industry’s focus began to shift from R&D to commercial implementation.

As a result, AI imaging companies have attracted significant attention in the capital markets, with frequent financing rounds. From the perspective of clinical application, the development of AI has greatly alleviated the severe mismatch between supply and demand for resources in the medical imaging field. Particularly during the COVID-19 pandemic, AI imaging technology was effectively applied to the screening and diagnosis of individuals infected with the novel coronavirus.

CDSS Development Is Timely Under the Rating Policy: Opportunities and Challenges Coexist

Since the National Health Commission launched initiatives in 2018 to further advance hospital informatization centered on electronic medical records, the rigid demand for Clinical Decision Support Systems (CDSS) among healthcare institutions has increased substantially, thereby strongly promoting the development of the CDSS industry. The widespread adoption of CDSS has also enhanced the level of informatization in hospitals to a certain extent, playing a positive role in reducing clinical misdiagnosis and missed diagnosis rates, minimizing medical deviations, and improving clinical standardization.

However, in terms of actual clinical application, CDSS still faces many challenges that need to be overcome, such as the natural resistance from senior physicians, the professionalism and authority of CDSS knowledge graphs, and how systems can be reasonably integrated into the diagnosis and treatment process. To address these issues, new highlights emerged in the development of CDSS in 2020, including customization (such as combining national standards for the diagnosis and treatment of related diseases like VTE and single-disease quality control with the hospital's own clinical characteristics and habits), specialization (in cardiology, intelligent risk assessment for atrial fibrillation, risk prediction and prevention for acute kidney injury (AKI)), and CDSS products tailored for primary healthcare institutions.

Overall, the development of CDSS is still in a phase of exploratory trial and error, with opportunities and challenges coexisting.

Broad Prospects for the Application of Medical Big Data, Yet a Relatively Weak Development Foundation

In the early stages of the COVID-19 outbreak, one of the greatest challenges in epidemic prevention and control was the lag inherent in the national web-based direct reporting system for infectious disease outbreaks.

In the direct reporting system, the flow of epidemic data relies on manual entry by clinicians, which limits timeliness and is susceptible to human interference. Therefore, it is particularly important to establish mechanisms for pre-event early warning, real-time monitoring during events, and post-event traceability within the disease control system, where medical big data can play a significant role.

In addition, medical big data can be widely applied in various fields, including clinical research, hospital operational management, medical quality control and regulation, health insurance cost containment, and pharmaceutical R&D and marketing. However, the development of medical big data in China is still in its infancy. Disparate data standards across different hospital information systems hinder the effective utilization of medical big data. Unified data governance for these diverse systems is time-consuming, labor-intensive, and technically challenging, thereby impeding the implementation of medical big data application scenarios. In light of this, achieving standardization and structuring of hospital data has become a key objective of current informatization initiatives.

Policy-Driven Development: Large Healthcare Groups Build HMO Models with Chinese Characteristics

In 2020, the second year of the three-year grace period for the “divestiture” of state-owned enterprise (SOE) hospitals, the acquisition pace of major central SOE healthcare groups slowed slightly compared to the previous year due to the impact of the pandemic. Nevertheless, regional healthcare groups have begun to take shape. Several healthcare groups, including Sinopharm Healthcare, China Resources Healthcare, General Technology Healthcare, Gemflower Healthcare, and New Milestone Healthcare, now each operate more than 10,000 hospital beds, covering multiple provinces, cities, and autonomous regions across China.

As the reform of state-owned enterprise (SOE) hospitals accelerates further, large-scale national healthcare groups backed by central state-owned enterprises are poised to emerge in the near future, becoming a vital component of China’s healthcare service system.

We also look forward to seeing whether these institutions can forge a HMO model with Chinese characteristics, built upon an extensive medical network and integrated with the public health insurance system.

Capital Markets Are About to Welcome New Players in Healthcare Services

In the A-share market, thanks to the introduction of the registration-based IPO system on the ChiNext Board, private hospitals have become eligible for initial public offerings (IPOs). In July 2020, Huaxia Eye Hospital, Purui Eye Hospital, and He’s Eye Hospital successively submitted their ChiNext IPO applications. In the Hong Kong stock market, Hygeia Healthcare, China’s largest specialized oncology hospital group, successfully completed its IPO in June 2020 and achieved a significant market premium.

In the primary market, Bang’er Orthopedics, Shulan Medical, Sanbo Brain Hospital, and Lu Daopei Hospital have all completed Pre-IPO financing rounds and established clear IPO plans. Investment institutions are also increasingly focusing on specialized subfields with high entry barriers and growth potential, such as neurology, hematology, and orthopedics.

We look forward to the next A-share listed private hospital following Aier Eye Hospital.

Policy Guidance Drives Further Adjustment of Drug Pricing System, Intensifying Restructuring Across All Segments of the Pharmaceutical Commercial Supply Chain

In 2020, centralized drug procurement became normalized, significantly compressing profit margins in the hospital-side drug distribution channel. Guided by policies aimed at controlling medical insurance expenditures, the proportion of drug costs in hospital spending further declined, intensifying transformations across pharmaceutical retail, distribution, and marketing sectors.

