2021 Investment Hotspots in Digital and AI Healthcare: Insights from China Health Industry White Paper

Excerpted from the 2021 iCapital China Health Industry White Paper: Digital and AI Health Section, authorized for publication by VCBeat.

Preview of Main Content:

1. What major changes occurred in 2020?

2. Key Investment Themes and Market Forecasts for 2021

3. Forecast of Investment Hotspots in 2021

Core Views:

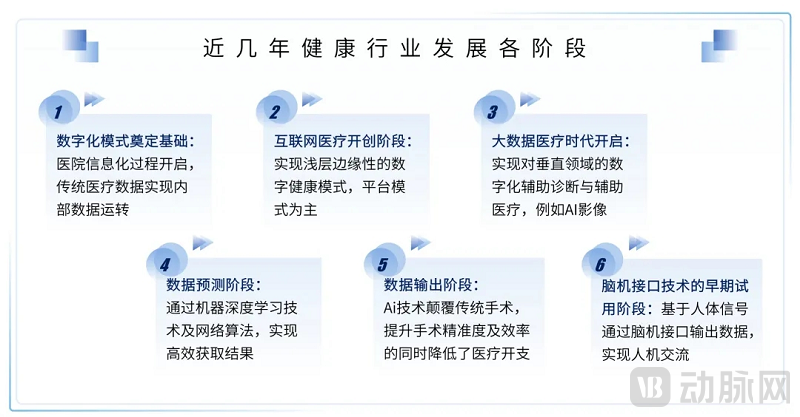

1.Intelligent healthcare is the ultimate goal, while digitalization is the inevitable path.The intelligentization of healthcare is not an overnight achievement. The initial wave of hospital informatization first realized structured data, establishing the fundamental digital infrastructure for digital healthcare. This foundation enables further training and applications based on data, starting with simple scenarios before advancing to complex ones. Consequently, the adoption of digital applications progresses from easy to difficult, evolving from data interpretation to data prediction, and finally to data output. The market initially saw shallow data applications such as online registration, consultations, payment, and medication purchases. It then transitioned to the analysis and synthesis of disease-specific data to form auxiliary diagnostic capabilities. Further advancements leverage deep machine learning to achieve medical and pharmaceutical predictions. In the future, processed data will be exported externally through applications such as surgical robots and brain-computer interface prosthetics. All these developments are driven by the continuous application, accumulation, and iteration of data and algorithms.

2.We maintain long-term confidence in the positive interaction and virtuous cycle between China’s health industry and its health insurance market.At present, the closed-loop ecosystem of “digital healthcare + pharmaceuticals + insurance” is taking shape in certain specialty fields or among specific consumer groups, but overall, it is far from realizing a comprehensive “industry-wide macro closed-loop.” Even after such a macro closed-loop is established, social health insurance will continue to play a pivotal role, with commercial health insurance serving merely as a supplement. Current challenges facing commercial health insurance include: first, relatively low premium volume; second, predominantly passive claims settlement, resulting in limited bargaining power over services and pharmaceuticals; and third, high customer acquisition costs in a market-driven environment. However, recent trends indicate that commercial health insurers are continuously innovating their products and receiving strong government support. From purely market-driven products like “Million Medical Insurance” to government-led initiatives such as “Hui Min Bao” (inclusive supplementary medical insurance), the foundation is being steadily strengthened. Large pharmaceutical companies and insurance institutions are proactively establishing collaborative mechanisms among healthcare, pharmaceuticals, and insurance. Meanwhile, originator drug manufacturers that have lost bids in centralized procurement are exploring new payment models, and the inclusion of commercial insurance formularies under the guidance of basic medical insurance is now on the agenda. Once a virtuous cycle among healthcare providers, pharmaceutical companies, and insurers is established, it will become a self-reinforcing process characterized by enhanced efficiency, reduced costs, internal circulation, and continuous strengthening, harboring immense commercial potential.

3.In the current digital health industry, the suitable model is a rational intersection of payers and customer acquisition scenarios, with the ultimate goal of the business model being scalable monetization.Currently, the singularity of payers in the healthcare industry and their clear demand for cost containment are quite unfavorable to digital health. Therefore, during the development stage of digital health, it is necessary to clearly identify the target users while simultaneously leveraging their payment capacity. Prioritizing hospitals and physicians as the primary user scenarios addresses issues related to traffic acquisition and conversion; meanwhile, positioning pharmaceutical companies and medical insurance as the primary payers supports scalable expansion by ensuring efficiency and stability.

4.Cutting-edge technologies, particularly AI, are redefining the cognitive boundaries of the health industry at an unprecedented pace.We believe that in the coming years, emerging fields such as genomic big data, AI-driven drug discovery, surgical robotics, and brain-computer interfaces will experience rapid development, accelerating scenario implementation and commercialization. More importantly, we believe that these frontier areas are precisely where super players capable of reshaping the entire industry landscape are most likely to emerge.

5.Key Investment Sectors in 2021:

(1)Recommended Model for Synergizing User Traffic and Conversion in the Joint Hospital-Physician Scenario:

·Driven by the upgrade of hospital informatization and in alignment with newly issued national policies, models with substantive capabilities to monetize drug and medical device decision-making include the spin-off of self-pay pharmacies in public hospitals and prescription circulation models under the dual-channel pharmacy system.

· Upgrading information flow based on internet technology enables institutions with limited capabilities to access enhanced digital healthcare management and medical technical expertise, including models such as co-construction and co-operation of departments, as well as in-hospital and out-of-hospital disease course management.

· Applications leveraging in-depth, disease-specific data, including digital assisted diagnosis and treatment based on standardized data (such as imaging), as well as precision medicine and personalized disease course management models utilizing non-standardized data (such as genomics, metabolism, and clinical phenotypes);

·Multidisciplinary medical data output, including surgical robots and brain-computer interface technologies;

(2)In the insurance sector, it is recommended to adopt business models capable of driving incremental market growth.

·Standard Entity: Insurance (brokerage) platforms capable of covering differentiated traffic or demonstrating the ability to improve conversion rates;

·Subtitle: Insurtech that leverages disease big data for risk control to enable product pricing and output capabilities;

(3)In the context of pharmaceutical companies, focusing on pre- and post-clinical scenarios:

· AI Drug Discovery and Development

·Digital Marketing for Market Access and Volume Growth of Pharmaceutical and Medical Device Products

When analyzing any industry, the first thing we look at is the overall market, with demographic structure being one of the most critical factors. Over the past few decades, China’s demographic dividend has been one of the most significant positive drivers of its development. In the context of China’s digital health industry, two aspects of its demographic structure are particularly noteworthy:

· The post-80s generation, as digital natives, has quietly entered middle age.

· Increased longevity has led to a growing elderly population.

What Are Digital Natives? The earliest batch of Chinese internet companies were founded around the year 2000. At that time, the post-80s generation was approximately 15 to 20 years old—an age when they had the leisure and interest to explore the online world during their school years. They were the cohort most adept at discovering and readily embracing the internet. It is fair to say that the internet has profoundly shaped an entire generation.

