Why Are Capital Giants Like CBC Group, Hillhouse, and Hony Rushing Into SPACs?

In late May, CB Capital submitted a new prospectus to the U.S. Securities and Exchange Commission (SEC), announcing that Summit Healthcare Acquisition Corp., a special purpose acquisition company (SPAC) sponsored by the firm, is poised to list on the Nasdaq with a planned fundraising target of $200 million. According to the disclosed business strategy, the SPAC will focus on seeking investment opportunities driven by the growing consumer spending power and innovation-led payment capabilities of Chinese patients, primarily targeting the pharmaceuticals, medical technology, and diagnostics sectors.

If the IPO proceeds smoothly, this will become the first SPAC initiated by domestic capital and focused on vertical projects in China’s biopharmaceutical sector amid the global SPAC boom.

SPACs, also known as blank-check companies, are shell entities with no operating business and only cash assets. Their sole purpose is to identify suitable targets, merge with them, and facilitate their public listing. Prospectuses for SPACs typically do not include specific details such as market size or product potential; instead, investors place the greatest emphasis on the sponsors’ and management team’s proven track record in capital markets and their strong ability to integrate industrial resources.

As a result, SPAC sponsors are often prominent figures from various fields. Examples include Chamath Palihapitiya, founder of Social Capital, who transitioned from private equity to SPACs; Richard Li, founder of Pacific Century Group; Albert Leung, former Chairman of Blackstone Group’s Greater China region, who moved from wealth management to SPACs; Adrian Cheng, the third-generation heir to Chow Tai Fook, who leveraged his business operational expertise into SPACs; and Shaquille O’Neal, the “Shaq,” who entered the SPAC space following his illustrious sports career.

According to the plan, the timeframe for completing the acquisition of a target company after a SPAC’s listing is 12 to 24 months. As a result, Buffett jokingly referred to SPACs as “killers,” once remarking, “If you held a gun to my head and forced me to buy another company, I would buy another company.”

SPACs are a unique listing vehicle in European and American capital markets, not a new phenomenon in the capital markets.

As early as the 1990s, U.S. companies began going public using the SPAC structure. However, the absence of clear regulatory guidelines for early-stage SPACs allowed some to facilitate listings for companies with weak intrinsic value, resulting in losses for public investors and drawing significant scrutiny. Since the turn of the millennium, the U.S. Securities and Exchange Commission (SEC) has issued a series of regulatory rules, gradually standardizing SPAC operations.

Typically, a complete SPAC transaction involves several stages, including the sponsor establishing the SPAC, the SPAC’s initial public offering (IPO), the search for target assets, and the merger and acquisition transaction (i.e., De-SPAC).The distinctive features of SPACs lie in their ability to raise capital efficiently and their strong private equity investment characteristics., SPACs have regained new vitality within the current thriving private equity investment ecosystem and the relatively mature capital markets of Europe and the United States.

Like conventional corporate entities, SPACs can also raise capital from public investors through an initial public offering (IPO). The majority of these funds are deposited into a trust account and invested in conservative instruments to generate returns, pending the completion of a De-SPAC transaction and closing. A SPAC IPO is quite similar to a traditional IPO, with differences primarily in valuation determination, closing timeline, cost structure, and trading units.

For instance, the IPO unit price of a SPAC is typically set at $10, with differences among various SPAC units lying primarily in the types of equity they include. Generally speaking, for SPACs established by experienced and well-capitalized sponsors, each trading unit consists solely of one share of common stock, whereas more SPAC trading units comprise one share of common stock plus 1/4 to 1/2 of a warrant.

The purpose of SPAC investment is similar to that of private equity investment, namely to raise a certain amount of capital to invest in companies with high growth potential. The difference lies in whether the funds are raised from public investors or from specific institutional investors. It is important to note that a SPAC listing is fundamentally different from a back-door listing. The former is an incremental entity proactively established to facilitate the public listing of potential target companies, whereas the latter is a last-resort option for existing listed companies that are no longer sustainable.

In fact, SPACs remained lukewarm for a long time, with a turning point only emerging in recent years.