In the pharmaceutical retail sector, the outflow of prescriptions is advancing steadily, with off-hospital retail terminals making in-depth strategic deployments and innovations in prescription fulfillment, drug categories, and services. Regarding prescription fulfillment, as online incremental prescriptions from enterprise-led internet hospitals remain limited and are not yet covered by medical insurance payments, the outflow of prescriptions continues to be dominated by existing prescriptions from public hospitals. Consequently, pharmacy stores adjacent to hospitals and Direct-to-Patient (DTP) pharmacies, serving as the primary terminals for the outflow of paper-based prescriptions from hospitals, have become key focus areas for active deployment by chain pharmacies, innovative internet healthcare platforms, and pharmaceutical companies. Meanwhile, prescription sharing platforms, which represent the main model for the outflow of electronic prescriptions from hospitals, are still in a phase of regional exploration. Some chain pharmacies with strong operational foundations and high regional coverage have begun piloting collaborations with regional prescription circulation platforms affiliated with hospitals.

Furthermore, prescription review is an indispensable component in facilitating the outflow of prescriptions from hospitals. Various stakeholders choose either on-site prescription review or a hybrid model combining on-site and remote review, based on their operational needs and cost considerations; however, remote prescription review has not yet received explicit policy endorsement.

Pharmaceutical Marketing: Deep Empowerment by New Technologies Drives Precision and Efficiency

Against the policy backdrop of healthcare insurance cost-containment driving a restructuring of drug pricing systems, pharmaceutical companies’ profit margins can no longer sustain the traditional, extensive drug marketing model. In 2020, it became frequent for entire marketing teams for specific drug categories to be laid off, and for regional contract sales organizations (CSOs) to go bankrupt or be acquired. In this process, the sharp decline in the number of medical representatives has become the most direct manifestation of the transformation in the pharmaceutical marketing system.

Amid declining profits and intense regulatory pressure, pharmaceutical companies must pursue marketing strategies that are compliant, refined, and efficient. Two emerging trends in pharmaceutical marketing are expanding reach to grassroots healthcare providers and digitizing pharmaceutical marketing. In real-world clinical settings, grassroots physicians face significant patient heterogeneity, leading to highly personalized needs and a diverse range of challenges. To address these issues, some companies are integrating big data and artificial intelligence to develop physician-centric medical knowledge graphs that encompass drugs, diagnostics, materials, surgical procedures, and more. These tools enable pharmaceutical companies to achieve broader and more efficient coverage, facilitate more effective transmission of professional information between new drugs and key opinion leaders (KOLs), and help grassroots physicians access the same specialized expertise as KOLs with greater efficiency.

Furthermore, in solutions tailored for pharmaceutical companies, building a data middle platform that supports multiple core departments not only empowers medical representatives but also enables business-related functions such as Marketing and Medical Affairs.

Diversified Payment Models Spawn City-Specific Insurance and Specialty Drug Coverage, Setting the Trend

In January 2020, the China Banking and Insurance Regulatory Commission (CBIRC) and twelve other departments jointly issued the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” which explicitly stated: “Strive to expand the commercial health insurance market to exceed RMB 2 trillion by 2025, making it an important component of China’s distinctive healthcare security system.” From January to November 2020, premium income in the health insurance segment reached RMB 764.1 billion, indicating substantial growth potential over the next five years.

In recent years, commercial health insurance products, ranging from corporate supplemental medical insurance to high-limit medical insurance, have remained in an exploratory phase. In 2020, the most notable commercial insurance products were city-specific supplementary medical insurance and specialized drug insurance. Specialized drug insurance focuses on areas with the highest out-of-pocket burdens and the most critical needs, such as oncology and rare disease medications not covered by social security. It shifts away from the traditional post-service reimbursement model of medical insurance, adopting instead a direct payment-in-kind approach. This involves negotiating and settling prices directly with the supply chain, while commercial insurers define the drug formulary to provide specific coverage for medications excluded from the national medical insurance catalog.

Specialty Drug Insurance has achieved a breakthrough in bridging the link between commercial insurance and the pharmaceutical industry, marking a turning point in the development of commercial health insurance. In the realm of city-specific insurance, products such as Huimin Bao, Shimin Bao, and Quanmin Bao—various exclusive insurance schemes named after cities—are priced at under RMB 100. These plans are positioned to provide affordable coverage for critical illnesses, focusing on alleviating the social issue of poverty caused by medical expenses.

City-backed insurance, endorsed by the government, mobilizes social resources to generate additional individual funding outside the social security system, thereby expanding the risk pool for critical illness coverage. In terms of scope, it generally extends beyond in-network medical expenses to include an out-of-network drug formulary, marking a significant step forward in the coverage and management of non-reimbursable costs. Furthermore, instead of the traditional fee-for-service reimbursement model, this coverage adopts a benefit-in-kind approach similar to specialized drug insurance. This not only alleviates the financial burden and accessibility challenges faced by patients with serious illnesses but also reintegrates the core principles of health insurance by establishing dedicated drug formularies and pharmacy networks through integration with the pharmaceutical industry, representing a crucial advancement in managing out-of-pocket healthcare expenses.

In 2020, the capital market for serious healthcare services experienced heightened activity, with a pronounced divergence between leading and mid-tier players, underscoring the sector’s high value, high barriers to entry, and scarcity.