The post-80s generation witnessed the internet’s evolution from nothing to something, experiencing firsthand and at the forefront the myriad transformations it brought. Seven or eight years ago, these individuals were around 25 or 26 years old—a period marked by strong desires for communication, knowledge acquisition, and consumption. As the core user base for internet-based instant messaging, information services, and e-commerce, they became one of the key drivers behind the prosperity of the internet industry.

It is 2021. Those born in 1980 have just crossed the threshold of age 40, while the rest of the post-80s generation will enter middle age within the next three to five years. From a medical perspective, individuals around the age of 35 are beginning to show early signs of chronic diseases, which has fundamentally shifted their attention to personal health: from relying on youthful resilience to pull all-nighters before age 30, to embracing goji berry-based wellness practices today. This shift in mindset, combined with the post-80s cohort’s innate familiarity with the internet as digital natives, has fueled an initial surge in the popularity of digital health.

However, in the digital health sector, the contribution from the demographic base of digital natives remains limited. Currently, not every individual entering middle age seeks medical consultation or treatment. Nevertheless, it is foreseeable that over the next three to five years, the rising prevalence of chronic diseases within this cohort will provide a powerful impetus for the overall development of the digital health industry.

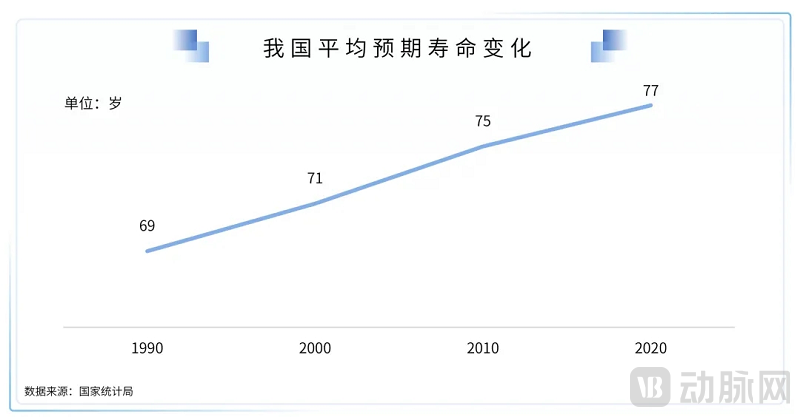

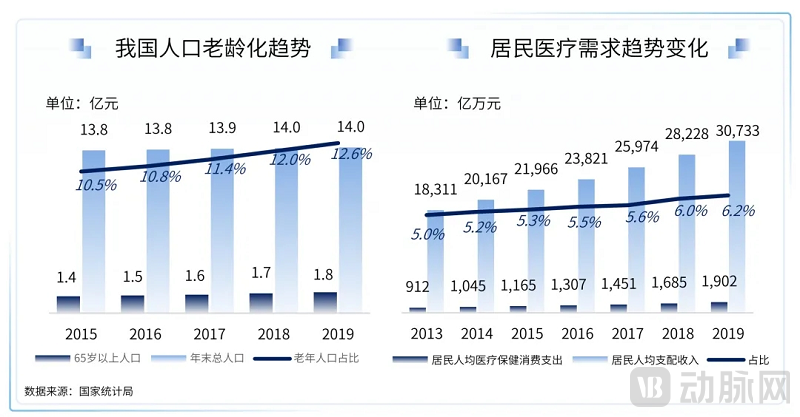

Another point is that the trend of increasing longevity among the Chinese population is an indisputable fact. According to data from the National Bureau of Statistics, life expectancy for Chinese people has risen from 68.55 years in 1990 to 77.30 years in 2020.

This data is highly significant: China’s elderly population is continuously growing and becoming more concentrated, making four-generation households increasingly common. What does this imply? High-quality medical resources are in short supply globally, and the middle-aged and elderly populations exhibit the highest utilization rates of these resources.

This means that if there is no significant improvement in the supply-side of existing medical resources, when the post-1980s generation enters middle and old age, they will be forced into a predicament of competing with their parents' generation for medical resources, at which point medical inflation will far exceed normal levels.

Naturally, the government will not remain idle. Enhancing the supply side of medical resources requires not only hard investments, such as training more excellent physicians and increasing the number of high-quality hospital beds, but also soft investments to improve efficiency across all aspects of healthcare delivery. Consequently, hospital informatization has long been a key criterion in hospital accreditation, while the demand for supply-side reforms is continuously driving the rapid development of medical digitalization. In the future, whether from an administrative or market perspective, the need to enhance efficiency through digitalization will become increasingly important.

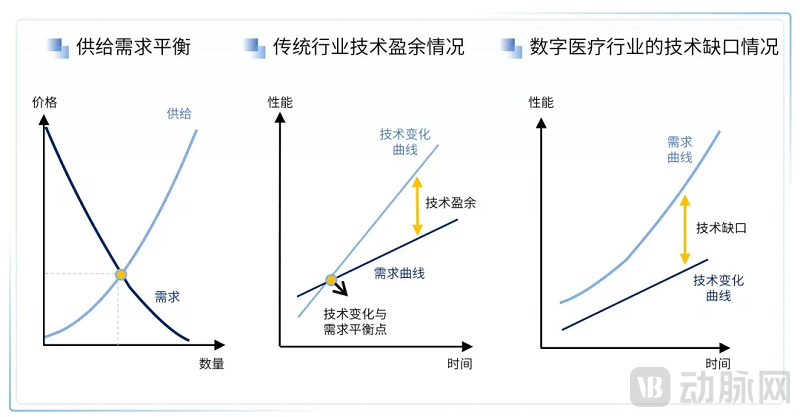

From an economic perspective, both supply and demand exhibit price elasticity, with the supply and demand curves intersecting at a point that represents market equilibrium. For most other industries, the demand curve shows a pronounced diminishing curvature. When a new technological product is launched, it is often priced at a premium or its capabilities exceed current market needs, resulting in a period of “technological surplus.”

In contrast, the healthcare industry has long exhibited a persistent phenomenon: regardless of advancements in medical capabilities, they fall far short of meeting the public’s growing demand for new medical technologies. Consumers demonstrate extremely low price sensitivity toward healthcare expenditures, meaning that demand for healthcare services remains largely unaffected by price fluctuations.

This represents a significant, long-term tailwind for the healthcare industry: regardless of how advanced medical technologies become, there is a low probability of technological capacity outstripping societal demand. Consequently, healthcare companies are both able and willing to make bold investments in research and development.

Global R&D spending on innovative drugs continues to rise, alongside advancing capabilities in diagnostic testing. Beyond capital investment, this growth is primarily driven by strong societal demand. Digital and AI technologies have already begun to demonstrate their technological and medical prowess in drug discovery and medical imaging. Against the backdrop of substantial healthcare needs, new application scenarios and technical approaches will continue to emerge.

Livelihood Issues: One of the Greatest Challenges Is Healthcare for the PeopleSuccessive national leaders have prioritized healthcare, achieving remarkable results that have drawn global attention. Basic medical insurance now provides near-universal coverage, encompassing 96.8% of the population according to statistics from the National Health Commission.

At every stage of national development, there are corresponding healthcare policies that align with the prevailing circumstances. However, as the country advances to a higher level, these existing policies inevitably reveal their limitations. Consequently, healthcare reforms are continuously being implemented to better suit the current national context.

