2021 White Paper on Medical Technology and Device Industry: A Comprehensive Analysis of a Market Exceeding RMB 850 Billion

Excerpt from the 2021 iCapital China Health Industry White Paper:Medical Technology and Devices, authorized for publication by VCBeat.

Preview of the Main Content:

1. What significant changes occurred in 2020?

2. Key Investment Themes and Market Outlook for 2021

3. Forecast of Investment Hotspots in 2021

4. 25 Companies Worth Watching

Core Viewpoints:

1.Nearly all global medical device giants have grown and strengthened through mergers and acquisitions.Large.Mergers and acquisitions among Chinese medical device companies are also accelerating onto the fast track. The polarization in performance among healthcare enterprises caused by the COVID-19 pandemic in 2020 has accelerated this process. It is expected that a significant number of pandemic-benefited companies will acquire pandemic-impacted ones over the next three to five years, a trend that will be particularly pronounced in the in vitro diagnostics (IVD) sector, where numerous technology-driven startups will become acquisition targets for established firms.

2. The government’s vigorous promotion of volume-based procurement policies has not only compressed costs in the intermediate links of medical products but also served as a significant driver inducing independent innovation among Chinese medical device enterprises.The era when a single product could sustain a company’s growth for a decade is gone forever. Medical device companies with R&D capabilities limited to a single-product pipeline will find it increasingly difficult to achieve independent growth and expansion in the future.

3. Product pipelines with substantial market demand and a significant impact on medical insurance expenditures will inevitably be included in volume-based procurement once import substitution reaches a certain level. Therefore, manufacturers of these products must expand their portfolios with new, high-margin, highly innovative product lines to prevent a rapid decline in corporate profits.

4. Key Sectors for Capital Investment in 2021:

▪ Medical Robots

▪ Interventional Minimally Invasive Devices and Consumables

▪ Electrophysiology-related surgical equipment and consumables

▪ High-value consumables for stomatology and ophthalmology

▪ Mass Spectrometry

▪ Molecular Diagnostics

▪ Raw Materials for IVD Reagents

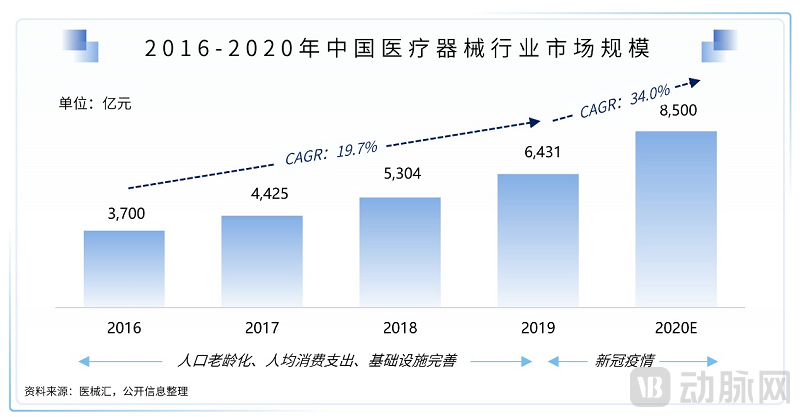

China's Medical Device Industry Ushers in a Second Wave of Growth

The Chinese medical device market currently accounts for nearly 20% of the global medical device market, with its share continuing to rise.

In 2019, the market size of China’s medical device industry reached RMB 634.1 billion, representing a year-on-year growth of approximately 19.6% compared to 2018. Driven by a surge in demand for a range of medical devices—including surgical masks, nucleic acid testing kits, and extracorporeal membrane oxygenation (ECMO) machines—revenue in China’s medical device industry was projected to exceed RMB 850 billion in 2020. In the post-pandemic era, with the Chinese government introducing various policies to accelerate the improvement of healthcare infrastructure, the medical device industry is expected to maintain robust growth in the coming years.

Key Drivers of Future Growth in China's Medical Device Market

Key Drivers of Future Growth Include:

The aging population has led to a growing number of individuals with chronic diseases;

Income growth drives the increase in per capita healthcare consumption expenditure;

Improvement of Medical Clinic and Hospital Infrastructure.

In 2020, driven by the surge in demand for in vitro diagnostics (IVD) and medical consumables due to the COVID-19 pandemic, the combined annual operating revenue of 53 A-share listed medical device companies included in the statistics reached RMB 57.2 billion, representing a 37.4% year-on-year increase from 2019. The total net profit attributable to shareholders of these A-share listed medical device companies reported in their interim reports for 2020 exceeded RMB 14 billion, nearly doubling the RMB 7.105 billion recorded in 2019. Among them, companies such as Zhijiang Biotech, Daan Gene, Mingde Biology, BGI Genomics, Intco Medical, and Kangtai Medical were among the beneficiaries of the pandemic, with performance growth exceeding 200%.

The pandemic will drive long-term expansion of the medical infrastructure market and its penetration into primary care settings, while accelerating the substitution of imported medical devices with domestically produced alternatives.

The Pandemic Prompted Many Countries to Reduce or Waive Import Tariffs on Medical Devices, Accelerating the Global Expansion of China’s Medical Device Industry

In the first half of 2020, although the COVID-19 pandemic had been effectively contained in China, it continued to rage in other countries around the world. Under the impact of the pandemic, many countries introduced measures to reduce or exempt import tariffs on medical devices, aiming to leverage external resources to address shortages in their domestic medical product supplies. This created a historic opportunity for Chinese medical enterprises to rapidly expand into overseas markets. Relevant data show that China’s exports of medical consumables in the first half of 2020 increased by 43% compared with the same period in 2019.

Currently, the epidemic is accelerating in emerging markets such as India and Brazil. Due to factors including insufficient vaccination rates and scarce medical resources, demand for anti-epidemic products such as COVID-19 testing reagents is likely to remain strong. This trend benefits Chinese IVD companies by boosting exports of their diagnostic products. Meanwhile, demand for epidemic-related equipment, including ventilators, patient monitors, portable ultrasound systems, mobile DR units, and CT scanners, has surged significantly. On April 30, 2021, the Ministry of Foreign Affairs stated that since April 2021, China had exported more than 26,000 ventilators and oxygen concentrators to India.

The pandemic has accelerated regulatory approvals in the industry, helping to reduce companies’ approval costs and shorten product approval cycles.

On February 25, 2020, to fully meet the needs of epidemic prevention and control, the National Medical Products Administration (NMPA) established a green channel for the emergency approval of medical devices, ensuring the supply of emergency prevention and control materials and medical devices required for epidemic response. Special measures were implemented for the registration, production licensing, and inspection and testing of medical device products such as medical masks and medical protective clothing, with merged approval processes. For enterprises converting their production lines to manufacture medical devices, emergency approval procedures were applied, and medical device registration certificates and production licenses were issued in accordance with the law.

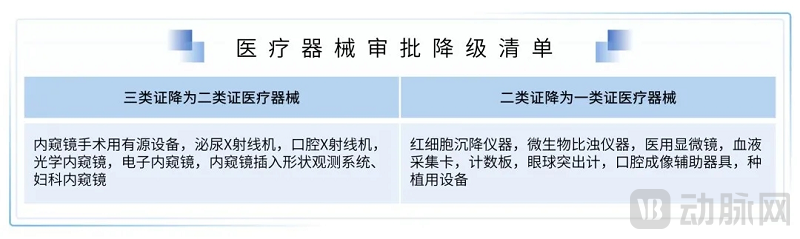

In December 2020, the National Medical Products Administration (NMPA) issued the “Announcement on Adjusting Certain Contents of the ‘Medical Device Classification Catalog’,” downgrading seven categories of medical devices from Class III to Class II, and eight categories from Class II to Class I. For manufacturers, this reclassification reduces product approval cycles and significantly accelerates market entry. For instance, the estimated timeline for Class II registration is at least 15–21 months, extending to at least 33 months for categories requiring clinical trials. If downgraded to Class I, the filing process takes only one to two weeks, substantially shortening the cycle. Meanwhile, initial registration and renewal fees are also significantly reduced. Taking imported medical devices as an example, registration fees are RMB 308,800 for Class III, RMB 210,900 for Class II, while Class I devices are exempt from fees.

The Pandemic Drives Upgrades in the Medical Device Supply Chain, Promotes Continuous Industry Consolidation, and Accelerates Response to Healthcare Demands

The outbreak has disrupted production schedules, and coupled with transportation controls, it has dealt a significant blow to the global medical device supply chain. The ripple effects along the supply chain persist; in the short term, this will lead to tight supplies of imported medical devices in China, while in the long term, the pandemic will exert structural impacts on the medical device supply chain.