In 2020, amid the pandemic, the number of financing transactions in the specialized medical services market increased rather than decreased. Leading specialty healthcare groups, represented by Sanbo Brain Hospital, Lu Daopei Hospital, Meizhong Jiahe, and Shulan Healthcare, continued to attract significant capital attention, accounting for one-third of the total transaction value in the services sector.

However, investors have adopted a markedly more cautious stance toward mid-tier deals, underscoring the characteristics of high-quality, serious medical service assets: long cultivation cycles, significant challenges, and high value.

High expectations in the secondary market are feeding back into the primary market, and the capital market will continue to deepen the momentum in the serious medical services sector in 2021. Leading institutions such as Sanbo Brain Hospital will successively list on the A-share market. It is expected that 2021 will be a year when the IPO window opens for medical services, which will undoubtedly inject new vitality into the financing environment for the medical services track in the primary market.

The 14th Five-Year Plan, released in March 2021, identified frontier fields such as brain science as key areas of focus. National policies encouraging rigorous medical practices and cutting-edge technological projects will further drive the development of the professional healthcare services industry.

In 2020, impacted by the pandemic, capital market enthusiasm for consumer healthcare waned, with a significant decline in the total number of transactions compared to 2019. The average financing amount per transaction in 2020 remained largely consistent with the historical average deal size in this sector.

From the perspective of market characteristics, specialty chains with distinct disciplinary features demonstrate significantly better financing performance than general practice chains. The market continues to focus on sectors such as dentistry, ophthalmology, child psychology, pediatrics, and medical aesthetics.

For instance, Invisalign, a star orthodontic product in dentistry, has built high disciplinary barriers through multiple patents and its own aesthetic and portable features, dominating the fiercely competitive consumer healthcare industry. Similarly, Little Apple Pediatrics, which focuses on the niche segments of pediatric endocrinology and growth and development, has achieved rapid growth and overtaken competitors, surpassing general pediatric clinics.

The opening of national policies and the simplification of approval processes for medical service institutions have provided a favorable external environment for the third-party medical services outsourcing market. The National Health Commission has successively issued licenses for ten types of medical service institutions, including medical laboratory testing centers, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, hospice care centers, rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers.

Capital market enthusiasm for the third-party medical services sector continues to rise. Third-party independent medical institutions, guided by specialized hospital division of labor and aimed at enhancing the overall allocation efficiency of medical resources, represent a significant trend. From the early outsourcing of hospital informationization to the emergence of independent third-party medical laboratory testing, large-scale transformation in the supply of in-hospital services and third-party operations have become imperative. The number of financing cases increased steadily from 2018 to 2020, with financing scales expanding continuously.

Yi Kai believes that third-party independent medical institutions possessing the four characteristics of standardizability, economies of scale, high entry barriers, and replicability will be highly sought after by the market. Such institutions can not only achieve better quality control but also facilitate resource sharing, reduce hospital costs, and improve efficiency. Furthermore, they can build a complete upstream and downstream industry chain, thereby enhancing industry competitiveness.

The continuous improvement of hospitals’ demands for safety compliance, medical quality, and management efficiency is the fundamental driver behind the sustained development of digital healthcare.

In terms of policy, the Chinese government is increasing its support for digital healthcare. The implementation of initiatives such as the “Healthy China 2030” plan, “Internet + Healthcare,” medical big data management standards, and tiered assessments for electronic medical records, smart services, and smart management will lay a solid foundation for the digital healthcare ecosystem. Meanwhile, performance evaluations of public hospitals at tertiary, secondary, and primary levels, along with reforms such as the “Two-Invoice System” and the zero-markup policy, have created an imperative need for intelligent upgrades in hospitals.

From a technological perspective, the deployment of 5G networks and the increasing maturity of Internet of Things (IoT) technology have significantly reduced management and maintenance costs. The approval and promotion of AI-powered medical devices, along with the digitalization and intelligent transformation of hospitals, will usher in a new round of iterative upgrades for traditional healthcare.

Regarding the pandemic, data from Boston Consulting Group shows that before the outbreak, approximately 170 public hospitals in China offered internet hospital services. By May 2020, in the post-outbreak period, this number had reached 1,000. Meanwhile, the pandemic also catalyzed the rapid growth of sectors such as transport robots, disinfection robots, and remote diagnosis and treatment.

The digital transformation of traditional healthcare is directly reflected in a significant improvement in hospital management quality and operational efficiency. The development of the Hospital Internet of Things (HIoT) has given rise to innovations such as intelligent patient triage, digital wards, and digital pharmacies, which have substantially reduced labor costs and enhanced the management efficiency of traditional hospitals. The emergence of internet hospitals has achieved a seamless integration between offline medical institutions and online platforms, fostering complementary synergy and maximizing resource utilization. Digital diagnostic technologies, such as AI-based medical imaging and AI-assisted diagnosis, continue to advance and have been successfully integrated into traditional medical practices, significantly improving the accuracy of diagnoses and operational efficiency.

With social development and the continuous improvement of people’s living standards, Chinese citizens’ willingness and ability to spend on healthcare are steadily rising. However, China’s population is aging at an accelerating pace, with the proportion of those aged 65 and above projected to reach approximately 17% by 2030.