The healthcare industry is among the most strictly regulated sectors under national policies. Nearly every new policy introduction reshapes the competitive landscape, while simultaneously creating greater development opportunities for innovative enterprises. Companies with a strong innovation mindset, willing to shed legacy burdens and continuously explore in the new environment, will also be the pioneers benefiting from the dividends of healthcare policy reforms.

In recent years, the successive reforms in the healthcare industry have invariably centered on national welfare and people's livelihood. With policies being rolled out frequently, each reform has ventured further into deep-water zones. This trend can be summarized from the following four aspects:

Reducing Healthcare Expenditures (Cost Containment in Health Insurance)

· Volume-Based Drug Procurement

· Two-Invoice System

·Drug Cost Proportion (Now Abolished)

· DRGs

·Volume-Based Procurement of Medical Consumables

· Reform of the Personal Account in Medical Insurance

Increase the Supply of Medical Resources

· Zero Tariffs on Anti-Cancer Drugs

·Acceptance of Overseas New Drug Clinical Data to Shorten the Time Lag Between Domestic and International Market Launches

· Establish the Hainan Boao Lecheng International Medical Tourism Pilot Zone and the Shenzhen-Hong Kong-Macao Drug and Medical Device Access Pilot Demonstration Zone, creating channels for the use of drugs not yet marketed overseas.

· Certain innovative specialty drugs are subject to a reduced value-added tax (VAT) rate of 3%, covering a total of 148 anticancer drug formulations and 96 active pharmaceutical ingredients (APIs).

· Marketing Authorization Holder (MAH) System for Drugs

· Allowing Physicians to Practice at Multiple Locations

·Consistency Evaluation of Generic Drugs

· AI-Assisted Diagnostic Tool Approved via Green Channel for Innovative Medical Devices

Convenience

·Internet hospitals can conduct follow-up consultations for some common and chronic diseases

·Inclusion of Online Internet-Based Diagnosis and Treatment in Medical Insurance

· Opening of Online Sales for Prescription Drugs

· Inclusion of Internet Hospital Drug Sales in Medical Insurance Coverage

· Pharmacy Dual-Channel

·Tiered Diagnosis and Treatment (e.g., Construction of Medical Consortia and County-Level Medical Communities)

Anti-Corruption

· Separation of Medical Care and Pharmacy, Outflow of Prescriptions

· Zero-Markup Drug Policy

· Prohibition of Pharmacy Trusteeship

· Medical Representative Filing System

· Full Liberalization of Online Prescription Drug Sales

· The National Healthcare Security Administration has issued a document stating that medicines sold by internet hospitals can be covered by the pooled medical insurance fund; however, the medical insurance quota for medicine sales by internet hospitals must be based on the total medical insurance budget of their affiliated medical institutions.

·Internet Medical Service Fees Included in Health Insurance Settlement

· Hainan has opened the Boao Lecheng International Medical Tourism Pilot Zone, and Shenzhen has established a pilot demonstration zone for the "Greater Bay Area Drug and Medical Device Connect" program, allowing limited importation and local use of new drugs and medical devices not yet marketed in China.

·Pilot Implementation of the Dual-Channel Policy for Pharmaceuticals in Qingdao, Chengdu, Zhejiang, and Other Regions Accelerates Outflow of Prescriptions

· Regions Intensify Crackdown on In-Hospital Marketing by Pharmaceutical Representatives

· National Centralized Procurement Platforms in Guangdong and Other Regions Open to Retail Pharmacies and Hospitals

· Guangdong Includes Psychotherapy in Medical Insurance Coverage

In 2020, in response to pandemic control needs, the National Health Commission and other departments intensively rolled out a series of policies that significantly accelerated the development of digital health. This compressed what would have otherwise taken three to five years of public education into just one year, achieving widespread adoption of online medical consultations and e-prescribing via the internet.

These policies are broadly divided into three phases:

· Emergency Relief Phase: The government requires all regions to centrally publish links to local internet hospitals and encourages the provision of online follow-up consultations.

· Healthcare Insurance Improvement Phase: The National Healthcare Security Administration issued a document to include eligible "Internet+" medical service fees in the scope of medical insurance payment.

· Normal Development Phase: The National Health Commission has called on all regions to accelerate the establishment of internet hospital service platforms.

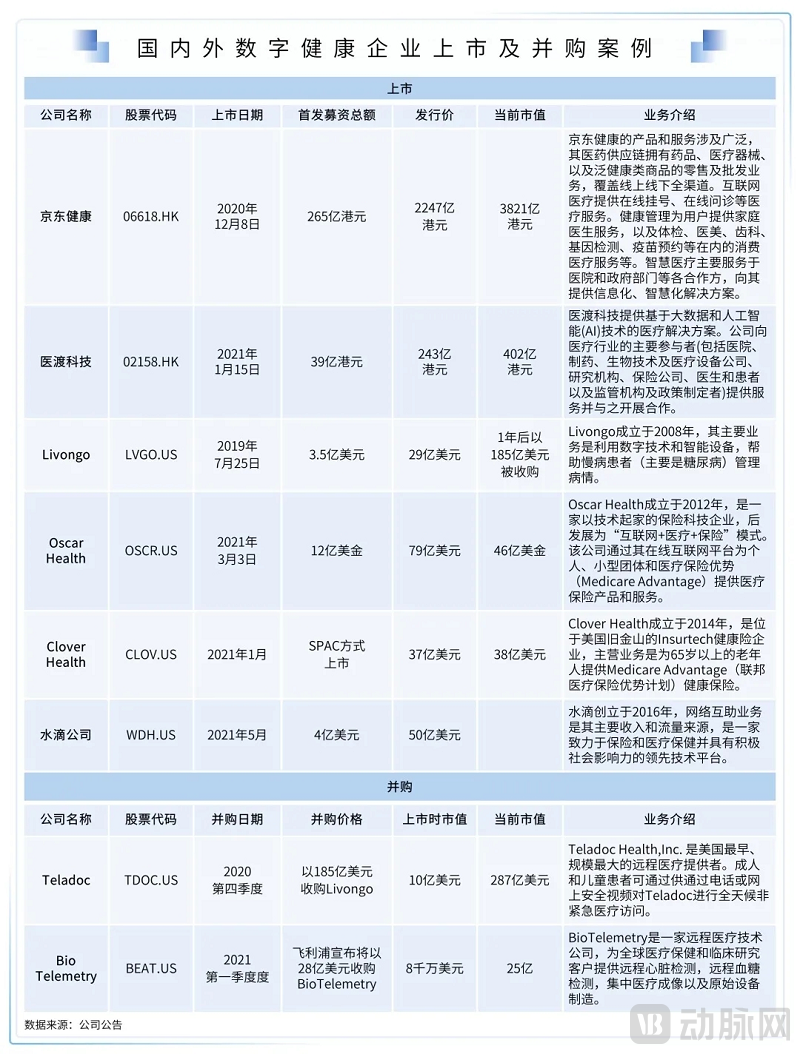

The initial public offerings and mergers and acquisitions of several domestic and international digital health companies in 2020 had a significant impact on global capital markets:

Many film and television works have imagined and showcased what the future of healthcare might look like.

