Who Will Emerge as the Domestic Leader in China's Minimally Invasive Surgical Device Market? Insights from Heavy Investments by Hillhouse and Qiming

What is the Evergreen Hot Topic in Medical Device Investment?

Minimally invasive surgery is undoubtedly one such field. From the perspective of the major sub-sectors of the global medical device industry, minimally invasive surgery has consistently remained one of the most prioritized niche segments for both device manufacturers and investment institutions.

As surgical procedures have transitioned from open to minimally invasive techniques, minimally invasive surgical instruments—represented by endoscopic systems, endoscopic staplers, ultrasonic scalpels, and disposable trocars—have flourished, giving rise to global giants in the field such as Johnson & Johnson and Medtronic. With the rapid advancement of minimally invasive surgery, digital surgical tools, exemplified by surgical robots, are leading the field into an era of precision and intelligence. This trend has not only spawned global unicorns like Intuitive Surgical but also made surgical robots an exceptionally hot topic in China’s medical investment circle over the past year.

Compared with domestic surgical robots, which are still striving to achieve a “zero-to-one” breakthrough, Chinese manufacturers entered the market for minimally invasive surgical instruments more than a decade ago. However, the extent of “import substitution” has lagged far behind that of the coronary stent and orthopedic industries, which started at roughly the same time. In the coronary stent sector, three leading domestic companies have emerged: MicroPort, Lepu Medical, and Jiwei Medical. Although the overall market share of domestic products in the orthopedic industry remains relatively low, it has also produced leading Chinese companies with annual sales exceeding RMB 1 billion, such as Weigao Orthopaedics, Double Medical, AK Medical, and Kindly Medical.

However, in the field of minimally invasive surgical instruments, while there are numerous domestic manufacturers holding registration certificates for endoscopic staplers and ultrasonic scalpels, no Chinese industry leader with annual revenue exceeding RMB 1 billion has yet emerged.

In the market for minimally invasive surgical instruments, long dominated by Johnson & Johnson and Medtronic, will the industry landscape undergo a transformation in the coming years? Is there an opportunity for a domestic leader with annual revenue exceeding RMB 1 billion to emerge in the near future? Top-tier investment institutions in the healthcare sector have already provided their answers.

2019, Boyu Capital, GICAnd WuXi AppTec supported Jieshi Medical’s strategic acquisition of Rich Surgical. In 2020, Hillhouse Capital successively invested in several minimally invasive surgical device companies, including Kangji Medical, Yisi Medical, and Houkai Medical; Qiming Venture Partners invested in Intuitive Conmed, which specializes in staplers, and Shengzhe Medical, which focuses on ultrasonic scalpels. In 2021, CITIC Medical Fund led the investment in Yichao Medical, a company specializing in energy-based surgical devices.VCBeat (WeChat ID: vcbeat) has found through its statistics that in the past two years, the two major sectors of important single products in the field of minimally invasive surgical instruments, namely ultrasonic scalpels and laparoscopic staplers, have attracted nearly 2 billion yuan in financing.

Recent Financing Events in the Field of Minimally Invasive Surgical Instruments

Minimally invasive surgery refers to surgical procedures performed through small incisions or natural body orifices. It is widely used in various surgical specialties, including general surgery, obstetrics and gynecology, urology, thoracic surgery, and orthopedics. Compared with traditional open surgery, which involves greater trauma, minimally invasive surgery offers reduced tissue damage, less pain, smaller scars, fewer complications, lower risk of infection, and shorter hospital stays and recovery times.