The growing elderly population has further accelerated the rise in healthcare expenditures, resulting in a slower growth rate of medical insurance revenues compared to expenditures. This widening gap between income and outlays has intensified financial pressure on China’s basic medical insurance system. Against this backdrop, the Chinese government is vigorously supporting the development of commercial health insurance. For instance, the “Basic Healthcare and Health Promotion Law,” issued by the Standing Committee of the National People’s Congress in June 2020, explicitly outlines policies encouraging the growth of commercial health insurance. In the United States, claims payments from commercial health insurance account for as much as 37% of total healthcare spending, whereas in China this proportion remains below 5%, indicating substantial future market potential for commercial health insurance in China.

In recent years, MGA and TPA companies in China have experienced robust growth. Leveraging SaaS platforms, these firms are accelerating the integration of the entire upstream and downstream industry chain. For instance, Nanyan Insurance Technology completed its acquisition of the TPA service provider Medilink-Global, aiming to integrate the industrial supply chain and seek higher profit margins.

The maturation of the commercial health insurance industry has also bolstered the high-end clinic sector. Direct billing through commercial insurance offers convenience to more high-income individuals, channeling their attention toward high-end clinics. Meanwhile, some high-end clinics are actively expanding into Third-Party Administrator (TPA) services, driving TPA involvement toward the mid-stream and front-end stages of clinical care.

Serious medical care features high technical barriers and substantial market demand. Healthcare service assets represented by this sector will be a major hotspot pursued by the capital market in 2021, with scarce assets such as specialized medical groups remaining the value anchor of China’s healthcare service industry. We believe that sub-sectors likely to become investment hotspots in 2021 include:

Oncology

In June 2020, Hygeia Healthcare Group listed on the Hong Kong Stock Exchange. Since its listing, its share price has nearly tripled, and its market capitalization has exceeded HK$30 billion, demonstrating strong market performance. Additionally, V-Daopei Medical Group, specializing in hematology and oncology, and Shulan Healthcare Group, characterized by its “specialized-focused, general-complementary” model, have both secured multiple rounds of financing. This indicates that, against the backdrop of intense competition in innovative oncology drugs, large healthcare groups with high technological barriers and specialized competitive advantages—being scarce assets in the capital markets—will continue to be highly sought after by investors, with a more pronounced head effect.

Neurology

Neurological disorders are among the most technically complex medical conditions, and neurology is often regarded as a discipline at the pinnacle of medicine, characterized by exceptionally high professional barriers. Due to factors such as the lengthy training period required for neurologists, the number of neurologists per capita in China is significantly lower than that in developed countries, resulting in a severe supply shortage. Consequently, high-quality neurological healthcare assets have gained substantial recognition from the capital market. In March 2020, Donglei Brain Hospital secured RMB 80 million in Series B financing, and in May 2020, Sanbo Brain Hospital raised over RMB 800 million in its Series B round, fueling heightened interest in the neurology sector. Sanbo Brain Hospital submitted its IPO application to the ChiNext board in early 2021, and its listing is expected to draw significant market attention to this specialized segment.

Cardiovascular Medicine

The prevalence of cardiovascular disease (CVD) in China continues to rise. In 2019, the estimated number of prevalent CVD cases reached 330 million. Meanwhile, CVD remains the leading cause of death, accounting for two out of every five deaths. In recent years, digital technologies—such as AI-based imaging—have become closely integrated with cardiovascular care, complementing each other and significantly improving the efficiency and coverage of diagnosis and treatment. The fact that companies like Hong Kong Asia Medical and Shukun Technology have secured multiple rounds of financing has further bolstered market confidence in this niche sector.

Healthcare service assets, represented by serious medical care, enjoy higher valuation premiums in the capital market due to their strong resilience against risks and economic cycles, the certainty of their development prospects, and their steady growth. Leveraging a large population base, each subsector harbors substantial unmet demand, creating the potential for the emergence of large, leading healthcare groups. Some segments have not yet fully blossomed, constrained by factors such as the healthcare system, payment mechanisms, and medical technology; it is hoped that technological innovation will unlock more opportunities in the future.

With the growth of per capita disposable income and heightened health consumption awareness among residents, consumer-oriented chain medical groups have become a hot investment focus in the capital market in recent years.

Dentistry

As the only listed dental chain medical group on China’s A-share market, Topchoice Medical has seen its stock price surge since early 2019, with its market capitalization exceeding RMB 70 billion, demonstrating remarkable market performance.

With Topchoice Medical as the benchmark, various dental chain hospitals have demonstrated outstanding performance in recent years. For instance, Sunny Dental, a chain institution hailed as the leader in digital orthodontics in China, completed a Series A financing round worth hundreds of millions of yuan; Smartee Dental, which developed the Smartee clear aligner technology with independent intellectual property rights, completed a Series C financing round worth hundreds of millions of yuan; and Fissen Technology, a comprehensive provider of digital dental solutions, also completed a Series C financing round worth hundreds of millions of yuan.

Among the various segments of dentistry, orthodontics stands out as one of the markets with the greatest potential, characterized by high demand, high average transaction value, strong customer retention, and scalability, promising robust future growth. Meanwhile, the market penetration of premium products such as Invisalign, coupled with the integration of AI technologies (e.g., 3D printing) into orthodontic practices, will undoubtedly inject greater vitality into this sector.

