Breaking Foreign Monopoly: How Mindray, Yuwell and Other Chinese Firms Are Driving Domestic Substitution in China's Defibrillator Market

According to the "Report on Cardiovascular Health and Diseases in China 2019" released by the National Center for Cardiovascular Diseases of China, there are approximately 544,000 cases of sudden cardiac death (SCD) annually in China. In contrast, the total number of sudden cardiac deaths in the United States is approximately 300,000 per year, which is roughly half that of China.

In the past, the survival rate for out-of-hospital sudden cardiac arrest in the United States was only 5%–8%. Today, in major U.S. cities with widespread availability of automated external defibrillators (AEDs) and comprehensive public training programs, the survival rate has risen to 50%–70%. In contrast, China’s AED penetration rate is less than 1%, and the resuscitation success rate for sudden cardiac death is merely 1%. Furthermore, while the annual number of implantable cardioverter-defibrillator (ICD) implants in the United States reaches as high as 200,000 units, China’s annual ICD implant volume is only 1,000 units—just 1/400th of the U.S. figure. (Source: Chinese Circulation Journal – “Current Status and Prevention of Sudden Cardiac Death in China”)

The significant disparity in the number of defibrillators and the success rate of resuscitation from sudden cardiac death between China and the United States indicates that, to a certain extent, defibrillators determine the survival rate of patients experiencing cardiac arrest. More than 80% of cardiac arrests are caused by ventricular fibrillation, making early defibrillation a critical link in the chain of survival for cardiac arrest patients. During cardiac arrest, the heart is unable to effectively pump blood, leading to severe ischemia and hypoxia in vital organs throughout the body. Defibrillators deliver pulsed electrical currents to the patient’s heart to administer electroshock therapy, thereby terminating life-threatening arrhythmias.

Based on the placement of the electrode pads, defibrillators can be classified into implantable cardioverter-defibrillators (ICDs) and external defibrillators. ICDs involve placing electrodes inside the chest to directly contact the myocardium for defibrillation. External defibrillators deliver defibrillation indirectly by placing electrodes on the chest wall and can be categorized into manual external defibrillators and automated external defibrillators (AEDs). Building upon AED technology, wearable cardioverter-defibrillators (WCDs) have also been developed.

ICD Implantable Cardioverter Defibrillator

An electronic device implanted into the patient’s thoracic cavity, connected to the heart via transvenous defibrillation leads, capable of automatically detecting and promptly terminating malignant ventricular arrhythmias. The ICD combines defibrillation and pacing functions: when the patient experiences tachycardia, the ICD can restore normal sinus rhythm through high-energy electrical shocks; when the patient experiences bradycardia, the ICD can normalize the heart rhythm through low-energy electrical pulses. Appropriate use of ICDs can correct rapid ventricular arrhythmias, reduce the incidence of sudden cardiac death, and prolong patient survival. Multiple clinical studies have confirmed that ICDs are the optimal therapeutic approach for preventing sudden cardiac death.

AED Automated External Defibrillator

A portable, automated defibrillator that can automatically diagnose specific arrhythmias and deliver electrical shocks for defibrillation, enabling laypersons to initiate resuscitation quickly and significantly improving survival rates for patients with sudden cardiac death. Unlike traditional professional defibrillators, AED devices feature a “user-friendly” design that allows non-professionals to operate them after minimal training. In a sense, it is not merely an emergency medical device but also represents a new paradigm in first aid—one that emphasizes the critical importance of immediate, effective intervention by on-site bystanders.

WCD Wearable Defibrillator

A wearable device that provides short-term defibrillation therapy without surgical implantation, enabling portability and rapid treatment based on automated external defibrillator (AED) technology. It is clinically indicated for patients at risk of sudden cardiac death who either do not meet the criteria for implantable cardioverter-defibrillator (ICD) implantation in the short term or have indications but cannot undergo ICD implantation immediately. The wearable cardioverter-defibrillator (WCD) is portable, allowing patients greater freedom of movement and removing treatment constraints to fixed locations. Furthermore, as the device does not require implantation, it avoids potential procedure-related complications and reduces postoperative care costs for patients.