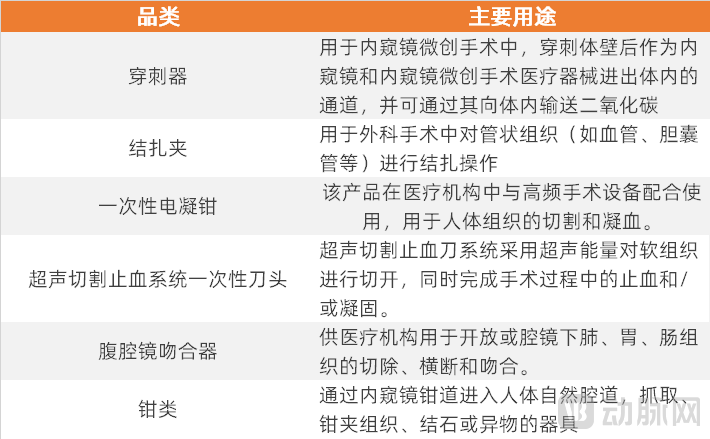

The extensive category of minimally invasive surgical instruments encompasses a wide variety of products. Accessories for minimally invasive surgical instruments mainly include: trocars, polymer and metal ligation clips, disposable electrocoagulation forceps, laparoscopic staplers, ultrasonic cutting and hemostasis systems (disposable blades and main units), as well as various grasping forceps.

# Main Instruments for Minimally Invasive Surgery

According to the prospectus of Kangji Medical,China’s market for minimally invasive surgical instruments grew from RMB 9.6 billion in 2015 to RMB 19.5 billion in 2019, representing a compound annual growth rate (CAGR) of 17.8%, and is projected to reach RMB 40.8 billion by 2024.

Among them,Endoscopic staplers and ultrasonic scalpels are the two primary categories in minimally invasive surgery.These are also the two sectors most highly valued by primary market investors. In surgical procedures, staplers are referred to as “guns,” and ultrasonic scalpels as “knives.” Based on the size and length of the devices, they are further categorized into “long guns,” “short guns,” “big knives,” and “small knives.” Ultrasonic scalpels serve the functions of tissue dissection and hemostasis, while staplers are used for tissue cutting and closure.

Why Have Ultrasonic Scalpels and Staplers Garnered the Most Attention Among These Two Major Product Categories?

Nie Honglin, Chairman of Yisi Medical, a leading domestic enterprise in minimally invasive surgical instruments, told VCBeat: “This is related to the import monopoly.”Ultrasonic surgical devices represent a niche segment dominated by a single imported brand.In the field of surgical staplers, devices are categorized into open surgical staplers and laparoscopic surgical staplers. Domestic manufacturers have already captured 60%–70% of the market share for open surgical staplers. However, in the realm of laparoscopic surgical staplers, significant challenges persist in structural design and material selection. This is because all components and functionalities must be miniaturized within a slender metal shaft, while the structure is typically subjected to mechanical forces ranging from 1,000 to 2,000 newtons.In the field of endoscopic staplers, imported brands still account for 70%-80% of the market share.”

In 2019, the market size of surgical staplers in China was approximately RMB 9.5 billion, while that of ultrasonic scalpels was around RMB 2 billion. From the perspective of market potential, the market sizes for both surgical staplers and ultrasonic scalpels are not particularly large.

In the current market, factors such as the low penetration rate of minimally invasive surgery and import monopoly are limiting the expansion of the ultrasonic scalpel and stapler markets.

On the one hand, the penetration rate of minimally invasive surgery in China remains low at present.

According to data from Kangji Medical’s prospectus, the number of minimally invasive surgical procedures performed per million population in China was only 4,248 in 2015, with a penetration rate of just 28.5%. By 2019, the number of minimally invasive surgical procedures per million people had risen to 8,514, and the penetration rate increased to 38.1%.

In developed countries such as those in Europe and the United States, minimally invasive surgery is the mainstream surgical approach. In 2019, the number of minimally invasive surgeries performed per million population and the penetration rate of minimally invasive surgery in the United States were 16,877 procedures and 80.1%, respectively.

On the other hand, the market for ultrasonic scalpels and surgical staplers is dominated by imported brands, and their high product prices have also constrained market expansion.

Taking the ultrasonic scalpel as an example,In China’s ultrasonic scalpel market, Johnson & Johnson holds a dominant position. The high prices have limited widespread adoption in hospitals, particularly for minor surgical procedures, due to cost-containment pressures. This has constrained the expansion of the ultrasonic scalpel market size. Should prices decline, there is significant potential for rapid growth in clinical procedure volume.This requires leading domestic medical device manufacturers to reduce the clinical costs of ultrasonic scalpels while ensuring product quality, thereby enabling broader adoption of ultrasonic scalpel devices in clinical surgeries.