Ophthalmology

In China, over 600 million people suffer from refractive errors, making it one of the most prevalent ophthalmic conditions and a core demand driver in the eye care market. The emergence of products and technologies such as orthokeratology (OK) lenses, femtosecond laser surgery, and implantable collamer lens (ICL) implantation has further deepened the development of refractive error correction services. Represented by Aier Eye Hospital, whose stock price has surged since its listing with a market capitalization exceeding RMB 230 billion, the overall ophthalmic market has been strengthened. The simultaneous IPO bids by three chain eye hospital groups—Huaxia Eye Hospital, Purui Eye Hospital, and He’s Eye Hospital—have kept this segment highly active in 2021.

Pediatrics

Amid China’s nationwide implementation of the two-child policy and a severe shortage of pediatricians per capita, the healthcare needs of pediatric patients remain inadequately met. Growing parental anxiety has intensified demand for high-quality, service-oriented pediatric care, creating substantial market opportunities for Chinese healthcare institutions.

Over the past year, Kyoto Children's Hospital, the largest non-public tertiary pediatric specialty hospital in China; Damai and Xiaomi, a rehabilitation platform for children with autism; Little Apple Pediatrics, an internet healthcare platform; and Weino, a high-end domestic pediatric chain institution, have all garnered significant favor from numerous investors.

Medical Aesthetics

In recent years, the primary drivers of growth in the medical aesthetics industry have been the domestic substitution on the supply side, the expansion of consumer age demographics, and market penetration into lower-tier regions. As consumer awareness of medical aesthetics has improved, pricing for procedures has become more transparent and market-driven. The enhanced value of medical services has strengthened the bargaining power of institutions, further sustaining the industry’s robust development. Compared with surgical cosmetic procedures, which are characterized by low frequency, high cost, and high entry barriers, non-surgical medical aesthetics (often referred to as “light” medical aesthetics) have become a key catalyst for industry expansion, leveraging their attributes of high frequency, premium pricing, standardizability, and lower professional barriers.

Since the end of 2019, medical aesthetics institutions have actively embraced the wave of capital investment. Mergers and acquisitions within the industry have become increasingly active, with resources accelerating their concentration among leading players. Large chain medical aesthetics institutions such as Ruili Medical Aesthetics and Langzi Shares have gone public one after another, while large plastic surgery and cosmetic chains like Yimeier and United Lige have also demonstrated strong performance.

The strong performance of Aier Eye Hospital and Topchoice Medical in the capital markets, coupled with the simultaneous IPO bids by three ophthalmology hospital chains—Huaxia Eye Hospital, Purui Eye Hospital, and He’s Eye Hospital—has ensured that this sector remains a key investment hotspot in 2021. However, as competition in the consumer healthcare market intensifies and the quality of emerging companies varies significantly, a critical challenge for investors will be to identify and select target companies that possess distinct professional specialties, robust competitive moats, and promising prospects for sustainable growth.

Since the National Health and Family Planning Commission included 10 categories of independently established medical institutions in the field of social investment in August 2017, third-party independent medical service providers have been highly sought after by the capital market. The shift of certain in-hospital services to third-party independent medical institutions will be a major trend in future development, and policy dividends will drive continued in-depth growth across various sub-sectors.

Third-Party Medical Imaging Center

Panorama Medical Imaging completed a Series B equity financing round exceeding RMB 600 million in early 2020. The robust development of domestic third-party medical imaging centers, represented by Panorama Medical Imaging, has significantly addressed the insufficiency of diagnostic capabilities at the primary care level, while also alleviating the strain on imaging resources in public hospitals in first-tier cities. However, due to the substantial capital investment required and the extended period needed to achieve profitability, investors are exercising greater caution in selecting target companies. Market leaders with strong operational capabilities and scalable, replicable business models are increasingly favored.

Third-Party Pathology Diagnostic Center

China currently faces challenges such as a significant shortage of pathologists and relatively weak pathological diagnostic capabilities, giving rise to third-party pathology diagnostic centers. The pathology industry in China is currently grappling with a severe talent shortage; the number of registered pathologists falls far short of clinical demands, with a workforce gap approaching 100,000. Low income levels in pathology departments are also a contributing factor to this talent scarcity.

Driven by the rising demand for pathological diagnoses, the efficiency gains from AI in pathology, and favorable national policies, third-party pathology diagnostic centers are experiencing rapid growth. Established players in this sector, such as Huayin Health and Hengdao Pathology, are poised to attract significant interest from the capital market.

Third-Party Medical Laboratory

Against the backdrop of the COVID-19 pandemic in 2020, traditional independent clinical laboratories (ICLs) also experienced business growth. Particularly during the period of surging demand for COVID-19 testing, their performance improved significantly, leading to substantial stock price increases for listed companies such as Dian Diagnostics, KingMed Diagnostics, and Da An Gene. We believe that ICLs will continue to enjoy capital dividends and remain favored by the capital market over the next three years. Unlisted industry leaders, represented by Adicon and Kangsheng Global, are expected to attract greater attention.