To further improve the resuscitation rate for cardiac arrest patients in China, the development and widespread adoption of defibrillators are essential. However, as Class III active medical devices, defibrillators present certain technical barriers. Previously, the Chinese defibrillator market was nearly monopolized by large foreign enterprises, with domestic brands largely absent. In recent years, Chinese companies have made significant efforts, developing the first AED, ICD, and WCD products with fully independent intellectual property rights. The emergence of domestic brands can break the market monopoly, reduce the price of defibrillators on the market, and benefit more domestic patients with atrial fibrillation.

This article reviews 19 domestic and international companies involved in ICDs, AEDs, and WCDs, aiming to explore the development trends in these three niche segments of the defibrillator market. How will the global defibrillator market evolve? Can Chinese companies achieve import substitution with domestically produced alternatives?

It typically takes over a decade for defibrillators to progress from research and development (R&D) through clinical trials to market launch. Both early-stage R&D and later-stage commercialization require companies to possess substantial financial strength. Multinational corporations expand their markets through mergers and acquisitions, characterized by long product development cycles and slow updates; in contrast, small enterprises focus on technological and product innovation but face constraints in funding and time. This dynamic has led to a defibrillator market marked by consolidation and expansion among large firms, while small and medium-sized enterprises remain fragmented.

Major Acquisition in the Defibrillator Sector

In 2012, Asahi Kasei Corporation of Japan acquired Zoll for $2.21 billion.In 2016, Abbott acquired St. Jude Medical for $25 billion, integrating St. Jude’s defibrillator business in what stands as Abbott’s largest acquisition to date.Previously, St. Jude Medical also acquired Ventritex, a company that produced ICDs. Physio-Control, a global leader in defibrillator manufacturing, was sold by Bain Capital to Stryker for $1.28 billion in 2016, following its earlier acquisition by Medtronic. In 2017, MicroPort acquired Sorin, LivaNova’s cardiac rhythm management brand, for $190 million. In 2019, Zoll Medical Corporation acquired Cardiac Science, expanding its AED product line. Large corporations have continued to engage in mergers and acquisitions, gradually monopolizing the defibrillator market, leaving smaller companies to achieve breakthroughs only through technology and product innovation.