As capital market interest rates continued to decline, increasingly large pools of cash struggled to find sufficient high-quality assets, prompting the exploration of new instruments and driving SPAC IPO volumes and fundraising amounts to record highs. Among these, specialized SPACs focused on the healthcare sector emerged slightly later but have since experienced rapid growth.

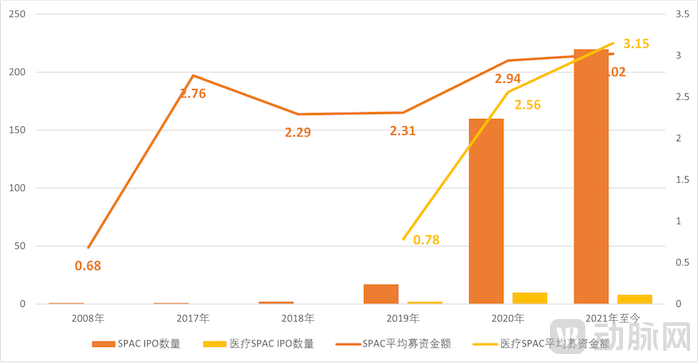

VCBeat’s statistics reveal that in 2020, a total of 160 SPAC companies went public on U.S. stock exchanges, raising over $47 billion in total—surpassing the combined IPO proceeds from all previous years for SPACs. In 2021, despite the U.S. Securities and Exchange Commission (SEC) further tightening its regulation of SPACs, 220 SPAC companies had already gone public by the end of May, raising $66.5 billion in total. This figure exceeded the full-year total of the previous year, with the average amount raised per SPAC continuing to climb. The SPAC frenzy has also become a major channel for corporate IPOs. According to publicly available data, SPAC financings accounted for nearly 50% of all equity financing in the U.S. stock market throughout 2020.

Since 2019, a specialized category of SPACs focused on healthcare investments has emerged in the market, demonstrating strong growth momentum. From 2019 to the end of May 2021, there were 2, 10, and 8 healthcare-focused SPAC listings globally, respectively. The average amount raised per offering grew from USD 78 million to USD 315 million, representing a compound annual growth rate (CAGR) of 59.25%, compared to a CAGR of 9.34% for the overall SPAC market during the same period. Summit Healthcare, backed by QiaoKang Capital, is one such example following its listing.

It is hardly surprising that the sponsors behind these healthcare SPACs typically possess extensive experience in medical innovation practices or investment. For instance, Compute Health, founded by Intel Chairman Omar Ishrak; Health Assurance, launched by the founding team of Livongo, the U.S. intelligent diabetes management platform acquired by Teladoc for $18.5 billion; and Revolution Healthcare raised $750 million, $500 million, and $500 million, respectively, during their IPOs. They remain the top three healthcare SPACs to date in terms of IPO fundraising amounts.

In China, in addition to Summit Healthcare, Hony Capital, which is being established by Hony Capital, also regards healthcare as an important direction for M&A targets. It is understood that Hony Capital plans to raise $300 million through an IPO.

Furthermore, according to the prospectus, during the issuance periods of Health Assurance and Revolution Healthcare, top-tier private equity firms such as General Catalyst and ARCH were attracted to participate in the public offering phase. Introducing reputable institutional investors at the early stages to bolster confidence among investors and potential targets has become a significant trend in the current SPAC market. During this period, prominent investment firm Hillhouse Capital was also drawn in.

Public information indicates that among the SPAC companies held by Hillhouse Capital, Montes Archimedes focuses on identifying merger and acquisition targets in the biopharmaceutical sector. The latter is a SPAC sponsored by Patient Square Capital, an investment firm founded by Jim Momtazee, the former head of KKR’s Health Care division. Jim Momtazee specializes in investing in M&A targets within the biopharmaceutical industry, having previously invested in the innovative pharmaceutical company Jazz, the hospital chain HCA, the innovative drug investment platform BridgeBio, and the CRO firm PRA Health, which was recently acquired by another publicly listed company, ICLR, for $12 billion.

Based on the data generated so far, SPACs have delivered substantial returns to top-tier investment firms and sponsors. Statistics show that in 2020, the overall returns from SPACs tripled compared to 2019, which had just set a new record.

From an investment perspective, SPACs are highly favorable to sponsors.