Third-Party Sterile Supply Center

As one of the largest cost centers in hospitals, the central sterile supply department (CSSD) is increasingly being outsourced, a trend that presents significant opportunities for third-party CSSD centers. The emergence of these centers has substantially addressed critical pain points in infection control and regulatory compliance within the industry, while offering industrial advantages through enhanced upstream and downstream integration. Under the normalized impact of the pandemic, third-party CSSD centers have demonstrated remarkable operational economies of scale, making them one of the few beneficiary segments in the medical services sector. Leading companies such as Laoken Medical and Julikang are viewed favorably for their future prospects.

Third-party independent medical institutions are characterized by standardizability, significant economies of scale, high entry barriers, and strong replicability. Companies that can achieve chain-based and group-oriented development, establish robust collaborative relationships with general hospitals, and provide more diversified services to primary healthcare institutions will inevitably be sought after by the capital market.

With the rapid advancements in artificial intelligence, big data, mobile internet, cloud computing, and the Internet of Things (IoT), modern technology is reshaping new healthcare service models by transforming traditional methods of seeking medical consultation. Since 2020, favorable policies, technology-driven innovation, and the outbreak of the pandemic have further accelerated the development of “new infrastructure” in traditional healthcare services, as specifically reflected in the following aspects:

Renovation and Upgrading of Traditional Hospitals

Digital healthcare is increasingly permeating offline scenarios in traditional hospitals. The emergence and implementation of concepts such as digital operating rooms, digital pharmacies, and digital wards have significantly enhanced the quality of diagnosis and treatment in traditional hospitals, as well as the overall efficiency of medical staff. Over the past year, interest in hospital Internet of Things (IoT) has surged. Lianxin Technology completed two rounds of RMB 450 million in financing within a year, drawing market attention to the entire sector. Hospital IoT platform companies such as Nobo Medical, Ruihua Kangyuan, and Depin Medical have also secured hundreds of millions in capital financing. iCapital predicts that leading companies in this niche segment will continue to attract significant attention in 2021.

Empowering Traditional Medical Technologies

Over the past year, numerous digital diagnostics companies have achieved significant milestones. For instance, Shukun Technology secured RMB 590 million in strategic financing; Infervision and Airdoc planned to list on the STAR Market; Keya Medical prepared for an IPO on the Hong Kong Stock Exchange; and Ande Yizhi obtained the first National Medical Products Administration (NMPA) Class III medical device certificate for AI-assisted diagnosis. The rise of AI-driven diagnostics has substantially enhanced diagnostic capabilities and efficiency within China’s healthcare system, while also driving improvements in the clinical service capacity of traditional hospitals.

Furthermore, as a novel digital health solution, digital therapeutics (DTx) are entering the public spotlight and ushering in a new era for the evolution of traditional medical technologies. Currently, this niche sector is still in its nascent stage, with scarce investment targets. Star companies capable of acquiring real-world clinical data and demonstrating therapeutic efficacy are bound to attract significant market attention.

The Rise of Internet Hospitals

In recent years, internet hospitals have experienced significant growth under the support of national policies. Particularly influenced by the COVID-19 pandemic in 2020, they have ushered in new development opportunities and played a substantial role in achieving “balanced allocation of medical resources” and “improved efficiency of healthcare services.”

Major commercial giants such as Alibaba, JD.com, and Baidu continue to expand their presence in this sector. Leading companies like Weimai Group have secured capital financing over the past two years. It is anticipated that this niche market will remain highly favored in the coming year. Key areas of interest for investors will include the implementation of medical insurance coverage for internet hospitals, the outflow of prescriptions from hospitals, and innovations in patient management models across both in-hospital and out-of-hospital settings.

Guided by national policies, China’s commercial health insurance market has demonstrated strong growth momentum. According to data released by the Chinese government’s official website, premium income from commercial health insurance grew from RMB 86.3 billion in 2012 to RMB 706.6 billion in 2019, representing a compound annual growth rate (CAGR) of over 30%. By the end of November 2020, premium income from commercial health insurance in China reached RMB 764.1 billion, a year-on-year increase of 16.4%; claims expenditures amounted to RMB 253.1 billion, up 22.4% year on year. Long-term health insurance has accumulated over RMB 1 trillion in risk reserve funds for policyholders.

However, despite the promising outlook, commercial health insurance also faces multiple challenges, mainly reflected in:

1) Medical insurance remains the primary payment method, with commercial health insurance accounting for a low proportion of medical expenditures. Compared to developed countries, China's commercial health insurance sector is still in its nascent stage;

2) Currently, commercial health insurance primarily covers middle- and high-income groups. While the elderly have a significant demand for commercial insurance, their willingness to purchase is low, leading to higher consumption of public medical insurance resources. This has created a mismatch between the uptake of commercial health insurance and the utilization of public medical insurance resources.

3) Severe product homogenization, with disorderly competition and price wars prevalent in the market.

In the face of numerous opportunities and challenges in the commercial health insurance market, a large number of TPA (Third-Party Administrator) companies and MGA (Managing General Agent) companies have emerged, becoming new healthcare payers and an emerging force in the development of the insurance industry.

In recent years, traditional Third-Party Administrator (TPA) companies have actively transitioned toward a “Managing General Agent (MGA) + Software-as-a-Service (SaaS) + TPA” business model, striving to achieve deep integration between insurance protection systems and health management while providing one-stop solutions. Meanwhile, they are actively embracing emerging technologies such as medical big data, the Medical Internet of Things (IoMT), artificial intelligence, and internet-based healthcare to upgrade and transform traditional commercial health insurance.