Hillhouse Capital stated: “At present, surgical intervention remains one of the most conventional and primary modalities for cancer treatment. In China, both the incidence of cancer and the rate of treatment are rising year by year, particularly among patients with lung cancer, gastric cancer, colorectal cancer, liver cancer, and breast cancer. Minimally invasive surgery represents the future direction of surgical practice, with an increasing number of new technologies and devices being applied to minimally invasive procedures, thereby broadening their adoption and driving the field toward greater maturity.”

Meanwhile, the market size for endoscopic staplers is approximately RMB 6 billion, with domestic brands holding only a 30% market share. The current market size for ultrasonic scalpels stands at RMB 2 billion, with domestic brands accounting for merely 15% of the market. However, due to widespread off-label reuse in clinical practice, the actual market size is likely at least four to five times larger. With the implementation of policies such as strict controls on the reuse of single-use consumables, measures to curb the proportion of consumable costs, DRG payment reforms, and volume-based procurement of medical consumables, cost-effective domestic brands are poised to rapidly capture market share.

Although the current penetration rate is low, China’s minimally invasive surgical market holds immense growth potential. This growth is driven by multiple factors, including market expansion into primary care settings, policy support, and an increasing market share of domestically produced devices.

The primary growth driver is the rising penetration rate of minimally invasive surgical procedures, leading to a continuous increase in the number of surgeries performed.A major factor limiting the low penetration rate of minimally invasive surgery in China is the limited number of hospitals capable of performing such procedures. Hospitals offering minimally invasive surgical services require specific configurations, and these capabilities are largely concentrated in Grade III Class A hospitals. By the end of 2019, only 4,400 out of 23,735 hospitals in China were equipped to perform minimally invasive surgeries, including 1,400 Grade III Class A hospitals. In contrast, 71.0% of the 6,146 hospitals in the United States were capable of performing minimally invasive surgeries.

Historically, extending minimally invasive surgical services to more primary-level hospitals has been a major challenge.

Hillhouse Capital stated to VCBeat: “Currently, minimally invasive surgical procedures in China remain highly concentrated in the tertiary hospital market, with over 60% of laparoscopic surgeries performed at tertiary hospitals,”Among them, the top 200 hospitals in China for minimally invasive surgery account for more than 70% of the usage of staplers and ultrasonic scalpels in China.Compared with coronary PCI and orthopedic surgeries, both PCI and routine orthopedic procedures have become relatively decentralized, with moderate technical difficulty; more than 2,000 hospitals are capable of performing these operations. In contrast, laparoscopic surgery is primarily used for oncologic resections, resulting in a higher concentration of providers and higher hospital tiers among institutions offering such procedures. Laparoscopic instruments used by surgeons during these operations, particularly endoscopic staplers and ultrasonic scalpels, directly perform tissue cutting and suturing. Suboptimal product quality can significantly increase surgical risks; therefore, physicians maintain extremely high quality standards for laparoscopic surgical tools.

With improved patient affordability, greater physician awareness and acceptance of minimally invasive surgical procedures, and an increasing number of hospitals and physicians capable of performing such procedures, the number of minimally invasive surgical procedures per million population and the penetration rate of minimally invasive surgery in China are projected to reach 18,242 cases and 49.0%, respectively, in 2024.

The second major growth driver stems from policy initiatives, including DRGs and volume-based procurement, which will boost the market share of domestic manufacturers.

Volume-based procurement of surgical staplers has been implemented in multiple regions across China, including Shanxi, Jiangsu, Chongqing, and Hunan.

In May 2020, the proposed winning results of the joint volume-based procurement of medical consumables in Chongqing Municipality, Guizhou Province, Yunnan Province, and Henan Province were announced. Among them, 18 groups of staplers were included, with 31 products identified as proposed winners. The average price reduction reached 73.13%, with the highest reduction being 97.76%. Most of the manufacturers selected in this procurement were domestic (Chinese) manufacturers.

In May 2021, a letter issued by the Guangdong Provincial Healthcare Security Administration, titled “Letter on Jointly Conducting Provincial Alliance-Based Volume-Based Procurement of Drugs and Consumables Including Ultrasonic Scalpel Tips,” circulated within the industry. According to the document, Guangdong Province intended to take the lead in establishing a procurement alliance to jointly carry out volume-based procurement of provincial-level drugs and consumables, including ultrasonic scalpel tips.

