Third-Party Sterile Supply Centers Accelerate Licensing Amid Policy Support, Driving Sustained Revenue Growth

With VCBeatAs predicted in VCBeat’s “Special Report on Third-Party Sterile Supply Centers: Seizing Opportunities and Riding the Trend,”2016Since [year], the third-party sterile supply center industry has experienced rapid development,2021more rapidly.

First, both existing and newly established third-party sterile supply centers have gradually obtained medical institution practice licenses. Through regulatory oversight, the more standardized third-party sterile supply center industry has avoided market chaos characterized by mixed quality, safeguarded the industry’s reputation, facilitated business operations for these centers, and driven continuous revenue growth.

Second, medical institutions in China, including hospitals, dental clinics, medical aesthetics centers, and community health centers, have experienced rapid growth. In particular, there has been a substantial surge in demand for third-party sterile supply centers among small and medium-sized private medical institutions. Data released by the National Health Commission shows that as of the end of March 2021, the total number of healthcare institutions nationwide reached 1.026 million. Compared with the end of March 2020, the number of healthcare institutions across China increased by 17,273, including an increase of 1,170 hospitals and 17,572 primary healthcare institutions. As of the end of March 2021, there were 36,000 hospitals. Compared with the end of March 2020, the number of public hospitals decreased by 76, while the number of private hospitals increased by 1,246.

Third, the government has strengthened regulatory oversight of medical institutions and successively issued policies such as the Guiding Opinions on Strengthening Operational Management of Public Hospitals, the Accreditation Standards for Tertiary Hospitals (2020 Edition), and the Notice on Issuing the Specifications for Cost Accounting in Public Hospitals. These measures have driven hospitals to adopt refined operational practices and effectively control costs. Due to cost considerations, an increasing number of hospitals have begun to procure third-party sterile supply services.

Influenced by the aforementioned factors, the third-party sterile supply center industry accelerated its development in the first half of 2021, with both customer base and revenue maintaining substantial growth.

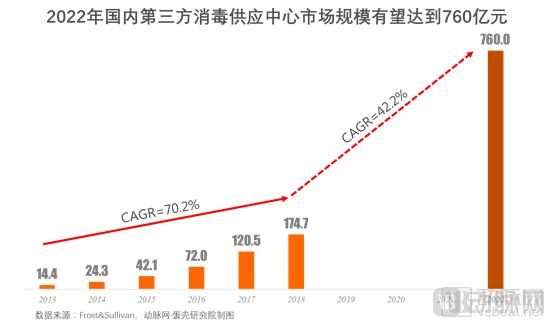

Previously, VCBeat·VBInsight estimated that the market size of China’s third-party sterile supply centers would reach RMB 76 billion by 2022, with a compound annual growth rate (CAGR) of 42.2% from 2018 to 2022. Given the current favorable development trends, we anticipate that the third-party sterile supply center industry will exceed these expectations and achieve even higher targets.

Meanwhile, we have also observed that the third-party sterile supply center industry has undergone significant changes driven by shifts in core factors such as policy and market dynamics. To explore its development pathways, current transformations, and future trends, we have conducted a comprehensive review of the third-party sterile supply center industry.

Core Viewpoints:

The number of third-party sterile supply centers approved between 2021 and 2022 will continue to grow;

Third-party sterile supply centers will provide comprehensive services covering flexible endoscopes, rigid instruments, and medical textiles in the future;

The number of third-party sterile supply centers is relatively small, with a distribution pattern of "more in the east and fewer in the west"; enterprises need to establish more centers.

Branded, Grouped, and Chain-operated Third-party Sterile Supply Centers Will Win Market Competition in the Future;

Sustained long-term policy support and gradual expansion of the industry scale will drive substantial growth in corporate revenues;

In August 2017, the National Health and Family Planning Commission issued the “Notice on Deepening the ‘Streamline Administration, Delegate Power, Improve Regulation, and Upgrade Services’ Reform to Stimulate Investment Vitality in the Medical Field,” which pointed out the addition of five categories of independently established medical institutions: rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers.This marks the point at which disinfection service enterprises have acquired the status of medical institutions.

In May 2018, the “Basic Standards for Medical Sterile Supply Centers (Trial)” and the “Management Specifications for Medical Sterile Supply Centers (Trial)” were issued.Detailed provisions have been made regarding departmental setup, staffing, infrastructure, functional zone planning, and equipment configuration.

In 2019, the National Health Commission issued the "Notice on Issuing the Basic Standards and Management Specifications (Trial) for Three Types of Medical Institutions, Including Medical Sterile Supply Centers."It was mentioned that disinfection institutions should, in accordance with relevant regulations, complete adjustments to the infrastructure of disinfection centers and disinfection equipment by the first half of 2019, and obtain the "Medical Institution Practice License."

