Peptide Drug Developer SinoBiopharmaceutical Debuts on STAR Market with 352.51% Surge

On June 3, 2021, Sinotech Biologics, a developer of peptide-based drugs, listed on the STAR Market. The company’s IPO price was RMB 17.9 per share, with 20 million RMB-denominated ordinary shares offered to the public. Its stock surged to RMB 81 at the morning open, representing a gain of 352.51%.

Image source: Sina Finance

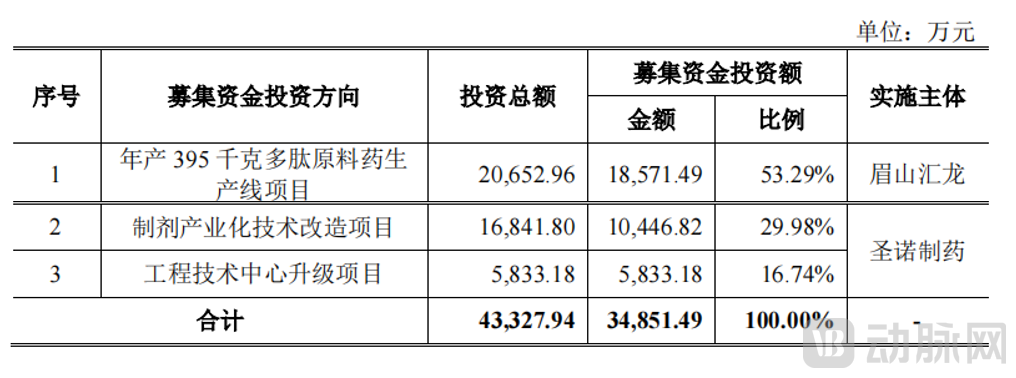

Upon its listing on the STAR Market, Chengdu Shengnuo Biopharm Co., Ltd. will primarily allocate the raised funds to three projects: the construction of a production line with an annual capacity of 395 kilograms of peptide active pharmaceutical ingredients (APIs), the technological transformation for industrialization of formulations, and the upgrading of its engineering technology center.

Shengnuo Biopharm's Use of Proceeds from Fundraising (Source: Company Prospectus)

Chengdu Sinotech Bioscience Co., Ltd. (hereinafter referred to as “Sinotech Bioscience”)Established in July 2001 and located in Dayi County, Chengdu, it is one of the earliest professional peptide drug manufacturers in China. The company possesses core technologies for peptide synthesis and modification, with advanced and efficient capabilities in process development and large-scale production of peptide drugs.The company is primarily engaged in the research and development, production, and sales of peptide active pharmaceutical ingredients (APIs) and formulations. It also provides pharmaceutical research services for innovative peptide drugs and custom manufacturing services for peptide-based products to enterprises.It is one of the few companies in this field with a full industry chain layout encompassing the research and development, production, and sales of peptide active pharmaceutical ingredients (APIs) and formulations.

As disclosed in the prospectus, process development and manufacturing capabilities for peptide drugs constitute Shengnuo Biopharm’s core competitive advantages and the foundation of its business development. Currently, the company has mastered scaled-up production technologies for 15 peptide active pharmaceutical ingredients (APIs), among which 7 have obtained marketing authorization in China and 8 have achieved activated status under U.S. Drug Master File (DMF) filings. Furthermore, eight extended-developed peptide drug products have secured 12 marketing authorizations in China. Its product portfolio covers therapeutic areas where peptide drugs play a significant role, including immunology, gastroenterology, antiviral therapy, obstetrics and gynecology, diabetes, cardiovascular and cerebrovascular diseases, rare diseases, and orthopedics.

The company’s peptide formulations, enfuvirtide for injection and carbetocin injection, are the first domestically produced generic peptide drugs in China. Generic active pharmaceutical ingredients (APIs) with high synthetic complexity, including bivalirudin, liraglutide, thymalfasin, icatibant, and enfuvirtide, have been exported to international markets such as Europe, the United States, India, and South Korea. End customers include well-known pharmaceutical companies both domestically and abroad, such as Fresenius, Aurobindo, Mylan, Lupin, Salubris, Shanghai First Biochemical Pharmaceutical, and Yangtze River Pharmaceutical Group.