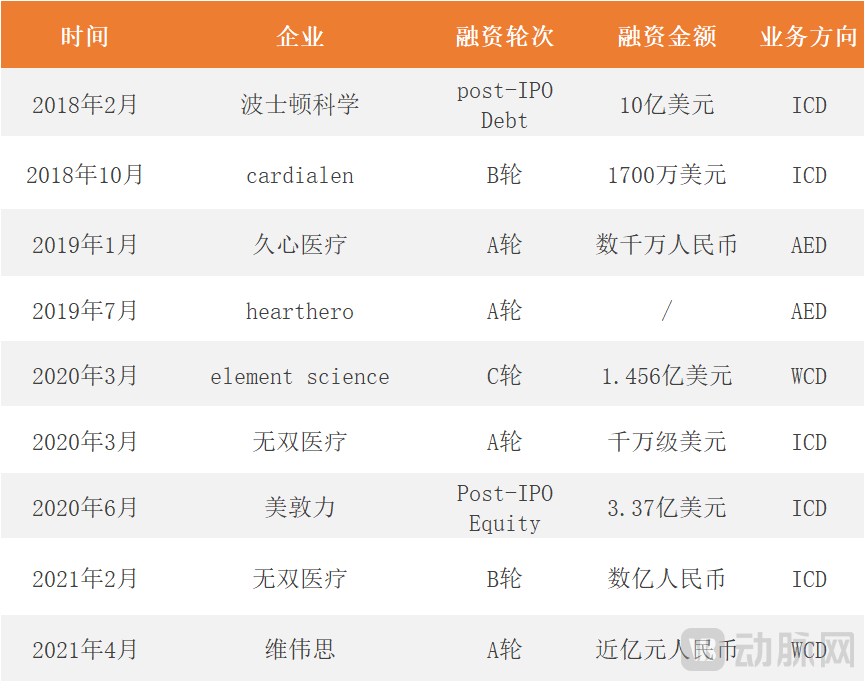

Financing Activities of Defibrillator-Related Companies, 2018–2021

As shown in the table, defibrillator-related companies have secured substantial financing amounts, which is primarily attributable to the inherent nature of these enterprises. Given the high technical complexity and significant entry barriers associated with defibrillator technology, this sector is typically dominated by companies of a certain scale. Furthermore, as there are many publicly listed companies in the defibrillation field, financing progress has been relatively slow, with few large-scale financing events occurring over the past four years.

Wushuang Medical, which entered the defibrillator market with implantable cardioverter-defibrillators (ICDs)—the most technically complex products in the field of cardiac rhythm management—completed two large-scale financing rounds in 2020 and 2021, with its Series B round raising hundreds of millions of RMB. Major investment firms such as Northern Light Venture Capital and Qiming Venture Partners recognized Wushuang Medical’s growth potential and participated in both financing rounds. Weiweisi, which developed the first domestically produced wearable cardioverter-defibrillator (WCD), completed a financing round of nearly RMB 100 million in 2021, led by Northern Light Venture Capital.