From a horizontal perspective, relevant enterprises will further optimize their logistics systems and establish more scientific and rational management mechanisms as well as response protocols for public health emergencies. By continuously advancing channel integration, they will effectively reduce costs across procurement, transportation, and distribution, while strengthening the stability of their channel networks to gain greater advantages in the allocation of medical supplies between supply and demand.

From a vertical perspective, upstream manufacturers may acquire midstream distributors to optimize distribution channels; large midstream channel companies may acquire small upstream producers to achieve in-house manufacturing; and midstream channel companies may acquire downstream healthcare service providers to enhance service delivery. Various forms of mergers and acquisitions can more rapidly align supply across the upstream and downstream segments. The pandemic will promote continued industry consolidation in the future, accelerating responsiveness to healthcare demands.

The Pandemic Accelerates the Adoption of New Medical Technologies, with AI Effectively Reducing the Workload of Healthcare Professionals

A variety of new medical technologies played a significant role during the pandemic, such as ward robots, virus isolation systems, airborne virus purification systems, information systems for operating rooms and wards, and rapid temperature screening systems. The introduction of AI technology effectively reduced the workload of overburdened physicians in clinical laboratories, pathology departments, and radiology departments during the pandemic, alleviating their work intensity while improving the efficiency and accuracy of diagnosis and treatment.

Many hospitals lack rapid diagnostic capabilities in their fever clinics; the epidemic will drive the development of the rapid diagnostics industry, including POCT.

Rapid diagnostic capability is a fundamental requirement during the pandemic. Point-of-care testing (POCT) products that are convenient, miniaturized, and suitable for rapid diagnosis will become a new growth hotspot in the in vitro diagnostics (IVD) sector. During the pandemic, more than 100 companies, including Wondfo, Autobio, Daan Gene, Snibe, Maccura, Medconn, Getein, Kanghua Biology, and Urit, successively launched test kits and various rapid detection methods. Among these, POCT products played a significant role in epidemic prevention and control due to their portability and speed.

On the other hand, the COVID-19 pandemic has exposed the lack of rapid diagnostic capabilities in fever clinics of many hospitals. In the future, the demand for convenient, miniaturized POCT products suitable for rapid diagnosis, such as compact biochemical analyzers, hematology analyzers, PCR equipment, and gene sequencers, will become increasingly prominent. Microfluidics may become the next breakthrough point.

High-value consumables may face significant short-term pressure due to the pandemic, but are expected to sustain a rebound in the post-pandemic era.

High-value surgical consumables represent the hospital-based medical device segment most severely impacted in the short term. During the pandemic, the volume of routine surgical procedures declined significantly, with exceptions made only for critical and emergency cases. Orthopedic devices, cardiovascular stents, pacemakers, and endoscopic instruments suffered substantial short-term disruptions, leading to significant inventory backlogs. Established companies were able to leverage their scale to mitigate short-term pressures, whereas small and medium-sized enterprises (SMEs) with limited cash flow faced a more严峻 situation.

In the long run, innovation remains the central theme for high-value medical consumables; the decline in surgical volume is only temporary and will not affect the sector’s future growth.

Changes in payment policies, registration and approval processes, and the corporate listing environment have brought both challenges and opportunities to medical device companies, making product innovation the key to future success.

Payment Policies for High-Value Consumables Are Becoming Clearer; Following Coronary Stents, Orthopedic Consumables and IVD Products May Soon Be Subject to National Centralized Procurement

In July 2019, the General Office of the State Council issued the Notice on the Plan for Reforming the Governance of High-Value Medical Consumables. The Notice stipulates that classified centralized procurement of high-value medical consumables should be explored in accordance with principles such as volume-based procurement, linking volume with price, and promoting market competition. All public medical institutions must conduct open transactions and transparent procurement of high-value medical consumables on procurement platforms. For high-value medical consumables with a high degree of localization, large annual procurement volumes, a wide range of selectable manufacturers, and relatively clear product evaluation standards, centralized procurement by category should be explored. Medical institutions are encouraged to jointly conduct volume-based negotiated procurement, and cross-provincial alliance procurement is to be actively explored. This document officially ushered in the era of volume-based procurement for high-value consumables, signaling that the medical device sector is poised for dramatic changes. Since then, high-value consumables in fields such as cardiovascular care and orthopedics, as well as in vitro diagnostics (IVD), have entered a phase characterized by “provincial and municipal pilot volume-based procurement plus national centralized procurement” (hereinafter referred to as “National Centralized Procurement”).

In the first round of China’s national volume-based procurement (VBP), coronary stents were selected, with the bid opening officially held in Tianjin on November 5, 2020. Unlike the mechanism adopted in volume-based procurement for orthopedic devices in multiple provinces—where imported and domestically produced products are grouped separately for competitive bidding—the rules for the national VBP of coronary stents did not separate domestic and imported products into different groups, nor did it involve negotiations. Different specifications and models under the same registration certificate were treated as a single procurement unit. Ultimately, the average price reduction for winning domestic bids was 92%, while that for imported products was 95%. Following the conclusion of the bidding process, the average price of coronary stents dropped directly from RMB 13,000 to approximately RMB 700. The stock prices of numerous listed medical device companies fell sharply in response, entering a prolonged downward trend lasting several months.

Unlike pharmaceuticals, high-value medical consumables have virtually no market in outpatient pharmacies, with public hospitals accounting for the vast majority of market share. The first round of national centralized procurement for coronary stents included 80% of the national volume as intended procurement quantities. Therefore, whether a consumables manufacturer wins bids in the national centralized procurement will have a decisive impact on its financial performance. To increase their win rates, bidding companies have submitted drastically reduced prices.

Previously, the head of the Department of Pharmaceutical Price and Procurement Bidding at the National Healthcare Security Administration stated in an interview that the administration had discussed and established selection criteria for the national centralized procurement of medical consumables. The basic requirements include a high degree of domestic production, large annual absolute procurement volume, a broad range of eligible manufacturers, and relatively clear product evaluation standards.

Orthopedic implant consumables represent a significant segment of the medical device industry, characterized by a large market size. With the deepening aging of the population, there is still considerable room for further growth in surgical volumes. Unlike pharmaceuticals, high-value medical consumables encompass a wide variety of categories; orthopedic products alone involve tens of thousands of specifications and models, making it difficult to establish unified quality assessments through consistency evaluations similar to those used for generic drugs. Therefore, the national centralized procurement rules for orthopedic products may differ significantly from the national centralized procurement policy for coronary stents. Due to the excessive number of specifications and models of orthopedic implants in the trauma and spine fields, joint implants, which have relatively fewer specifications, are currently the primary category included in provincial and municipal volume-based procurement pilots.

Currently, high-value medical consumables, represented by orthopedic medical devices, are generally subject to centralized volume-based procurement (VBP) tenders organized at the provincial level, with some regions conducting such tenders at the prefecture-level city level. To date, several regions, including Jiangsu, Anhui, Fujian, Zhejiang, Hunan, Shandong, Qinghai, Qiannan Prefecture in Guizhou Province, and Qujing City in Yunnan Province, have implemented pilot VBP programs for certain orthopedic medical device products (primarily joint implants). According to information released by these pilot regions, the average price reduction for orthopedic medical devices within the scope of volume-based procurement has been approximately 50–80%.

In January 2020, the General Office of the National Health Commission issued the “Notice on Printing and Distributing the First Batch of Key Governance Lists for High-Value Medical Consumables,” which listed 18 types of high-value medical consumables as the first batch of key governance targets, including intervertebral fixation/replacement systems, bone shavers, hip joint prostheses, and single/multi-component metal bone fixation instruments and accessories.

On November 20, 2020, the Center for Guidance on Drug Pricing and Procurement of the National Healthcare Security Administration issued the “Notice on Carrying Out Rapid Data Collection and Price Monitoring for the Second Batch of Centralized Procurement of High-Value Medical Consumables” (No. 26 [2020] of the Letter from the Center for Drug Pricing and Procurement), which explicitly stated that the categories mainly included in the list of medical consumables for the second batch are artificial hip joints, artificial knee joints, orthopedic materials, defibrillators, occluders, and staplers.

In early March 2021, in accordance with the “Notice on Carrying Out the Reporting of Hospital Procurement Data for Certain High-Value Medical Consumables” (No. 7 [2021] of the National Healthcare Security Administration’s Center for Guidance on Drug Pricing and Centralized Procurement), the reporting of procurement data for high-value consumables in the categories of artificial joints, spine, and trauma officially commenced. The defibrillators, occluders, and staplers mentioned above were not yet included in the scope of reporting. Consequently, the industry believes that orthopedic consumables are highly likely to be partially or fully included in the national centralized procurement program in 2021.