Over the past year, leading companies in this niche sector have been highly favored by the capital market. InsurGeek completed a $25 million Series C financing round in March 2020; Waterdrop Insurance completed a $230 million Series D financing round in August 2020; and Nanyan Insurance Technology completed a RMB 250 million Series C financing round in October 2020.

Yi Kai believes that the separation of production and sales, and even the separation of production and services, will inevitably become a future development trend in the commercial health insurance industry. Agencies with platform operational capabilities and the ability to provide comprehensive insurance service solutions are poised to seize new growth opportunities in the coming year.

We believe that the following 20 primary-market healthcare services and digital health companies possess distinct disciplinary specialties and competitive advantages, making them worthy of close attention in 2021:

Sanbo Brain Hospital

Established in 2004, the Group currently oversees six hospitals (including one under construction), with a total of over 2,000 beds. It is the largest private medical group in China specializing in neurosciences, integrating clinical care, teaching, and research. In May 2020, Sanbo Brain Hospital secured Series B financing exceeding RMB 800 million, led by Taikang, and submitted its IPO application to the ChiNext board at the end of 2020.

Lu Daopei Medical Group

Established in 2001, the company currently operates five medical institutions with a cumulative total of over 700 beds, making it a leading domestic chain healthcare group in the private sector for hematological diseases. In July 2020, the company completed its Series B equity financing of over RMB 500 million, led by Temasek, and has formulated a clear IPO plan.

Shulan Healthcare Group

Established in 2013 and initiated by an academician team led by Academicians Li Lanjuan and Zheng Shusen of the Chinese Academy of Engineering, the organization possesses unique and hard-to-replicate medical resources. It currently operates three directly affiliated hospitals (two under construction), nine managed hospitals, one clinic, and nine physician groups, functioning as a comprehensive chain healthcare group characterized by its “strong specialty, limited general practice” model.

Hong Kong Asia Medical

Founded in 1999, the Group currently operates three hospitals and two overseas cardiovascular centers. As a leading large-scale hospital chain specializing in cardiovascular medicine, it is progressively expanding its nationwide network in China and exploring international markets.

Boner Orthopedics

Established in 2012, the group currently operates 14 hospitals with a cumulative total of over 4,000 beds, positioning itself as a leading chain medical group in China specializing in orthopedics and rehabilitation. In January 2021, it secured nearly RMB 300 million in Series D financing from Fortune Capital (Dachen Caizhi) and Qianji Capital, with plans to list on the ChiNext board in 2021.

United Family Healthcare

Founded in 1997, it is one of China’s most renowned comprehensive high-end private healthcare institutions, having pioneered the premium private hospital sector in the country with its personalized services. Currently, it operates eight hospitals, two medical centers, and more than ten clinics, employing over 600 full-time physicians, a part-time expert team of more than 1,000 specialists, and a nursing staff exceeding 1,000. The group reported revenues of RMB 2.45 billion in 2019, completed its delisting in early 2021, and plans to pursue a future listing on either the Hong Kong Stock Exchange or the Chinese A-share market.

Arrail Dental

Founded in 1999, Arrail Dental, a leading brand in China’s high-end dental services industry, has long been committed to providing international, first-class, and professional dental care to the domestic middle class and expatriates, with over 100 high-end dental clinics established across China. In 2017, the company secured $90 million in Series D financing jointly invested by Goldman Sachs Group and Hillhouse Capital.

Aier Eye Hospital

Founded in 2005, Aier Eye Hospital is a well-known professional ophthalmic medical chain institution in China. It currently operates 18 eye hospitals and 3 eye clinics, with its business covering 17 cities across the country. The company completed a strategic financing of nearly RMB 200 million in November 2019, exclusively invested by China Life Health Care Fund, and submitted an IPO application to the ChiNext board in July 2020.

Amcare

Established in 2006, this premium private healthcare chain specializing in women’s and children’s services currently operates six women’s and children’s hospitals, comprehensive outpatient centers, and three postpartum care centers. With a presence across the Beijing-Tianjin-Hebei, Yangtze River Delta, and Pearl River Delta regions, it provides one-stop services encompassing obstetrics, gynecology, pediatrics, assisted reproduction, postpartum rehabilitation, postpartum recuperation, and medical aesthetics. It is the private hospital with the highest delivery volume in China. The company initiated listing tutoring on the ChiNext board in 2020.

Yimeier

Founded in 1997, Yimeier Group is one of the earliest players in China’s medical aesthetics industry and currently stands as the leading chain service provider in the domestic sector. Integrating clinical practice, scientific research, and teaching, the group operates a total of 13 aesthetic hospitals and outpatient clinics. Having garnered favor from numerous top-tier investors, the group plans to launch its initial public offering (IPO) in the near future.

Panorama Medical Imaging

As a leading third-party medical imaging center in China, Panorama Medical Imaging was established in 2011. It currently operates eight diagnostic centers and employs over 600 professionals, distinguishing itself as one of the few domestic players dedicated to pursuing precision imaging, practicing in-depth health screenings, and providing personalized medical services. In February 2020, the company completed a Series B equity financing round exceeding RMB 600 million. Due to its robust technical capabilities, it has garnered significant favor from investors and plans to initiate an IPO in 2021.