One PartyIn terms of SPACs, sponsors are granted considerable flexibility, including in the holding period and target selection.

For early-stage project investments, the holding period is often critical to success or failure. Leung Kam-sung, the sponsor of New Frontier Health Corporation—the first non-U.S. SPAC—once stated in a media interview that experienced and renowned investors, when lacking sufficient capital, often choose to establish equity funds. However, an inherent drawback of such funds is that they typically require exit within three to five years. “Many promising businesses may not reach maturity within three to five years, so exiting too early is not necessarily advisable.” In Leung’s view, Berkshire Hathaway’s market capitalization exceeds that of Blackstone Group largely because Warren Buffett selectively holds investments for the long term, whereas Stephen Schwarzman insists on exiting upon fund maturity.

In July 2019, New Frontier Health Corporation merged with the then-unprofitable United Family Healthcare. At the time, New Frontier Health projected that United Family Healthcare’s total revenue would achieve a compound annual growth rate (CAGR) of approximately 18% over the next five years, with adjusted EBITDA growing at a CAGR of around 50%. This decision received support from the majority of New Frontier Health’s public investors.

Meanwhile, during the SPAC formation period, the target sectors or regions for future acquisitions are typically listed only in broad terms, while the sponsors and management team possess sufficiently extensive networks. Furthermore, the equity structure of a SPAC is relatively clear; if investors disagree with the sponsors’ decisions, they can choose to redeem their shares, which in most cases does not affect the final merger outcome.

Palihapitiya once stated that venture capital work is exhausting, as it requires constant interaction with a fund’s general partners (GPs). In contrast, the SPAC structure is easier to manage and less taxing, allowing more energy to be devoted to identifying acquisition targets. After serving as Facebook’s early Vice President of Growth and founding Social Capital, Palihapitiya launched the SPAC known as IPOA in September 2017 and completed its acquisition of Virgin Galactic two years later. Following Virgin Galactic’s public listing, its stock price quickly doubled, drawing significant attention from secondary market investors to the SPAC model. Subsequently, Palihapitiya sponsored multiple SPACs, raising over $3 billion.

The Other PartyOn the other hand, SPACs allow sponsors to achieve extremely high returns with relatively low risk.

The initial costs to establish a SPAC typically range from $3 million to $4 million. Following its public listing, the SPAC’s market capitalization can reach between $50 million and several hundred million dollars. Under the unique rules governing SPACs, sponsors have the right to acquire 20% of the listed SPAC’s shares at a nominal price, offering substantial upside potential. Meanwhile, the risks borne by sponsors are limited, with maximum losses capped at the upfront expenditures, including fees paid to underwriters and intermediaries, as well as personnel costs for the management team.

For the target company, i.e., the enterprise preparing for an initial public offering (IPO), the advantages of a SPAC are evident.

First, SPACs impose virtually no restrictions on company qualifications.In theory, virtually any company in any sector can go public through a SPAC. Industry insiders told VCBeat that target companies generally need to meet only two conditions: first, at the time of the merger with the SPAC, the target company’s valuation must exceed 80% of the amount raised by the SPAC; second, the target company must provide audited financial statements for at least the past two to three years, prepared in accordance with U.S. GAAP or IFRS standards. “The first condition does not pose a substantial barrier, given the considerable flexibility in valuing target companies. The second condition reflects the SEC’s general baseline requirements for companies seeking to list in the United States,” said the industry practitioner.

Secondly, SPACs can offer companies a faster path to going public.Moreover, the outcome is more certain. Typically, a company can go public within 3–6 months from the signing of a merger letter of intent with the SPAC, whereas a traditional IPO takes 8–12 months. This process involves virtually no underwriters and does not require raising capital from the market. There is hardly any external resistance, and success is essentially guaranteed as long as the prescribed procedures are followed step by step. Furthermore, the valuation of the target company can be relatively flexible, as it fundamentally requires only the SPAC’s approval and mutual agreement between the two parties, unlike an IPO, which depends heavily on market conditions and even relies on investment banks and investors.