On March 4, 2021, the Sichuan Provincial Healthcare Security Administration released a policy interpretation of the “Implementation Plan for Centralized Procurement of Medical Consumables by Medical Institutions in Sichuan Province,” specifically noting that all in vitro diagnostic (IVD) reagents, except for cleaning solutions, were included in the scope of this centralized procurement. Previously, the IVD industry was considered unlikely to be impacted by volume-based procurement in the short term, due to the prevalence of closed systems where many reagents and instruments must be used together.

National Centralized Procurement of High-Value Consumables Will Have a Significant Impact on All Segments of the Medical Device Industry

In the second half of 2020, the centralized procurement of coronary stents sent the stock prices of industry leaders Lepu Medical and MicroPort on a roller-coaster ride. By year-end, rumors of centralized procurement for orthopedic implants began to circulate, causing major players such as Double Medical, Kylin Medical, Chunli Medical, and AK Medical to experience sharp declines in their stock prices and significant reductions in institutional holdings. The market’s primary concern was that national centralized procurement for orthopedics would repeat the fate of coronary stents, whose end-user prices were slashed by 90%, severely impacting corporate performance.

Orthopedic consumables have historically been a major hotspot for kickbacks within the medical device industry, with distribution channels accounting for nearly 80% of the final product price. In its prospectus submitted to the Shanghai STAR Market (version dated February 19, 2021) and in its response to the second round of audit inquiries, Weigao Orthopaedics provided a relatively direct answer regarding the potential impact of volume-based procurement on orthopedic manufacturers: “If the reduction in the ex-factory price of relevant products does not exceed 80%, the winning bid price will not approach or fall below the company’s production costs.” In the short term, compared with manufacturers, it is undoubtedly distributors that are first pushed to the brink of survival by centralized procurement.

At this point, all manufacturers in the industry must face up to the major trend of centralized procurement and make preparations in advance:

1) Homogeneous products that rely on sales-driven strategies and face intense competition will inevitably hit “rock-bottom prices” following volume-based procurement (VBP). Failure to win bids will result in loss of market share, while winning bids at unsustainably low prices is akin to quenching thirst with poison. Companies that secure bids must strictly control production costs and optimize distribution services, transforming this segment into a high-volume, low-margin cash flow business for the company;

2) Overseas markets have become a significant source of profits, making market entry abroad increasingly critical;

3) Product innovation has become the only viable path to success for future medical device and consumable companies.

Registration and Approval System Drives Innovation in Medical Device Products

In 2020, regarding registration and approval, in addition to the emergency approval of medical devices for epidemic prevention and control conducted by the National Medical Products Administration (NMPA) under the pandemic circumstances as previously mentioned, a total of 26 innovative medical device products were approved for market launch in China. The most notable among these was the approval of Class III AI medical device certifications for several artificial intelligence medical device companies, including Keya Medical, Shukun Technology, and Deepwise Medical, marking the dawn of a new era for product commercialization by AI medical device enterprises that had previously been in a period of stagnation.

Benefiting from regulatory breakthroughs that addressed the industry-wide challenge of obtaining Class III medical device approvals, the AI medical device sector once again attracted significant capital attention in 2020, with multiple AI medical device companies completing several rounds of financing throughout the year. Beijing Keya Ark, which received China’s first Class III certification for an AI medical device, filed its application for listing on the Main Board of the Hong Kong Stock Exchange on the evening of March 16, 2021.

The STAR Market and the Hong Kong Stock Exchange Will Welcome Medical Device Companies with a More Open Stance

The highly anticipated Shanghai STAR Market has created a series of wealth-creation myths since its launch, but there have also been cases of subsequent weakness and stock prices halving. Unlike new drug R&D companies, the STAR Market has not yet seen medical device companies listed under the fifth set of criteria.

Therefore, since the second half of 2019, numerous medical device companies have chosen to list on the Hong Kong Stock Exchange (HKEX) under its new listing standards. These include Venus Medtech, the first unprofitable medical device company to go public under these new rules, followed by Peijia Medical and Kangji Medical, among others. While companies determine their optimal listing venue by comprehensively evaluating factors such as place of incorporation, capital structure, shareholder background, market valuation benchmarks, liquidity levels, and needs for IPO and subsequent financing, it is undeniable that in the coming years, both China’s A-share market and the Hong Kong stock market will embrace the listings of more medical device enterprises with greater openness.

In recent years, new medical technologies have continued to emerge. Against the backdrop of the 2020 digitalization strategy compounded by the COVID-19 pandemic, the application of new technologies such as artificial intelligence, robotics, single-cell sequencing, and CRISPR in diagnosis and treatment has begun to show signs of commercialization. These new technologies are of great significance for disease prevention, prediction, diagnosis, treatment, and prognosis, and will profoundly influence the development direction of medical devices and diagnostics.

Artificial Intelligence Technology

Artificial intelligence technology serves as a powerful complement to traditional medical diagnosis and treatment, assisting physicians in providing second opinions and formulating personalized treatment plans. In May 2019, the National Medical Products Administration launched the Action Plan for Regulatory Science of Drugs in China, designating artificial intelligence medical devices as one of the first nine key research projects.

Currently, the most widely applied area of artificial intelligence technology in the medical device industry is imaging + AI. Products from industry players such as Tuma Shenwei, Infervision, Deepwise Medical, and Huiyi Huiying have matured, with multiple registration certificates already issued in this field.

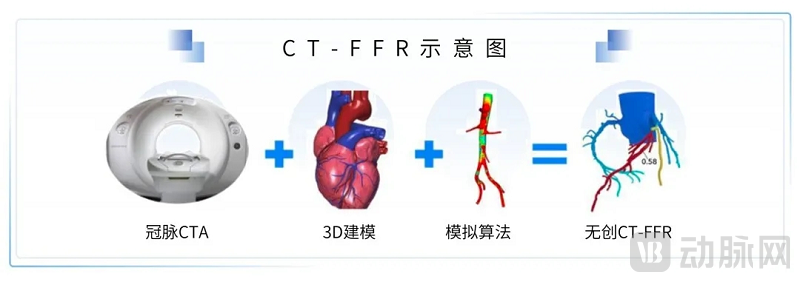

In the field of cardiovascular and cerebrovascular diseases, imaging-based Fractional Flow Reserve (FFR) measurement leverages technologies such as artificial intelligence and computational fluid dynamics algorithms. This approach not only assesses the anatomical severity of coronary artery stenosis but also enables functional evaluation of the coronary arteries, representing one of the most advanced applications of AI technology to date. Based on different FFR measurement methodologies, imaging-based FFR primarily includes CT-FFR (FFR derived from coronary computed tomography), FFR-Angio (FFR derived from coronary angiography), and FFR-IVUS/OCT (FFR derived from intravascular ultrasound and optical coherence tomography). The combined application of these cutting-edge technologies with conventional invasive FFR measurement techniques allows hospitals and physicians to provide personalized diagnostic plans and more precise diagnostic results for individual patients, thereby establishing a gold standard for value-based healthcare. Keya Medical’s DeepVessel FFR® is the first non-invasive coronary functional assessment product in China fully based on artificial intelligence deep neural networks. Pulse Medical’s QFR, based on coronary angiography, is the world’s first wire-free FFR system.

The application of artificial intelligence (AI) in the field of in vitro diagnostics (IVD) has become widespread, particularly facilitating multiple stages in multi-analyte testing, such as model optimization and validation during product development, as well as data analysis and integration in commercial applications. In recent years, AI has also demonstrated its capacity to integrate multi-omics information, thereby supporting precision diagnosis and treatment. Exact Sciences, a leading enterprise in early colorectal cancer screening, leverages AI to organically combine various methodologies in its flagship product, Cologuard®. This test qualitatively detects DNA markers associated with colorectal neoplasia and fecal occult hemoglobin, generating a composite score for colorectal cancer screening. Currently, WuXi Diagnostics is a pioneering company in China that utilizes AI to integrate multi-omics data. The company has developed integrated diagnostic products for complex and difficult-to-diagnose diseases, including biliary atresia in children and Alzheimer’s disease.