Peptides(Peptides) are compounds formed by multiple amino acids linked together via peptide bonds. Their linkage pattern is identical to that of proteins. Molecules containing fewer than 100 amino acids are typically referred to as polypeptides, while those with more than 100 amino acids are classified as proteins. Peptide drugs represent a new class of therapeutic agents derived from the pharmaceutical application of peptides. Their molecular size falls between that of small-molecule chemical drugs (MW < 500) and protein-based biologics (MW > 10,000), thereby combining certain characteristics of both.

Compared with protein-based drugs such as monoclonal antibodies and recombinant proteins, peptide drugs offer advantages including simpler spatial structures, higher stability, and lower or non-existent immunogenicity, while retaining the high specificity and efficacy characteristic of protein therapeutics. In comparison with small-molecule chemical drugs, peptide drugs demonstrate superior biological activity and specificity, as well as greater potential in addressing complex diseases. Furthermore, the manufacturing processes for peptide drugs share similarities with those for small-molecule drugs, featuring controllable quality, easily verifiable structures, and lower production costs.

The quality control standards for peptide drugs are comparable to those of small-molecule chemical drugs, while their biological activity is similar to that of protein-based therapeutics. By combining the advantages of both, peptide drugs demonstrate superior performance in clinical applications and manufacturing processes, making them suitable for addressing complex diseases that are difficult to treat with small-molecule chemical drugs, including metabolic disorders and cancer.

Although the R&D process for peptide drugs is similar to that of traditional small-molecule drugs, they exhibit unique differences in process design, manufacturing methods, structural elucidation, quality studies, and R&D and production equipment. In particular, scaling up from gram-level laboratory preparation to kilogram-level commercial production poses significant challenges. Therefore, scalable manufacturing has become a key factor in the commercialization of peptide drugs, with chemical synthesis currently being the primary approach for their large-scale production.

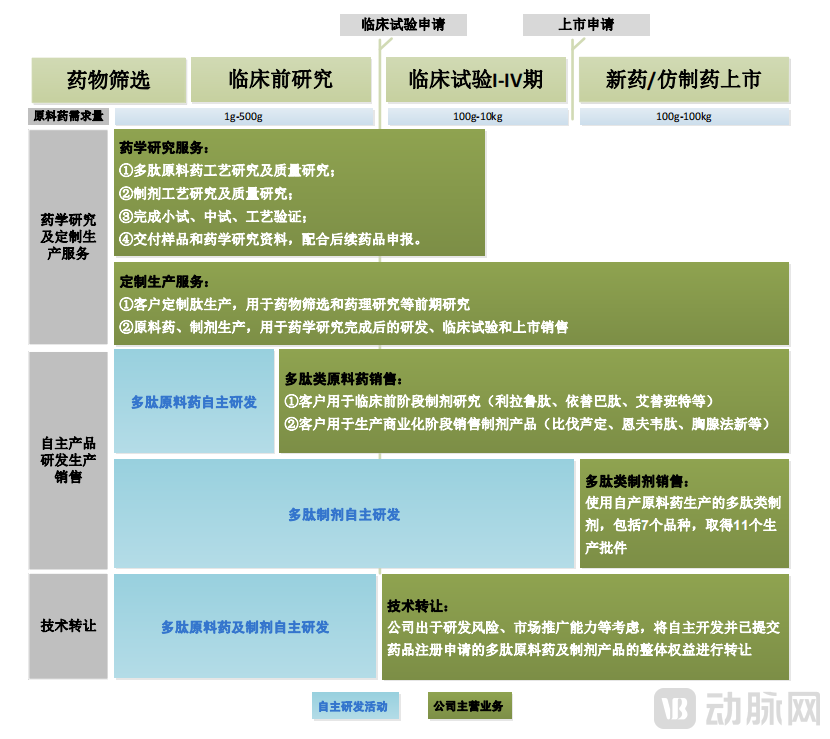

Chengdu Shengnuo Biopharm Co.,Ltd. employs chemical synthesis for the research, development, and production of peptide drugs. Its core business leverages scalable process R&D and manufacturing capabilities based on peptide synthesis and modification technologies, with products and services covering the entire lifecycle of peptide drugs—from drug screening, preclinical studies, and clinical trials to commercialization.The stages in which the company’s main products and services are positioned are shown in the figure below:

(Image source: Shengnuo Biopharm’s IPO prospectus)

According to the prospectus, Shengnuo Biopharm's operating revenue is primarily derived from pharmaceutical research and custom manufacturing services for peptide drugs, peptide active pharmaceutical ingredients (APIs), peptide formulation products, as well as contract manufacturing of levosimendan formulations and the production and sales of its APIs.