For instance, in "Agents of S.H.I.E.L.D.," Coulson is brought back from the brink of death and undergoes memory implantation via virtual reality technology to treat his PTSD;

For example, in “Blade Runner 2049,” people can extend their lifespans by producing artificial internal organs through genetic design;

For example, in *Prometheus*, the protagonist can enter a state of suspended animation within a single-person medical pod, where an AI system conducts physiological monitoring and automatically performs surgery via robotic arms.

For example, in *Alita: Battle Angel*, individuals with limb amputations can control prosthetics via brain-computer interfaces using brainwaves, achieving a seamless integration of machinery and the human body;

These highly intelligent medical technologies represent people’s aspirational vision. Although they may still seem distant, they remain the goal of continuous exploration and advancement in medical technology. The intelligent transformation of healthcare is not achieved overnight. The first wave of hospital informatization successfully established structured data, forming the foundational infrastructure of digital healthcare. This foundation enables further data-driven training and applications, initially deployed in simple scenarios before expanding to more complex ones.

Therefore, the adoption of digital applications progresses from easy to difficult, evolving from data interpretation to data prediction and finally to data output. The market first saw shallow data applications such as online registration, consultation, payment, and medication purchase. It then transitioned to analytical and inductive capabilities based on disease-specific data to form auxiliary diagnostic abilities. Furthermore, deep machine learning is now enabling medical and pharmaceutical predictions. In the future, processed data will be exported externally through devices such as surgical robots and brain-computer interface prosthetics. All of this is driven by the continuous application, accumulation, and iteration of data and algorithms.

The development trajectory of digital and AI health can be broadly divided into the following six phases in chronological order: (the phases listed below do not strictly represent a sequential timeline and may overlap; they are provided for reference and organizational purposes only)

Phase I

The process of hospital informatization has given rise to information systems such as HIS, LIS, and PACS, enabling traditional healthcare to rapidly accumulate large volumes of structured and visualized medical data, facilitating internal data exchange and circulation within hospitals, and laying the foundation for all future digital models. This is the earliest-developed and currently most mature stage, with companies such as Winning Health, Neusoft Group, and Wanda Information having completed their IPO processes.

Phase II

Internet-based information flow applications have enabled a superficial, peripheral model of digital health, primarily characterized by platform-based services such as digital registration, payment, consultation, pharmacy, marketing, clinical support, and chronic disease management. This phase is regarded as the inception of “Internet Healthcare.” Most companies in this sector were founded around 2010–2015. After 5–10 years of development, they have entered a mature stage, either having recently completed their initial public offerings (IPOs) or being on the verge of doing so. Examples include listed companies such as Ali Health, Ping An Good Doctor, 111.com, and Yidu Tech, as well as companies preparing for IPOs such as WeDoctor, Zhiyun Health, Yuanxin Technology, and Taimei Medical Technology.

Phase III

Leveraging in-depth disease-specific data, digital assisted diagnosis and medical care can be implemented for specific vertical domains, such as particular diseases or clinical departments. Examples include AI-based interpretation of medical imaging, virtual reality-assisted treatment for psychiatric disorders, and the design of insurance products for individuals with pre-existing conditions based on single-disease datasets. This stage has generated substantial demand for both the volume and quality of healthcare data, where the data layer directly determines the development of application layers, ushering in the era of “Big Data Healthcare.”

Starting from the field of medical imaging data, which is the easiest to standardize, most AI+imaging companies were established around 2015. After approximately five years of development, these companies have achieved AI-assisted disease diagnosis for specific body parts based on imaging modalities such as fundus photography, CT, DR, MRI, ultrasound, and ECG, and have successively obtained Class III medical device certification from the NMPA. Such AI imaging companies are gradually entering the mid-to-late stages of financing, leveraging their capital advantages to continue expanding their product lines and bringing them to market, with the competitive landscape now largely formed.

In the realm of non-imaging data, such as population-level disease sequence data, information is often characterized by low structure and poor completeness. Given the massive volume of this data, coupled with concerns over patient privacy and the lack of interoperability among hospitals, significant government-led initiatives are required to drive progress. Consequently, under the guidance of the National Health Commission, two state-owned data service companies—CEC Data and Lianren Health—were established in recent years to gradually clean and structure medical data. The business models built upon this foundation still require a considerable period for development and are currently in their early-to-mid stages. For instance, sectors such as precision medicine and personalized disease management, which leverage individual genomic, metabolomic, and clinical phenotypic data, as well as the actuarial industry designing insurance products for individuals with pre-existing conditions based on disease data, remain in the phase of capital value discovery.

Phase IV

Leveraging vast datasets from molecular pharmacology and pharmacokinetics, and employing deep learning techniques such as convolutional neural networks (CNNs) and recurrent neural networks (RNNs), this approach achieves efficient outcomes in areas that previously required substantial effort from medical professionals with no guarantee of success. Examples include AI-driven drug R&D processes such as protein structure prediction, target discovery, compound screening and synthesis, new indication discovery, and crystal form prediction. Most companies in this stage have experienced rapid growth in recent years; they are typically in early stages, often emerging from laboratories, AI technology firms, or incubators within large pharmaceutical companies. While commercial outputs are still being explored, the future potential is immense.

Phase V

Leveraging human physiological tissue data, along with 5G transmission technology, micro-sensing technology, and high-precision control technology, intelligent surgeries ranging from simple to complex procedures are being realized. Just as the development of minimally invasive surgery disrupted open surgery, surgical robots are ushering in a new round of iteration in minimally invasive surgical techniques: On one hand, they enhance the precision of surgical treatment, ensuring surgeons’ high-quality visibility and maneuverability for procedures that require meticulous care to avoid damage to surrounding tissues; on the other hand, they reduce the difficulty of manual operations for surgeons. Given that training a qualified surgeon for a specific procedure typically takes two years or even longer, this technology can significantly increase the supply of medical resources. Furthermore, precise operations improve efficiency, benefiting more patients while simultaneously reducing medical costs through economies of scale.

Since the da Vinci surgical robot received FDA approval in 2000, robotic technology has continuously iterated, evolving from multi-port to single-port techniques, and even to natural orifice transluminal endoscopic surgery (NOTES). Surgical robots are becoming increasingly specialized by department. For relatively rigid tissues in orthopedics, neurosurgery, and dentistry, positioning robots standardize surgical procedures. For soft tissues in cardiology, general surgery, vascular surgery, and abdominal procedures, operational robots enhance surgical precision. Numerous domestic technologies are currently pursuing approval from the National Medical Products Administration (NMPA).Surgical robots can drive the sales of disposable consumables through equipment placement, thereby evolving into a business model dominated by consumable sales with equipment as a secondary component, creating the prerequisites for large-scale commercialization. Currently, the procurement cost of each da Vinci system is approximately RMB 20 million, resulting in a very high threshold for hospital adoption. This creates significant potential for future domestic substitution through low-cost alternatives.The surgical robot industry typically follows a "Copy to China" or "Me Too" model, benefiting from mature overseas references and a vast domestic market. However, it also imposes stringent requirements for technological upgrades and prudent patent avoidance strategies. At this stage, the field involves multidisciplinary integration among medicine, communications, and mechanical power engineering, placing extremely high technical demands on upstream components. Consequently, complete domestic substitution remains difficult to achieve in the short term. In the fields of neurosurgery and dentistry, some domestic technologies have already obtained Class III medical device certificates from the NMPA. The industry remains in a phase of rapid development, characterized by strong demand for capital.