The ongoing volume-based procurement initiatives across various regions are reducing the prices of consumable medical products, expanding their clinical penetration rates, and simultaneously driving industry consolidation, which benefits leading manufacturers with substantial operational scale and high industry rankings.

Minimally invasive surgical instruments represent one of the earliest sectors in China’s domestic substitution initiative. In the stapler segment, Chinese manufacturers entered the market more than two decades ago; however, the vast majority were small-scale enterprises focused on open surgical staplers. Due to limited capital and technological capabilities, their overall competitiveness remained weak.

Although domestic enterprises entered the market relatively early and in considerable numbers, international giants represented by Johnson & Johnson and Medtronic still firmly dominate the high-end market for minimally invasive surgical instruments to this day, cross-Domestic enterprises hold a significant share of the minimally invasive surgical instruments market, leveraging advantages such as comprehensive product portfolios, leading-edge technology, strong R&D capabilities, and long-standing industry heritage.

Why Do Many Domestic Manufacturers Struggle to Achieve a Major Breakthrough in Market Share in the Minimally Invasive Surgery Market?

An industry insider pointed out, “There are quite a few manufacturers that have obtained certification for domestically produced laparoscopic staplers and ultrasonic scalpels, with many having done so over a decade ago. However, product quality varies significantly, and only a few truly approach the standards of multinational corporations (MNCs). Only those products whose quality genuinely rivals that of MNCs and gains clinical acceptance and adoption can secure a certain market share in top-tier tertiary hospitals—particularly in complex laparoscopic procedures—thereby building positive user experience and reputation, which in turn drives further expansion into more hospitals. If domestic products suffer from poor quality and are limited to use in non-tertiary hospitals or simple surgeries, their market share will inevitably remain low.”

How Can Domestically Produced Products Break Through? Embracing Change and Innovation Is the Way Forward.

For domestic companies to break through, they first need robust quality control and production systems. By continuously improving and enhancing product quality, and steadily catching up with and approaching the quality standards of multinational corporations (MNCs), they can instill confidence in physicians to use their products in complex surgical procedures.

Nie Honglin, Chairman of Yisi Medical, stated: "Taking endoscopic staplers as an example, these devices play a core functional role in minimally invasive surgeries and are typically used in the surgical treatment of major diseases such as lung cancer, gastric cancer, and colorectal cancer. Any quality issues could cause severe harm to patients. Therefore, upon entering this field, our primary focus was ensuring product quality, while also achieving breakthrough innovations in core functionalities. Yisi Medical’s products have surpassed imported brands in key performance metrics. The articulation angle of our endoscopic staplers has been expanded from the international standard of 42 degrees to 60 degrees, and the operation has been optimized from two-handed to one-handed use. Previously, due to the limited articulation angles of imported products, surgeons were often forced to remove both the tumor and the entire anus during low rectal cancer surgeries. Through continuous collaboration and clinical trials with physicians, Yisi Medical’s innovative technology has provided better clinical options, enabling some patients to preserve their anus post-surgery."

Second, in terms of R&D pathways, most domestic manufacturers of staplers and ultrasonic scalpels have historically followed a strategy centered on imitation, progressing from low-level imitation to high-level imitation, and finally to incremental innovation.Generally, after Johnson & Johnson or Medtronic launches a product, domestic manufacturers can obtain regulatory approval within three to five years of starting imitation.

This model is not a sustainable path for China’s medical device industry. Domestic companies need to transform their R&D models, explore genuine independent innovation, and build true R&D capabilities, rather than remaining confined to manufacturing capacity.

Zhang Hui, founder of Intuitive Surgical’s domestic competitor in electric stapler R&D, had years of R&D experience at GE and Johnson & Johnson before starting her own venture. She stated, “Truly good products should stem from clinical needs, rooted in a deep understanding of customer requirements. Innovation should be drawn from these needs by deconstructing them and expressing them through technology—this is the logical path for research and development. Constant imitation is not sustainable; if others stop innovating, you will have no new products.”