Shengnuo Biopharm Financial Data (Source: Company Prospectus)

From 2018 to 2020, Chengdu Shengnuo Biopharm Co.,Ltd. reported operating revenues of RMB 278 million, RMB 327 million, and RMB 379 million, representing year-on-year growth rates of 17.54% in 2019 and 15.92% in 2020. Selling expenses amounted to RMB 114 million, RMB 167 million, and RMB 182 million respectively, with year-on-year increases of 45.87% in 2019 and 9.05% in 2020. The ratio of selling expenses to operating revenue for the three years was 41.12%, 51.03%, and 48.01%, respectively.

Among these, the promotion expenses for the formulation business, one of Shengnuo Biopharm’s core operations, accounted for more than 84% of its operating revenue. The revenue from this segment contributed gross profits of RMB 8.7371 million, RMB 15.7419 million, and RMB 17.6812 million, respectively. In its prospectus, Chengdu Shengnuo Biopharm Co., Ltd. disclosed that product promotion expenses represented over 95% of its total selling expenses.

Whether Shengnuo Biopharm has issues with excessively high marketing expenses and insufficient R&D investment sparked widespread discussion across major media outlets when the company submitted its prospectus. Many media reports characterized Shengnuo Biopharm as “heavy on marketing, light on R&D.”

In fact, compared with listed companies in the same industry, although Shengnuo Biopharm’s selling expenses as a percentage of operating revenue were higher than the industry average during the reporting period, they were not the highest in the industry. In addition, Shengnuo Biopharm stated in its prospectus that comparable companies in the industry, such as Asymchem, Porton PharmaSolutions, and Pharmaron, are primarily engaged in custom research, development, and manufacturing services and are not involved in the domestic sales of formulated drugs; therefore, they do not incur marketing and promotion expenses, resulting in lower selling expense ratios.

In its explanation of the use of raised funds, the company also partially addressed the issue of excessively high marketing expenses for its formulation products. Chengdu Shengnuo Biopharm Co.,Ltd. stated that as a latecomer in China’s polypeptide formulation market, the company faces significant competitive pressure. Since it has not yet established an in-house marketing team, it relies on professional third-party promoters for market outreach, resulting in a substantial burden of marketing expenses for its formulation products.

Therefore, we may speculate that the company aimed to capture a certain market share while developing its products to maintain their competitiveness; however, due to the lack of an in-house marketing team, its financial performance regarding product promotion expenses appears less favorable. Nevertheless, even when analyzing Chengdu Shengnuo Biopharm Co., Ltd.’s R&D investment alone, there remains considerable room for improvement.

Shengnuo Biopharm Financial Data (Source: Company Prospectus)

Based on the prospectus data, it can be observed that from 2018 to 2020, Shengnuo Biopharm’s R&D expenses accounted for 5.64%, 3.55%, and 5.94% of its annual revenue, respectively. Calculations show that the company’s cumulative R&D investment over these three years represented 5.06% of its cumulative operating income for the same period, precisely meeting the threshold set forth in the “Guidelines for Evaluating Sci-Tech Innovation Attributes (Trial)” which requires that “cumulative R&D investment over the most recent three years accounts for more than 5% of cumulative operating income over the same period.” As a technology-driven enterprise, Shengnuo Biopharm may find it more advantageous to prioritize product development in order to sustain its competitiveness in future growth.

Shengnuo has five core technical personnel, all of whom possess over 15 years of research and practical experience in the field of peptide synthesis. The team was previously awarded the title of "Top Innovation and Entrepreneurship Team" under Sichuan Province's High-Level Talent Introduction Program.