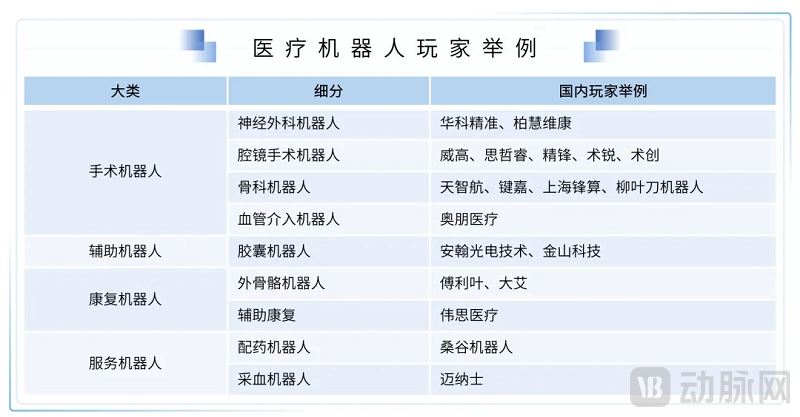

Robotics

The clinical applications of robotics are expanding, encompassing not only intraoperative settings such as cardiovascular surgery, orthopedics, and obstetrics and gynecology, but also in-hospital scenarios like medication dispensing and sterilization, as well as out-of-hospital contexts including home care and postoperative rehabilitation. Correspondingly, medical robots can be categorized into several subtypes, such as assistive robots, surgical robots, and rehabilitation robots.

Surgical robots are undoubtedly the most high-profile category in robotics. They enhance the precision and safety of surgical procedures, while also reducing surgeon fatigue during prolonged operations and minimizing frequent radiation exposure for medical staff. In the future, surgical robots will become a critical high-end assistive technology in surgical practice. Since receiving FDA approval for market launch in 2000, the da Vinci Surgical System had installed 5,582 units worldwide by the end of 2019, generating nearly $4.5 billion in revenue, which fully validates the substantial market potential for surgical robots.

Globally, the United States was the earliest to deploy surgical robots and currently has the most comprehensive coverage across all sub-sectors, essentially monopolizing the markets for laparoscopic and vascular interventional surgical robots. Products have also successively emerged from Israel, Japan, and certain European countries. The orthopedic surgical robot market currently features numerous players, with major industry giants actively entering the space, including Medtronic’s Mazor spinal surgical robot, Stryker’s MAKO joint surgical robot, and Zimmer Biomet’s MedTech spinal surgical robot.

Although the development of surgical robots in China started relatively late, it has progressed rapidly in recent years due to policy support and technological breakthroughs. Notable players have emerged in various niche sectors, such as Tinavi Medical Technologies, the first publicly listed surgical robot company in China, which specializes in spine and trauma surgery robots.

Leveraging the development of 5G technology, surgical robots will become a critical platform for enabling remote surgery. In January 2019, Sizrui, in collaboration with Huawei and Mengchao Hepatobiliary Hospital of Fujian Medical University, conducted the world’s first remote surgical animal experiment using 5G technology. In March of the same year, China Mobile, together with Huawei and the Chinese PLA General Hospital, successfully performed China’s first 5G-based remote human surgery—the implantation of a deep brain stimulator (often referred to as a "brain pacemaker") for Parkinson’s disease. In the future, the integration of “surgical robots + 5G” will further break through limitations in surgical procedures and spatial constraints, allowing more patients to benefit from high-quality medical care.

Single-Cell Technology

Single-cell technologies are dedicated to distinguishing differences between cells. Among these, single-cell sequencing garnered significant attention from the capital market in 2020. This technology reveals the unique genetic information and gene expression profiles of individual cells, thereby enabling the differentiation of distinct cell types, and holds substantial clinical potential in the fields of oncology and immunology.

Future single-cell detection technologies will continue to evolve, with ongoing advances in multiplexed sequencing. Integrating spatial information into single-cell analysis to further elucidate the interactions between individual cells and their neighbors represents a visible new direction for single-cell technologies.

Among the top 10 innovative applications of 2020 announced by The Scientist, several products involve the innovation and application of single-cell technology. BioLegend obtained a license for CITE-seq and developed TotalSeq™-C Human Universal Cocktail v1.0. CITE-seq enables the assessment of proteins in each cell while conducting single-cell transcriptomic studies, which is of great significance for precise detection in the field of infectious diseases.

Furthermore, IsoPlexis employs its Single-Cell Intracellular Proteome solution to monitor more than 30 protein signaling pathways and the operational mechanisms of entire protein networks, thereby enabling effective assessment of the efficacy of targeted therapies, such as antibody-based treatments or small-molecule drugs.

Two products from 10X Genomics were selected. The first is the Chromium Single Cell ATAC + Gene Expression product, which is based on the ATAC-seq assay and enables the acquisition of epigenetic and gene expression data from individual cells. 10X Genomics has also launched the Visium Spatial Gene Expression Solution, advancing next-generation spatial transcriptomics technologies. This solution accurately reveals the specific locations of gene expression within tissue samples by providing whole-transcriptome data from one or several cells, capturing tens of thousands of molecular identifiers at each spot. Currently, this product is widely used in research on neurodegenerative diseases and holds significant development potential in developmental biology, oncology, and immunology.

CRISPR Technology

Since its emergence in 2012, CRISPR technology has seen continuous expansion in applications and technological optimization, with ongoing research into new indications for the treatment of genetic diseases. In July 2020, a team from the University of California, Berkeley, led by Nobel laureate Professor Jennifer Doudna, reported the discovery of an “ultra-compact” CRISPR enzyme—CasΦ (Cas12j). CasΦ is a Cas protein encoded by giant phages; it is approximately half the size of the commonly used Cas9 and Cas12a enzymes, facilitating easier entry into human and plant cells to exert its function, and enabling the targeting of a broader range of gene sequences.

During the COVID-19 pandemic, numerous products leveraging CRISPR technology for rapid SARS-CoV-2 detection have emerged. Dr. Tony Y. Hu from Tulane University School of Medicine demonstrated that pairing a fluorescence microscopy readout device with a smartphone to determine SARS-CoV-2 viral load in saliva via CRISPR-Cas12a assays is as effective as established quantitative reverse transcription polymerase chain reaction (qRT-PCR) methods. Similarly, Dr. Melanie Ott, Director of the Gladstone Institute of Virology, published findings confirming the efficacy of a detection method that combines Cas13a protein with a fluorescent reporter molecule—which emits fluorescence upon cleavage—mixed with patient samples from nasal swabs, where fluorescence is detected using a smartphone camera attached to a microscope to indicate a positive result for SARS-CoV-2. In the future, the development of CRISPR-based point-of-care testing (POCT) will be a significant highlight in the field of infectious diseases.

Over the next decade, China’s medical device industry will witness trends such as domestic substitution, independent innovation, platform-based strategies, and supply chain extension. As technology continues to advance and industry boundaries become increasingly blurred, non-traditional players—including internet giants, medical device service providers, and pharmaceutical companies—are entering the medical device sector in search of new growth opportunities.

One of the New Entrants: Internet Giants

The impact of AI technology on the medical device industry has prompted Chinese internet giants to enter the fray, with Alibaba, JD.com, Tencent, and ByteDance all making strategic moves. On one hand, they are leveraging their big data capabilities and consumer-facing platforms to build internet healthcare ecosystems, such as Alibaba Health and JD Health. On the other hand, they are increasing investments in the upstream segment of the industry chain, particularly in medical equipment, and forming strategic partnerships with traditional MedTech players.

The Second Wave of New Entrants: Professional Medical Device Service Companies

In recent years, the medical device sector has experienced robust growth. The vast majority of companies have primarily relied on organic growth, managing the entire process from identifying clinical needs and product development to market launch and establishing their own platforms for commercial sales. This model places exceptionally high demands on the R&D, operational, and commercialization capabilities of founding teams. However, with the implementation of the Medical Device Registration Holder (MAH) system, increasingly stringent regulatory oversight, and the reshaping of distribution channels by volume-based procurement (VBP), specialized service providers with high entry barriers or platform enterprises benefiting from economies of scale are poised to become standout players in the value chain. The business model of these companies focuses on accelerating and professionalizing specific segments of the value chain, thereby bringing high-quality products to clinical practice more quickly and effectively. Such enterprises include, but are not limited to, CRO/CDMO firms and platform-based specialized sales companies.

The Third Wave of New Entrants: Pharmaceutical Companies Venture into the Medical Device Sector

The landscape of traditional pharmaceutical companies is maturing, and the sector will inevitably continue to be impacted by centralized volume-based procurement (VBP). In this context, a growing number of pharmaceutical enterprises are seeking horizontal expansion into the medical device sector to diversify future revenue streams and cash flow, mitigate overall operational risks, and strengthen competitive barriers and core advantages. Collaboration models are emerging in diverse forms, including full acquisitions, equity investments, technical collaborations and licensing, as well as strategic channel partnerships. From a therapeutic perspective, synergistic pharma-device collaborations can provide patients with one-stop, closed-loop solutions that address the entire patient journey, while also generating more real-world data to support the integration of more innovative commercial insurance schemes.