Phase VI

Technologies for capturing and analyzing human micro-physiological signal data (such as electroencephalogram waves and neural currents) enable “conscious” communication between humans and machines by outputting data through brain-computer interfaces (BCIs). Companies in this stage are still in a very early exploratory phase, with most research and application trials conducted within universities and hospitals. Examples include using BCIs to deliver neural stimulation for epilepsy treatment and controlling mechanical prosthetic limbs via BCIs. As the most cutting-edge technology currently available, BCI applications are epoch-making in significance. This field is capable of attracting substantial capital investment and generating immense value, representing the “hardest” core technology within the digital healthcare sector.

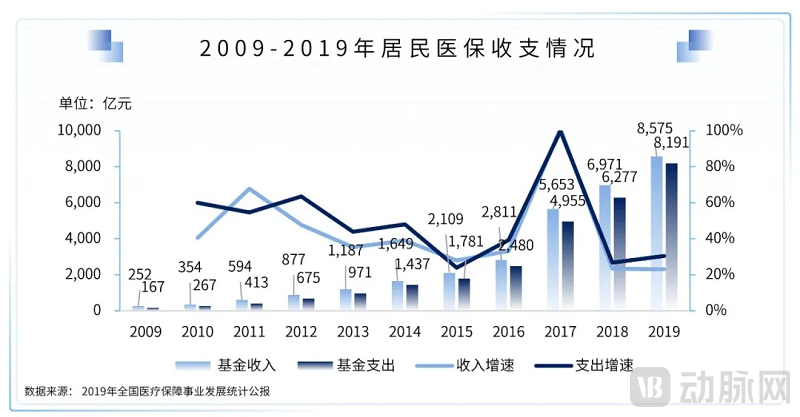

According to statistics from the National Healthcare Security Administration, the coverage rate of China’s basic medical insurance (including urban employee basic medical insurance, urban and rural resident basic medical insurance, and the New Rural Cooperative Medical Scheme) has remained stable at over 96.8% (as of January 2021), basically achieving universal coverage for all eligible individuals.

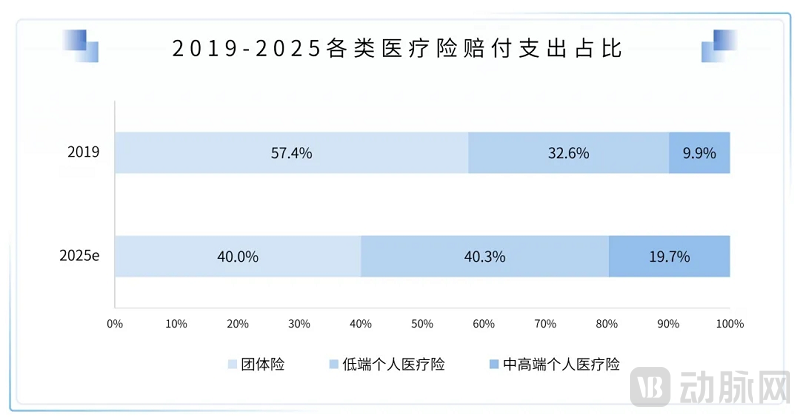

Another set of data shows that the original premium income from health insurance reached RMB 817.3 billion in 2020, accounting for 18% of total premium income, with a five-year historical CAGR of 19%. Among these, critical illness insurance accounted for 60%, and medical insurance accounted for 23%. Meanwhile, the original insurance claim payouts in 2020 amounted to RMB 292.1 billion, representing a year-on-year increase of 24%.

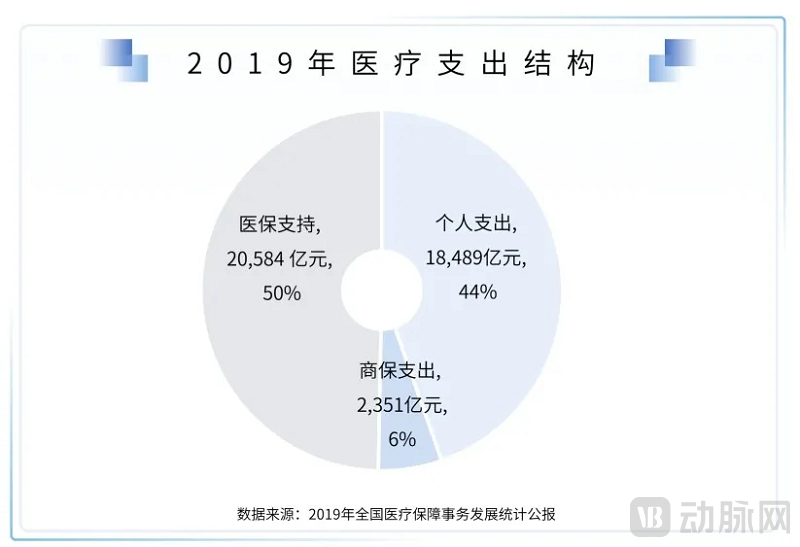

In the overall structure of healthcare expenditure in 2019, medical insurance spending remained the largest component, accounting for 50%, while commercial health insurance spending rose from 4% in 2018 to 6%.

The above data reflect three facts:

· The revenue of the national medical insurance has reached a bottleneck, with limited room for future growth; meanwhile, medical insurance expenditures are increasing year by year, gradually approaching the upper limit of payouts.

· Commercial health insurance is growing rapidly, but its share of total social claims remains low, and it has yet to exert significant influence.

· Residents face immense pressure from personal medical expenditures, with poverty relapse due to illness being widespread, thereby affecting social stability.

Addressing the root causes of high out-of-pocket medical expenses for residents has long been a key national priority. The solution requires a dual approach: tackling both supply and demand dynamics, and enhancing risk pooling—specifically, leveraging large-scale mutual aid mechanisms to spread individual risks.

It is unlikely that out-of-pocket expenses currently borne by individuals (primarily those falling outside the scope of the national basic medical insurance pooling fund) will be covered by public medical insurance; instead, they are more likely to be covered by commercial health insurance.

However, the process of commercial health insurance replacing out-of-pocket payments will be protracted. On one hand, as for-profit entities, commercial insurers engage in pre-selection of insured populations, typically excluding or denying coverage for pre-existing conditions, thereby necessitating an initial focus on covering healthy individuals. On the other hand, unlike mandatory social health insurance contributions, participation in commercial health insurance is voluntary and market-driven. Insurers must achieve scale in premium collection, particularly by attracting a larger pool of healthy individuals to spread the risk associated with those who are ill. This market-based supply-and-demand dynamic makes adverse selection highly likely. Consequently, the rational design of commercial insurance products plays a critical role in shaping this substitution process.