Wen Yongjun, Chairman & Chief Scientist of Shengnuo BiopharmHe is one of the earliest experts in China to conduct research in the field of peptide drugs. He led the development of thymopentin, the first peptide drug approved by the state and granted a New Drug Certificate in China, and spearheaded the first domestic generic version of thymalfasin. He has successively received the “Outstanding Contribution Award for Peptide Applications” at the 10th and 12th International Peptide Symposia, as well as the “Outstanding Talent Award” at the 2nd National Frontier Technology Exchange Conference on Peptide Drug R&D and Large-Scale Production. In 2018, he was selected for the Sichuan Tianfu Entrepreneurial Leading Talent Program.

In terms of facility construction, the R&D Center of Shengnuo Biopharm has established 2,150 square meters of R&D laboratories for novel peptide drugs, peptide raw materials, and related peptide products, compliant with Good Laboratory Practice (GLP) standards. The center is also equipped with a wide array of advanced R&D instruments, including internationally state-of-the-art specialized equipment such as the fully automatic CS936 series peptide synthesizers imported from the United States, Switzerland, and Japan; Agilent liquid chromatography-mass spectrometry (LC-MS) systems; Waters ultra-performance liquid chromatography (UPLC) systems; PerkinElmer polarimeters; and dynamic axial compression column (DAC) systems of various specifications.

Currently, Shengnuo Biopharm has established a coordinated R&D mechanism encompassing information collection, feasibility analysis, project initiation, and R&D process management. This system ensures the smooth and efficient execution of all operational stages in the product development lifecycle—including project initiation, process and quality research, laboratory-scale trials, pilot-scale trials, scaled-up manufacturing, and product registration—thereby accelerating product submission and market launch.

Chengdu Shengnuo Biopharm'sIts main product portfolio spans multiple therapeutic areas, including digestive system disorders, immune-mediated diseases, oncology, chronic hepatitis B, diabetes, and obstetrics.It is one of the domestic manufacturers with a relatively comprehensive product line of peptide-based drugs.

In overseas markets, the company has eight products—bivalirudin, eptifibatide, icatibant, liraglutide, octreotide acetate, ziconotide, teriparatide, and ganirelix—with active Drug Master File (DMF) filings in the United States. In the domestic market, the company has obtained 19 drug registration approval numbers or domestic filings for peptide drugs in China, including eight peptide active pharmaceutical ingredients (APIs) and twelve peptide formulation specifications. It is the first domestic company to develop generic versions of two formulation products: enfuvirtide and carbetocin.

Currently, Chengdu Shengnuo Biopharm Co., Ltd. has 11 products under application for registration approval, with more than ten additional peptide drug products in the research and development stage. The company disclosed in its prospectus that it plans to further expand and diversify its product portfolio in the future.

Through independent research and development, Chengdu Shengnuo Biopharm Co., Ltd. has mastered core proprietary technologies for peptide synthesis and modification, including long-chain peptide conjugation technology, large-scale production technology for mono-disulfide cyclic peptides, synthesis technology for multi-disulfide cyclic peptides, fragment condensation technology, PEGylation modification technology, and fatty acid modification technology. The company has successfully resolved technical bottlenecks in the large-scale production of various peptide active pharmaceutical ingredients (APIs), such as enfuvirtide, liraglutide, teriparatide, and exenatide. Furthermore, it has overcome process challenges associated with excessive impurity levels caused by complex structural features, such as multiple disulfide bonds and cyclic peptide structures, in products like ziconotide and linaclotide.

Currently,The company's peptide active pharmaceutical ingredient (API) products have been exported to multiple countries and regions, including Europe, the United States, South Korea, and India.Notably, the active pharmaceutical ingredient (API) of bivalirudin supported Fresenius’s product in becoming the second approved generic drug of this variety in the U.S. market; this formulation achieved sales of USD 53.155 million in the United States in 2018, capturing a market share of 21.71%. The APIs of enfuvirtide and thymalfasin respectively supported clients’ generic products to be marketed in Mexico and South Korea. The APIs of icatibant and ziconotide were the first to complete the submission of Drug Master Files (DMFs) for generic APIs to the U.S. FDA. Additionally, APIs for eight varieties, including liraglutide, have supported clients’ formulation development in preparation for market launches in the United States and Europe.

As of now, Chengdu Shengnuo Biopharm Co.,Ltd. has established business relationships with well-known multinational pharmaceutical companies, including Fresenius, Aurobindo, Mylan, and Lupin.