Third, SPACs can alleviate share dilution pressure to some extent.In a traditional IPO, the pre-IPO crossover financing round typically dilutes 20% of equity shares, and the IPO itself further dilutes another 20%. If the greenshoe option is also taken into account, the share dilution would be even greater. Crossover financing and the IPO usually occur sequentially within one year. Moreover, biopharmaceutical companies need to raise capital annually in the primary market; excessive equity dilution is unfavorable for the founding team.

A practitioner specializing in SPAC mergers and acquisitions told VCBeat that, based on the current response from Chinese companies, high-performing startups show strong interest in SPACs, while larger-scale companies still prefer traditional IPOs. “SPACs provide a window into overseas capital markets for companies and startups that urgently need funding but have little hope of listing domestically on the STAR Market or ChiNext in the short term, as well as for those still in rapid development, not yet profitable, or even without specific products. According to industry practices, the post-merger enterprise valuation is most appropriate at approximately 3–5 times the SPAC’s market capitalization. Given that the median market cap of mainstream SPACs in the market is around $400 million, the calculated options for large enterprises are relatively limited.”

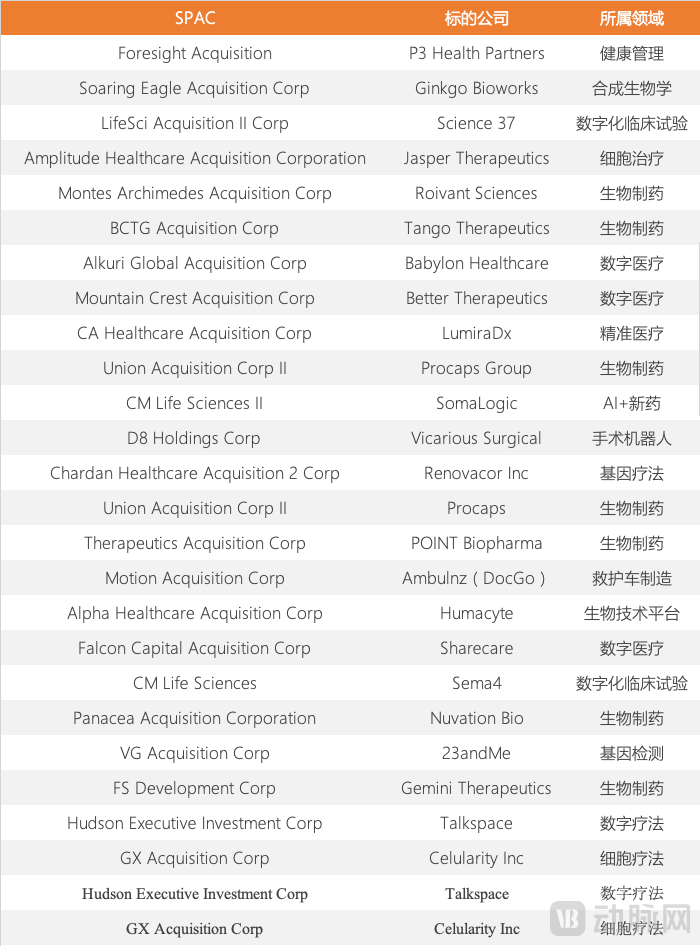

A brief review by VCBeat reveals that since 2021, a total of 24 SPACs have announced mergers with innovative healthcare projects, secured shareholder approval, or completed transactions. These include high-profile companies such as Ginkgo, Babylon, 23andMe, and Talkspace. Based on currently available public data, once these transactions are finalized, they will create a combined market capitalization exceeding $50 billion.

Overall, healthcare companies poised to go public via SPACs are predominantly those driving frontier technological innovations—such as cell therapy, gene therapy, and AI-enabled new drug development—as well as those pioneering digital business model innovations, including digital therapeutics and decentralized clinical trials.

Among these M&A deals, synthetic biology company Ginkgo Bioworks is poised to achieve the highest valuation. As a global leader in synthetic biology, Ginkgo Bioworks integrates AI with life science tools to build scalable engineering and data platforms. It has amassed a vast, flexible, and diverse library of genetic parts, enabling the engineering of microbes with tailored biological traits to meet specific demands.