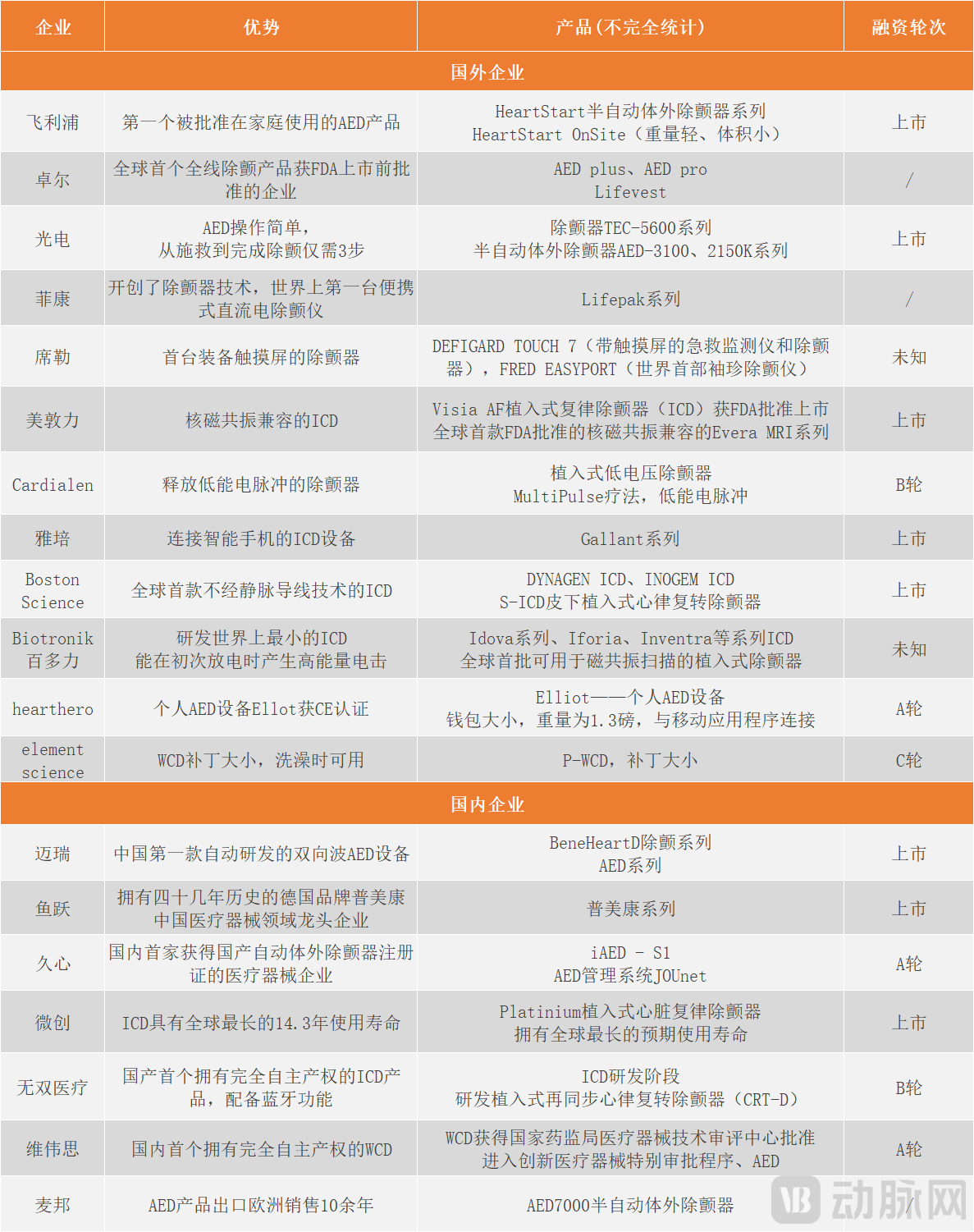

For years, China’s defibrillator market has been monopolized by imported products. In the AED segment in particular, Philips, ZOLL, and Nihon Kohden have captured significant market share, leaving limited room for domestic brands to grow. However, in recent years, China’s defibrillator market has developed rapidly, with domestic companies such as Mindray, Yuwell, and Jiuxin making concerted efforts to break the import monopoly and achieve import substitution with domestically produced alternatives.

The AED market was the first to develop in China. In this field,Mindray and Yuwell, two major medical device companies, have taken different strategic pathsMindray entered the market by independently developing China’s first biphasic waveform AED, striving for innovation in technology and products; while Yuwell made a strong market entry by acquiring the German brand Primedic, which has over forty years of history, aiming to achieve technology importation and domestic production. Differing from the strategic directions chosen by these two listed industry giants, Wushuang Medical opted to tackle the more challenging ICD product segment, whereas Weiweisi is dedicated to the R&D of WCD products.

Data from the National Medical Products Administration (NMPA) show that,Among registered domestically produced medical device products, Mindray has a total of 16 defibrillator models, Jiuxin Medical has 5, while Beijing Futian, Shanghai Kohden, and Beijing Maibang each have 1.Mindray’s 2020 annual report shows that its defibrillator sales volume increased by more than 30%. According to Yuwell’s 2020 annual report, the year-on-year growth rate of its AED products reached 20%. This indicates that the demand for defibrillators in the Chinese market is growing.

Mindray Defibrillator Source: Mindray 2020 Annual Report

To establish a foothold in the defibrillator industry, some companies rely on resources and market presence accumulated over the long term, while others achieve breakthroughs through technological innovation. Early defibrillators often utilized industrial alternating current (AC), which posed a risk of harm to the human body. Currently, most defibrillator manufacturers have developed groundbreaking biphasic waveform technology, which delivers high-current, low-energy shocks for defibrillation therapy. Meanwhile, companies are advancing toward automation, enabling defibrillators to automatically adjust the delivered energy based on the patient’s impedance. Particularly in the implantable cardioverter-defibrillator (ICD) sector, which presents the greatest technical challenges, and the flexible-application automated external defibrillator (AED) sector, innovations are emerging continuously as companies strive to build their own technological advantages.

ICD is a high-tech achievement that closely integrates modern clinical cardiac electrophysiology and pacing technologies with advanced microelectronics. It is widely recognized as one of the Class III active implantable medical devices with the highest technological barriers and R&D risks in the industry.