The implementation of the aforementioned policies means that third-party sterile supply centers must be reasonably constructed and operate in a standardized manner in accordance with regulatory requirements, and must obtain a Medical Institution Practice License before they can provide sterile supply services. Obtaining this license signifies that the sterile supply center fully complies with construction and operational standards, has gained recognition from regulatory authorities, and demonstrates strong institutional strength and professional capabilities. Furthermore, with a Medical Institution Practice License, the service quality of third-party sterile supply centers can meet the needs of medical institutions at all levels, thereby fostering greater trust among these institutions. Since 2019, third-party sterile supply centers have become more proactive in applying for the Medical Institution Practice License.

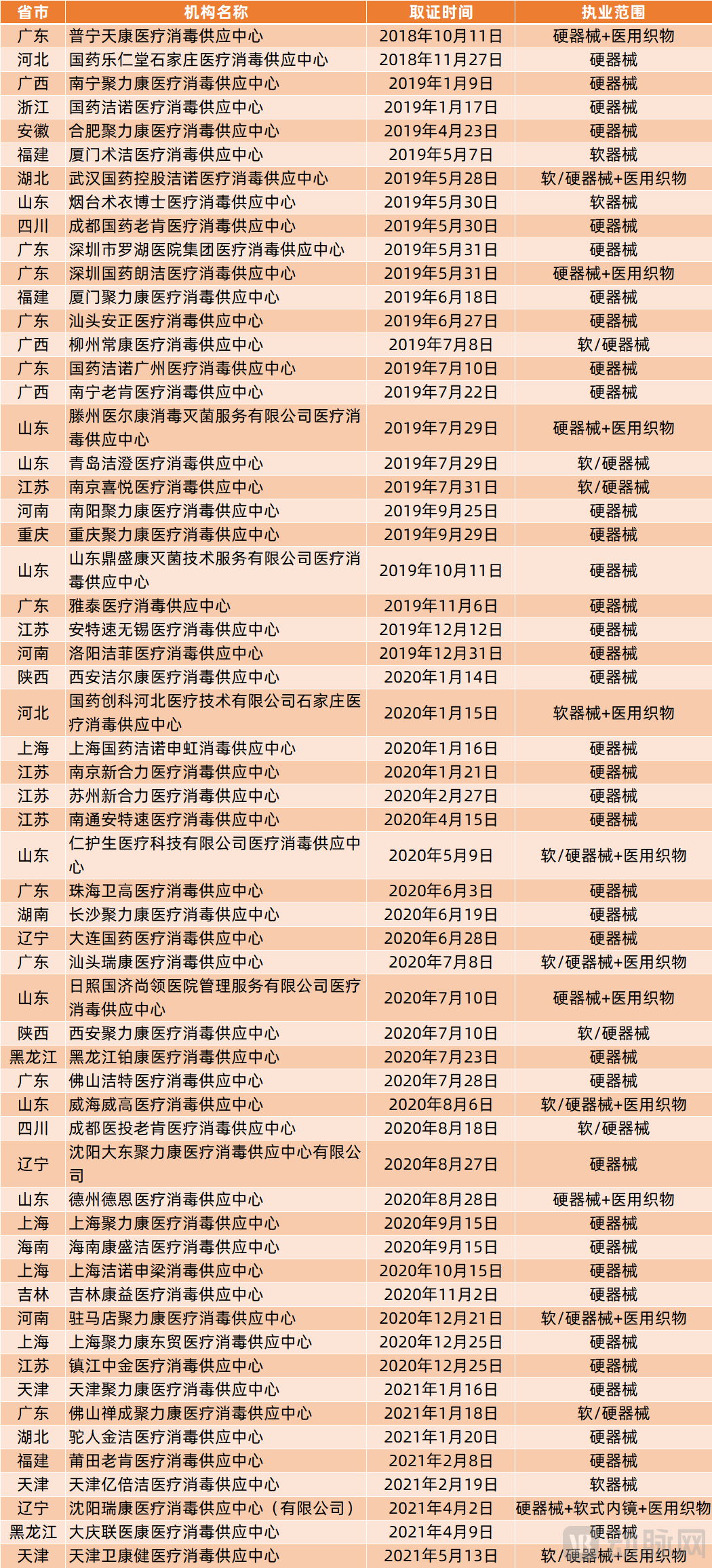

According to the official website of the National Health Commission, as of now, a total of 59 third-party sterile supply centers in China have obtained Medical Institution Practice Licenses (excluding projects pending approval). Among them, 2 were approved in 2018, 23 in 2019, 26 in 2020, and 8 so far in 2021.