We do not believe that China’s commercial health insurance sector will closely follow the trajectory of its U.S. counterpart. While China’s commercial health insurance industry is undoubtedly poised for rapid growth, its scale will remain significantly smaller than that of the United States for a considerable period. The uniqueness of the U.S. market lies in its large base of high-premium policyholders, greater price elasticity for healthcare services and pharmaceuticals, and the government’s willingness to entrust public insurance beneficiaries to commercial insurers. These factors have enabled the emergence of integrated medical-pharmaceutical-insurance closed-loop models within corporate groups, such as Kaiser Permanente’s HMO model and UnitedHealth Group’s PBM model.

Current Challenges in China’s Commercial Health Insurance: Low Premium Volume, Passive Claims Management with Limited Bargaining Power over Services and Pharmaceuticals, and High Customer Acquisition Costs in a Market-Driven Environment. However, recent trends indicate continuous product innovation and strong government support for commercial health insurance. From purely market-driven products such as “Million Medical” insurance to government-led initiatives like “Huimin Bao” (inclusive supplementary medical insurance), the sector is steadily strengthening its foundation.

Over the past five years, fully market-oriented million-yuan medical insurance products have experienced a surge in popularity. Relying on this single phenomenal product, commercial insurance companies have achieved coverage for 90 million individuals, with total premiums exceeding RMB 50 billion in 2020. Similarly, following its inception in Shenzhen, the “Huimin Bao” (inclusive health insurance) scheme has attracted over 8 million policyholders. Since last year, we have also witnessed the emergence of various local Huimin Bao programs backed by local governments, with a continuously growing number of participants and total premiums surpassing RMB 5 billion. Notably, the recently launched “Huhui Bao” in Shanghai has already enrolled over 4 million participants. The model—backed by the Shanghai Municipal Government, allowing payment through personal accounts of Shanghai’s basic medical insurance, and underwritten jointly by nine commercial insurance institutions—represents another significant exploration into using commercial insurance to replace out-of-pocket payments. Although the current Huimin Bao model poses substantial potential risks to insurers (due to severe adverse selection from insurable pre-existing conditions and the conflict between the public-welfare nature of government initiatives and the profit-driven objectives of commercial insurance), and despite the low average premium per policy resulting in a relatively small overall premium volume, it is evident that both the government and commercial insurers share a strong and consistent willingness and determination to collaboratively explore new models.

Large pharmaceutical companies and insurance institutions have proactively established mechanisms linking pharmaceuticals, healthcare services, and insurance. Meanwhile, originator drug manufacturers that lost bids in centralized procurement are exploring new payment models, and the inclusion of a commercial insurance formulary led by the basic medical insurance system has been placed on the agenda. In recent years, the concept of a commercial insurance formulary covering drugs outside the national reimbursement drug list (NRDL) has repeatedly been proposed. With the implementation and phased achievements of volume-based procurement (VBP) under the basic medical insurance system, this topic has once again become a focal point in discussions between insurers and government authorities. Commercial health insurance typically operates on a passive, post-service reimbursement model, often serving as supplementary coverage after reimbursement through public hospitals at tier II or above, with covered drugs generally required to fall within the NRDL scope. From a fundamental perspective, the commercial insurance formulary serves as a robust complement to the NRDL. However, in the absence of strong oversight from hospitals and the basic medical insurance system, “how to implement effective risk control” remains a significant challenge.

Taking originator drugs as an example, after the implementation of volume-based procurement (VBP), a large number of originator drugs failed to win bids. As VBP expands its scope, this phenomenon will become even more prevalent. Originator drugs boast superior manufacturing processes and more stable quality. Although domestically produced drugs that have won bids have passed the consistency evaluation and are close to originator drugs in most indicators, there are still certain differences in clinical efficacy. Therefore, originator drugs retain certain market value. However, as healthcare cost containment is a national strategy, originator drugs must inevitably seek alternative payers rather than relying solely on out-of-pocket payments by patients. Commercial health insurance serves as an ideal payer. Currently, the scale and fragmentation of China’s commercial health insurance market are insufficient to enable broad-based price reduction negotiations with originator pharmaceutical companies. In the future, one possible scenario is that the National Healthcare Security Administration would lead various insurance companies in jointly formulating a commercial insurance drug formulary and participating in negotiations with pharmaceutical manufacturers. This approach would not only provide a payment buffer for originator drugs but also create room for the development of commercial health insurance, ultimately improving accessibility to high-quality medicines for residents.

At present, the “digital healthcare-pharmaceuticals-insurance” closed loop is taking shape in certain specialty fields or among specific consumer segments, but overall it is far from reaching a stage where a true “industry-wide grand closed loop” can be realized. Even after such a grand closed loop is established, social insurance will still play a pivotal role within it, with commercial insurance serving merely as a supplement.

China’s digital health industry, characterized by its innovation and forward-looking nature, faces significant policy lag. Unlike traditional healthcare, it cannot easily gain hospital access and secure medical insurance reimbursement within the existing policy framework. Consequently, payment mechanisms exert a profound impact on the digital health sector, particularly during the early to mid-stages of enterprise development, where even superior products must carefully consider appropriate commercialization and payment strategies.

In the current digital health industry, the suitable model lies in the rational intersection of payers and customer acquisition scenarios, with the ultimate goal of business models being scalable monetization. At present, the singularity of payers in the healthcare industry and their clear demand for cost containment are quite unfavorable to digital medical health. Therefore, during the development stage of digital medical health, it is necessary to clearly identify who the users are while simultaneously leveraging their ability to pay.

Medical Insurance

As the largest payer, the primary current demand is cost containment. Once digital health products can verify their cost-containment capabilities and are included in the tender catalog, they offer guaranteed stability, making them a highly contested strategic market.

Pharmaceutical (Medical Device) Companies

As the most flexible payer currently, the primary demands are in the research and development, market access, and volume growth of pharmaceuticals and medical devices. Digital health products can strategically focus on specific stages of the product lifecycle of pharmaceutical and medical device companies to foster collaborative development.

Health Insurance

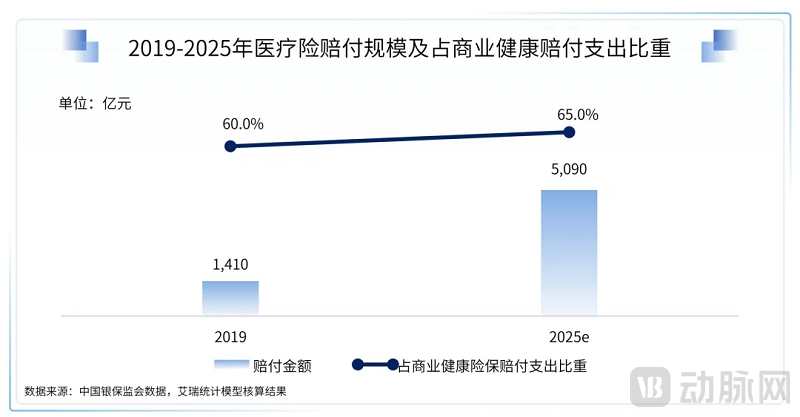

In 2020, the total amount of health insurance claims reached RMB 292.1 billion, a year-on-year increase of 24%. The two largest segments of health insurance are critical illness insurance and medical expense insurance. Critical illness insurance is an indemnity-type product with limited impact and correlation to the digital health industry; whereas medical expense insurance is a reimbursement-type product that is highly correlated with the quality and pricing of healthcare services, serving as the primary payer. As the most promising payer over the next five years, the current primary demand for health insurance lies in achieving premium scale growth under controlled risk.