Its adoption rate in China remains low. According to data reported by the National Center for Quality Control in Interventional Treatment of Arrhythmias under the National Health Commission, 4,471 implantable cardioverter-defibrillator (ICD) procedures were performed in mainland China in 2018. This is primarily due to the high cost of ICD devices, the technical complexity of implantation surgeries, and challenges in clinical implementation. The domestic ICD market is predominantly dominated by European and American companies, including Boston Scientific, Medtronic, Biotronik, and St. Jude Medical (acquired by Abbott).

ICD products not only present significant challenges in early-stage research and development, but also carry certain risks in later-stage market promotion. In recent months, several major international companies have issued multiple recalls for their ICD products. In December 2020, Boston Scientific confirmed that it had received six reports globally of voltage overload during discharge therapy in its subcutaneous implantable cardioverter-defibrillators (S-ICDs), leading to a voluntary Class II recall of the S-ICD. In March 2021, Boston Scientific initiated another voluntary recall of the S-ICD, this time classified as Class I. In April 2021, Medtronic voluntarily recalled certain ICD products due to battery issues, also classified as a Class I recall. As Class III medical devices implanted within the human body, the safety of ICDs is of paramount importance.

In the highly challenging field of implantable cardioverter-defibrillators (ICDs), every growing enterprise, regardless of its size, should possess its own core technological advantages.

In 2015, MicroPort's PLATINIUM series of implantable cardioverter-defibrillators (ICDs) was launched.Platinium VR Implantable Cardioverter Defibrillator Features the World’s Longest Battery Life of 14.3 Years, which can reduce the risks associated with frequent ICD replacements. Biotronik has developedThe World’s First ICD Capable of Delivering Ultra-High-Energy Shocks During Initial Discharge, and was approved by the FDA in 2015.

Boston Scientific has developed the S-ICD, which isThe world’s first and only commercially available ICD product with transvenous lead-free implantation. Traditional ICD therapy requires the placement of defibrillator leads within the cardiac chambers, which may lead to complications such as lead dislodgement, infection, and perforation. The S-ICD allows the defibrillation lead to be entirely implanted in the subcutaneous tissue, avoiding contact with the circulatory system and effectively preventing complications associated with traditional transvenous ICD leads. In 2012, the FDA approved the clinical use of the S-ICD. In 2016, the S-ICD received NMPA approval for market launch in China.

Medtronic’s Evera MRI Series ICD is the world’s first FDA-approved 3T MRI-compatible defibrillator., patients implanted with this series of defibrillator products can undergo magnetic resonance imaging (MRI) scans under specific conditions, which facilitates their routine physical examinations.

CurrentlyICD Products Not Yet Launched in China, but Suzhou Wushuang Medical is actively engaged in R&D. Since its inception, Wushuang Medical has proactively pursued the development and commercialization of Class III active medical devices in the field of cardiac rhythm management, including implantable cardioverter-defibrillators (ICDs) and implantable cardiac pacemakers, boldly entering the defibrillator market with its ICD products. The ICD product under development by Wushuang Medical features fully independent intellectual property rights and is equipped with Bluetooth functionality in addition to basic functions, having completed multiple animal studies.

In 2020, implantable cardioverter-defibrillators (ICDs) were included in the “First Batch of National Key Governance Lists for High-Value Medical Consumables,” enabling centralized national efforts to address issues such as artificially high prices and overuse of ICDs. These measures may inject new vitality into China’s ICD market by reducing usage costs and standardizing clinical practices amid the monopoly held by foreign brands. Nevertheless, domestically produced ICDs need to continue strengthening their competitiveness and strive to capture market share with original products.

Cardiac arrest mostly occurs out of hospital, and the golden rescue time is only 4 minutes, during which professional emergency personnel generally cannot arrive in time. For patients with cardiac arrest, cardiopulmonary resuscitation (CPR) combined with an automated external defibrillator (AED) is the best rescue measure. However, the penetration rate of AEDs in China is not high, which often leads to inadequate emergency response.