(Table by VCBeat, data source: National Health Commission)

In October 2018, China’s first third-party sterile supply center obtained a Medical Institution Practicing License. The number of third-party sterile supply centers granted this license saw substantial growth over the subsequent three years (2019–2021). This surge was driven by two factors: existing third-party sterile supply centers proactively upgraded their infrastructure and sterilization equipment, actively applying for licenses once they met regulatory requirements; meanwhile, newly built third-party sterile supply centers were constructed in accordance with policy-mandated standards and likewise pursued licensure diligently.

An analysis of certification status among third-party sterile supply centers reveals multiple trends and changes within the industry.

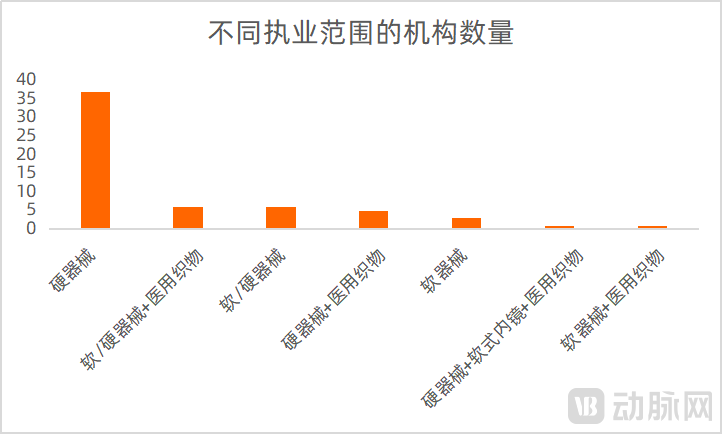

Based on the approved scope of practice, 55 third-party sterile supply centers are authorized to provide sterilization services for rigid instruments; 17 are authorized to provide sterilization services for flexible instruments; and 8 are authorized to provide sterilization services for medical textiles. Among these, 37 third-party sterile supply centers specialize in rigid instruments, while 3 specialize in flexible instruments. Although fewer in number, third-party sterile supply centers with comprehensive scopes of practice—such as those covering both flexible and rigid instruments; flexible instruments and medical textiles; rigid instruments and medical textiles; flexible/rigid instruments and medical textiles; or rigid instruments, flexible endoscopes, and medical textiles—offer broader service ranges and possess stronger competitiveness.

From this perspective, third-party sterile supply centers will expand their service boundaries in the future by developing an integrated “triad” service model covering soft instruments, hard instruments, and medical textiles, thereby enhancing their competitiveness.

The approval status as of 2021 also supports the above viewpoint: in the first half of 2021, four new third-party sterile supply centers specializing in rigid instruments were approved, one new center specializing in flexible instruments was approved, and three new centers providing comprehensive services were approved.