In terms of market sales, domestic brands also need to transform their image and gain recognition from China’s top-tier (Grade 3A) hospitals. By offering professional products with robust performance, they can earn physicians’ trust and shed the perception of Chinese-made medical devices as being low-quality and low-priced.

In an interview, Zhang Hui recounted an experience from 2017, when Intco Medical took its products to the MEDICA medical device exhibition in Düsseldorf. At the time, European distributors remarked that the product did not seem to be made by Chinese manufacturers. Upon hearing this, Zhang Hui’s initial reaction was sadness, as Chinese medical devices were often perceived as low-priced and low-quality. During domestic promotion efforts, many hospitals and procurement agencies also held the belief that domestic brands could never surpass multinational corporations and that Chinese-made products should necessarily be low-priced.

The historical image of domestic brands has imposed a significant burden on high-quality Chinese manufacturers. To change this situation, local enterprises must possess strong commercialization capabilities, including high-level academic education and specialized service capabilities.

Smarter Operating Rooms: How Staplers and Ultrasonic Scalpels Are Evolving

In the field of surgical instruments, in addition to domestic substitution,Another notable trend is the wave of intelligent and automated upgrades in ultrasonic scalpels and stapler products.

First, let us examine surgical staplers. In the trend of stapler upgrades, driven by advances in new materials, big data, robotics, and artificial intelligence, surgical staplers are increasingly being optimized toward intelligence and automation. Electric surgical staplers enable standardized physician operations and consistent output through automated control, thereby reducing the learning curve for surgeons while enhancing the precision of minimally invasive surgical procedures.

The greatest clinical benefit of electric staplers is the reduction of leakage, bleeding, or fluid exudation. Traditional staplers cause shaking and traction on target tissues during firing and closure, whereas high-quality electric staplers can reduce such traction and shaking by 90%, thereby improving staple formation and reducing leakage from anastomosed organs. Compared with traditional staplers, electric staplers feature greater head stability, less vibration, and smoother firing, laying a solid foundation for the future development of intelligent staplers.

Johnson & Johnson and Medtronic have both launched powered staplers, which have gained widespread recognition in clinical applications. Currently, several Chinese-branded powered staplers have also received regulatory approval, including Intuitive Surgical’s powered circular staplers and powered endoscopic staplers; Hunan Yimaisi Medical’s single-use fully powered endoscopic staplers; Weierkaidi’s single-use powered endoscopic cutting staplers; Fenghe Medical’s single-use powered linear cutting staplers for endoscopic use; and Yisi Medical’s single-use and reusable powered staplers.

In the field of ultrasonic scalpels, intelligence is also a major trend. The entire operating room is undergoing intelligent upgrades, and as a critical surgical instrument, the ultrasonic scalpel must integrate seamlessly with numerous other products in the operating room.

In recent years, surgical robots have emerged as a novel product in operating rooms. Starting with Intuitive Surgical’s laparoscopic surgical robot, these systems have recently expanded into numerous fields, including orthopedics, cardiology, neurosurgery, and dentistry. The advent of new platforms has established a new starting point for ultrasonic scalpel products.

Robotic systems and minimally invasive surgical instruments are not mutually exclusive; robotic surgery still requires a variety of passive and active tools.Many surgical robotics companies lack the in-house capability to manufacture minimally invasive surgical instruments; for instance, Intuitive Surgical has partnered with Johnson & Johnson on surgical robots and ultrasonic scalpels.

In the future, a collaborative model between robotics companies and minimally invasive surgical device manufacturers may emerge as a beneficial partnership.

Minimally invasive surgical robot companies in China that have established portfolios across five major sectors—laparoscopy, orthopedics, vascular intervention, natural orifice, and percutaneous puncture—have also entered into partnerships with Houkai Medical, an ultrasonic scalpel manufacturer. Yichao Medical, a developer and manufacturer of ultrasonic soft tissue cutting and hemostatic devices, collaborated with “Miaoshou Robot” to complete the world’s first 5G-enabled remote surgery in 2019, and subsequently achieved successful remote surgical collaborations with “Kangduo Robot.”