Following the implementation of the "Notice on Key Tasks for Deepening Medical and Healthcare System Reform in the Second Half of 2020" issued by the General Office of the State Council in October 2020, national centralized volume-based procurement (VBP) has expanded from pharmaceuticals to high-value medical consumables. The national pilot program for volume-based procurement of medical consumables covers 17 product categories, primarily belonging to cardiovascular, orthopedic, ophthalmic, mesh, surgical consumables, and other categories. Key criteria for selecting products for volume-based procurement include a high degree of domestic production, large absolute annual procurement volumes, a broad range of eligible manufacturers, and relatively clear product evaluation standards. Only clinical products meeting these criteria are eligible for inclusion in the national VBP program. Marking the official launch of national centralized procurement, coronary stents—with a domestic production rate of 80%—saw their prices drop from over RMB 10,000 to an average of around RMB 700, representing a price reduction of more than 90%. This is projected to reduce annual expenditures by RMB 11.7 billion.

On April 1, 2021, the National Centralized Procurement Platform for Medical Consumables issued the “Notice on Carrying Out Information Collection for the Centralized Procurement of Certain High-Value Orthopedic Medical Consumables,” stating that information collection for high-value orthopedic medical consumables would be conducted in batches, with artificial hip and knee joints being included in the first batch. It is widely believed within the industry that artificial hip and knee joints will be the next category of high-value medical consumables to undergo national centralized procurement.

A significant decline in the prices of high-value medical consumables is a foreseeable trend, as device manufacturers will inevitably proactively reduce prices to gain market share. Against this backdrop, with a limited number of winning bidders, market concentration has increased, posing a risk of marginalization for non-winning enterprises and leading to an industry reshuffle. Meanwhile, volume-based procurement presents certain development opportunities for companies within the industry:

Conducive to the Development of Large-Scale CSOs

A major reason for the artificially high prices of high-value medical consumables has long been the multi-tiered agency sales model, which involves markups at each level. Following the implementation of volume-based procurement (VBP), the “two-invoice system” will be enforced, significantly squeezing profit margins in the distribution chain. This will directly eliminate a cohort of distributors that lack both upstream product advantages and downstream direct access to end-user institutions. However, against the backdrop of exchanging price reductions for increased volume, manufacturers cannot fully transition to direct sales and must still collaborate with agents. Consequently, large-scale Contract Sales Organizations (CSOs) that possess extensive terminal resources across China and can provide services at reasonable prices will usher in a new era of industry growth.

Conducive to the development of enterprises with strong product innovation capabilities and diverse product portfolios.

To respond to volume-based procurement (VBP) of medical consumables, manufacturers will formulate corresponding strategies based on the different stages of each product’s life cycle to maximize the value of their entire product portfolio. For instance, products that have been on the market for many years and have become basic models are well-suited for inclusion in VBP, securing hospital access through lower gross margins. In contrast, new products are better positioned to target the high-end market, achieving higher gross margins and profits. Meanwhile, funds saved through VBP will be directed by the state toward encouraging innovation. Companies with independent R&D capabilities and a diverse, well-tiered product portfolio are expected to increase their market share and maintain stronger financial performance during the implementation of VBP.

Against this backdrop, medical consumables companies with a single-product portfolio face a higher risk of disruption, whereas platform enterprises with comprehensive product lines and strong innovation capabilities are poised to enter a fast track for corporate growth, driven by policy support.

Conducive to the development of enterprises with overseas expansion capabilities

As China advances its volume-based procurement (VBP) program for medical consumables, the uncertainty surrounding manufacturers’ bid success and post-award profit margins has led investment institutions to focus on consumable companies with global expansion capabilities. International sales offer the following advantages: First, diversified revenue streams. Before the implementation of VBP, companies generating revenue from both domestic and international markets enjoyed broader market access and easier revenue scaling. Second, risk mitigation. Companies relying solely on domestic sales face significant operational risks if they fail to win bids in VBP programs; such firms must seek new growth drivers through developing new products or distributing products from winning bidders, which entails considerable risk. Third, economies of scale. Companies with sales capabilities in both domestic and international markets can leverage economies of scale in production, reducing per-unit costs. This helps maintain a competitive edge in VBP bidding and increases the likelihood of winning contracts.

In summary, when evaluating manufacturers of high-value medical consumables that are likely to be included in volume-based procurement (VBP) programs in the near term, financial investors should comprehensively assess factors such as cost control for mature products, potential for overseas market entry, and the capability to deliver innovative products. Strategic investors, meanwhile, may consider aspects such as product portfolios, distribution channels, and supply chain integration. It is foreseeable that the range of products subject to national-level VBP will continue to expand in the short term; therefore, investors should maintain a cautiously optimistic attitude when investing in such products.

While volume-based procurement (VBP) has driven down the prices of cardiovascular and orthopedic implant consumables to rock-bottom levels, the industry widely believes this will accelerate the R&D and commercialization of innovative diagnostic and therapeutic products. The advancement of VBP has increased hospitals’ willingness to adopt diagnostic products, facilitating precise diagnosis and helping to avoid over-treatment. Currently, coronary stents have already been included in the national centralized procurement program, while many provinces and municipalities have launched provincial-level VBP for orthopedic consumables, with national centralized procurement imminent. We believe that precision diagnostic and therapeutic products in these two sectors are poised to enter a period of significant growth dividends.

Equipment, Software, and Related Consumables for PCI Diagnosis and Procedural Guidance

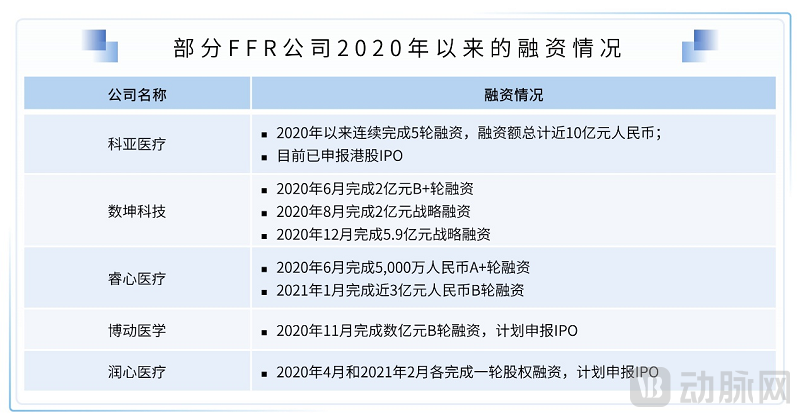

Impacted by the volume-based procurement (VBP) policy, capital has shifted its focus to cardiovascular interventional products excluded from the VBP catalog. A notable example is the consumables associated with fractional flow reserve (FFR), a diagnostic method that more accurately determines whether patients require stent implantation. Since 2020, and particularly in the second half of that year, FFR companies have secured financing frequently. The table below summarizes the funding activities of selected companies since 2020.

In recent years, the concept of precision diagnosis and treatment has been gradually implemented in orthopedics. With the implementation of volume-based procurement policies, the demand for precision diagnosis and treatment in orthopedics will further increase. Computer-assisted technologies, represented by orthopedic surgical robots, have played a significant auxiliary role in preoperative, intraoperative, and postoperative stages, enabling a more intelligent, precise, and customized surgical process. These technologies can effectively improve surgical accuracy, reduce trauma area, alleviate patient pain, and extend the service life of implanted prostheses, thereby greatly enhancing the efficiency of medical resource utilization. In this context, in addition to international and domestic orthopedic giants actively laying out surgical robots, many start-ups have also entered this field. Intelligent orthopedic robots will usher in a window period for development in the next five years.

The STAR Market is designed to serve technological innovation enterprises that are not yet mature but possess innovative capabilities and growth potential. As a technology-intensive and technology-driven sector, the medical device industry involves multiple high-tech fields such as biomedicine and information technology, making it one of the key industries recommended for listing on the STAR Market under its listing recommendation guidelines. As of April 18, 2021, a total of 262 companies had been listed on the STAR Market, including 55 healthcare companies. Among these, 28 were medical device and in vitro diagnostics (IVD) companies, accounting for 50.91% of the healthcare companies. The specific list is as follows:

Since the STAR Market launched its fifth listing standard in June 2019 (requiring an estimated market capitalization of no less than RMB 4 billion, with core businesses or products approved by relevant national authorities, substantial market potential, and demonstrated phased achievements; pharmaceutical companies must have at least one core product approved for Phase II clinical trials, while other enterprises aligned with the STAR Market’s positioning must possess distinct technological advantages and meet corresponding criteria), innovative drug developers that previously failed to meet rigid profitability and revenue thresholds entered a golden era of financing. However, over the past nearly two years, no innovative medical device company has applied this standard for its IPO filing.