Leveraging its extensive R&D experience in the field of peptide active pharmaceutical ingredients (APIs), Chengdu Shengnuo Biopharm Co., Ltd. also provides pharmaceutical research services for innovative peptide drugs and custom manufacturing services for peptide-based products.As disclosed in its prospectus, Chengdu Shengnuo Biopharm has provided pharmaceutical research and development services for more than 30 Class I innovative peptide drug projects, among which one product has been approved for marketing and seven have entered clinical trials. Its clients in new drug R&D include well-known innovative pharmaceutical companies and research institutions such as Bio-Thera Solutions, Suzhou PegBio, and Bajia Yi.

Although China’s peptide drug market started relatively late, it has experienced rapid growth, with sales rising from RMB 5.6 billion in 2009 to RMB 29.56 billion in 2017, representing a compound annual growth rate (CAGR) of 23.12%, which is significantly higher than the overall growth rate of the global peptide drug market.

According to QYResearch statistics, the global peptide drug market size was approximately USD 15.2 billion in 2010 and reached USD 28.5 billion by 2018, with a compound annual growth rate (CAGR) of 8.17%. Compared to the global pharmaceutical market size of approximately USD 1.3 trillion in 2018, the peptide drug market accounted for only 2.19%, andThe growth rate of the peptide drug market is approximately twice that of the overall global pharmaceutical market.The peptide drug market is projected to grow at a compound annual growth rate (CAGR) of 7.9%, reaching a market size of $49.5 billion by 2027.

Currently, dozens of peptide drugs have demonstrated significant clinical efficacy and broad application prospects in the global market. Many peptide products have achieved annual sales exceeding hundreds of millions of dollars within just one to two years after launch. In 2016, there were six peptide drugs with global annual sales surpassing $1 billion each, such as Teva Pharmaceutical Industries’ glatiramer acetate, which accounted for 20% of the multiple sclerosis market and generated approximately $4.2 billion in global sales; and Novo Nordisk’s liraglutide, used for the treatment of type 2 diabetes, with sales exceeding $2.8 billion.

According to data from pharmaceutical research institutions EvaluatePharma and PDB, the market sizes for orphan/rare diseases, oncology, and diabetes within the peptide drug sector all exceed USD 3 billion. The remaining four therapeutic areas—gastrointestinal, orthopedics, immunology, and cardiovascular/cerebrovascular diseases—have relatively smaller market sizes, although they do include individual blockbuster drugs.

Significant Opportunities Lie Ahead in the Development of New Peptide Formulations in ChinaCurrently, nearly half of the peptide drug molecules marketed globally have not yet been launched in China. The utilization rate of the top ten global best-selling peptide products remains relatively low in China. Peptide drugs hold vast market potential and significant growth opportunities in domestic therapeutic areas such as oncology and diabetes.

In terms of market distribution, there are more than 40 peptide drugs currently marketed in China, primarily spanning seven major therapeutic areas: immunology, gastroenterology, oncology, orthopedics, obstetrics, diabetes, and cardiovascular diseases. Among these, immunological agents dominate the market, accounting for over 50% of the domestic share. Gastrointestinal and anticancer drugs follow, each representing approximately 20%. The markets for orthopedics, obstetrics, diabetes, and cardiovascular diseases are relatively small, collectively comprising only 7% of the total market. These segments are still dominated by primary products and have not yet reached maturity.

From a global perspective, 85% of the peptide market is concentrated in the treatment of chronic diseases such as cancer and diabetes, while emergency and surgical adjuvant medications account for only about 15%. Chronic disease treatment represents the true lucrative segment of the peptide industry. In contrast, China’s peptide market is dominated by short-term or emergency medications used in immunology, gastroenterology, obstetrics, and cardiovascular care (including angina and acute myocardial infarction). Treatments for chronic conditions such as cancer, orthopedics (e.g., osteoporosis), and diabetes account for only 26% of the market share, indicating substantial room for growth.

Overall, China’s peptide drug market remains in a developmental stage. In the coming years, China’s peptide drug industry will continue to be dominated by generic drugs, with innovation primarily focused on the research and development of peptide generics and the improvement and optimization of manufacturing processes.