There are significant disparities in survival rates for out-of-hospital cardiac arrest (OHCA) worldwide, with rates in Asia, North America, and Europe ranging from 1.1% to 26.1%, representing a 24-fold difference. Compared with developed countries such as the United States and Japan, the availability of automated external defibrillators (AEDs) in developing countries lags far behind. Moreover, many people lack the necessary emergency first-aid skills. During the 2021 National People’s Congress and Chinese People’s Political Consultative Conference, NPC deputy Zhu Lieyu recommended that AEDs be made as ubiquitous as fire extinguishers, thereby empowering the public to use AEDs with confidence, competence, and proficiency.

China has a low AED penetration rate and a small market size, yet demand is substantial. For a long time, the market has been dominated by foreign brands, with each AED priced at RMB 20,000–30,000. Significant cross-border price disparities have greatly raised the barrier to AED adoption.The challenges in promoting automated external defibrillators (AEDs) stem, from the product perspective, from issues such as safety, operational complexity, and usage costs; from the broader societal perspective, they arise from factors including national policy support, corporate development and responsibility, and public awareness of emergency first aid.

Currently, companies are primarily focusing on the public sector by developing portable, effective, and user-friendly “foolproof” automated external defibrillators (AEDs) for non-professionals. The most critical R&D direction is automation and intelligence, with ease of use being paramount. In fact, AEDs have already achieved a high level of automation; most devices are equipped with voice prompts and can automatically analyze the patient’s heart rhythm to determine whether defibrillation is necessary. This automatic assessment of the need for defibrillation is a crucial step, as delivering an electric shock to patients who do not require it may cause damage to normal myocardial tissue and delay life-saving treatment.

Zoll Medical has over four decades of history in the field of defibrillators, and itsFull Line of Defibrillation Products Receives FDA Premarket Approval. ZOLL’s defibrillator monitors and AEDs are equipped with Real CPR Help® and See-Thru CPR™ technologies, which provide real-time feedback on the depth and rate of chest compressions and filter out compression-induced artifacts from the ECG monitor, enabling rescuers to view the patient’s underlying cardiac rhythm during cardiopulmonary resuscitation (CPR).Philips' HeartStart series of AEDs was the first to be approved for home use., expanding the application areas of emergency medical products. Hearthero has developed a personal AED device—Elliot—which is wallet-sized and weighs only 1.3 pounds.

After nearly a decade of research, development, and testing, Mindray broke through more than 1,000 foreign patent barriers and successfully developed China’s first AED product with fully independent intellectual property rights in 2013, thereby reducing the price of AED products.The Mindray BeneHeart D3 features automatic impedance compensation, allows emergency data export via USB flash drive, powers on in just 2 seconds, and charges to 200 J in only 3 seconds.According to incomplete statistics, Mindray’s AEDs have saved 66 patients in various settings.

March 2017,Yuwell Medical Completes 100% Equity Acquisition of German Company Metrax GmbH, Bringing the 40-Year-Old German AED Brand PRIMEDIC into Its PortfolioIn 2005, Primedic pioneered the global development of a series of defibrillators featuring biphasic waveform technology. Building on this established foundation, Yuwell introduced the technology while continuing its own research and development of new innovations. In 2019, Yuwell launched the M600, a new generation of automated external defibrillators (AEDs) with biphasic waveform technology.

Jiuxin Medical isThe first medical device company in China to obtain the registration certificate for a domestically produced automated external defibrillator,The “iAED-S1” is its first AED product to be launched. Jiuxin employs proprietary low-energy biphasic waveform technology and dynamic impedance compensation technology to improve defibrillation success rates.

Driven by internet-based healthcare, enterprises will also remotely manage devices via the Internet of Things to transmit patients’ vital sign data in a timely manner.Jiuxin Medical has launched the AED management system, JOUnet, which features an AED map that provides users with the location and availability of nearby AED devices. The system is accessible via mobile phones or computers, making it no longer difficult for emergency responders to locate AEDs. Meanwhile, ZOLL Data, under ZOLL Medical, offers data management services for emergency care operations. Data from AED devices are stored and uploaded in real time, enabling healthcare professionals to promptly assess rescue situations and organize patient data.