Tianzhihang, the company closest to meeting the fifth set of listing standards, convened board meetings and an extraordinary general shareholders’ meeting on January 4 and 19, 2020, respectively. It revised its chosen listing criterion to the second set, which requires a projected market capitalization of no less than RMB 1.5 billion, annual revenue of no less than RMB 200 million in the most recent year, and cumulative R&D expenditure accounting for no less than 15% of cumulative operating revenue over the past three years. The company successfully went public under this second criterion, indicating that the fifth set of standards has not yet been fully opened to medical device companies. With strong national support for innovative medical devices, primary market investors have increasingly anticipated that the fifth set of STAR Market listing standards will be extended to innovative medical device companies.

Since the launch of the STAR Market, we have observed increasingly stringent requirements for enterprises’ scientific and technological (S&T) innovation attributes. In March 2020, based on a review of prior examination experience, the China Securities Regulatory Commission (CSRC) issued the Guidelines for Evaluating S&T Innovation Attributes (Trial), which established a “3+5” evaluation indicator system. This system comprehensively assesses enterprises’ S&T innovation attributes by focusing on three aspects—R&D investment, invention patents, and revenue growth—as well as five specific scenarios demonstrating exceptional S&T innovation capabilities. On April 16, 2021, the CSRC revised the Guidelines, changing the framework from “3+5” to “4+5” by adding an indicator requiring that R&D personnel account for more than 10% of the total workforce. The revision also explicitly stipulates stricter scrutiny for enterprises in sectors such as financial technology and business model innovation, while prohibiting real estate enterprises and financial investment firms from listing on the STAR Market.

We believe that the Fifth Set of Listing Standards, the Guidelines for Evaluating Sci-Tech Innovation Attributes, and their related revisions can actively promote the development of innovative medical devices, enabling device companies with genuine core technologies and R&D capabilities to achieve rapid growth driven by capital.

In the Hong Kong IPO market during the same period, the historical perception of low valuations and poor liquidity has been gradually reversed among listed innovative medical device companies. Innovative medical device enterprises with high technical barriers, leading product development progress, and clear leadership in their respective niche sectors have been highly sought after in Hong Kong. Their valuation levels are no lower than those on the STAR Market, delivering substantial returns to investors.

As can be seen, since Kangdelai Medical Devices and Venus Medtech successfully listed on the Hong Kong Stock Exchange (HKEX) at the end of 2019, several companies have successfully completed their HKEX listings in both 2020 and 2021. In just the first quarter of 2021, three companies went public, suggesting that more enterprises are expected to pursue initial public offerings (IPOs) on the HKEX. It is understood that while the criteria under Listing Rule 18A.05(5) remain unclear, more companies will opt to list on the HKEX first.

As expected, exit channels for innovative medical device companies on the STAR Market and the Hong Kong Stock Exchange will remain smooth in 2021, significantly boosting investment and financing activity across the innovative medical device sector. Companies will be able to secure ample funding to accelerate product innovation and regulatory registration, markedly enhancing their risk resilience and enabling strategic positioning in frontier fields. China’s innovative medical device industry is entering its “golden decade.”

The current epidemic prevention and control efforts have exposed issues such as insufficient grassroots medical personnel, relatively limited professional capabilities, and inadequate medical equipment in China, preventing the tiered diagnosis and treatment system from fully functioning. Conventional real-time fluorescent quantitative PCR can only be conducted in specialized PCR laboratories by trained professionals. Since the vast majority of grassroots hospital laboratories lack such personnel and facilities, samples must be transported to qualified laboratories. This resulted in prolonged turnaround times and insufficient testing capacity for nucleic acid detection of COVID-19 during the early stages of the outbreak. On February 8, 2020, a press conference held by the Joint Prevention and Control Mechanism of the State Council stated, “We hope that new, rapid testing methods can be deployed at the grassroots level, enabling medical institutions with fewer resources to conduct tests.” The COVID-19 pandemic has accelerated the rapid development of molecular point-of-care testing (POCT), which allows for closed-tube nucleic acid extraction and amplification, achieving on-site rapid testing with a “sample-in, result-out” workflow. During the pandemic, this technology has been widely used in grassroots clinics, emergency departments, customs checkpoints, and other settings.

Compared with other in vitro diagnostic platforms, POCT offers significant advantages, primarily including: first, effectively shortening the testing turnaround time from sample collection to reporting; second, requiring minimal space and no extensive ancillary equipment; third, imposing fewer requirements on operators, allowing non-specialist laboratory technicians or even the patients themselves to perform the tests. Based on these advantages, POCT can be applied across a wide range of testing areas, mainly including:

During the COVID-19 pandemic, the government, medical institutions at all levels, and the general public have recognized the importance of tiered diagnosis and treatment. Primary care hospitals should assume responsibilities such as routine treatment for patients with clear diagnoses and stable conditions, as well as grassroots prevention and control of infectious diseases. It is widely believed within the industry that in the post-pandemic era, the government will continue to introduce various policies to further strengthen investment in primary healthcare capabilities, improve medical equipment, and conduct professional training for personnel. These measures aim to effectively implement the tiered diagnosis and treatment system, enabling it to play a more active role in universal health coverage. Given their limited space and funding, as well as a relatively smaller patient sample size, primary healthcare institutions are better suited for the deployment of point-of-care testing (POCT) devices.

Beyond the impact of the COVID-19 pandemic, the accelerating aging of the population has led to a rising prevalence of chronic diseases among the elderly, such as diabetes and cardiovascular and cerebrovascular disorders. These conditions require long-term monitoring and regular check-ups, with primary care hospitals and home-use medical devices expected to absorb the majority of this demand, thereby further accelerating the development of the point-of-care testing (POCT) industry. We believe that, in addition to molecular POCT, biochemical POCT, coagulation POCT, and immunoassay POCT are all entering a golden period of growth. Notably, the current POCT industry faces homogeneous competition; international giants dominate the mid-to-high-end market, while domestic companies, though numerous, hold relatively low market shares. We suggest that financial investors should focus on technologically advanced enterprises capable of manufacturing high-end POCT devices or platform-based companies that cover multiple methodologies, including biochemical, molecular, and immunoassay testing.

To balance the quality and safety of IVD reagents with technological innovation in the industry, the FDA+LDT (Laboratory Developed Test, referring to in vitro diagnostic tests developed, validated, and used exclusively within a single laboratory) model has become mainstream abroad. The FDA regulates the market approval of in vitro diagnostic products under its medical device review framework, while laboratories holding Clinical Laboratory Improvement Amendments (CLIA) certificates provide innovative testing services through LDTs. Once a laboratory obtains CLIA certification, its test reports and results can be used to guide clinical diagnosis and treatment, gaining widespread recognition from patients, hospitals, and insurance companies.

China’s health regulatory authorities maintain stringent oversight of in vitro diagnostic (IVD) reagents. In 2007, the China Food and Drug Administration (CFDA) promulgated the “Administrative Measures for the Registration of In Vitro Diagnostic Reagents (Trial),” classifying items such as genetic testing, diagnosis of hereditary diseases, and drug target detection under Category III, the most stringent level of product registration management. With advances in detection technologies and clinical research, an increasing number of reagents that meet clinical disease needs have emerged and matured. However, due to the complex regulatory approval pathway, prolonged approval timelines, and the absence of clear regulations governing laboratory-developed tests (LDTs), their commercialization path remains unclear.

In March 2021, the National Medical Products Administration (NMPA) officially released the newly revised Regulations on the Supervision and Administration of Medical Devices. Article 53 stipulates that “for in vitro diagnostic (IVD) reagents for which no products of the same variety are yet marketed domestically, eligible medical institutions may, based on their clinical needs, independently develop such reagents and use them within their own facilities under the guidance of licensed physicians. Specific administrative measures shall be formulated by the drug regulatory department of the State Council in conjunction with the health administrative department of the State Council.” Prior to the issuance of the new regulations, the NMPA published a response to a deputy to the National People’s Congress (Document No. [2020] 27 of the NMPA) on its official website in November 2020, explicitly stating for the first time that “there is indeed a clinical need for monitoring using laboratory-developed tests (LDTs).” The NMPA further stated, “We believe that for IVD reagent products undergoing rapid technological advancements, pathways should be expanded to recognize laboratory capabilities, thereby allowing new technologies, methods, and items to be applied within a certain scope. This approach will not only meet the clinical demand for new technologies but also promote the development and application of innovative products.”