Taking million-yuan medical insurance as an example, this blockbuster product in the individual medical insurance market generated over RMB 50 billion in total premium income in 2020. However, population penetration has slowed, and growth has peaked. Future sustained growth will rely more on sales strategies such as converting short-term policies to long-term ones and transitioning from individual to family coverage.

To leverage health insurance payments, digital health products must either provide differentiated services within insurance offerings, enable granular pricing capabilities for the design of insurance products covering substandard or even uninsurable risks, or continue to serve as a channel that delivers a large volume of precise customers and facilitates transactions for existing insurance products.

C-end scenarios (Internet user traffic scenarios)

Pure consumer-facing (C-end) traffic, as a fully marketized resource, has been dominated by major traffic platforms. Meanwhile, healthcare is a relatively low-frequency scenario, making it highly susceptible to "dimensional reduction attacks" where high-frequency platforms overpower low-frequency ones. Consequently, in pure C-end scenarios, even if major traffic platforms suffer from late-mover disadvantages and delayed awareness, they can still replicate market-validated models and leverage traffic allocation to support their proprietary businesses, maintaining a high probability of eventual dominance. Furthermore, for pure C-end models embedded within these major traffic platforms, unless they possess strong brand competitiveness in products or services, they are highly likely to face suppression and traffic restrictions by the platforms in the future, thereby lacking sufficient room for growth.

Taking the B2C pharmaceutical e-commerce industry as an example, self-operated B2C pharmaceutical e-commerce platforms require continuous customer acquisition efforts. Due to the high demand for customer precision and consumers’ price sensitivity towards standardized pharmaceutical products, customer churn is high. This results in persistently elevated customer acquisition costs at scale, making it difficult for Customer Lifetime Value (LTV) to cover expenses, thereby posing significant financial challenges. Currently, among self-operated B2C pharmaceutical e-commerce platforms, only Alibaba Health and JD Health are expected to sustain profitability. Other independent platforms either maintain a small scale to break even, get acquired, or exit the market entirely.

Furthermore, although third-party B2C pharmaceutical e-commerce platforms primarily rely on public-domain traffic from high-traffic platforms and low-cost customer acquisition, with many having already achieved break-even or profitability, they face significant long-term challenges. On one hand, they are subject to traffic cannibalization by the platforms’ own self-operated mega-pharmacies; on the other hand, they contend with intense price competition from peers. Additionally, these platforms are unable to divert customers away from the transaction ecosystems. If they fail to promptly explore new growth models, their corporate valuation will face substantial challenges in the future.

Certainly, the core supply chain assets of pharmaceutical e-commerce companies may become acquisition targets for large platforms seeking to enter the digital health industry in the future, although their valuation logic may change.

H-side Scenarios (Hospital Scenarios)

Pure hospital-side traffic is a specialized resource. Acquiring such resources often demands strong public relations capabilities; once secured, they tend to exhibit exclusivity and monopolistic characteristics, thereby creating competitive barriers. However, this model lacks the ability to be rapidly replicated, with most players ultimately becoming regional leaders. Examples include listed companies such as Neusoft and Winning Health, which emerged during the wave of hospital informatization, as well as numerous regional firms of varying sizes.

Furthermore, in the current hospital-side (H-end) scenario, large hospitals hold significant bargaining power and exhibit limited willingness to act as payers. Since business models based purely on the H-end scenario require certain fixed-cost investments for implementation, it is necessary to identify alternative payers to achieve financial revenue.

Generally scalable revenue channels include commissions on transaction service fees for pharmaceuticals and medical devices, as well as marketing expenses from pharmaceutical and medical device companies, resembling the U.S. Pharmacy Benefit Manager (PBM) model. Meanwhile, merely securing hospital resources is often insufficient to realize these revenues; as complex entities, hospitals involve intricate decision-making processes, which impose high demands on the top-level design of a company’s business model.

D-side Scenario (Physician Scenario)

Pure D-side traffic is a semi-proprietary, semi-marketized resource. On one hand, it still requires certain public relations efforts to build trust; on the other hand, it exhibits a degree of replicability. However, it lacks exclusivity and monopolistic characteristics, making it highly susceptible to migration across various platforms.

Furthermore, patient volume is concentrated primarily in the hands of physicians at large public hospitals. As Chinese doctors remain employees of public medical institutions and cannot practice independently as their American counterparts do, they are subject to stringent administrative control by their hospitals. This limits their participation in external commercial activities and exposes them to significant professional liability, forcing them to carefully weigh benefits against risks. Although transparent, compliant income is a key demand among physicians, adhering to the principle that “wealth should be acquired through proper means,” most doctors remain highly cautious about new revenue streams, with the exception of already validated models such as service fees from online consultations on digital health platforms.

Taking a chronic disease management platform oriented toward the outflow of physician prescriptions as an example, although it has registered over 1 million physicians, only 1% are active prescribers. Due to persistently high fixed costs associated with physician operations and maintenance, low personnel efficiency, and the need for physician incentives, the platform has remained in a state of long-term financial loss. Its unit economics are insufficient to support a sustainable profit model. Without further exploration and transformative changes in conversion strategies, the business may continue to rely on capital injections for survival.

I-Side Scenarios (Insurance Scenarios)

Pure Channel I traffic is a semi-marketized and semi-proprietary resource, with its core originating from insurers’ robust offline agent teams or partnered traffic platforms, acquiring user traffic through individual and group insurance lines.

Among these, offline agent traffic is characterized by high average transaction value and high repurchase rates, while internet traffic is distinguished by its broad reach and younger demographic. Through thoughtful design, digital health products can be offered as value-added services to insurance policies or integrated directly into them (with service fees not exceeding 20% of the total premium), thereby effectively addressing challenges related to customer acquisition and payment. However, this is contingent upon meeting the requirements of insurance companies. Nevertheless, with such back-to-back bundling arrangements, insurers often demand certain equity or controlling interests. Consequently, digital health enterprises inevitably face the dilemma of taking sides, requiring them to make trade-offs between the breadth and depth of their business development.

Using “Ping An RUN” as a classic case study of insurance companies developing digital health products:

Ping An RUN belongs to the “Ping An Le Jiankang” product series of Ping An Health Insurance. It is the first health management product in China, built upon the Vitality system of South Africa’s Discovery Limited. The primary function of Ping An RUN is that, after users pay an annual fee, they can directly redeem rewards through healthy behaviors (such as step counts). The total value of the rewards available far exceeds the annual fee, thereby encouraging users to exercise more, enhancing user engagement, and raising health awareness. Meanwhile, physical activity positively impacts individual health; upon policy renewal, individuals may benefit from increased coverage amounts, premium refunds, and other incentives (with certain versions offering insurance discounts of up to 30%). Ping An RUN was initially launched as a bundled feature embedded within the Ping An Fu life insurance product. When selling life insurance through agent channels, agents guided customers to activate the Ping An RUN feature, with the annual fee covered by the life insurance premiums. In the early stages, when competition in the life insurance market was less intense, Ping An Fu achieved strong sales, but insurance agents expressed considerable reservations about the tied selling of Ping An RUN. Later, as market competition intensified, Ping An Fu life insurance with the Ping An RUN feature became a differentiated product in the market, evolving into a signature offering. Reportedly, the total value of rewards circulated through Ping An RUN exceeds RMB 1 billion annually.