AED devices are becoming increasingly intelligent and user-friendly, enabling non-medical personnel to provide timely emergency assistance. In response to public hesitation and lack of confidence in using AEDs, both the Chinese government and enterprises have taken action.

Article 184 of the Civil Code of the People’s Republic of China stipulates that a rescuer shall not bear civil liability for any harm caused to the recipient as a result of voluntarily providing emergency assistance. Hangzhou is the first city in China to regulate the configuration and use of automated external defibrillators (AEDs) in public places through local legislation, implementing the Administrative Measures for Automated External Defibrillators in Public Places in Hangzhou since 2021. These Measures require that AEDs be configured in accordance with regulations at locations such as airports, railway stations, and large shopping malls, and further provide that “a rescuer shall not bear civil liability in accordance with the law for any harm caused to the recipient as a result of voluntarily providing emergency assistance using an automated external defibrillator.”

Meanwhile, major defibrillator manufacturers such as Mindray and Yuwell have actively assumed social responsibility by donating automated external defibrillators (AEDs) and conducting emergency first aid training programs. According to incomplete statistics, as of 2020, Mindray had donated a cumulative total of over 2,000 AED units and training devices to organizations including the Red Cross, schools, scenic areas, airports, and railway stations, and has continued to promote public awareness and training in emergency first aid through various collaborations and initiatives. Yuwell-Primedic AEDs have safeguarded the lives of hundreds of thousands of participants in marathon events at all levels across China, and have been instrumental in resuscitating multiple runners who suffered cardiac arrest on the race course.

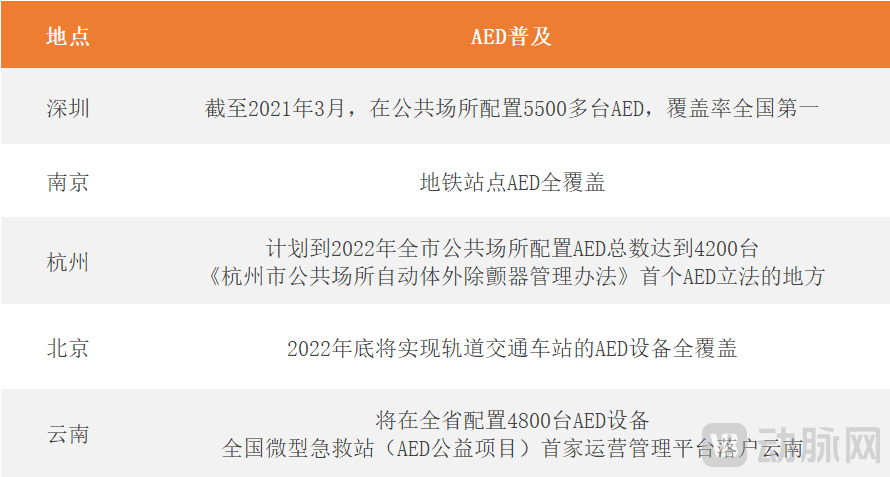

Distribution of AEDs in Selected Chinese Cities

With technological breakthroughs, product commercialization, and policy implementation, automated external defibrillator (AED) devices are being widely deployed across China, presenting a significant opportunity for domestic enterprises. As the AED industry continues to expand, companies must not only focus on product research and development but also prioritize the promotion of first-aid knowledge and the delivery of emergency response training to address public hesitancy and lack of proficiency in using these devices. In this regard, Chinese companies possess inherent geographic advantages that enable them to provide comprehensive after-sales support services alongside AED sales.