The industry generally views the amendment to this regulation as a relaxation of regulatory oversight over Laboratory Developed Tests (LDTs), representing a significant benefit for companies whose primary business model relies on third-party testing. However, it is worth noting that the regulation explicitly states that “in vitro diagnostic reagents for which no products of the same category have yet been marketed in China… may be used within the institution itself.” This deregulation primarily benefits enterprises whose registration processes cannot keep pace with clinical demand, encouraging the research and development of innovative, clinically needed tests using platform technologies such as Next-Generation Sequencing (NGS) and mass spectrometry. This allows these companies to generate some revenue through LDTs before obtaining marketing authorization. While the amendment to this clause shows a favorable trend for the LDT model, specific implementation details are still pending issuance by the regulatory authorities.

On a global scale, every medical device giant has become an industry leader through mergers and acquisitions (M&A). M&A cases in the medical device sector are commonplace, primarily driven by the following four reasons:

The market size and growth potential of the medical device sector are relatively limited.

Medical devices encompass a vast array of products with significantly diverse forms, ranging from basic low-value consumables such as disposable medical gloves and syringes to complex, large-scale equipment like tumor radiotherapy systems. The fragmented nature of the medical device industry means that technical expertise and market accumulation vary considerably across different niche segments, resulting in high barriers to cross-category and cross-segment expansion.

For companies that have already become giants in their respective niche sectors, the desire to expand their “market space” is even more intense. There are two ways to expand market space: one is to add new product lines, and the other is to enter new markets. However, relying solely on internal R&D to expand product lines often carries significant risks and requires a long time frame, especially when aiming to extend into niche tracks entirely different from their core domain. Similarly, when entering new markets, such as expanding sales overseas, relying exclusively on internal capabilities often results in insufficient market understanding and limited resource accumulation, ultimately leading to failure. Therefore, mergers and acquisitions (M&A) serve as a pathway for these industry giants to seek market space, break through existing bottlenecks, and achieve a second leap in growth.

Medical device technologies mature rapidly, and competition can easily intensify; mergers and acquisitions can help companies establish a competitive advantage.

Unlike the development of new drugs in the pharmaceutical industry, which often takes more than a decade, medical devices feature rapid technological maturation and short product iteration cycles. This makes it easy for a large number of competitors to emerge in a short period, leading to intensified market competition. Coupled with factors such as the fragmented nature of the medical device sector and limited market size, companies that fail to further expand their market share are highly likely to become acquisition targets. In the medical device field, mergers and acquisitions (M&A) may serve as a protective shield for enterprises. By expanding market share through M&A, companies can fully leverage economies of scale, such as reducing costs through scaled production and achieving scaled sales through shared distribution channels. Through M&A, companies can quickly become leaders in niche segments, establish competitive advantages, and build sufficient barriers to entry, thereby increasing the difficulty for new entrants to capture market share.

Medical device technologies evolve rapidly; companies maintain their technological leadership through mergers and acquisitions.

The medical device industry is characterized by rapid technological updates and iterations. Due to their mature organizational structures, large enterprises often lack a sufficient sense of crisis, resulting in R&D capabilities that are frequently less robust than those of small and medium-sized enterprises (SMEs). Therefore, for large companies, acquiring innovative technology firms can mitigate internal R&D risks while maintaining technological leadership. This strategy ensures their product performance remains superior to that of competitors, thereby sustaining their market share.

Integration of Upstream and Downstream Industries to Enhance Scale Effects

Leading companies in the medical device sector can gain two key advantages by acquiring upstream and downstream entities. First, acquiring upstream suppliers helps reduce operational costs, thereby enhancing market competitiveness. Second, acquiring downstream distributors allows them to control sales channels and transform into comprehensive healthcare service providers.

Post-pandemic, we believe that mergers and acquisitions in China’s medical device industry will enter a fast track.

COVID-19 Beneficiaries Accumulate Substantial Capital, Gaining M&A Strength

During the COVID-19 pandemic, many low-value medical device companies engaged in the production of face masks and disinfectants generated substantial cash inflows, fostering a strong desire for industrial upgrading. Meanwhile, in vitro diagnostic (IVD) companies that reaped significant financial gains from nucleic acid testing sought to expand their product portfolios in pursuit of more sustainable development. Sansure Biotech, a notable beneficiary of the pandemic, was the first to take the initiative.

On May 12, 2021, Sansure Biotech (688289.SH) announced that it had reached an agreement with Zhuhai Baolian Asset Management Co., Ltd. to acquire 95.863 million shares (representing 18.63% of the total share capital) of Shanghai Kehua Bio-engineering Co., Ltd. (002022) held by Baolian Assets through a negotiated transfer. The purchase price was RMB 1.95 billion, equivalent to RMB 20.34 per share. Upon completion of this transaction, Sansure Biotech became the largest shareholder of Kehua Bio-engineering. Sansure Biotech and Kehua Bio-engineering will be able to achieve complementary advantages in areas such as technology platforms, product portfolios, distribution channels, and markets, further enhancing their disease-specific solutions and comprehensive scenario-based system solutions, thereby fully leveraging synergies.

We anticipate that more companies benefiting from the COVID-19 pandemic will achieve significant growth through mergers and acquisitions.

In recent years, the primary healthcare market has remained robust, cultivating a number of potential M&A targets.

In recent years, investor enthusiasm for the healthcare sector has remained strong. This vigor in the primary market has fueled the development of China’s medical device industry, giving rise to a large number of startups. After several years of growth, some companies have emerged as industry leaders, and the opening of the STAR Market has accelerated their IPO processes, further solidifying their leading positions. Meanwhile, other companies hold certain market shares in specific niche segments but face bottlenecks that cannot be overcome through organic growth alone. For these enterprises, breaking through development constraints via mergers with other companies, or being acquired by industry leaders to compete at a higher level, can drive further business advancement.

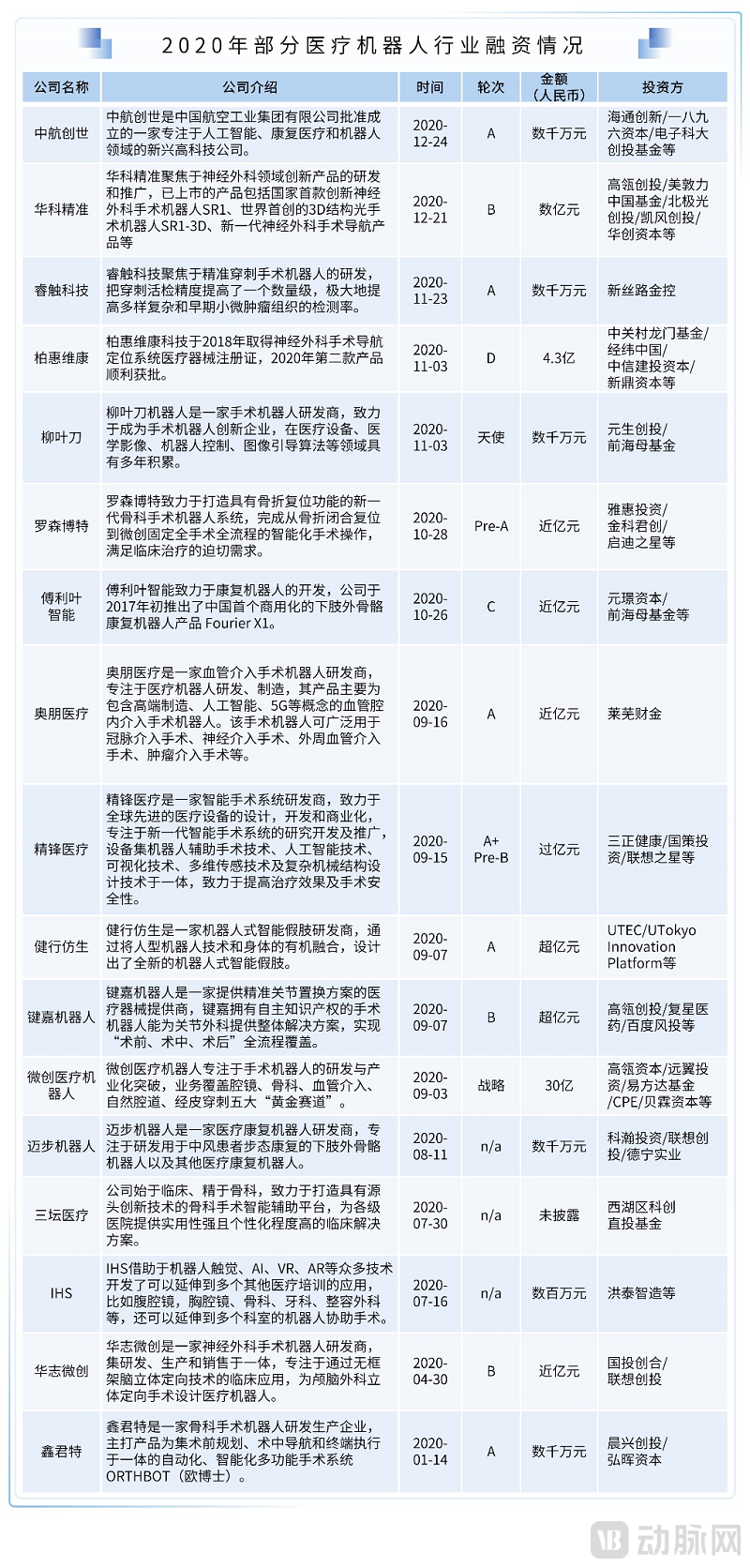

In contrast to 2019, which saw only 12 financing deals totaling RMB 131 million, the medical robotics sector emerged as a standout performer in 2020, with a cumulative 24 financing rounds and a total funding amount exceeding RMB 4.3 billion.