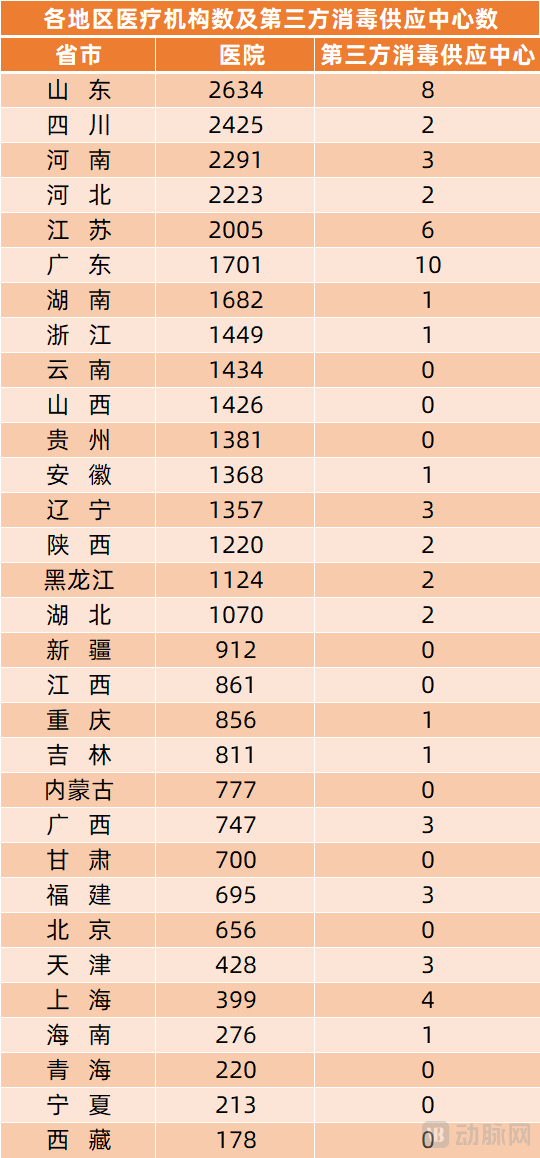

In terms of geographic distribution, 20 provinces and municipalities across China have issued operating licenses for Central Sterile Supply Departments (CSSDs). Among them, Guangdong Province is home to 10 third-party CSSDs that have obtained Medical Institution Practicing Licenses, accounting for 17% of the total. Shandong, Jiangsu, and Shanghai have 8, 6, and 4 such facilities, respectively. Meanwhile, 11 provinces, municipalities, and autonomous regions—including Beijing, Shanxi, Inner Mongolia, Jiangxi, Guizhou, Yunnan, Gansu, Qinghai, Ningxia, and Xinjiang—have not yet issued operating licenses for CSSDs.

(Sorted in descending order by the number of medical institutions; data as of the end of March 2021)

Overall, the distribution of third-party sterile supply centers in China presents a pattern of "more in the east and fewer in the west."The exceptions are Beijing, Shanxi, and Jiangxi, where no third-party sterile supply centers exist yet, and the model remains dominated by self-built sterile supply centers within public hospitals. Notably,At the current stage, the distribution of third-party sterile supply centers is closely related to local medical resources, economic development, and the degree of policy openness, with all three factors being indispensable.For example, regions with limited medical resources and smaller market potential, such as Qinghai, Ningxia, and Tibet, currently have no third-party sterile supply centers. Although provinces like Gansu, Inner Mongolia, Xinjiang, Yunnan, and Guizhou have a relatively large number of healthcare institutions, they also lack third-party sterile supply centers due to their status as economically underdeveloped areas.

VCBeat has previously learned that the sterilization cost per surgical instrument is RMB 4.5–5.5 for tertiary hospitals and approximately RMB 6.5–7.5 for secondary hospitals. The higher the hospital tier, the more saturated its capacity tends to be, resulting in better utilization of equipment and facility resources; consequently, the depreciation and amortization of fixed assets allocated to each instrument are relatively lower. In contrast, third-party sterile supply centers can reduce the sterilization cost per instrument to RMB 3–4, enabling annual operational cost savings of approximately RMB 7 million for tertiary hospitals and RMB 3 million for secondary hospitals.

Furthermore, third-party sterile supply centers that have obtained a Medical Institution Practice License and are integrated into the regulatory framework can help medical institutions reduce capital investment, improve service efficiency and the quality of disinfection and sterilization, lower infection risks, and significantly enhance resource utilization efficiency.Therefore, we believe that an increasing number of hospitals will opt to procure services from third-party Central Sterile Supply Departments (CSSDs) due to cost and other factors.