Although implantable cardioverter-defibrillators (ICDs) have been confirmed by multiple clinical trials as the preferred treatment for preventing sudden cardiac death, many patients at high risk of sudden cardiac death still have contraindications to ICD implantation or fall outside the indications for ICD use. The first scientific statement on wearable cardioverter-defibrillators (WCDs), released by the American Heart Association in 2016, indicated that WCDs can be used as a temporary measure to prevent sudden cardiac death in patients at transient risk of life-threatening arrhythmias who require permanent defibrillator therapy.

WCD devices are still a relatively new category, but numerous previous trials have confirmed their efficacy and safety.The first multicenter randomized controlled trial of WCD, the VEST study, showed that WCD did not reduce the incidence of sudden cardiac death within 90 days in patients with myocardial infarction and reduced ejection fraction (ejection fraction ≤35%), but it was able to lower the overall mortality rate in this patient population., ZOLL Medical’s LifeVest wearable defibrillator can reduce all-cause mortality by 36% within 90 days.

From June 2018 to October 2019, Fuwai Hospital led a multicenter clinical observational study of wearable cardioverter-defibrillators (WCDs) in China. The study utilized the latest-generation LifeVest 4000 device provided by ZOLL. Results showed that clear surface electrocardiographic signals were successfully recorded for all patients during the wearing period, with no cases of inappropriate shocks due to sensed interference or other causes. Although ventricular fibrillation was recorded in only one patient, all 13 episodes were correctly identified and successfully terminated.

Both trials utilized ZOLL’s LifeVest WCD, the first WCD to be launched globally. In 2006, ZOLL completed its acquisition of Lifecor’s assets, successfully incorporating the LifeVest wearable cardioverter defibrillator into its product portfolio. Patients can wear the LifeVest for continuous vital signs monitoring during most of the day, except for brief periods while bathing. Typically,From the device detecting a life-threatening rapid heartbeat to automatically delivering an electric shock, the entire event occurs within approximately one minute.Previously, Zoll Medical’s LIFEPAK defibrillator had been approved by the FDA for use in certain children at risk of cardiac arrest.

Patients wearing WCD devices need to adapt to more complex and diverse out-of-hospital environments, addressing issues of safety, portability, and compliance. WCD trials conducted in China have shown thatImpact on Sleepis the primary reason for poor wearable compliance among Chinese patients. Although the LifeVest weighs no more than two pounds, its vest-like design still causes inconvenience in patients’ daily lives, particularly during sleep.

San Francisco-based Element Science is developing a patch-like wearable cardioverter defibrillator (P-WCD), which primarily consists of ECG-sensing patch electrodes, defibrillation electrodes, and a main defibrillator unit. The P-WCD product is easy to use and canProvides continuous protection during daily activities such as bathing and sleeping., which may help address the issue of poor patient compliance.

Left: LifeVest; Right: P-WCD (Source: ZOLL official website, Element Science official website)

Left: LifeVest; Right: P-WCD (Source: ZOLL official website, Element Science official website)

Currently, ZOLL Medical Corporation is the only company with a wearable cardioverter defibrillator (WCD) product on the global market, and there are no domestically produced brands available in China. Therefore, this market still has significant room for growth.Suzhou ViVista has developed a wearable cardioverter defibrillator (WCD) with fully independent intellectual property rights, leveraging defibrillation technology, spray-adhesive technology, and flexible sensor technology—a first of its kind in China.. This WCD product was approved by the Center for Medical Device Technical Evaluation of the National Medical Products Administration on January 7, 2021, to enter the Special Review Procedure for Innovative Medical Devices.

Medical wearable devices are experiencing robust growth. According to the "2021 Internet Cardiovascular Disease Management Data Insights" report jointly released by VCBeat and JD Health, global sales of wearable medical devices exceeded $3 billion in 2018 and were projected to surpass $6 billion by 2023. However, current commercially available wearable devices are primarily focused on health monitoring, with relatively few therapeutic wearable products on the market.

WCDs face high technical barriers and complex application environments, making domestic regulatory approval inevitably challenging. Only by ensuring safety while achieving portability and addressing poor patient adherence can WCDs achieve broader adoption in China.