As the national positioning of medical robots is gradually elevated to the level of national strategy, core products from leading enterprises have successively entered the “green channel” for regulatory approval. Tinavi Medical Technologies, represented by its orthopedic navigation and positioning robots, has been listed on the STAR Market, significantly boosting investor confidence in the medical robotics sector within the primary market. In particular, laparoscopic surgical robots, as the pinnacle of minimally invasive surgery, have long been dominated globally by Intuitive Surgical. After years of dedicated technological breakthroughs, first-tier domestic companies in this field have all advanced their products into clinical trials, indicating that the first regulatory approval for a Chinese-made laparoscopic surgical robot is imminent.

Furthermore, neurosurgical navigation and positioning robots that have already received market approval, as well as orthopedic joint replacement robots, spinal navigation and positioning robots, and vascular interventional robots currently in the R&D stage, all exhibit characteristics of high barriers to entry, large market size, few competitors, and long development cycles, making them focal points for various investment institutions.

With the conclusion of the 2020 national centralized procurement of coronary stents, surgical diagnosis and treatment approaches for cardiovascular and cerebrovascular diseases—particularly comprehensive care protocols centered on percutaneous coronary intervention (PCI)—are set to shift direction in 2021, ushering in a new era. The drastic price reduction of therapeutic coronary stents to “cabbage prices” has accelerated the research, development, and commercialization of other innovative diagnostic and therapeutic products.

On one hand, the concept of “intervention without implantation” is gradually gaining clinical acceptance. Correspondingly, drug-coated balloons (DCBs), specialized balloons (including chocolate balloons, etc.), and balloon-based intravascular lithotripsy (IVL) technology are set to enter a fast track for clinical adoption. Currently, multiple companies in China have obtained National Medical Products Administration (NMPA) registration for coronary drug-coated balloon products. Among them, B. Braun Melsungen AG, a long-established German medical device manufacturer, holds the majority of the domestic market share for coronary DCBs thanks to its superior drug-coating technology and balloon performance. Other domestic manufacturers that have already received registration certificates include Lepu Medical, Shenqi Medical, Liaoning Yinyi, and Grand Pharma (Kindno). In addition, many innovative medical device companies with portfolios in vascular interventional products are actively expanding into DCBs and other vascular interventional devices. With the deepening implementation of centralized procurement for coronary stents, we anticipate that the market for drug-coated balloons and other specialized balloon products will experience a rapid ramp-up in sales volume over the next 2–3 years.

On the other hand, equipment, software, and related consumables used for PCI diagnosis and procedural guidance are gradually demonstrating their clinical application value. As is well known, diagnostic modalities for coronary heart disease (CHD) include electrocardiography (ECG), coronary angiography, coronary computed tomography angiography (CCTA), intravascular ultrasound (IVUS), and fractional flow reserve (FFR). Among these, coronary angiography has long been regarded as the “gold standard” for CHD diagnosis. Under the dual pressures of national centralized procurement and Diagnosis-Related Groups (DRGs)-based payment, cardiovascular care is shifting from a previous model that emphasized treatment over diagnosis to one focused on precise diagnosis and precision therapy. This transition will bring about significant adjustments in the profit structure, with value migrating from therapeutic products in highly competitive (“red ocean”) markets toward diagnostic products and ancillary diagnostic services with prominent clinical value. Meanwhile, these diagnostic products will substantially shorten the learning curve for junior physicians and help primary-care hospitals better perform related procedures.

High-value consumables for cardiovascular testing and diagnosis, along with innovative AI-based diagnostic methods and services—previously receiving limited attention from investors—are set to become market hotspots. These include high-value consumables for testing and diagnosis, such as IVUS catheters and OCT catheters, as well as optimized diagnostic solutions for calculating coronary fractional flow reserve (FFR) derived from pressure wires, artificial intelligence, hemodynamic models, and the aforementioned high-value consumables. In September 2020, LifeTech Scientific obtained domestic registration certificates for its pressure microcatheters and related equipment. Representing further milestones, Keya Medical and RuiXin Medical secured China’s first two Class III medical device certifications for coronary CT-FFR in January 2020 and April 2021, respectively. Benefiting from these favorable developments, Keya Medical completed multiple rounds of substantial financing in 2020 and submitted an application for listing in Hong Kong in early 2021. Such innovative products and technologies are not only applicable to the diagnosis of coronary artery disease but have also expanded to cerebrovascular diseases (including AI-assisted stroke diagnosis) and, foreseeably, to the diagnosis of structural heart diseases as well as the planning and guidance of valvular clinical procedures.

In the field of cardiology, electrophysiology (EP) technology plays a crucial role, primarily in the diagnosis and treatment of cardiac arrhythmias. Beyond conventional pharmacological management, catheter ablation (also known as EP procedures) not only controls arrhythmia symptoms and improves quality of life but also enhances prognosis by reducing the incidence of stroke, cardiovascular events, and mortality. The Chinese EP market reached nearly RMB 5 billion in 2019, maintaining a five-year compound annual growth rate (CAGR) of over 30%. Driven by population aging, an increasing number of patients with cardiac arrhythmias, and the widespread adoption and technological upgrades of EP procedural products, the market size for EP-related products is projected to approach RMB 20 billion by 2024. Currently, EP-related products, including equipment and various catheter-based consumables, constitute important business lines for multinational medical device giants such as Johnson & Johnson, Abbott, Medtronic, and Boston Scientific. The domestic market is largely monopolized by these foreign leaders, with the top three players collectively accounting for nearly 90% of the market share in China’s EP sector.

Electrophysiology products are generally categorized into three major types: mapping systems (3D/2D), mapping catheters, and radiofrequency ablation catheters. Taking Johnson & Johnson (USA) as an example, its main products in the electrophysiology field include the CARTO 3D system, star-shaped magnetic-electric dual-location mapping catheters, radiofrequency ablation catheters, and body surface reference electrodes. The research and development (R&D) of these devices and catheters requires overcoming significant technical barriers. Moreover, the overall R&D cycle is long, and the risk of failure is high; therefore, domestic companies still face numerous technical challenges in achieving product breakthroughs. During electrophysiology procedures, physicians must perform a series of complex surgical operations ranging from diagnosis to treatment. Consequently, product operability, quality stability, and device safety are critical considerations for successful commercialization. For instance, rapid modeling based on software algorithms in 3D mapping systems, as well as the comprehensive performance of radiofrequency ablation catheters regarding temperature, power, and pressure, represent technical barriers that domestic companies must continue to overcome in the future. Currently, companies in China with electrophysiology product portfolios include Huitai Medical, MicroPort EP MedTech, and Lepu Medical. Notably, the electrode catheters and radiofrequency ablation electrode catheters developed by Huitai Medical were the first domestically produced products to receive market approval. In September 2020, the company successfully passed the listing review on the STAR Market, signaling that an increasing number of outstanding domestic enterprises are exerting effort in the electrophysiology market.

Meanwhile, following the national volume-based procurement of coronary stents, physicians are increasingly seeking and mastering more innovative, cutting-edge technologies to benefit a broader population of patients with cardiovascular diseases. Although the electrophysiology market remains in its early stages of development, the long-term trend toward import substitution remains unchanged.

In recent years, as living standards have continued to improve, the demand for “aesthetic enhancement” has intensified, driving rapid expansion in the three major markets of prosthodontics, orthodontics, and dental implants. In 2020, Angelalign, the leading domestic player in clear aligner therapy, sustained robust business growth and initiated its Hong Kong stock exchange listing application, further bolstering investor confidence in the consumer-grade segment of high-value dental consumables. The vast untapped lower-tier market and significant consumption potential in China will not give rise to just one listed company; rather, first-tier enterprises in the high-value dental consumables sector are poised to attract sustained attention from the capital markets.