Under the merger agreement between Ginkgo Bioworks and the SPAC company Soaring Eagle, the two parties have valued Ginkgo Bioworks at $15 billion. Through the merger, Ginkgo Bioworks is expected to receive $2.5 billion, including $1.725 billion raised by Soaring Eagle in its IPO and $775 million in PIPE investment pre-committed by private equity investors. According to disclosures, the transaction is scheduled to be completed in the third quarter of this year.

Another example of a frontier technology innovator going public via SPAC is 23andMe. As a globally renowned consumer genetics company, 23andMe pioneered the direct-to-consumer provision of unique, personalized genetic information related to health risks, ancestry, and traits. It is also the only consumer genetic testing company to have received U.S. Food and Drug Administration (FDA) authorization for its over-the-counter health and carrier status reports.

Furthermore, 23andMe has gradually established a recontactable database for genetic research, comprising genotypic and phenotypic data. Leveraging these data, 23andMe has developed an extensive product portfolio encompassing more than 30 therapeutic programs across oncology, respiratory diseases, cardiovascular diseases, and other areas.

Under the merger agreement reached between 23andMe and VG Acquisition, the two parties will complete the merger in the second quarter of 2021, after which 23andMe will be listed and traded under the stock ticker “ME.” In this transaction, 23andMe is valued at $3.5 billion and will receive $509 million in cash from VG Acquisition as well as $250 million in PIPE investments committed by institutional investors.

Talkspace, a leading provider of digital and virtual behavioral healthcare, and Babylon Healthcare, a well-known digital therapeutics startup, have successively announced that they have reached merger agreements with SPAC companies.

The SPAC partner for Talkspace is Hudson Executive Investment Corp. Upon completion of the merger, Hudson Executive will operate under the name Talkspace and list on the Nasdaq Stock Market under the ticker symbol “TALK.” Reportedly, the transaction implies an initial enterprise value of $1.4 billion for Talkspace, approximately 11 times its estimated net revenue for 2021. In addition, Hudson Executive will provide Talkspace with $250 million in cash to serve as growth capital. The two parties are expected to close the transaction in late Q1 or early Q2 of 2021.

Babylon Healthcare connects patients with doctors through its app, offering features such as video consultations, remote symptom assessments, and scheduling appointments with specialists like therapists, covering a wide range of conditions including hair loss and chronic kidney disease. Reportedly, Babylon Healthcare is set to be acquired by Alkuri Global, a special purpose acquisition company (SPAC) launched by former Groupon CEO Rich Williams and former COO Steve Krenzer, at a valuation of $3.5 billion.

Even as the U.S. securities market, the most vibrant SPAC ecosystem, has faced heightened regulatory scrutiny, enthusiasm for SPACs has not truly waned. Meanwhile, capital markets in Singapore, Hong Kong, China, and other regions have successively announced explorations into introducing SPAC mechanisms.

Does this mean that domestic startups will spring up like mushrooms to ride the wave of SPAC listings? Perhaps not entirely.

On the one hand, not all startups are ready. Although SPACs offer a faster and more stable path to going public, the formal requirements of traditional IPOs also apply to the SPAC model. This means that startups must have a sound corporate governance structure, an effective financial management system, a professional and efficient IPO coordination team, and be able to provide audited financial statements for multiple periods. However, the completeness of the operational and management environment is precisely what many growing startups lack.

On the other hand, not all startups can find a suitable SPAC match. It is worth noting that the most prominent SPACs are currently still sponsored by overseas investors. Drawing on past experience, overseas investors’ understanding of Chinese companies and the domestic market environment remains inferior to that of domestic investors, which may lead to differentiated investment judgments. In other words, at this stage, mainstream SPAC investors are more likely to favor potential targets in their local markets rather than projects in China and other emerging Asian markets.

Furthermore, for most startups, the processes and qualification requirements involved in SPACs are complex and intertwined; when their external support systems and internal responsiveness are not yet mature, they may choose to adopt a wait-and-see approach.

In fact, as a tool that has suddenly gained popularity in the capital markets, SPACs also require a process of trial and error and validation. Currently, both the initiation and merger-and-acquisition activities of domestic SPACs are in their infancy; therefore, it is essential to maintain rationality and reverence alongside the excitement.