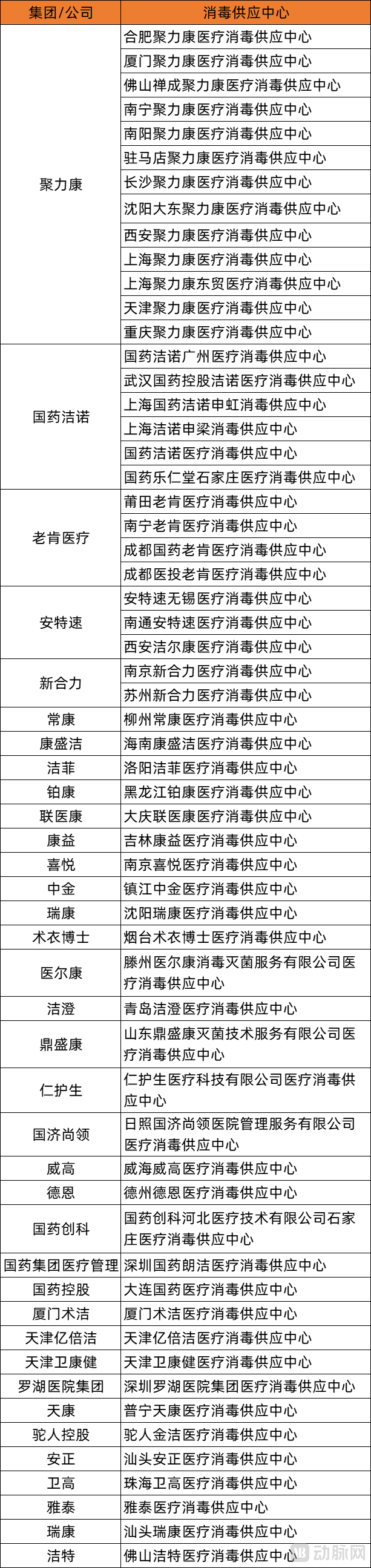

From the perspective of approved enterprises, third-party sterile supply centers are exhibiting a "proliferation of diverse players" and are evolving toward branding, corporatization, and chain operations.Currently, the leading enterprises in the third-party sterile supply center sector, including Julikang, Sinopharm Jienuo, Laoken Medical, Antesu, and New Heli, each have 13Approval was granted to 6, 4, 3, and 2 centers, respectively, leading other companies.

Overall, group-affiliated centers account for 47.5% of all third-party sterile supply centers, while other independently operated third-party sterile supply centers make up the remaining 52.5%. Among these, Sinopharm-affiliated entities—Sinopharm Chuangke, Sinopharm Medical Management, and Sinopharm Holdings—have each invested in and established one third-party sterile supply center. If Sinopharm-affiliated enterprises are categorized as a single group, they collectively operate nine third-party sterile supply centers.

At present, the number of third-party sterile supply centers remains far lower than that of hospital-owned sterile supply departments. However, as policies continue to advance and hospitals become more sensitive to operational costs, the business volume of third-party sterile supply centers is poised for rapid growth.The current number of third-party sterile supply centers is relatively low, and companies in the industry need to establish more such facilities to meet the substantial future demand for sterile supply services.

It is worth noting that the General Office of the State Council has issued policies such as the "Opinions on Supporting Social Forces to Provide Multi-level and Diversified Medical Services," vigorously supporting the establishment of medical institutions by social forces, thereby enabling an increasing number of social entities to enter the healthcare sector. On the other hand, the policies clearly specify the construction, operational, and equipment requirements for sterile supply centers.The entry barriers for third-party sterile supply centers have been significantly lowered, leading to a rapid increase in the number of industry players and intensifying market competition. We predict that in the future market landscape of third-party sterile supply centers, companies with strong branding, group-scale operations, and chain networks will emerge as the competitive winners.

Throughout the development of third-party sterile supply centers, policy has been one of the most critical driving forces. As the industry entered its golden period of growth, favorable policies continued to be introduced, underscoring the state’s optimism and high expectations for third-party sterile supply centers.

In January 2019, the General Office of the State Council issued the “Opinions on Strengthening Performance Appraisal of Tertiary Public Hospitals,” emphasizing that medical safety would become a key component of the appraisal indicators.From this perspective, regulatory authorities will impose stricter controls on the disinfection and use of medical devices within hospitals, which will also create revenue growth opportunities for third-party sterile supply centers.

In 2020, the National Health Commission and the National Administration of Traditional Chinese Medicine jointly issued the “Guiding Opinions on Strengthening Operational Management of Public Hospitals,” promoting hospitals’ emphasis on cost control, refined management, and improved operational efficiency. In December 2020, the National Health Commission released the “Accreditation Standards for Tertiary Hospitals (2020 Edition),” which places greater emphasis on daily quality management and performance, with the Diagnosis-Related Group (DRG) payment model playing a core role.

DRG payment is a bundled payment system based on Diagnosis-Related Groups, currently applied to short-term inpatient care. Following its implementation, all hospital services have shifted from generating incremental revenue to incurring incremental costs, making effective cost control increasingly critical. Theoretically, if the National Healthcare Security Administration sets the bundled payment rate for a specific DRG at 10,000 yuan, a medical institution treating a patient in that group would realize a profit of 1,000 yuan if the treatment cost is 9,000 yuan, but incur a loss of 1,000 yuan if the cost reaches 11,000 yuan.In light of this, to address the cost and operational challenges posed by DRG-based payment, hospitals are likely to actively procure services from third-party sterile supply centers. This strategy aims to reduce investment in their in-house sterile supply departments, thereby freeing up resources to expand inpatient bed capacity and enhance overall efficiency.

Additionally,In 2019, ten government departments jointly issued the “Opinions on Promoting the Sustainable, Healthy, and Standardized Development of Socially Run Medical Institutions,” which called for further strengthening government procurement of services and required all localities to formulate implementation measures for government procurement of medical and health services by the end of 2019, specifying details such as the entities responsible for procurement, scope of services, methods, procedures, and supervision and management.

In accordance with the aforementioned policies, the market size of third-party sterile supply centers will continue to expand, injecting vitality into industry development.