Guided by a minimally invasive approach, Hillhouse has invested not only in traditional minimally invasive surgical devices but also in multiple surgical robotics companies, including MicroPort Surgical Robot, Keya Robotics, Huake Jingzhun, and Weimai Medical. In their view, the relationship between surgical robots and minimally invasive surgical devices is analogous to the investment philosophy of the internet sector.On one hand, it invests in standalone internet companies; on the other, it backs traditional enterprises that can be transformed and empowered by internet technologies. Hillhouse Capital has expressed long-term optimism about minimally invasive surgical companies capable of empowering traditional surgical instruments with robotics. Firms that can build an integrated “robotics + minimally invasive surgical instruments” model will establish higher competitive barriers than those offering standalone minimally invasive surgical instruments.

In addition to intelligence, reusable ultrasonic scalpel tips represent another major R&D trend. Yisi Medical has taken the lead in the industry by launching reusable ultrasonic scalpel tips, potentially reducing surgical costs to one-half to one-third of those associated with imported brands’ disposable ultrasonic scalpel tips.

China performs 30 million minimally invasive surgical procedures annually. As more high-end products gain regulatory approval and more companies achieve scaled sales, the domestic market for minimally invasive surgical devices is expected to give rise to two or three large-scale enterprises. However, competition in this sector is also intensifying. An increasing number of companies are entering the field, and minimally invasive surgical devices are undergoing continuous updates and iterations. The application scope of stapler products is constantly expanding, with growing specificity, which has led to rising demand for specialization in niche segments. Most local enterprises have a single-product structure; if they fail to keep pace with technological trends, they will be at a competitive disadvantage during the industry’s consolidation phase.

VCBeat has also compiled a list of promising domestic minimally invasive surgical device companies.

Yisi Medical: Dual Layout in Minimally Invasive Surgical Instruments—Ultrasonic Scalpels and Staplers

Yisi Medical has completed the research, development, and production of a range of high-value surgical consumables, including the easyEndo endoscopic stapler and the easyUS ultrasonic scalpel hemostasis system. In the highly competitive surgical instrument market—dominated by foreign brands, particularly in the endoscopic stapler segment—it has rapidly emerged as the leading domestic brand.

Ruiqi Surgical: A Minimally Invasive Surgical Instrument Platform Under Jianshi Medical

Rich Surgical specializes primarily in the field of minimally invasive surgical procedures. Its product portfolio encompasses three major series: open staplers, endoscopic staplers, and energy-based devices, providing high-quality and safe open and laparoscopic surgical instruments for general surgery, thoracic surgery, and obstetrics and gynecology procedures.

Houkai Medical: Continuous R&D of Ultrasonic Scalpel Devices

Houkai Medical is a leading domestic brand in minimally invasive surgery, with comprehensive capabilities in product development, iteration, and manufacturing, particularly in the field of energy-based surgical devices. The company boasts a domestically leading ultrasonic cutting and hemostasis system, comprising two generations of ultrasonic generator units and multiple series of ultrasonic transducers—including USE, USS, and MIC—tailored to various medical departments and clinical indications. Its products have been validated in hundreds of large hospitals across China and are currently serving over one hundred hospitals worldwide, including those in Europe and North America.

Intuitive Medical: Filling the Gap in China’s Electric Circular Stapler Market

Founded in 2015, Intuitive Surgical Innovation (Yingtu Kang) is a high-tech company dedicated to innovative surgical products, independently developing a full range of electric intelligent stapler systems. Grounded in deep insights into customer needs, Yingtu Kang Medical aspires to be the most innovative enterprise in the surgical instrument industry. The launch of its electric intelligent stapler platform not only leverages motor-driven in situ closure and firing to improve anastomosis success rates but also achieves intelligent control and real-time feedback of tissue pressure during the stapling process. Furthermore, Yingtu Kang Medical has implemented numerous improvements to traditional stapler designs based on addressing physicians’ actual clinical needs. For instance, when using laparoscopic staplers in hard-to-reach areas such as the pelvic floor during low anterior resection (LAR) surgery, the novel 55-degree articulating head design, combined with a shorter joint length, effectively meets surgeons’ requirements for performing deep pelvic cutting and anastomosis.