This case is highly unique. Ping An RUN achieved its subsequent growth precisely because, as a proprietary product of Ping An, it received vigorous administrative promotion from within Ping An Life Insurance. Had it been a collaborative product with no equity-level ties, it might have failed at the outset when encountering initial promotional resistance.

P-End Scenario (Pharmacy Scenario)

Traffic from pharmacy-end (P-end) scenarios represents a highly market-oriented resource and is currently an undervalued customer acquisition channel. This is largely attributable to the absence of digital health products well-suited to this traffic segment. According to data from the Annual Statistical Report on Drug Supervision and Administration (2020), released by the Department of Comprehensive Planning and Finance and the Information Center of the National Medical Products Administration, there were 550,000 pharmacy outlets across China as of the end of 2020. Among these, 240,000 outlets belonged to chain pharmacies (corresponding to approximately 6,000 chain headquarters), resulting in a chain affiliation rate of 56%.

In the pharmacy sector, conventional pharmacies primarily serve patients with chronic diseases, whereas DTP (Direct-to-Patient) pharmacies mainly cater to oncology patients, offering a more precisely defined user base. Furthermore, regarding resource expansion, chain pharmacies benefit from centralized management by their headquarters. In principle, coordinating with the provincial branch headquarters enables access to all stores across the province, with dedicated personnel liaising with individual stores for specific implementation, thereby achieving high expansion efficiency.

Traffic in general pharmacy scenarios has the following characteristics:

· The majority are individuals with pre-existing conditions.

· The majority are middle-aged and elderly.

· In most cases, the pharmacy setting represents the terminal end of medical care delivery and a passive point of revenue generation.

·Pharmacy staff have limited ability to sell non-pharmaceutical products.

Currently, there are few digital health products on the market targeting pharmacy-based (P-end) scenarios. This may be because the most common and scalable monetization model in the digital health industry at present is pharmaceuticals, which conflicts with the core business of pharmacies. Some insurers have attempted to sell insurance products in pharmacies but encountered difficulties. The primary obstacle was that pharmacy customers often include individuals with pre-existing conditions, resulting in low conversion rates. Consequently, these insurers shifted to offering low-cost, small-amount complimentary insurance policies to acquire underwriting information from users at a low cost, enabling subsequent secondary development.

Some insurtech companies are also deploying innovative payment products through on-site sales at pharmacies. The monetization point remains within the pharmacy, attracting patient participation through discounts, with cost support provided by pharmaceutical companies or insurers. Whether this model can achieve financial viability at scale remains to be seen. We look forward to more innovative digital health products integrating with pharmacy scenarios in the future.

As previously mentioned, it is essential to adopt a dynamic perspective, as patterns only yield synergistic effects under appropriate conditions. Based on a rational cross-analysis of current payers and traffic scenarios, we present the following insights for the digital health industry:

The user scenario prioritizes hospitals and physicians, addressing challenges in traffic acquisition and conversion; meanwhile, payment solutions prioritize pharmaceutical companies and medical insurance, supporting scalable expansion through enhanced efficiency and stability.

Pure C-end Scenario Mode Remains Neutral

>>>>

Optimistic about model exploration in combined H+D scenarios

· Full-course disease management for specific conditions, including digital-assisted diagnosis and treatment

· Digital medical technologies for specialized disease categories, including surgical robots and brain-computer interface technologies applied in specialized departments

· Co-building Departments: Empowering Under-resourced and Less Experienced Departments through Enhanced Medical Management Capabilities and Clinical Expertise Transfer

· The aforementioned models need to be supported by medical insurance reimbursement, pharmaceutical company payments, and, to a certain extent, departmental funding.

·Under the framework of "H as the core and D as the supplement," we recommend exploring models with substantial monetization capabilities for pharmaceuticals and medical devices, such as prescription circulation models based on public hospitals and their spin-off self-pay pharmacies (similar to PBM), as well as models that enable pharmaceutical companies to participate in market access and adherence management on this basis.

·Under the premise of prioritizing D with H as a supplement, it is recommended to explore disease management models endorsed by public tertiary Grade-A hospitals.

In the I-end scenario, models with the ability to drive incremental market growth are recommended.

· Standard Entity: Insurance (brokerage) platforms capable of capturing differentiated traffic or enhancing conversion rates

· Subheading: InsurTech Leveraging Disease Big Data for Risk Control to Enable Product Pricing and Output Capabilities

· Non-underwritten population: Severe adverse selection; business model remains to be validated. Maintain a neutral stance toward the current models of payment shifting via innovative payment solutions and market-oriented operation of city-specific supplemental medical insurance (Huiminbao).

B2B Scenarios: Focusing on Pre- and Post-Clinical Trial Contexts for Pharmaceutical Companies

· AI Drug Discovery and Development

· Digital Marketing for Pharmaceutical and Medical Device Product Access and Volume Growth

IMPORTANT STATEMENT

Each research analyst who is primarily responsible for drafting all or part of this research report hereby declares:

(1) Any views expressed in this report accurately reflect the author’s personal opinions on the industry and companies;

(2) The analyst has not, does not, and will not receive any compensation for the views or recommendations expressed in this report.

This research report is intended solely for use by our clients and partners. Except for disclosures related to China Renaissance Capital, this report is based on publicly available information that we consider reliable; however, we do not guarantee the accuracy or completeness of such information, and clients should not rely on it as being accurate or complete. We update our research from time to time when possible. In addition to certain industry reports published on a regular basis, the majority of our reports are published on an ad hoc basis as deemed appropriate by our analysts.

Our investment banking personnel, sales staff, and other professionals may provide our clients with oral or written market commentaries or trading strategies that are contrary to the views expressed in this research report. Our asset management division may make investment decisions that are inconsistent with the recommendations or opinions expressed in this report.

This report does not constitute explicit or implicit investment advice, nor does it take into account the specific investment objectives, financial conditions, or needs of individual clients. Clients should consider whether any opinions or recommendations in this report are suitable for their particular circumstances and, if necessary, seek professional advice, including tax advice.

Selected research reports are published as electronic publications on our internal client portal and WeChat official account, and are made available simultaneously to all clients and partners. Not all research content is forwarded to our clients or provided to third-party aggregators, and we assume no liability for any of our research reports redistributed by third-party aggregators.

China Galaxy Capital makes no commitment that it has not had, does not have, or will not have business relationships with the companies mentioned in this report, or that it will not pursue business opportunities related to them.

This report is copyrighted by China Renaissance Capital. No part of this material may be (i) reproduced in any form or by any means, including photocopying or duplication, or (ii) redistributed for commercial purposes, without the prior written consent of China Renaissance Capital.