Nanyan Insurance Technology

Established in 2015, it is a leading integrated insurtech service platform in China. Leveraging its unique “MGA + SaaS + TPA” business model and comprehensive capabilities in health insurance—the only one of its kind in the country—the company is committed to building a Chinese version of “UnitedHealth” that integrates commercial insurance with value-based healthcare. In October 2020, it completed a C-round financing of RMB 250 million, led by Qianji Capital.

ShanZhen

Shanzhen is a China-based platform dedicated to health services, insurance, and risk management for middle-aged and elderly individuals. Leveraging its health service network, family doctor programs, and extensive user communities, Shanzhen has accumulated a massive nationwide database of health data for the middle-aged and elderly population. It deeply engages in product development, risk control, and technological applications for senior health insurance, addressing the critical market demand for integrated medical services and health insurance among the elderly, thereby delivering significant social value. Shanzhen has garnered favor from numerous leading investors, including Hillhouse Capital, Qiming Venture Partners, GGV Capital, and SIG China.

Adicon

It is one of the top three players in China’s third-party medical testing industry. Founded in 2004, Adicon is a nationwide, cross-regional chain operator of independent third-party medical laboratories. It has established more than 20 medical laboratories to date, offering services including medical testing, clinical drug trials, scientific research support, health management, and pathology consultation. In January 2021, it completed an $88 million strategic financing round led by Khazanah Nasional, Malaysia’s sovereign wealth fund, and plans to launch an initial public offering (IPO) on the Hong Kong Stock Exchange.

LaoKen Medical

Established in 1998, the company is a leading enterprise in China’s private sector for the manufacturing of medical sterilization equipment and infection control, as well as the largest chain operator of independent third-party sterilization centers. Laoken Medical was listed on the National Equities Exchange and Quotations (NEEQ) in 2015, announced its delisting at the end of 2020, has since completed a new round of financing post-delisting, and has clear plans for an initial public offering.

Ande Medical Intelligence

Founded in 2017, the company is a technology firm dedicated to the application of artificial intelligence (AI) in healthcare. It is a global pioneer and leader in AI for medical imaging and stands as the only platform enterprise worldwide capable of providing whole-body AI-assisted diagnostic solutions. In June 2020, it obtained China’s first Class III registration certificate for AI-assisted diagnosis from the National Medical Products Administration (NMPA). The company plans to file for an initial public offering (IPO) on the ChiNext board by mid-2022 and is currently launching its Pre-IPO financing round.

LinkDoc Technology

Founded in 2014, LinkDoc Technology is a unicorn enterprise in China’s medical big data and artificial intelligence sectors. It is committed to providing a full-disease-cycle service platform for cancer patients in China, actively exploring innovative online service models for specialty oncology pharmaceuticals, and establishing an integrated online-offline healthcare delivery system for oncology. The company delivers high-quality medical and health services covering the entire disease continuum, from clinical care to medication. In 2020, the company completed a RMB 700 million Series D+ financing round, and in March 2021, it received strategic investment from AliHealth.

Dingdang Kuaiyao

Founded in 2014, Dingdang Kuaiyao is an O2O-based home delivery platform for pharmaceuticals and a third-party information display platform that assists pharmacies in meeting the demand for convenient services. It is a leading enterprise in China’s internet healthcare sector. In 2020, the company completed two rounds of financing to accelerate its “Thousand Cities, Ten Thousand Stores” strategic layout.

Zhiyun Health

Established in 2014, it is China’s leading one-stop platform for chronic disease management and smart healthcare. Currently, through its independently developed hospital SaaS system, pharmacy SaaS system, and advanced internet hospital platform, it provides services to nearly thousands of hospitals and tens of thousands of pharmacies across China, reaching 500 million patients with chronic diseases. In January 2020, it completed a RMB 1 billion Series D financing round led by CMB International, with clear plans for an initial public offering (IPO).

MedTrust Health

Founded in 2017, Medbanks Health is committed to innovating healthcare payment models by leveraging “Internet+” to connect patients, pharmaceutical companies, and commercial insurers. The company aims to drive the deep integration of financial instruments with the healthcare sector, creating a differentiated ecological closed loop of “Internet+ Healthcare + Pharmaceuticals + Insurance.” Following a strategic investment from China Life Reinsurance Company Ltd. in March 2020, the company secured Series B financing in March 2021, jointly led by Ant Group, Shanghai Bio-Medicine Industry Equity Investment Fund, and Sinovation Ventures.

2021.5

IMPORTANT NOTICE

Each research analyst who is primarily responsible for drafting all or part of this research report hereby declares:

(1) Any views expressed in this report accurately reflect the author’s personal opinions on the industry and companies;

(2) The analyst has not, does not, and will not receive any compensation for the views or recommendations expressed in this report.

This research report is intended solely for our clients and partners. Apart from disclosures related to China Renaissance Capital, this report is based on publicly available information that we consider reliable; however, we do not guarantee the accuracy or completeness of such information, and clients should not rely on it as being accurate or complete. We update our research in a timely manner where possible. With the exception of certain industry reports published on a regular basis, the majority of our reports are released on an ad hoc basis when deemed appropriate by our analysts.